Key Insights

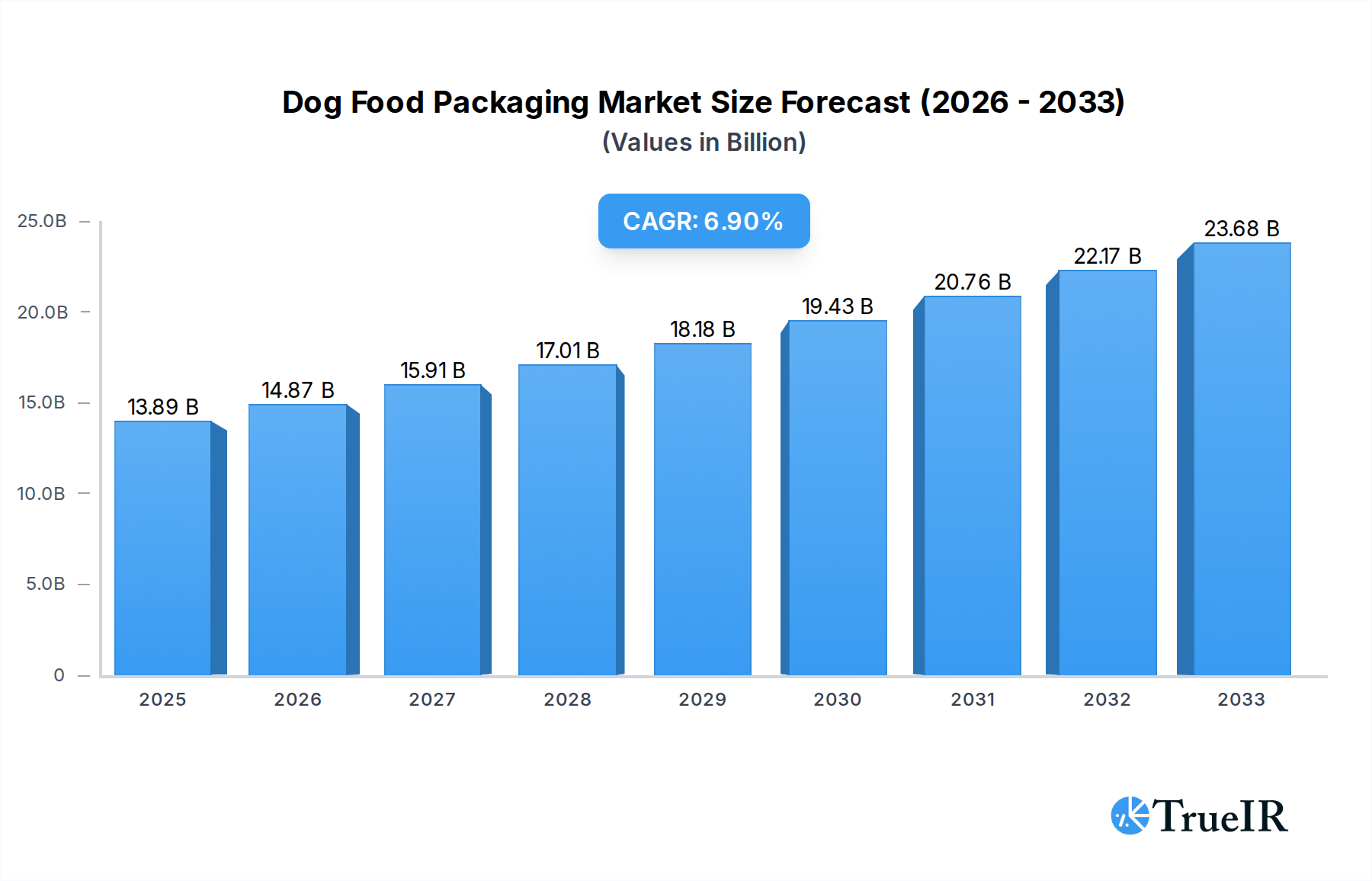

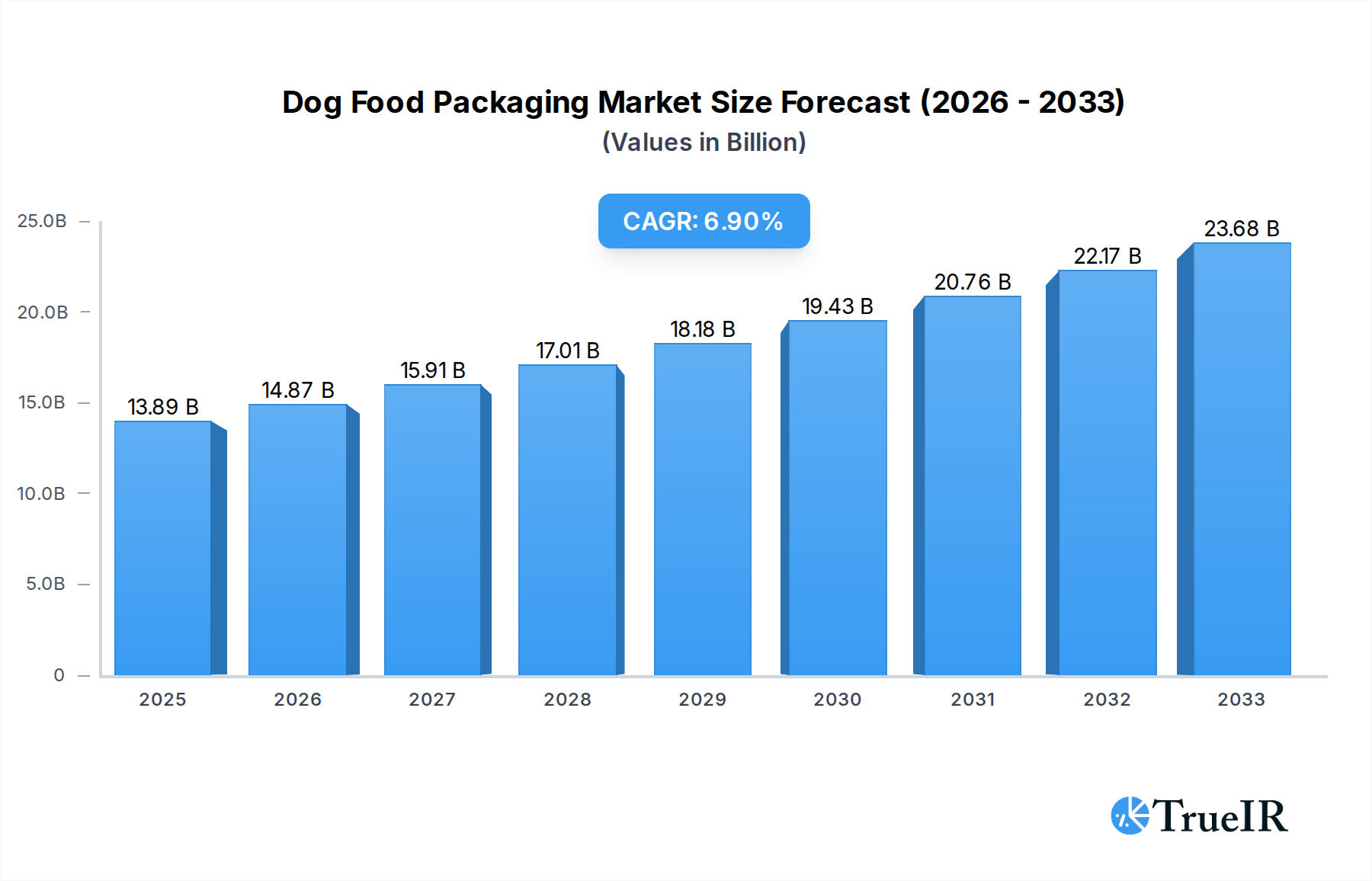

The global Dog Food Packaging market is projected to reach a substantial $13.89 billion in 2025, demonstrating robust growth with a Compound Annual Growth Rate (CAGR) of 6.9% through 2033. This expansion is fueled by a confluence of factors, primarily the increasing humanization of pets, leading to higher consumer spending on premium and specialized dog food products. The growing awareness among pet owners regarding the importance of nutritional quality and safety is directly translating into a demand for advanced and innovative packaging solutions. Key drivers include the rising disposable incomes in emerging economies, which allows for greater expenditure on pet care, and the increasing adoption of e-commerce for pet food purchases, necessitating durable and attractive packaging for shipping. Furthermore, the proliferation of specialized diets, such as grain-free, organic, and breed-specific formulas, further segment the market and spur the need for diverse packaging formats that can maintain product freshness and communicate unique selling propositions effectively.

Dog Food Packaging Market Size (In Billion)

The market is segmented by application into Dry Food, Wet Food, Chilled and Frozen Food, and Others. Dry food packaging, often leveraging Paper and Paperboard and Flexible Plastic, currently holds a significant share due to its widespread consumption. However, the growing demand for premium wet food and frozen options is driving innovation in materials like Rigid Plastic and Metal, along with specialized barrier technologies to ensure extended shelf life and preserve nutrient integrity. Emerging trends indicate a strong push towards sustainable packaging solutions, with manufacturers exploring recycled content, biodegradable materials, and reduced plastic usage. While this presents an opportunity, potential restraints include the higher cost of sustainable materials and the complex regulatory landscape governing food-grade packaging materials. Companies like Amcor, Constantia Flexibles, and Mondi Group are at the forefront of developing these advanced and eco-friendly packaging solutions to cater to evolving consumer preferences and industry demands.

Dog Food Packaging Company Market Share

Dog Food Packaging Market: Global Industry Analysis, Size, Share, Growth, Trends, and Forecast 2019–2033

This comprehensive report delves into the dynamic global dog food packaging market, offering an in-depth analysis of its structure, trends, opportunities, and competitive landscape. Spanning a study period from 2019 to 2033, with a base year of 2025, this report provides critical insights for industry stakeholders, including manufacturers, suppliers, investors, and consumers. The global dog food packaging market is projected to reach astronomical figures, with market size estimated at over 100 billion in the base year 2025 and expected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period of 2025–2033. The historical period from 2019–2024 has laid the groundwork for this expansive growth, driven by an ever-increasing pet humanization trend and rising disposable incomes worldwide.

Dog Food Packaging Market Structure & Competitive Landscape

The global dog food packaging market exhibits a moderately concentrated structure, with a few key players holding significant market share, alongside a robust presence of smaller, specialized manufacturers. Innovation remains a pivotal driver, with companies continuously investing in research and development to create sustainable, functional, and aesthetically appealing packaging solutions. Regulatory impacts, particularly concerning food safety, environmental sustainability, and labeling, are increasingly shaping market strategies, pushing for eco-friendly alternatives and compliant materials. Product substitutes, such as bulk buying or alternative storage methods, are minimal given the convenience and shelf-life advantages offered by conventional packaging. End-user segmentation is predominantly driven by the distinct needs of dry kibble, wet food, and specialized chilled or frozen dog food products, each requiring tailored packaging properties. Mergers and acquisitions (M&A) activity has been a notable trend, consolidating market players and expanding their global reach and product portfolios. For instance, the market has witnessed over 10 billion in M&A deals historically, aiming to capitalize on emerging markets and technological advancements. The concentration ratio among the top five players is estimated at 60%, indicating a strong but not entirely consolidated market.

- Innovation Drivers: Advanced material science, smart packaging technologies, and sustainable design principles.

- Regulatory Impacts: Increased demand for recyclable, compostable, and biodegradable materials; stringent food contact regulations.

- Product Substitutes: Limited, primarily focused on alternative storage solutions for consumers.

- End-User Segmentation: Dry food dominates due to bulk sales, followed by wet food and specialized frozen/chilled options.

- M&A Trends: Strategic acquisitions to enhance market presence, expand product offerings, and gain access to new technologies.

Dog Food Packaging Market Trends & Opportunities

The global dog food packaging market is experiencing unprecedented growth, fueled by a confluence of evolving consumer preferences, technological advancements, and a growing global pet population. The market size, valued at over 100 billion in 2025, is projected to skyrocket to over 150 billion by 2033, exhibiting a strong CAGR of xx%. This expansion is underpinned by the escalating trend of pet humanization, where dogs are increasingly viewed as integral family members, leading owners to seek premium, high-quality food options packaged in ways that reflect this elevated status. Technological shifts are revolutionizing the packaging landscape, with an increasing adoption of flexible plastic packaging for its versatility, cost-effectiveness, and superior barrier properties, especially for dry dog food. This segment alone is expected to account for over 70 billion in market value by 2033. Rigid plastic packaging also holds a significant share, particularly for premium wet food products, offering robust protection and an appealing shelf presence. Innovations in material science are leading to the development of advanced barrier films, resealable closures, and portion-controlled packaging, enhancing product freshness and convenience.

Consumer preferences are increasingly leaning towards sustainable packaging solutions. This has opened up significant opportunities for manufacturers exploring biodegradable, compostable, and recyclable materials, including paper and paperboard-based packaging, which is gaining traction, especially for dry food. The market for paper and paperboard packaging is estimated to grow by over 5% annually. Furthermore, the rise of e-commerce has spurred demand for durable, tamper-evident packaging that can withstand the rigors of shipping, creating a niche for specialized e-commerce-ready solutions. Opportunities also lie in the development of smart packaging technologies that can monitor product freshness, provide authentication, or offer interactive consumer experiences. The chilled and frozen food segment, though smaller, presents considerable growth potential, driven by consumer demand for fresher, less processed options and requiring specialized barrier and freezing-resistant packaging. This segment is predicted to grow at a CAGR of 6.5%. The competitive dynamics are intensifying, with companies focusing on product differentiation through unique designs, eco-friendly attributes, and enhanced functionality. Strategic partnerships and collaborations are becoming crucial for companies to expand their geographical reach and technological capabilities. The overall market penetration rate for specialized dog food packaging is projected to exceed 90% by 2033, reflecting the indispensability of effective packaging in this booming industry.

Dominant Markets & Segments in Dog Food Packaging

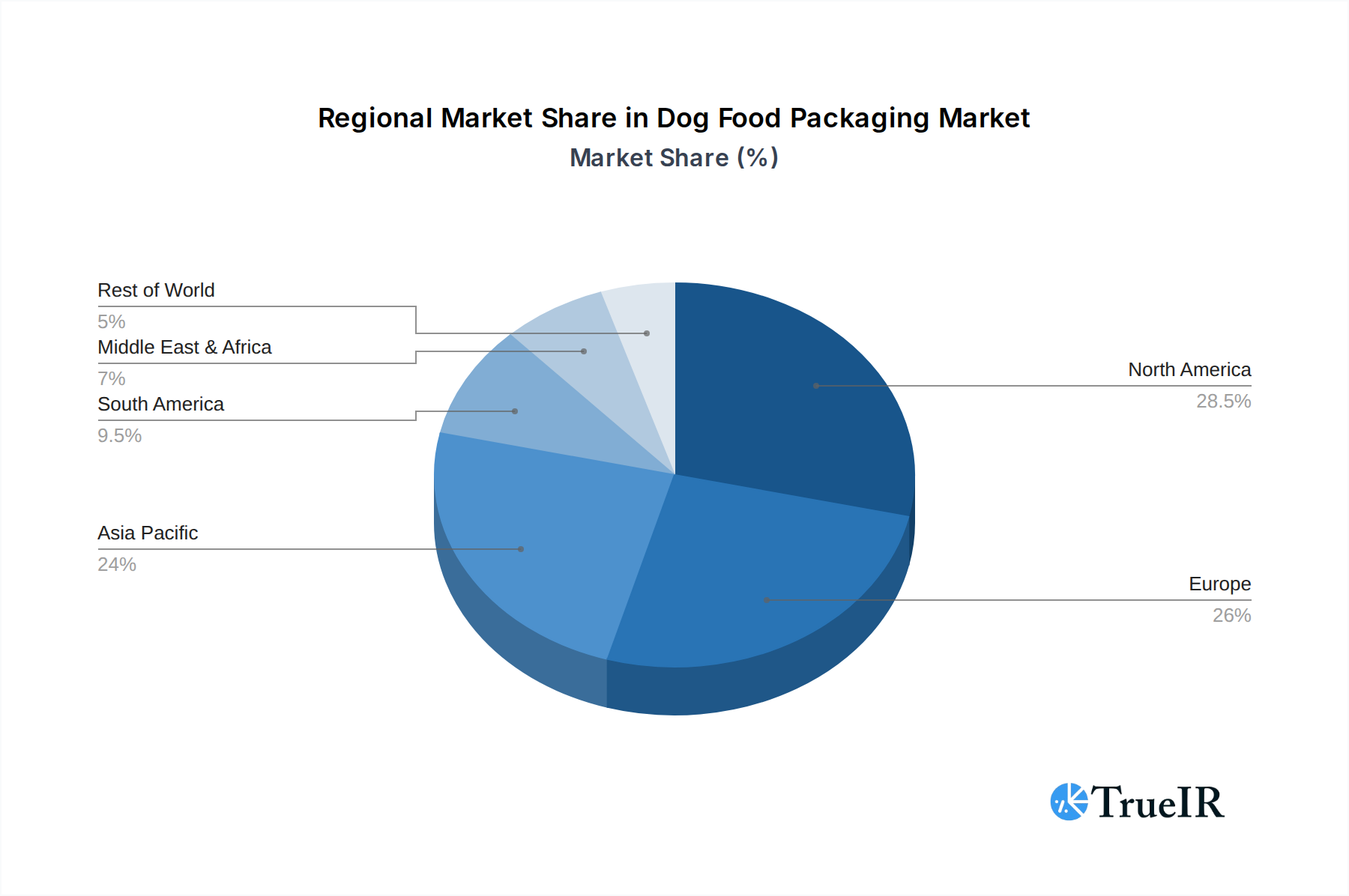

The global dog food packaging market is characterized by distinct regional dominance and segment leadership, driven by varying economic conditions, consumer behaviors, and regulatory frameworks. North America currently holds a significant share of the market, estimated at over 35 billion, driven by high pet ownership rates and a strong consumer inclination towards premium dog food products. The United States, in particular, is a powerhouse in this segment. Asia-Pacific is emerging as the fastest-growing region, with an anticipated CAGR of 7.2%, propelled by increasing disposable incomes, rapid urbanization, and a growing middle class embracing pet ownership.

- Dominant Region: North America leads in market value due to established pet care industries and high per capita spending on pet products.

- Fastest Growing Region: Asia-Pacific is projected to witness the highest growth due to increasing pet adoption and a burgeoning middle class.

In terms of application, Dry Food continues to dominate the dog food packaging market, accounting for over 60 billion in market value in 2025. This is attributed to its widespread availability, longer shelf life, and cost-effectiveness, making it the primary choice for a vast majority of dog owners. The packaging for dry food primarily relies on flexible plastic pouches and multi-wall paper bags, offering excellent barrier properties to maintain freshness and prevent spoilage.

- Application: Dry Food: Holds the largest market share due to its popularity, cost-effectiveness, and convenience. Key growth drivers include large-scale production, consumer preference for bulk purchases, and the need for robust barrier properties to ensure freshness.

The Flexible Plastic segment is the most dominant type of packaging, valued at over 50 billion in 2025. Its versatility, excellent moisture and oxygen barrier capabilities, printability, and relatively lower cost make it ideal for a wide range of dog food products, especially dry kibble. Advancements in flexible packaging technology, including multi-layer films and advanced printing techniques, further enhance its appeal.

- Type: Flexible Plastic: Dominates due to its superior barrier properties, cost-effectiveness, and printability. Key growth drivers include ongoing innovation in material science for enhanced sustainability and performance, and its adaptability for various product formats.

The Wet Food segment, while smaller than dry food, is also a significant contributor, with a market value projected to exceed 30 billion by 2033. This segment often utilizes metal cans and rigid plastic containers, offering excellent preservation and a premium feel. The Chilled and Frozen Food segment, though currently the smallest, is expected to witness substantial growth, driven by the demand for fresh, natural, and minimally processed dog food options. This necessitates specialized packaging capable of withstanding freezing temperatures and maintaining product integrity. The "Others" category, encompassing innovative or emerging packaging formats, is also poised for growth as the industry embraces novel solutions.

Dog Food Packaging Product Analysis

The dog food packaging market is witnessing a surge in product innovations aimed at enhancing convenience, sustainability, and product protection. Flexible plastic pouches with advanced resealable features and integrated dispensing mechanisms are gaining traction, offering superior freshness preservation and ease of use for consumers. The development of innovative barrier technologies, including those incorporating nanotechnology, is extending shelf life and reducing the need for artificial preservatives. Sustainable alternatives, such as compostable films derived from plant-based materials and recyclable mono-material structures, are becoming increasingly prominent. Competitive advantages are being derived from unique print designs, premium finishes, and the incorporation of "smart" features like temperature indicators or QR codes for product traceability and consumer engagement.

Key Drivers, Barriers & Challenges in Dog Food Packaging

Key Drivers: The dog food packaging market is primarily propelled by the ever-growing trend of pet humanization, leading to increased demand for premium and specialized food products. Rising disposable incomes globally further fuel this trend. Technological advancements in material science and manufacturing processes enable the development of more sustainable, functional, and cost-effective packaging solutions. Growing e-commerce penetration necessitates robust and attractive packaging for online retail.

Barriers & Challenges: Regulatory complexities, particularly concerning food safety standards and the increasing demand for sustainable packaging, pose significant challenges. Supply chain disruptions, fluctuating raw material costs, and the logistical complexities of global distribution can impact profitability. Intense competition among packaging manufacturers, coupled with the need for continuous innovation, exerts considerable pressure on pricing and margins. Addressing the environmental impact of packaging waste remains a critical challenge, driving the need for widespread adoption of recyclable and biodegradable alternatives, which can sometimes involve higher initial costs or require significant infrastructure investment.

Growth Drivers in the Dog Food Packaging Market

The growth of the dog food packaging market is primarily driven by the escalating humanization of pets, leading owners to invest more in premium and specialized food options. This behavioral shift is amplified by increasing global disposable incomes, particularly in emerging economies, making premium pet food more accessible. Technological advancements are a crucial catalyst, with innovations in material science leading to the development of enhanced barrier properties, improved shelf-life, and more sustainable packaging materials like compostable films and mono-material structures. The expanding e-commerce sector for pet products also necessitates durable, secure, and appealing packaging solutions optimized for shipping. Furthermore, a growing awareness of health and wellness among pet owners is driving demand for specialized packaging that preserves the nutritional integrity and freshness of premium dog food formulations.

Challenges Impacting Dog Food Packaging Growth

Several challenges are impacting the growth trajectory of the dog food packaging market. Stringent and evolving environmental regulations worldwide are creating pressure for manufacturers to adopt more sustainable packaging solutions, which can involve higher production costs and necessitate significant investment in new technologies and infrastructure. Supply chain volatility, including fluctuations in raw material prices and availability, can lead to unpredictable manufacturing costs and potential delays. Intense competition within the packaging industry can result in price wars and compressed profit margins, demanding continuous innovation to maintain market share. Furthermore, consumer education regarding the recyclability and disposability of various packaging types remains a hurdle, and the development of effective end-of-life solutions for complex multi-material packaging is still ongoing.

Key Players Shaping the Dog Food Packaging Market

- Amcor

- Constantia Flexibles

- Ardagh Group

- Coveris

- Sonoco Products Co

- Mondi Group

- Huhtamaki

- Printpack

- Winpak

- ProAmpac

- Berry Plastics Corporation

- Bryce Corporation

- Aptargroup

Significant Dog Food Packaging Industry Milestones

- 2019: Introduction of advanced compostable barrier films by leading material suppliers, responding to growing sustainability demands.

- 2020: Increased investment in flexible packaging solutions for e-commerce fulfillment driven by pandemic-induced online shopping boom.

- 2021: Major brands launch dog food lines in fully recyclable mono-material pouches, marking a shift towards circular economy principles.

- 2022: Development of smart packaging prototypes with integrated sensors for real-time freshness monitoring.

- 2023: Significant M&A activities consolidate market players, expanding product portfolios and geographical reach, with deals exceeding 5 billion.

- 2024: Growing adoption of paper-based solutions for dry dog food, offering a more sustainable alternative to traditional plastics.

Future Outlook for Dog Food Packaging Market

The future outlook for the dog food packaging market is exceptionally robust, driven by sustained pet humanization trends and increasing global pet ownership. Strategic opportunities lie in further innovation in sustainable packaging materials, including advanced biodegradable and recyclable options, as well as the development of novel dispensing and portioning technologies to enhance consumer convenience. The continued growth of e-commerce will fuel demand for specialized, durable, and aesthetically pleasing packaging solutions designed for online retail. Companies that can effectively address regulatory requirements, invest in advanced manufacturing capabilities, and align their product offerings with consumer preferences for health, wellness, and sustainability are poised for significant success in this expanding market. The market is expected to see continuous product development and strategic collaborations to meet the evolving needs of both pets and their owners.

Dog Food Packaging Segmentation

-

1. Application

- 1.1. Dry Food

- 1.2. Wet Food

- 1.3. Chilled and Frozen Food

- 1.4. Others

-

2. Type

- 2.1. Paper and Paperboard

- 2.2. Flexible Plastic

- 2.3. Rigid Plastic

- 2.4. Metal

- 2.5. Others

Dog Food Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Dog Food Packaging Regional Market Share

Geographic Coverage of Dog Food Packaging

Dog Food Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Dry Food

- 5.1.2. Wet Food

- 5.1.3. Chilled and Frozen Food

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Paper and Paperboard

- 5.2.2. Flexible Plastic

- 5.2.3. Rigid Plastic

- 5.2.4. Metal

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Dog Food Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Dry Food

- 6.1.2. Wet Food

- 6.1.3. Chilled and Frozen Food

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Paper and Paperboard

- 6.2.2. Flexible Plastic

- 6.2.3. Rigid Plastic

- 6.2.4. Metal

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Dog Food Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Dry Food

- 7.1.2. Wet Food

- 7.1.3. Chilled and Frozen Food

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Paper and Paperboard

- 7.2.2. Flexible Plastic

- 7.2.3. Rigid Plastic

- 7.2.4. Metal

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Dog Food Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Dry Food

- 8.1.2. Wet Food

- 8.1.3. Chilled and Frozen Food

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Paper and Paperboard

- 8.2.2. Flexible Plastic

- 8.2.3. Rigid Plastic

- 8.2.4. Metal

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Dog Food Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Dry Food

- 9.1.2. Wet Food

- 9.1.3. Chilled and Frozen Food

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Paper and Paperboard

- 9.2.2. Flexible Plastic

- 9.2.3. Rigid Plastic

- 9.2.4. Metal

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Dog Food Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Dry Food

- 10.1.2. Wet Food

- 10.1.3. Chilled and Frozen Food

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Paper and Paperboard

- 10.2.2. Flexible Plastic

- 10.2.3. Rigid Plastic

- 10.2.4. Metal

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Dog Food Packaging Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Dry Food

- 11.1.2. Wet Food

- 11.1.3. Chilled and Frozen Food

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Paper and Paperboard

- 11.2.2. Flexible Plastic

- 11.2.3. Rigid Plastic

- 11.2.4. Metal

- 11.2.5. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Amcor

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Constantia Flexibles

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Ardagh Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Coveris

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Sonoco Products Co

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Mondi Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Huhtamaki

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Printpack

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Winpak

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 ProAmpac

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Berry Plastics Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Bryce Corporation

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Aptargroup

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Amcor

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Dog Food Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Dog Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Dog Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Dog Food Packaging Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Dog Food Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Dog Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Dog Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Dog Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Dog Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Dog Food Packaging Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Dog Food Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Dog Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Dog Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Dog Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Dog Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Dog Food Packaging Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Dog Food Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Dog Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Dog Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Dog Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Dog Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Dog Food Packaging Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Dog Food Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Dog Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Dog Food Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Dog Food Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Dog Food Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Dog Food Packaging Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Dog Food Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Dog Food Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Dog Food Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dog Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Dog Food Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Dog Food Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Dog Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Dog Food Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Dog Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Dog Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Dog Food Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Dog Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Dog Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Dog Food Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Dog Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Dog Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Dog Food Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Dog Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Dog Food Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Dog Food Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Dog Food Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Dog Food Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dog Food Packaging?

The projected CAGR is approximately 4.4%.

2. Which companies are prominent players in the Dog Food Packaging?

Key companies in the market include Amcor, Constantia Flexibles, Ardagh Group, Coveris, Sonoco Products Co, Mondi Group, Huhtamaki, Printpack, Winpak, ProAmpac, Berry Plastics Corporation, Bryce Corporation, Aptargroup.

3. What are the main segments of the Dog Food Packaging?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.87 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dog Food Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dog Food Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dog Food Packaging?

To stay informed about further developments, trends, and reports in the Dog Food Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence