Key Insights

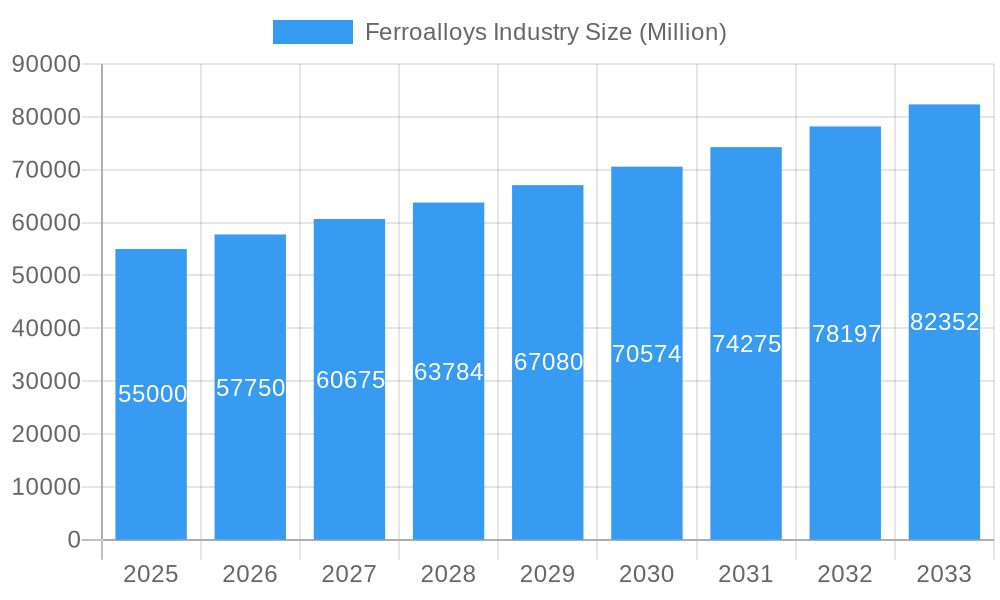

The global ferroalloys market experienced robust growth between 2019 and 2024, driven primarily by the burgeoning construction and automotive sectors. Steel production, the major consumer of ferroalloys, witnessed significant expansion during this period, fueling demand for these essential alloying agents. Factors such as increasing infrastructure development globally, particularly in emerging economies, further contributed to market expansion. While precise market size figures for 2019-2024 are unavailable, a reasonable estimation based on industry reports and observed growth trends suggests a steady Compound Annual Growth Rate (CAGR) of approximately 5-7% during that period. This translates to a market value exceeding $50 billion by 2024. The base year of 2025 sees a projected market size of $55 billion, reflecting continued strong demand.

Ferroalloys Industry Market Size (In Billion)

Looking ahead to 2033, the ferroalloys market is poised for continued growth, albeit at a potentially slightly moderated pace. The forecast period (2025-2033) anticipates a CAGR of around 4-6%, projecting market valuation to surpass $85 billion by 2033. This moderation may be attributed to factors such as cyclical fluctuations in steel production, potential shifts in material preferences within specific industries, and the impact of governmental regulations on emissions. However, ongoing global infrastructure projects, the rise of electric vehicles (requiring specialized steel alloys), and advancements in metallurgical processes are expected to sustain considerable market demand throughout the forecast period. The market’s future depends heavily on consistent economic growth, especially in developing nations.

Ferroalloys Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global ferroalloys industry, offering invaluable insights for investors, industry professionals, and strategic decision-makers. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033, this report meticulously examines market trends, competitive dynamics, and future growth prospects. The market size is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period. This report features key players including China Minmetals Corporation, Eurasian Resources Group, Ferro Alloys Corporation Limited, Ferroglobe, Finnfjord, Mechel, OM Holdings Ltd, Shanghai Shenjia Ferroalloys Co Ltd, SKP Group, and Tashi Group (list not exhaustive).

Ferroalloys Industry Market Structure & Competitive Landscape

The ferroalloys market exhibits a moderately concentrated structure, with a few large players holding significant market share. The Herfindahl-Hirschman Index (HHI) is estimated at xx, indicating a moderately competitive landscape. Innovation is a key driver, with companies investing heavily in R&D to improve production efficiency, reduce environmental impact, and develop new product applications. Regulatory changes, particularly those related to environmental protection and trade, significantly influence market dynamics. Product substitutes, such as alternative materials in steelmaking, pose a moderate threat. The industry is segmented by product type (e.g., ferrochromium, ferromanganese, silicomanganese), application (e.g., steelmaking, foundry), and geography. M&A activity has been moderate in recent years, with a total transaction value of approximately xx Million during the historical period (2019-2024), primarily driven by efforts to expand market share and access new technologies.

- Market Concentration: Moderately concentrated, HHI estimated at xx.

- Innovation Drivers: R&D investments in efficiency, environmental sustainability, and new applications.

- Regulatory Impacts: Significant influence from environmental and trade regulations.

- Product Substitutes: Moderate threat from alternative materials.

- End-User Segmentation: Steelmaking dominates, followed by foundry and other applications.

- M&A Trends: Moderate activity, totaling approximately xx Million (2019-2024).

Ferroalloys Industry Market Trends & Opportunities

The global ferroalloys market is experiencing robust growth, driven by expanding steel production, particularly in developing economies. Technological advancements, such as the adoption of more efficient smelting technologies and improved alloy compositions, are enhancing productivity and product quality. Consumer preferences are shifting towards higher-performance alloys with improved properties, leading to increased demand for specialized ferroalloys. Competitive dynamics are characterized by price competition, product differentiation, and technological leadership. Market penetration rates vary significantly across different regions and applications, with higher penetration in mature markets and faster growth in emerging economies. The market size is projected to reach xx Million by 2033, with a CAGR of xx% during the forecast period (2025-2033). Significant opportunities exist in emerging markets with growing infrastructure development and increasing steel consumption.

Dominant Markets & Segments in Ferroalloys Industry

China holds the dominant position in the global ferroalloys market, accounting for approximately xx% of global production in 2024. This dominance is driven by its vast steel industry, robust infrastructure development, and supportive government policies. Other significant markets include India, the United States, and the European Union. Within the product segments, ferrochromium and ferromanganese account for the largest shares of the market due to their widespread use in steel production.

- Key Growth Drivers in China:

- Large-scale steel production

- Extensive infrastructure projects

- Government support for industrial growth

- Key Growth Drivers in India:

- Rapid industrialization

- Increasing steel consumption

- Government initiatives to boost infrastructure.

- Key Growth Drivers in the U.S.:

- Reshoring of manufacturing

- Focus on sustainable steel production

- Government investment in infrastructure

Ferroalloys Industry Product Analysis

The ferroalloys industry is witnessing continuous innovation in product development. Advancements in smelting technologies are leading to higher purity alloys, improved metallurgical properties, and reduced production costs. New alloy compositions are being developed to cater to specific application requirements, such as higher strength, corrosion resistance, and improved weldability. These innovations are enhancing the competitiveness of ferroalloys in various applications, particularly in advanced materials and high-technology industries. The development of high-purity silicon metal for batteries and solar applications represents a significant breakthrough, opening up new growth avenues for the industry.

Key Drivers, Barriers & Challenges in Ferroalloys Industry

Key Drivers: Growing global steel production, particularly in emerging economies; increasing demand for high-performance alloys; technological advancements in smelting and alloy composition; supportive government policies in key markets.

Challenges: Fluctuations in raw material prices; environmental regulations and carbon emission targets; intense competition; potential supply chain disruptions; geopolitical uncertainties impacting trade flows. The impact of these challenges is estimated to reduce the market growth rate by approximately xx% by 2033.

Growth Drivers in the Ferroalloys Industry Market

The ferroalloys market's growth is primarily driven by the expanding global steel industry, especially in developing nations. Technological progress in smelting processes enhances efficiency and reduces production costs, while the rising demand for higher-performance alloys with superior properties further fuels market expansion. Favorable government policies and infrastructure development projects in several regions contribute significantly to market growth.

Challenges Impacting Ferroalloys Industry Growth

The ferroalloys industry faces several challenges, including volatile raw material prices causing unpredictable production costs. Stricter environmental regulations and the need to meet carbon emission targets require substantial investments in cleaner technologies, adding to operational expenses. Intense competition among producers and potential supply chain disruptions due to geopolitical events present further headwinds to market growth.

Key Players Shaping the Ferroalloys Industry Market

- China Minmetals Corporation

- Eurasian Resources Group

- Ferro Alloys Corporation Limited

- Ferroglobe

- Finnfjord

- Mechel

- OM Holdings Ltd

- Shanghai Shenjia Ferroalloys Co Ltd

- SKP Group

- Tashi Group

Significant Ferroalloys Industry Milestones

- July 2022: Ferroglobe PLC achieves high-purity (up to 99.995%) silicon metal powder production for batteries and advanced technologies. This signifies a significant step towards meeting the growing demand for high-quality materials in the EV and energy storage sectors.

- June 2022: Ferroglobe PLC and REC Silicon sign an MOU to establish a low-carbon, traceable U.S.-based solar supply chain. This collaboration aims to address the increasing demand for sustainable solar energy solutions and improve the domestic supply chain's resilience.

Future Outlook for Ferroalloys Industry Market

The ferroalloys market is poised for continued growth, driven by sustained demand from the steel and related industries. Strategic investments in advanced technologies, coupled with a focus on sustainable production practices, will shape the industry's future trajectory. The expansion into new high-growth applications, such as electric vehicles and renewable energy, presents significant opportunities for market expansion and increased profitability. However, navigating the challenges of raw material price volatility and meeting stringent environmental regulations will remain crucial for long-term success.

Ferroalloys Industry Segmentation

-

1. Application

- 1.1. Metallurgy

- 1.2. Semiconductors

- 1.3. Photovoltaic Solar Energy

- 1.4. Chemical Processing

- 1.5. Other Applications

Ferroalloys Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Ferroalloys Industry Regional Market Share

Geographic Coverage of Ferroalloys Industry

Ferroalloys Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Applications for Corrosion Resistance; Growing Demand from Steel Production Industries

- 3.3. Market Restrains

- 3.3.1. Increasing Applications for Corrosion Resistance; Growing Demand from Steel Production Industries

- 3.4. Market Trends

- 3.4.1. Growing Demand from Metallurgy Industry

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Ferroalloys Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Metallurgy

- 5.1.2. Semiconductors

- 5.1.3. Photovoltaic Solar Energy

- 5.1.4. Chemical Processing

- 5.1.5. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Asia Pacific

- 5.2.2. North America

- 5.2.3. Europe

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Asia Pacific Ferroalloys Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Metallurgy

- 6.1.2. Semiconductors

- 6.1.3. Photovoltaic Solar Energy

- 6.1.4. Chemical Processing

- 6.1.5. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Ferroalloys Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Metallurgy

- 7.1.2. Semiconductors

- 7.1.3. Photovoltaic Solar Energy

- 7.1.4. Chemical Processing

- 7.1.5. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Ferroalloys Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Metallurgy

- 8.1.2. Semiconductors

- 8.1.3. Photovoltaic Solar Energy

- 8.1.4. Chemical Processing

- 8.1.5. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. South America Ferroalloys Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Metallurgy

- 9.1.2. Semiconductors

- 9.1.3. Photovoltaic Solar Energy

- 9.1.4. Chemical Processing

- 9.1.5. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East and Africa Ferroalloys Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Metallurgy

- 10.1.2. Semiconductors

- 10.1.3. Photovoltaic Solar Energy

- 10.1.4. Chemical Processing

- 10.1.5. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 China Minmetals Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Eurasian Resources Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Ferro Alloys Corporation Limited

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Ferroglobe

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Finnfjord

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Mechel

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 OM Holdings Ltd

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Shanghai Shenjia Ferroalloys Co Ltd

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 SKP Group

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tashi Group*List Not Exhaustive

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 China Minmetals Corporation

List of Figures

- Figure 1: Global Ferroalloys Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Ferroalloys Industry Revenue (undefined), by Application 2025 & 2033

- Figure 3: Asia Pacific Ferroalloys Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: Asia Pacific Ferroalloys Industry Revenue (undefined), by Country 2025 & 2033

- Figure 5: Asia Pacific Ferroalloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: North America Ferroalloys Industry Revenue (undefined), by Application 2025 & 2033

- Figure 7: North America Ferroalloys Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Ferroalloys Industry Revenue (undefined), by Country 2025 & 2033

- Figure 9: North America Ferroalloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Ferroalloys Industry Revenue (undefined), by Application 2025 & 2033

- Figure 11: Europe Ferroalloys Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Europe Ferroalloys Industry Revenue (undefined), by Country 2025 & 2033

- Figure 13: Europe Ferroalloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Ferroalloys Industry Revenue (undefined), by Application 2025 & 2033

- Figure 15: South America Ferroalloys Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: South America Ferroalloys Industry Revenue (undefined), by Country 2025 & 2033

- Figure 17: South America Ferroalloys Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Ferroalloys Industry Revenue (undefined), by Application 2025 & 2033

- Figure 19: Middle East and Africa Ferroalloys Industry Revenue Share (%), by Application 2025 & 2033

- Figure 20: Middle East and Africa Ferroalloys Industry Revenue (undefined), by Country 2025 & 2033

- Figure 21: Middle East and Africa Ferroalloys Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Ferroalloys Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 2: Global Ferroalloys Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 3: Global Ferroalloys Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Ferroalloys Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Ferroalloys Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 6: China Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 7: India Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Japan Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: South Korea Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Rest of Asia Pacific Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 11: Global Ferroalloys Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 12: Global Ferroalloys Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: United States Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Canada Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Mexico Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Ferroalloys Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Ferroalloys Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 18: Germany Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 19: United Kingdom Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: France Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: Italy Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Rest of Europe Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Global Ferroalloys Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 24: Global Ferroalloys Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 25: Brazil Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Argentina Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of South America Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Ferroalloys Industry Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Ferroalloys Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 30: Saudi Arabia Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 31: South Africa Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Rest of Middle East and Africa Ferroalloys Industry Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Ferroalloys Industry?

The projected CAGR is approximately 16.1%.

2. Which companies are prominent players in the Ferroalloys Industry?

Key companies in the market include China Minmetals Corporation, Eurasian Resources Group, Ferro Alloys Corporation Limited, Ferroglobe, Finnfjord, Mechel, OM Holdings Ltd, Shanghai Shenjia Ferroalloys Co Ltd, SKP Group, Tashi Group*List Not Exhaustive.

3. What are the main segments of the Ferroalloys Industry?

The market segments include Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Applications for Corrosion Resistance; Growing Demand from Steel Production Industries.

6. What are the notable trends driving market growth?

Growing Demand from Metallurgy Industry.

7. Are there any restraints impacting market growth?

Increasing Applications for Corrosion Resistance; Growing Demand from Steel Production Industries.

8. Can you provide examples of recent developments in the market?

July 2022: Ferroglobe PLC entered a new phase in its silicon metal powder project for batteries and other advanced technologies, reaching a high purity production (up to 99.995%) in micrometer and sub-micrometer size.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Ferroalloys Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Ferroalloys Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Ferroalloys Industry?

To stay informed about further developments, trends, and reports in the Ferroalloys Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence