Key Insights

The global display paper box market is poised for significant growth, projected to reach an estimated market size of approximately $15,000 million by 2025. This expansion is driven by an increasing demand for sustainable and visually appealing packaging solutions across various industries. The market is expected to witness a Compound Annual Growth Rate (CAGR) of around 6.5% during the forecast period of 2025-2033, underscoring its robust upward trajectory. Key growth drivers include the rising popularity of e-commerce, which necessitates attractive point-of-purchase displays for product presentation, and a growing consumer preference for eco-friendly packaging materials. The Food and Beverage industry stands as a dominant application segment, leveraging display paper boxes for promotional activities and in-store merchandising of a wide array of products. Furthermore, the Electrical and Electronic industry is increasingly adopting these packaging solutions for showcasing high-value items, while the Cosmetics and Personal Care sector utilizes them for their aesthetic appeal and brand differentiation capabilities.

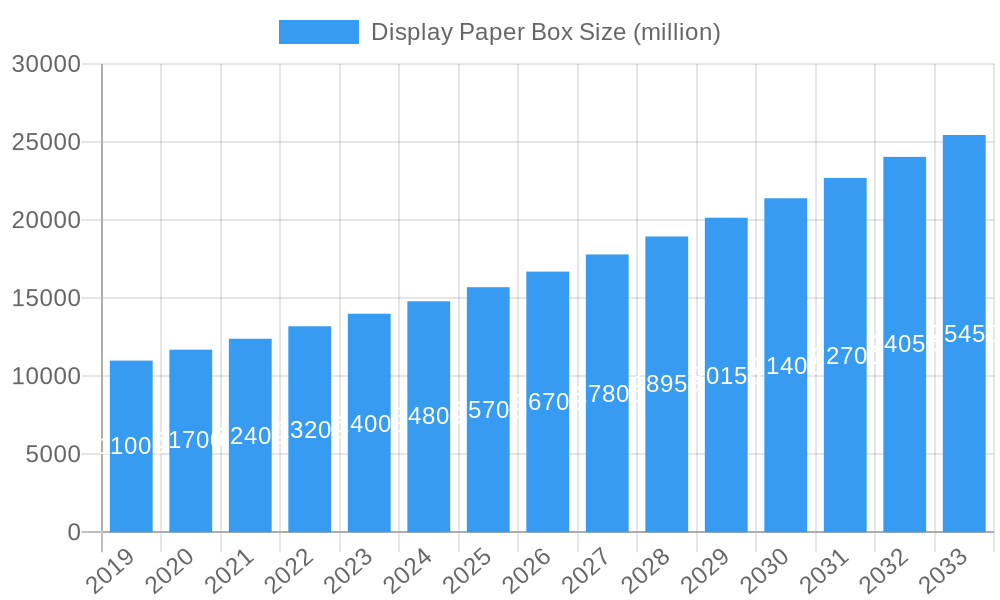

Display Paper Box Market Size (In Billion)

The market is segmented by type into Kraft Paperboard Display Paper Boxes and Corrugated Paperboard Display Paper Boxes, with both types experiencing healthy demand. Kraft paperboard boxes are favored for their eco-friendliness and durability, making them suitable for a broad range of applications. Corrugated paperboard boxes offer superior strength and protection, making them ideal for heavier items and more demanding shipping requirements. The competitive landscape is characterized by the presence of established global players such as DS Smith, International Paper, Smurfit Kappa Group, and WestRock, alongside emerging regional manufacturers. These companies are focusing on innovation, product customization, and sustainable manufacturing practices to gain a competitive edge. Restraints, such as fluctuating raw material prices and the need for specialized printing techniques, are being addressed through strategic sourcing and technological advancements. The market's future success hinges on its ability to adapt to evolving consumer demands for sustainability and visual impact in retail environments.

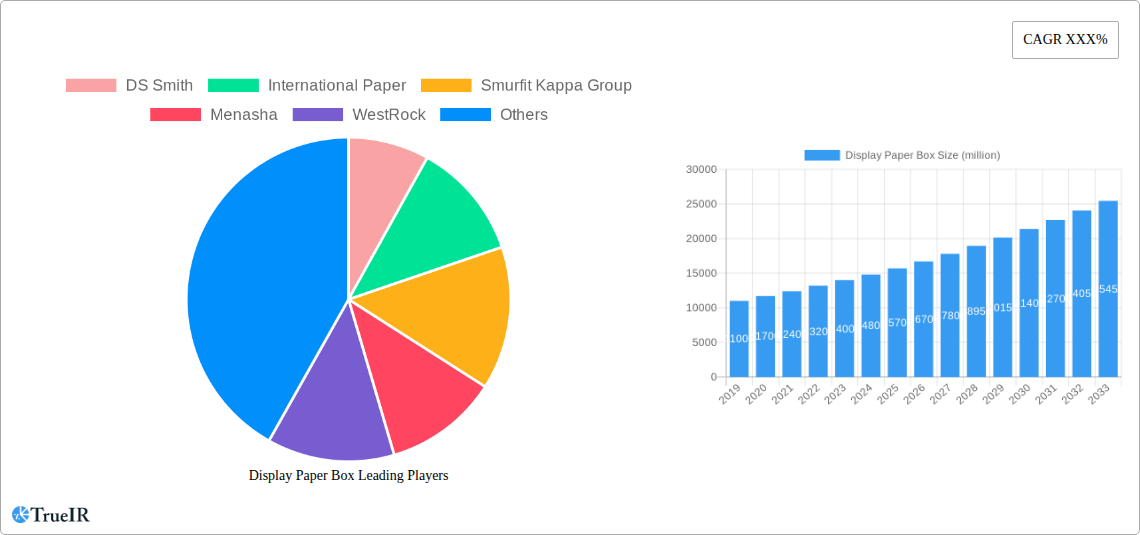

Display Paper Box Company Market Share

Display Paper Box Market Structure & Competitive Landscape

The global Display Paper Box market, valued at an estimated $XX million in 2025, exhibits a moderately concentrated structure. Key players like DS Smith, International Paper, Smurfit Kappa Group, Menasha, WestRock, and Sonoco command significant market share, driven by their extensive production capacities, robust distribution networks, and continuous product innovation. The competitive landscape is characterized by a dynamic interplay of established multinational corporations and emerging regional manufacturers, particularly in Asia. Innovation drivers are primarily focused on sustainable materials, enhanced printing technologies for brand visibility, and structural designs that optimize product display and transit protection. Regulatory impacts, primarily concerning environmental sustainability and packaging waste, are increasingly influencing material choices and manufacturing processes. Product substitutes, such as plastic displays or wooden crates, face growing consumer and regulatory pressure due to their environmental footprint. End-user segmentation reveals strong demand from the Food and Beverage Industry, Electrical and Electronic Industry, and Cosmetics and Personal Care Industry, each with distinct packaging requirements. Mergers and acquisitions (M&A) have been a significant trend, with an estimated XX million in M&A deal volume over the historical period, aimed at expanding market reach, acquiring new technologies, and consolidating market positions.

Display Paper Box Market Trends & Opportunities

The Display Paper Box market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately XX% from 2025 to 2033, reaching an estimated market size of $XX million by the end of the forecast period. This robust growth trajectory is underpinned by a confluence of evolving market trends and emerging opportunities. A primary trend is the escalating demand for sustainable packaging solutions. With increasing consumer awareness and stringent environmental regulations worldwide, businesses are actively seeking eco-friendly alternatives to traditional packaging materials. Display paper boxes, particularly those manufactured from recycled content and designed for recyclability, are gaining significant traction across all major application segments. This shift presents a considerable opportunity for manufacturers to invest in and promote their sustainable product offerings, thereby capturing market share and enhancing brand reputation.

Technological advancements in printing and structural design are also shaping the market landscape. High-definition printing capabilities allow for vibrant branding and intricate graphics, transforming display paper boxes into powerful marketing tools at the point of sale. Innovations in structural engineering are leading to more efficient, space-saving, and customizable display solutions that can be easily assembled and disassembled, catering to the dynamic needs of retailers and manufacturers. The e-commerce boom, while traditionally favoring shipping boxes, is now witnessing a rise in the use of attractive display paper boxes for direct-to-consumer shipments, enhancing the unboxing experience and contributing to brand loyalty. This trend opens up new avenues for online retailers to differentiate their products.

Consumer preferences are increasingly leaning towards visually appealing and convenient packaging. Display paper boxes that offer easy access to products and an attractive presentation are becoming paramount for consumer goods, especially in the Cosmetics and Personal Care Industry and the Food and Beverage Industry. Furthermore, the growing emphasis on premium product presentation in the Electrical and Electronic Industry, even for smaller devices, is driving demand for sophisticated and protective display paper boxes. The market penetration rate for corrugated paperboard display paper boxes is already high and is expected to continue its dominance due to its versatility, durability, and cost-effectiveness, while kraft paperboard display paper boxes are carving out a niche for their natural aesthetic and eco-friendly appeal.

The competitive dynamics are shifting, with companies focusing on offering customized solutions and integrated packaging services. Strategic collaborations and partnerships between packaging manufacturers and brand owners are becoming more prevalent to develop bespoke display solutions that align with specific marketing campaigns and product launches. The globalization of retail and the expansion of emerging economies also present significant growth opportunities, as more businesses adopt sophisticated retail display strategies to capture consumer attention. The ongoing digital transformation within the industry, including the adoption of AI and automation in design and production, is further optimizing efficiency and enabling faster turnaround times for customized orders, a critical factor in the fast-paced retail environment.

Dominant Markets & Segments in Display Paper Box

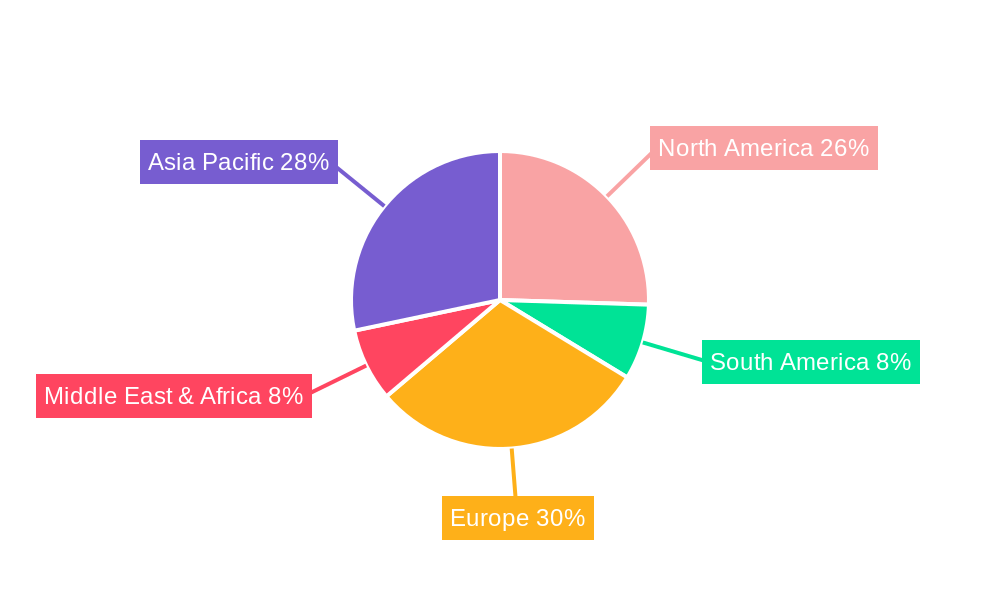

The global Display Paper Box market’s dominance is characterized by a powerful interplay between specific regions, countries, and industry segments, driven by robust demand, favorable economic conditions, and strategic industry developments.

Leading Region: Asia Pacific currently holds the dominant position in the display paper box market and is projected to maintain its leadership throughout the forecast period.

- Key Growth Drivers in Asia Pacific:

- Rapid Industrialization and Manufacturing Hubs: Countries like China, India, and Vietnam serve as global manufacturing powerhouses for a wide array of consumer goods, from electronics to apparel and food products, creating a perpetual demand for effective point-of-sale displays.

- Expanding Retail Infrastructure: The burgeoning middle class and the rapid growth of modern retail formats, including supermarkets, hypermarkets, and specialty stores, necessitate attractive in-store displays to capture consumer attention and drive sales.

- E-commerce Growth: While traditionally associated with shipping, the increasing sophistication of e-commerce logistics and the desire for enhanced unboxing experiences are leading to greater adoption of premium display packaging even for direct-to-consumer shipments within the region.

- Government Initiatives and Favorable Policies: Supportive government policies aimed at boosting manufacturing, promoting exports, and encouraging the adoption of sustainable packaging solutions further fuel the market's expansion.

- Cost-Effectiveness of Production: Lower manufacturing costs in many Asia Pacific nations allow for the production of competitive and high-volume display paper boxes.

Dominant Application Segment: The Food and Beverage Industry consistently represents the largest and most influential application segment for display paper boxes.

- Detailed Analysis of Food and Beverage Industry Dominance: The sheer volume of consumer packaged goods within the food and beverage sector, coupled with the intense competition at the retail shelf, makes attractive and functional display packaging indispensable. These boxes are crucial for product visibility, brand storytelling, and promotional activities. The demand spans a wide range of sub-segments, including snacks, beverages, confectionery, and ready-to-eat meals, all of which benefit immensely from eye-catching point-of-sale displays. Furthermore, the growing trend of impulse purchases and the emphasis on product freshness and safety reinforce the need for effective display solutions. The industry's constant introduction of new products and seasonal promotions further drives the demand for versatile and adaptable display paper boxes.

Dominant Type: Corrugated Paperboard Display Paper Box is the prevailing type, due to its inherent advantages.

- Detailed Analysis of Corrugated Paperboard Dominance: Corrugated paperboard display boxes offer an exceptional balance of strength, durability, light weight, and cost-effectiveness. Their structural integrity is vital for protecting products during transit and ensuring they remain upright and appealing on retail shelves. The corrugated structure provides excellent cushioning properties, safeguarding fragile items. Moreover, corrugated paperboard is highly versatile, allowing for intricate die-cutting and folding to create a vast array of custom shapes and designs tailored to specific product needs and branding requirements. Its excellent printability enables high-quality graphics and vibrant colors, essential for attracting consumer attention. The widespread availability of raw materials and established manufacturing processes further solidify its market dominance.

While the Electrical and Electronic Industry and Cosmetics and Personal Care Industry are also significant contributors, driven by their need for premium and protective packaging, the sheer volume and continuous demand from the Food and Beverage sector, combined with the versatile nature of Corrugated Paperboard, firmly establish them as the dominant forces in the global Display Paper Box market.

Display Paper Box Product Analysis

Display paper boxes are evolving beyond mere containment, now serving as powerful marketing tools. Innovations focus on enhancing structural integrity for better product protection during transit and at the point of sale, alongside advanced printing technologies that enable vibrant branding and intricate graphics, significantly boosting visual appeal. Competitive advantages are derived from customized designs that optimize shelf space and product visibility, along with the increasing integration of sustainable materials. The market is witnessing a rise in interactive and modular display solutions, catering to dynamic retail environments and evolving consumer engagement strategies, ensuring products stand out effectively.

Key Drivers, Barriers & Challenges in Display Paper Box

Key Drivers:

- Growing E-commerce Penetration: Increased demand for attractive packaging that enhances the unboxing experience for direct-to-consumer shipments.

- Rising Consumer Demand for Sustainable Packaging: Global push for eco-friendly, recyclable, and biodegradable packaging solutions.

- Emphasis on In-Store Branding and Merchandising: Retailers and manufacturers increasingly use display boxes to attract consumer attention and drive sales.

- Technological Advancements in Printing and Design: Improved capabilities for high-quality graphics and customizable structural designs.

- Growth of the Food and Beverage, Cosmetics, and Electronics Industries: These sectors are major end-users requiring effective display solutions.

Barriers and Challenges:

- Fluctuating Raw Material Costs: Volatility in the prices of paper pulp and related materials can impact production costs and profitability.

- Supply Chain Disruptions: Global logistics challenges and raw material availability issues can lead to production delays and increased lead times.

- Intense Competition and Price Pressures: A highly competitive market with numerous players can lead to price wars and reduced profit margins.

- Strict Environmental Regulations: Evolving and stringent regulations concerning packaging waste, recyclability, and single-use plastics can necessitate significant investment in compliant solutions.

- Development of Alternative Packaging Materials: While paperboard dominates, the ongoing development of innovative plastic or composite alternatives presents a potential challenge.

Growth Drivers in the Display Paper Box Market

The Display Paper Box market's expansion is primarily propelled by the escalating global consumer preference for sustainable and eco-friendly packaging solutions. This trend is significantly amplified by stringent governmental regulations worldwide aimed at reducing environmental impact and promoting circular economy principles. Technologically, advancements in printing capabilities, including high-resolution graphics and vibrant color reproduction, are transforming display paper boxes into powerful point-of-sale marketing tools, enhancing brand visibility and consumer engagement. Economically, the growth of retail sectors, particularly in emerging economies, coupled with increasing disposable incomes, fuels demand for attractive in-store merchandising that display paper boxes effectively provide. Furthermore, the convenience and efficiency offered by corrugated paperboard display boxes in terms of product protection, ease of assembly, and cost-effectiveness continue to be significant growth catalysts.

Challenges Impacting Display Paper Box Growth

Several factors pose challenges to the unfettered growth of the Display Paper Box market. Fluctuations in the price and availability of key raw materials, such as paper pulp, can significantly impact production costs and profit margins for manufacturers. Ongoing global supply chain disruptions, exacerbated by geopolitical events and logistical bottlenecks, can lead to extended lead times and increased operational complexities. The market also faces intense competitive pressure from a multitude of established players and emerging manufacturers, leading to price sensitivities and the need for continuous innovation to maintain market share. Furthermore, the evolving landscape of environmental regulations, while driving the shift towards sustainable paperboard, can also impose compliance costs and require significant investments in new technologies and processes, potentially hindering smaller players.

Key Players Shaping the Display Paper Box Market

- DS Smith

- International Paper

- Smurfit Kappa Group

- Menasha

- WestRock

- Sonoco

- Koch Industries

- Huizhou Cailang Printing Products

- A. Fleisig Paper Box

- Vpk Packaging Group

- NATPAK

- Shenzhen Powerful Technology

Significant Display Paper Box Industry Milestones

- 2019: Increased focus on biodegradable and compostable paperboard solutions gain traction.

- 2020: Pandemic-driven surge in e-commerce highlights the need for robust and attractive shipping/display packaging for direct-to-consumer delivery.

- 2021: Introduction of advanced UV printing technologies for enhanced graphic fidelity and durability on display boxes.

- 2022: Growing adoption of smart packaging features, such as QR codes and NFC tags, integrated into display paper boxes for consumer engagement and traceability.

- 2023: Significant investment in automation and AI for optimized structural design and rapid prototyping of display solutions.

- 2024: Emergence of modular and reconfigurable display paper box designs to adapt to changing retail footprints and seasonal promotions.

Future Outlook for Display Paper Box Market

The future outlook for the Display Paper Box market is exceptionally promising, driven by a strong convergence of sustainability imperatives and evolving retail strategies. The persistent global shift towards eco-conscious consumerism and increasingly stringent environmental regulations will continue to propel the demand for recyclable and renewable paperboard-based display solutions. Technological advancements in material science and digital printing will unlock new possibilities for customized, visually compelling, and even interactive display designs that enhance brand storytelling and consumer engagement at the point of purchase. The ongoing expansion of the e-commerce sector, coupled with a desire for premium unboxing experiences, will also create new avenues for innovative display paper box applications beyond traditional retail environments. Strategic collaborations between packaging manufacturers and brands, focusing on delivering holistic merchandising solutions, will further shape market dynamics, ensuring a robust growth trajectory for years to come.

Display Paper Box Segmentation

-

1. Application

- 1.1. Food and Beverage Industry

- 1.2. Electrical and Electronic Industry

- 1.3. Cosmetics and Personal Care Industry

- 1.4. Others

-

2. Type

- 2.1. Kraft Paperboard Display Paper Box

- 2.2. Corrugated Paperboard Display Paper Box

Display Paper Box Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Display Paper Box Regional Market Share

Geographic Coverage of Display Paper Box

Display Paper Box REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food and Beverage Industry

- 5.1.2. Electrical and Electronic Industry

- 5.1.3. Cosmetics and Personal Care Industry

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Kraft Paperboard Display Paper Box

- 5.2.2. Corrugated Paperboard Display Paper Box

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Display Paper Box Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food and Beverage Industry

- 6.1.2. Electrical and Electronic Industry

- 6.1.3. Cosmetics and Personal Care Industry

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Kraft Paperboard Display Paper Box

- 6.2.2. Corrugated Paperboard Display Paper Box

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Display Paper Box Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food and Beverage Industry

- 7.1.2. Electrical and Electronic Industry

- 7.1.3. Cosmetics and Personal Care Industry

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Kraft Paperboard Display Paper Box

- 7.2.2. Corrugated Paperboard Display Paper Box

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Display Paper Box Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food and Beverage Industry

- 8.1.2. Electrical and Electronic Industry

- 8.1.3. Cosmetics and Personal Care Industry

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Kraft Paperboard Display Paper Box

- 8.2.2. Corrugated Paperboard Display Paper Box

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Display Paper Box Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food and Beverage Industry

- 9.1.2. Electrical and Electronic Industry

- 9.1.3. Cosmetics and Personal Care Industry

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Kraft Paperboard Display Paper Box

- 9.2.2. Corrugated Paperboard Display Paper Box

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Display Paper Box Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food and Beverage Industry

- 10.1.2. Electrical and Electronic Industry

- 10.1.3. Cosmetics and Personal Care Industry

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Kraft Paperboard Display Paper Box

- 10.2.2. Corrugated Paperboard Display Paper Box

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Display Paper Box Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Food and Beverage Industry

- 11.1.2. Electrical and Electronic Industry

- 11.1.3. Cosmetics and Personal Care Industry

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Kraft Paperboard Display Paper Box

- 11.2.2. Corrugated Paperboard Display Paper Box

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 DS Smith

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 International Paper

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Smurfit Kappa Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Menasha

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 WestRock

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Sonoco

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Koch Industries

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Huizhou Cailang Printing Products

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 A. Fleisig Paper Box

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Vpk Packaging Group

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 NATPAK

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Shenzhen Powerful Technology

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 DS Smith

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Display Paper Box Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Display Paper Box Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Display Paper Box Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Display Paper Box Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Display Paper Box Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Display Paper Box Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Display Paper Box Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Display Paper Box Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Display Paper Box Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Display Paper Box Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Display Paper Box Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Display Paper Box Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Display Paper Box Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Display Paper Box Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Display Paper Box Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Display Paper Box Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Display Paper Box Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Display Paper Box Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Display Paper Box Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Display Paper Box Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Display Paper Box Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Display Paper Box Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Display Paper Box Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Display Paper Box Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Display Paper Box Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Display Paper Box Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Display Paper Box Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Display Paper Box Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Display Paper Box Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Display Paper Box Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Display Paper Box Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Display Paper Box Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Display Paper Box Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Display Paper Box Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Display Paper Box Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Display Paper Box Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Display Paper Box Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Display Paper Box Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Display Paper Box Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Display Paper Box Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Display Paper Box Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Display Paper Box Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Display Paper Box Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Display Paper Box Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Display Paper Box Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Display Paper Box Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Display Paper Box Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Display Paper Box Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Display Paper Box Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Display Paper Box Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Display Paper Box?

The projected CAGR is approximately 5.8%.

2. Which companies are prominent players in the Display Paper Box?

Key companies in the market include DS Smith, International Paper, Smurfit Kappa Group, Menasha, WestRock, Sonoco, Koch Industries, Huizhou Cailang Printing Products, A. Fleisig Paper Box, Vpk Packaging Group, NATPAK, Shenzhen Powerful Technology.

3. What are the main segments of the Display Paper Box?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.45 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Display Paper Box," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Display Paper Box report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Display Paper Box?

To stay informed about further developments, trends, and reports in the Display Paper Box, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence