Key Insights

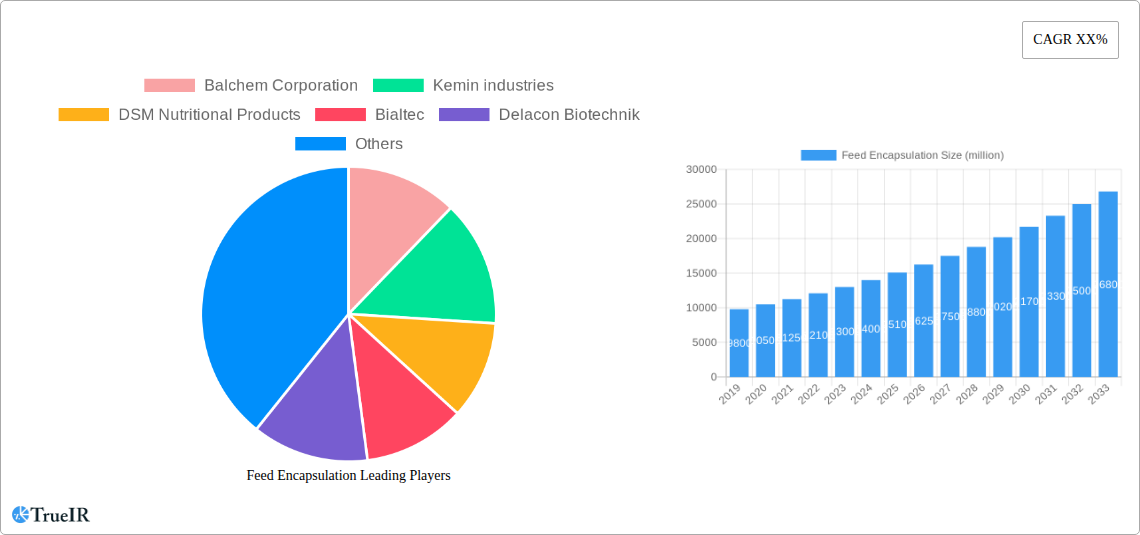

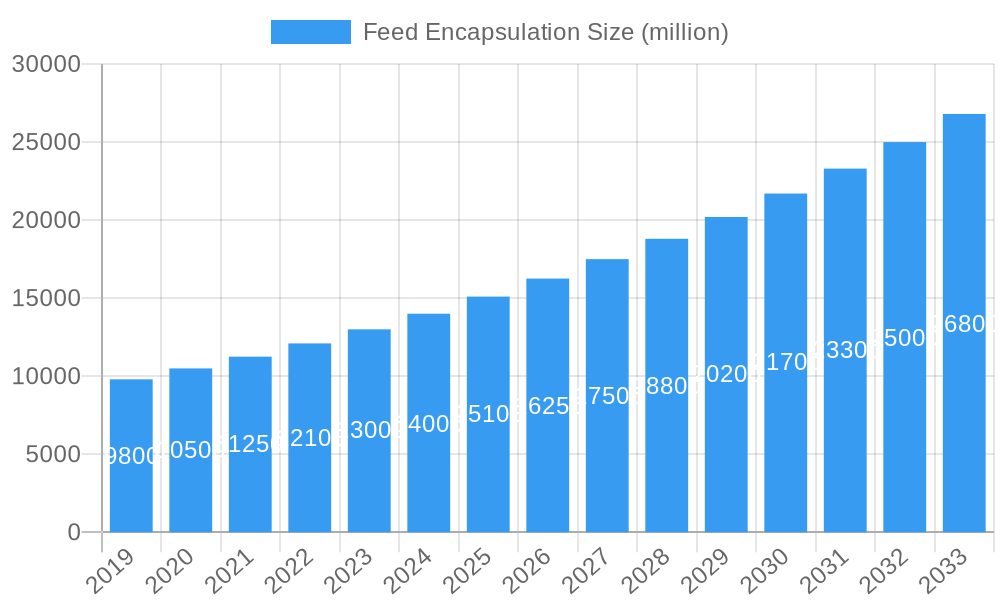

The global Feed Encapsulation market is experiencing robust growth, projected to reach a significant market size of approximately USD 15,500 million by 2025. This expansion is driven by an estimated Compound Annual Growth Rate (CAGR) of around 7.2% from 2019 to 2033, indicating sustained momentum in the coming years. The market is primarily propelled by the increasing demand for enhanced animal nutrition and health, a direct consequence of the growing global population and the subsequent surge in meat and dairy consumption. Feed encapsulation plays a crucial role in improving the efficacy of feed additives, protecting sensitive nutrients from degradation during feed processing, and ensuring targeted delivery within the animal's digestive system. Key applications like poultry, swine, and aquaculture are witnessing substantial adoption, as producers seek to optimize feed conversion ratios, reduce environmental impact through improved nutrient utilization, and enhance animal welfare. The rising awareness among farmers about the benefits of advanced feed technologies, coupled with supportive government regulations promoting sustainable animal agriculture, further fuels market expansion.

Feed Encapsulation Market Size (In Billion)

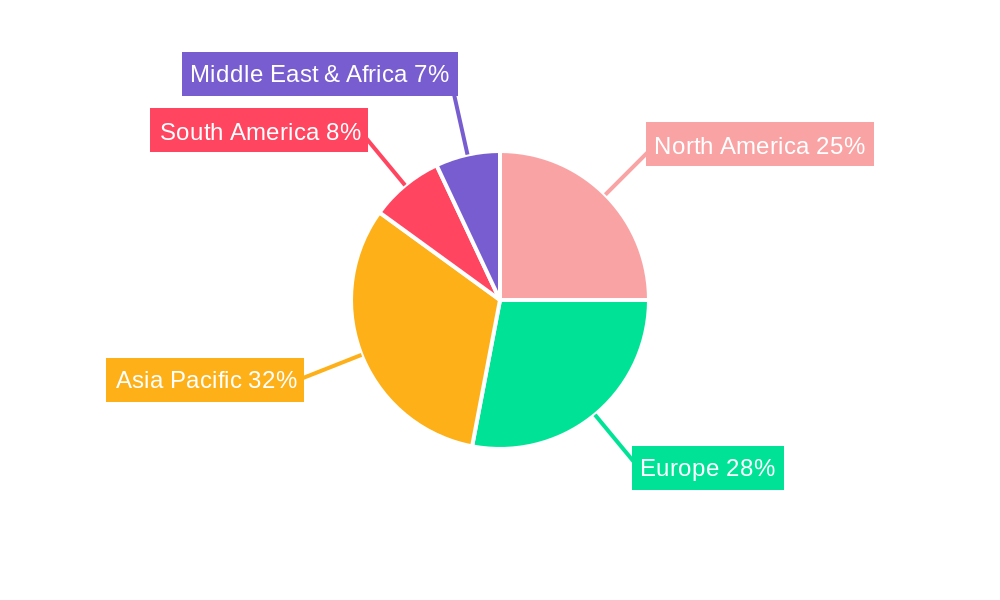

The market is characterized by several key trends, including the growing adoption of innovative coating materials such as advanced polymers, carbohydrates, and natural extracts, moving beyond traditional lipid-based approaches. These novel materials offer superior protection and controlled release mechanisms, catering to specific nutritional needs and animal types. However, the market also faces certain restraints, including the relatively high initial investment cost associated with advanced encapsulation technologies and the potential for fluctuating raw material prices, which can impact profitability. Despite these challenges, the continuous research and development efforts by leading companies like Balchem Corporation, Kemin Industries, and DSM Nutritional Products are introducing more cost-effective and efficient encapsulation solutions. The Asia Pacific region, particularly China and India, is emerging as a significant growth engine due to its rapidly expanding livestock industry and increasing disposable incomes. North America and Europe remain mature yet substantial markets, driven by a strong focus on precision nutrition and sustainable farming practices. The continuous innovation in encapsulation techniques and the expanding range of applicable feed additives are poised to unlock further market potential in the forecast period.

Feed Encapsulation Company Market Share

Here is a dynamic, SEO-optimized report description for Feed Encapsulation, incorporating your requirements.

Feed Encapsulation Market: Comprehensive Analysis and Future Outlook (2019-2033)

This in-depth report provides a definitive analysis of the global Feed Encapsulation market, offering unparalleled insights for stakeholders seeking to navigate this rapidly evolving industry. Leveraging high-volume keywords and a meticulously structured format, this report is engineered for maximum SEO impact and immediate utility. Our study encompasses a comprehensive historical analysis from 2019 to 2024, a detailed base year assessment for 2025, and a robust forecast period extending to 2033. Explore the strategic landscape, technological advancements, market trends, and key players shaping the future of animal nutrition and feed additive delivery.

Feed Encapsulation Market Structure & Competitive Landscape

The global Feed Encapsulation market is characterized by a moderately concentrated structure, with key players like Balchem Corporation, Kemin Industries, and DSM Nutritional Products holding significant market share. Innovation drivers are primarily fueled by the demand for enhanced nutrient bioavailability, improved animal health, and reduced environmental impact. Regulatory impacts, particularly concerning feed safety and ingredient efficacy, are increasingly influencing product development and market entry. Product substitutes, while present in the form of un-encapsulated additives, face limitations in efficacy and stability, reinforcing the value proposition of encapsulation. End-user segmentation by application, including Poultry, Swine, Aquaculture, and Ruminants, reveals distinct market dynamics and adoption rates. Mergers & Acquisitions (M&A) trends indicate strategic consolidation and expansion efforts by major corporations, with an estimated XX million in M&A volumes observed in recent years. The concentration ratio of the top 5 players is estimated at approximately XX%.

Feed Encapsulation Market Trends & Opportunities

The Feed Encapsulation market is poised for substantial growth, driven by an escalating global demand for efficient and sustainable animal protein production. Projected to reach a market size of over XXX million by 2033, the market exhibits a Compound Annual Growth Rate (CAGR) of approximately XX% during the forecast period. Key technological shifts are centered around the development of advanced encapsulation techniques, including nano-encapsulation and controlled-release technologies, offering superior protection and targeted delivery of sensitive feed additives. Consumer preferences for ethically sourced and healthier animal products are indirectly fueling the adoption of feed encapsulation, as it contributes to improved animal welfare and reduced antibiotic usage. Competitive dynamics are intensifying, with a focus on developing cost-effective solutions and expanding product portfolios to cater to diverse animal species and nutritional needs. Market penetration rates for specialized encapsulated additives are steadily increasing, signifying a growing awareness of their benefits among feed manufacturers and animal producers. The continuous innovation in polymers and natural materials for encapsulation is creating new opportunities for tailor-made solutions, addressing specific challenges in feed preservation and nutrient utilization. Furthermore, the growing emphasis on precision nutrition and the need to optimize feed conversion ratios are creating significant avenues for market expansion. The integration of smart technologies in feed delivery systems further amplifies the demand for precisely formulated encapsulated ingredients.

Dominant Markets & Segments in Feed Encapsulation

The Poultry segment is currently the dominant market within the Feed Encapsulation landscape, driven by the high volume of feed consumption and the continuous pursuit of improved feed efficiency and reduced mortality rates in the global poultry industry. Within this segment, Lipid-Based Coatings represent a leading type of encapsulation technology due to their cost-effectiveness, ability to protect sensitive ingredients like vitamins and probiotics, and their compatibility with various feed formulations.

- Key Growth Drivers in Poultry:

- Increased Global Demand for Poultry Protein: Surging global population and evolving dietary habits necessitate greater poultry production, directly impacting feed demand.

- Focus on Gut Health and Immunity: Encapsulated probiotics and prebiotics offer targeted delivery to enhance gut health, a critical factor in poultry performance and disease prevention.

- Reduced Antibiotic Reliance: Encapsulation of alternative growth promoters and immune modulators is a key strategy for the industry to comply with regulatory restrictions on antibiotic use.

- Cost-Effective Nutrient Delivery: Lipid-based encapsulation provides a cost-efficient method to protect and deliver essential nutrients, improving feed conversion ratios.

In terms of geographic dominance, Asia Pacific is emerging as a significant region, fueled by rapid growth in its livestock sector, particularly in countries like China and India, and a growing adoption of advanced feed technologies. The demand for specialized feed additives in Swine production is also substantial, with a growing emphasis on improving growth performance and mitigating specific health challenges through encapsulated supplements. Aquaculture is another burgeoning segment, where the need for precise nutrient delivery in aquatic environments and protection against water-soluble losses drives the adoption of advanced encapsulation techniques. Ruminants present a unique opportunity with the demand for rumen-protected nutrients, such as bypass fats and amino acids, to optimize milk production and fertility. The "Others" segment, encompassing companion animals and niche livestock, also contributes to market diversification.

Feed Encapsulation Product Analysis

Product innovation in feed encapsulation is largely focused on enhancing the stability and bioavailability of sensitive feed additives, including vitamins, minerals, probiotics, prebiotics, enzymes, and active pharmaceutical ingredients. Lipid-based coatings and advanced polymer formulations are at the forefront, offering controlled-release mechanisms and improved protection against degradation during feed processing and digestion. These advancements translate to superior animal health outcomes, increased growth rates, and optimized feed utilization, providing a significant competitive advantage to products incorporating these technologies.

Key Drivers, Barriers & Challenges in Feed Encapsulation

Key Drivers:

- Technological Advancements: Development of novel encapsulation materials (e.g., biodegradable polymers, natural compounds) and techniques (e.g., nano-encapsulation) enabling superior protection and targeted delivery.

- Economic Factors: Rising raw material costs and the need for efficient nutrient utilization drive demand for technologies that maximize feed conversion ratios.

- Policy & Regulatory Landscape: Increasing restrictions on antibiotic use in animal feed and growing consumer demand for antibiotic-free products create a strong impetus for encapsulated alternatives.

- Animal Health and Welfare Focus: Growing emphasis on improving animal immunity, gut health, and overall well-being through precise nutrient and supplement delivery.

Barriers & Challenges:

- Supply Chain Volatility: Fluctuations in the availability and cost of raw materials for encapsulation can impact production and pricing.

- Regulatory Hurdles: Navigating diverse and evolving regulations for feed additives and encapsulation materials across different regions can be complex.

- Cost of Implementation: Initial investment in encapsulation technology and higher per-unit costs of encapsulated ingredients can be a barrier for some producers.

- Performance Variability: Ensuring consistent efficacy and bioavailability of encapsulated products across different feed matrices and processing conditions remains a challenge.

- Limited Consumer Awareness: While industry awareness is growing, broader consumer understanding of the benefits of feed encapsulation for animal products is still developing.

Growth Drivers in the Feed Encapsulation Market

The Feed Encapsulation market is propelled by several key growth drivers. Technological innovation, particularly in areas like nano-encapsulation and advanced polymer science, allows for more effective protection and targeted release of valuable feed additives. Economically, the imperative to maximize feed conversion ratios and reduce waste in livestock production significantly boosts demand for encapsulated nutrients. Regulatory shifts, such as the global move away from antibiotic growth promoters, create a substantial opportunity for encapsulated alternatives that enhance animal health and performance. Furthermore, the increasing focus on animal welfare and the demand for sustainably produced animal protein are creating a favorable environment for feed encapsulation technologies that improve nutrient absorption and reduce environmental impact.

Challenges Impacting Feed Encapsulation Growth

Despite strong growth potential, the Feed Encapsulation market faces several challenges. Regulatory complexities in approving novel encapsulation materials and the varying standards across different countries can slow down market entry. Supply chain issues, including the availability and price volatility of key raw materials, pose a constant threat to production efficiency and cost-competitiveness. Intense competitive pressures among established players and emerging innovators necessitate continuous research and development to maintain a market edge. Moreover, the higher upfront cost associated with some advanced encapsulation technologies can be a significant barrier for smaller feed producers or those in developing markets, requiring a clear demonstration of long-term economic benefits.

Key Players Shaping the Feed Encapsulation Market

- Balchem Corporation

- Kemin Industries

- DSM Nutritional Products

- Bialtec

- Delacon Biotechnik

- Adisseo

- Evonik Industries

- Novus International

- Phytobiotics

Significant Feed Encapsulation Industry Milestones

- 2019: Advancements in biodegradable polymer encapsulation for enhanced environmental sustainability.

- 2020: Increased focus on encapsulating probiotics and prebiotics for improved gut health in poultry and swine.

- 2021: Development of novel nano-encapsulation techniques for targeted delivery of micronutrients in aquaculture.

- 2022: Growing adoption of rumen-protected amino acids for dairy cows to optimize milk production.

- 2023: Introduction of cost-effective lipid-based encapsulation solutions for widespread application in swine feed.

- 2024: Increased research into natural material-based encapsulation for a cleaner label approach in pet food.

Future Outlook for Feed Encapsulation Market

The future outlook for the Feed Encapsulation market is exceptionally promising, driven by ongoing innovations in delivery systems and a global shift towards precision nutrition in animal agriculture. Strategic opportunities lie in the further development of smart encapsulation technologies that respond to specific physiological conditions within the animal, optimizing nutrient release in real-time. The growing demand for antibiotic-free animal products will continue to fuel the market for encapsulated immune modulators and performance enhancers. Furthermore, the expansion of aquaculture and the increasing need for sustainable feed solutions in this sector present a significant untapped potential. We anticipate continued R&D investment and strategic partnerships to drive market penetration and broaden the application of feed encapsulation across all major livestock segments, ensuring improved animal health, efficiency, and sustainability.

Feed Encapsulation Segmentation

-

1. Application

- 1.1. Poultry

- 1.2. Swine

- 1.3. Aquaculture

- 1.4. Ruminants

- 1.5. Others

-

2. Types

- 2.1. Lipid-Based Coatings

- 2.2. Polymers

- 2.3. Protein-Based Coatings

- 2.4. Carbohydrates

- 2.5. Natural Materials

Feed Encapsulation Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Feed Encapsulation Regional Market Share

Geographic Coverage of Feed Encapsulation

Feed Encapsulation REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Poultry

- 5.1.2. Swine

- 5.1.3. Aquaculture

- 5.1.4. Ruminants

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Lipid-Based Coatings

- 5.2.2. Polymers

- 5.2.3. Protein-Based Coatings

- 5.2.4. Carbohydrates

- 5.2.5. Natural Materials

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Feed Encapsulation Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Poultry

- 6.1.2. Swine

- 6.1.3. Aquaculture

- 6.1.4. Ruminants

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Lipid-Based Coatings

- 6.2.2. Polymers

- 6.2.3. Protein-Based Coatings

- 6.2.4. Carbohydrates

- 6.2.5. Natural Materials

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Poultry

- 7.1.2. Swine

- 7.1.3. Aquaculture

- 7.1.4. Ruminants

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Lipid-Based Coatings

- 7.2.2. Polymers

- 7.2.3. Protein-Based Coatings

- 7.2.4. Carbohydrates

- 7.2.5. Natural Materials

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Poultry

- 8.1.2. Swine

- 8.1.3. Aquaculture

- 8.1.4. Ruminants

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Lipid-Based Coatings

- 8.2.2. Polymers

- 8.2.3. Protein-Based Coatings

- 8.2.4. Carbohydrates

- 8.2.5. Natural Materials

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Poultry

- 9.1.2. Swine

- 9.1.3. Aquaculture

- 9.1.4. Ruminants

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Lipid-Based Coatings

- 9.2.2. Polymers

- 9.2.3. Protein-Based Coatings

- 9.2.4. Carbohydrates

- 9.2.5. Natural Materials

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Poultry

- 10.1.2. Swine

- 10.1.3. Aquaculture

- 10.1.4. Ruminants

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Lipid-Based Coatings

- 10.2.2. Polymers

- 10.2.3. Protein-Based Coatings

- 10.2.4. Carbohydrates

- 10.2.5. Natural Materials

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Feed Encapsulation Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Poultry

- 11.1.2. Swine

- 11.1.3. Aquaculture

- 11.1.4. Ruminants

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Lipid-Based Coatings

- 11.2.2. Polymers

- 11.2.3. Protein-Based Coatings

- 11.2.4. Carbohydrates

- 11.2.5. Natural Materials

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Balchem Corporation

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Kemin industries

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 DSM Nutritional Products

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Bialtec

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Delacon Biotechnik

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Adisseo

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Evonik Industries

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Novus International

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Phytobiotics

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.1 Balchem Corporation

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Feed Encapsulation Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Feed Encapsulation Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Feed Encapsulation Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Feed Encapsulation Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Feed Encapsulation Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Feed Encapsulation Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Feed Encapsulation Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Feed Encapsulation Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Feed Encapsulation Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Feed Encapsulation Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Feed Encapsulation Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Feed Encapsulation Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Feed Encapsulation Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Feed Encapsulation Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Feed Encapsulation Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Feed Encapsulation Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Feed Encapsulation Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Feed Encapsulation Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Feed Encapsulation Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Feed Encapsulation Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Feed Encapsulation Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Feed Encapsulation Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Feed Encapsulation Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Feed Encapsulation Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Feed Encapsulation Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Feed Encapsulation Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Feed Encapsulation Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Feed Encapsulation Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Feed Encapsulation Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Feed Encapsulation Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Feed Encapsulation Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Feed Encapsulation Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Feed Encapsulation Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Feed Encapsulation Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Feed Encapsulation Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Feed Encapsulation Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Feed Encapsulation Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Feed Encapsulation Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Feed Encapsulation?

The projected CAGR is approximately 8.5%.

2. Which companies are prominent players in the Feed Encapsulation?

Key companies in the market include Balchem Corporation, Kemin industries, DSM Nutritional Products, Bialtec, Delacon Biotechnik, Adisseo, Evonik Industries, Novus International, Phytobiotics.

3. What are the main segments of the Feed Encapsulation?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Feed Encapsulation," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Feed Encapsulation report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Feed Encapsulation?

To stay informed about further developments, trends, and reports in the Feed Encapsulation, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence