Key Insights

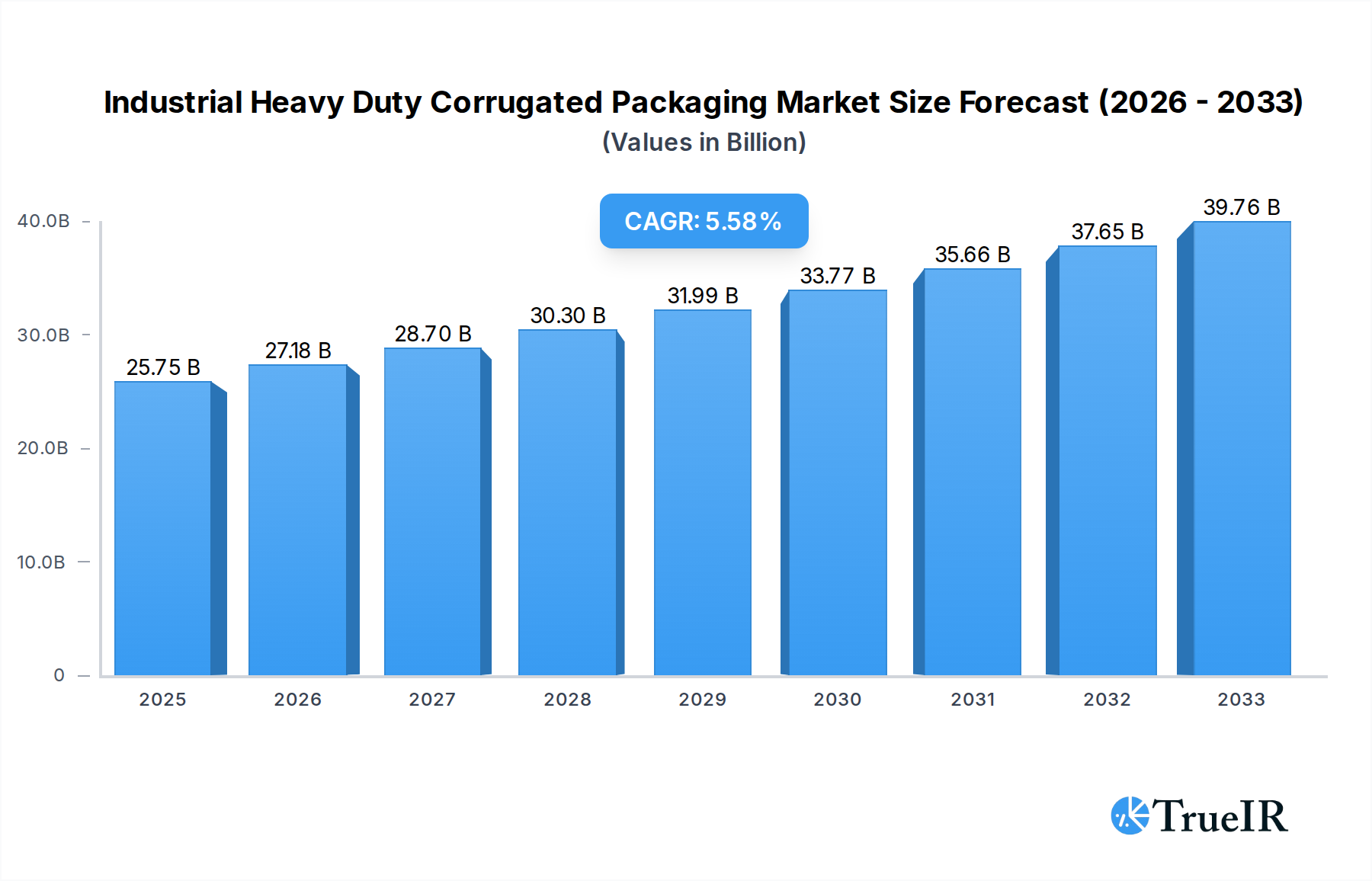

The Industrial Heavy Duty Corrugated Packaging market is poised for substantial growth, projected to reach $25.75 billion in 2025, with a robust Compound Annual Growth Rate (CAGR) of 5.57% through 2033. This expansion is fueled by the increasing demand for durable and sustainable packaging solutions across a spectrum of industries, including electronics, automotive parts, and heavy equipment. The inherent strength and protective capabilities of heavy-duty corrugated packaging make it an indispensable choice for safeguarding goods during transit and storage, particularly for products with significant weight and fragility. Key market drivers include the escalating global trade and e-commerce boom, which necessitates reliable packaging to prevent damage and reduce return rates. Furthermore, a growing emphasis on environmental responsibility is propelling the adoption of recyclable and biodegradable corrugated materials, aligning with sustainability goals and regulatory pressures. Innovations in material science and structural design are also contributing to enhanced performance, enabling the creation of packaging solutions that can withstand more extreme handling conditions and support heavier loads.

Industrial Heavy Duty Corrugated Packaging Market Size (In Billion)

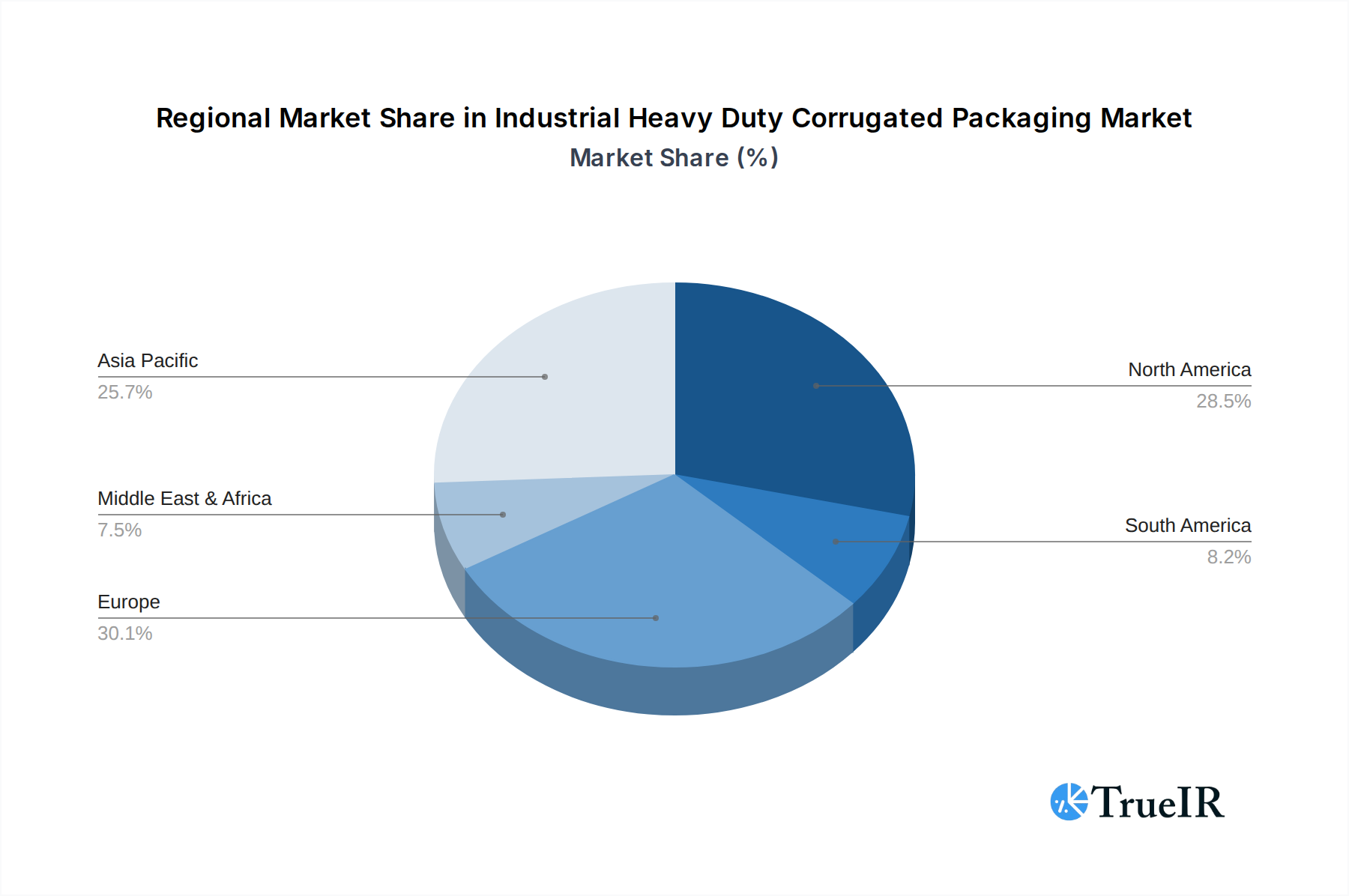

The market's trajectory is also influenced by evolving consumer and industrial expectations for efficient supply chains. Companies are increasingly prioritizing packaging that optimizes logistics, reduces shipping costs, and minimizes waste. This has led to a greater demand for customized heavy-duty corrugated solutions tailored to specific product dimensions and protection requirements. While the market is predominantly segmented by applications such as Electronics, Auto Parts, and Equipment Parts, the "Others" category, encompassing a wide array of industrial goods, also represents a significant growth area. Geographically, North America and Europe are leading markets due to established industrial bases and stringent quality standards. However, the Asia Pacific region is emerging as a critical growth engine, driven by rapid industrialization, burgeoning manufacturing sectors, and increasing investments in infrastructure. Despite the positive outlook, challenges such as raw material price volatility and the need for advanced manufacturing technologies to produce highly specialized designs may present some restraints, but the overarching demand for resilient and eco-friendly packaging is expected to propel sustained market expansion.

Industrial Heavy Duty Corrugated Packaging Company Market Share

Here is the SEO-optimized report description for Industrial Heavy Duty Corrugated Packaging, designed for immediate use without modification:

Industrial Heavy Duty Corrugated Packaging Market Structure & Competitive Landscape

The industrial heavy-duty corrugated packaging market is characterized by a moderately concentrated landscape, with key players like Smurfit Kappa, DS Smith, Mondi, and Stora Enso holding significant market shares. Innovation is a primary driver, focusing on enhanced strength, sustainability, and customizability to meet evolving industry demands for sectors such as auto parts and heavy equipment. Regulatory impacts, particularly concerning environmental standards and recycled content mandates, are shaping manufacturing processes and material sourcing. The threat of product substitutes, while present from rigid plastic and wooden crates, is mitigated by corrugated packaging's cost-effectiveness, recyclability, and adaptability for heavy-duty applications. End-user segmentation reveals strong demand from automotive, electronics, and industrial equipment sectors. Merger and acquisition (M&A) trends, with an estimated volume of over $5 billion in the historical period, indicate a strategic consolidation aimed at expanding geographic reach and product portfolios, further influencing market dynamics and competition.

Industrial Heavy Duty Corrugated Packaging Market Trends & Opportunities

The global industrial heavy-duty corrugated packaging market is experiencing robust growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 6.5% from 2019 to 2033, with the base year 2025 estimated to reach a valuation exceeding $50 billion. This growth is fueled by the escalating demand for durable and sustainable packaging solutions across a wide spectrum of industries. Technological shifts are paramount, with advancements in structural engineering of corrugated board, including multi-layer constructions and specialized coatings, enabling packaging to withstand immense loads and harsh transit conditions crucial for protecting electronics, auto parts, and heavy equipment. The increasing emphasis on e-commerce and global supply chains further propels the need for reliable, cost-effective, and environmentally friendly shipping solutions. Consumer preferences are increasingly tilting towards recyclable and biodegradable packaging materials, driving manufacturers to invest in sustainable practices and product development. Competitive dynamics are intensifying, with companies like GWP, Billerud, Rondo, SHISH, Piedmont National Corporation, Georgia-Pacific, and Rengo vying for market share through product innovation, strategic partnerships, and expanding production capacities. The market penetration rate for heavy-duty corrugated packaging is steadily increasing as industries recognize its superior performance-to-cost ratio compared to traditional alternatives. Opportunities abound in developing specialized packaging for niche applications, implementing smart packaging solutions for enhanced tracking and security, and expanding into emerging markets with developing industrial infrastructures. The drive towards circular economy principles is creating new avenues for innovation in material science and end-of-life management of corrugated packaging. The forecast period of 2025–2033 is expected to witness significant innovation in load-bearing capabilities, moisture resistance, and tamper-evident features, catering to increasingly complex logistical challenges.

Dominant Markets & Segments in Industrial Heavy Duty Corrugated Packaging

The global industrial heavy-duty corrugated packaging market is dominated by regions with robust industrial manufacturing bases and extensive logistics networks. North America and Europe currently lead in market share, driven by advanced economies with high demand for electronics, auto parts, and heavy equipment.

Application Dominance:

- Auto Parts: This segment is a significant growth driver due to the continuous production of vehicles and the global aftermarket. The need for robust packaging to protect sensitive and often heavy components during transit is paramount.

- Equipment Parts: Industrial machinery, construction equipment, and agricultural machinery parts demand highly durable and shock-absorbent packaging, making heavy-duty corrugated solutions indispensable.

- Electronics: While often perceived as fragile, high-value and large-format electronics also require substantial protection against impacts and vibrations during shipping, contributing to the growth of this segment.

- Others: This broad category encompasses a wide array of industrial goods, including chemicals, consumer durables, and oversized items, all of which benefit from the strength and cost-effectiveness of heavy-duty corrugated packaging.

Type Dominance:

- Three Layers: The three-layer corrugated board offers a superior balance of strength, cushioning, and cost-effectiveness, making it the preferred choice for most industrial heavy-duty applications. Its structural integrity is crucial for protecting heavier and more sensitive goods.

- Two Layers: While less prevalent for the heaviest loads, two-layer corrugated packaging finds applications where moderate strength is required, offering a more economical solution for certain auto parts and less demanding equipment components.

Key growth drivers in these dominant segments include increasing infrastructure development worldwide, supportive government policies promoting domestic manufacturing, and the growing trend of globalized supply chains that necessitate reliable and cost-efficient transportation solutions. The increasing complexity of product designs in the automotive and electronics sectors also demands sophisticated packaging designs that can be achieved with advanced corrugated structures.

Industrial Heavy Duty Corrugated Packaging Product Analysis

Innovations in industrial heavy-duty corrugated packaging are primarily focused on enhancing structural integrity, improving protection against environmental factors, and increasing sustainability. Advancements include the development of multi-wall corrugated structures with specialized liners, high-performance adhesives, and protective coatings to provide superior resistance to moisture, puncture, and impact. These product enhancements are crucial for the secure transport of critical components such as auto parts, heavy machinery parts, and high-value electronics. Competitive advantages stem from the material's inherent recyclability, cost-effectiveness compared to alternatives like wood or metal, and its customizable nature, allowing for tailored solutions to meet specific product protection needs and branding requirements.

Key Drivers, Barriers & Challenges in Industrial Heavy Duty Corrugated Packaging

Key Drivers:

- Economic Growth: Global industrial output and manufacturing expansion directly correlate with the demand for industrial packaging.

- E-commerce Proliferation: The surge in online retail for industrial goods necessitates robust and reliable shipping solutions.

- Sustainability Initiatives: Growing environmental awareness and regulations are pushing for recyclable and eco-friendly packaging.

- Technological Advancements: Innovations in corrugated board design offer enhanced strength and protective capabilities.

Barriers & Challenges:

- Supply Chain Volatility: Fluctuations in raw material prices (e.g., pulp, energy) and availability can impact production costs and lead times.

- Regulatory Complexities: Varying international regulations regarding packaging materials, import/export, and waste management can pose challenges.

- Competition from Alternatives: While cost-effective, corrugated packaging faces competition from plastics and other materials in specific niche applications.

- Logistical Constraints: Efficient transportation and warehousing of bulky heavy-duty packaging can sometimes be a challenge.

Growth Drivers in the Industrial Heavy Duty Corrugated Packaging Market

Growth in the industrial heavy-duty corrugated packaging market is primarily propelled by the expansion of global manufacturing sectors, particularly in automotive, electronics, and heavy machinery. The accelerating trend of e-commerce for industrial supplies also necessitates robust and protective packaging solutions. Furthermore, increasing governmental emphasis on sustainable practices and the circular economy is driving demand for recyclable and biodegradable packaging, where corrugated board excels. Technological innovations, such as the development of advanced multi-wall constructions and specialized coatings, are enhancing the performance and protective capabilities of heavy-duty corrugated packaging, making it a more attractive option for a wider range of applications.

Challenges Impacting Industrial Heavy Duty Corrugated Packaging Growth

The industrial heavy-duty corrugated packaging market faces several challenges that can impact its growth trajectory. Supply chain disruptions, including fluctuations in the availability and cost of raw materials like pulp and energy, can lead to increased production expenses and affect profitability. Regulatory complexities and inconsistencies across different regions regarding packaging standards, recyclability, and waste disposal can create operational hurdles for manufacturers and end-users. Intense competition from alternative packaging materials, such as rigid plastics and advanced composite materials, in certain specialized applications poses a continuous threat. Moreover, the inherent limitations in moisture resistance for standard corrugated board, without specialized treatments, can restrict its use in highly humid or wet environments.

Key Players Shaping the Industrial Heavy Duty Corrugated Packaging Market

Smurfit Kappa GWP DS Smith Mondi Stora Enso Billerud Rondo SHISH Piedmont National Corporation Georgia-Pacific Rengo

Significant Industrial Heavy Duty Corrugated Packaging Industry Milestones

- 2019: Increased focus on sustainable forestry practices and recycled content mandates by major packaging manufacturers.

- 2020: Accelerated adoption of advanced structural designs for enhanced load-bearing capacity in response to supply chain pressures.

- 2021: Significant investments in R&D for moisture-resistant coatings and high-strength corrugated board innovations.

- 2022: Mergers and acquisitions aimed at expanding global reach and diversifying product portfolios.

- 2023: Growing emphasis on smart packaging features for tracking and inventory management in industrial shipments.

- 2024: Development of specialized corrugated solutions for the electric vehicle battery transportation sector.

Future Outlook for Industrial Heavy Duty Corrugated Packaging Market

The future outlook for the industrial heavy-duty corrugated packaging market is exceptionally positive, driven by an intensified global demand for sustainable, cost-effective, and high-performance packaging solutions. Strategic opportunities lie in the continued innovation of advanced materials and designs that offer superior protection against environmental hazards and physical stresses, catering to the evolving needs of sectors like automotive and heavy equipment. The increasing global focus on the circular economy and reducing carbon footprints will further bolster the market’s reliance on recyclable corrugated packaging. Expansion into emerging economies with developing industrial infrastructures presents significant growth potential. The integration of smart technologies for enhanced traceability and supply chain visibility will also shape future market developments, promising a dynamic and expanding landscape for industrial heavy-duty corrugated packaging.

Industrial Heavy Duty Corrugated Packaging Segmentation

-

1. Application

- 1.1. Electronics

- 1.2. Auto Parts

- 1.3. Equipment Parts

- 1.4. Others

-

2. Types

- 2.1. Two Layers

- 2.2. Three Layers

Industrial Heavy Duty Corrugated Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Industrial Heavy Duty Corrugated Packaging Regional Market Share

Geographic Coverage of Industrial Heavy Duty Corrugated Packaging

Industrial Heavy Duty Corrugated Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.78% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Electronics

- 5.1.2. Auto Parts

- 5.1.3. Equipment Parts

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Two Layers

- 5.2.2. Three Layers

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Industrial Heavy Duty Corrugated Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Electronics

- 6.1.2. Auto Parts

- 6.1.3. Equipment Parts

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Two Layers

- 6.2.2. Three Layers

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Industrial Heavy Duty Corrugated Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Electronics

- 7.1.2. Auto Parts

- 7.1.3. Equipment Parts

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Two Layers

- 7.2.2. Three Layers

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Industrial Heavy Duty Corrugated Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Electronics

- 8.1.2. Auto Parts

- 8.1.3. Equipment Parts

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Two Layers

- 8.2.2. Three Layers

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Industrial Heavy Duty Corrugated Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Electronics

- 9.1.2. Auto Parts

- 9.1.3. Equipment Parts

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Two Layers

- 9.2.2. Three Layers

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Industrial Heavy Duty Corrugated Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Electronics

- 10.1.2. Auto Parts

- 10.1.3. Equipment Parts

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Two Layers

- 10.2.2. Three Layers

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Industrial Heavy Duty Corrugated Packaging Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Electronics

- 11.1.2. Auto Parts

- 11.1.3. Equipment Parts

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Two Layers

- 11.2.2. Three Layers

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Smurfit Kappa

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 GWP

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 DS Smith

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Mondi

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Stora Enso

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Billerud

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Rondo

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 SHISH

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Piedmont National Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Georgia-Pacific

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Rengo

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Smurfit Kappa

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Industrial Heavy Duty Corrugated Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Industrial Heavy Duty Corrugated Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Industrial Heavy Duty Corrugated Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Industrial Heavy Duty Corrugated Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Industrial Heavy Duty Corrugated Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Industrial Heavy Duty Corrugated Packaging?

The projected CAGR is approximately 5.78%.

2. Which companies are prominent players in the Industrial Heavy Duty Corrugated Packaging?

Key companies in the market include Smurfit Kappa, GWP, DS Smith, Mondi, Stora Enso, Billerud, Rondo, SHISH, Piedmont National Corporation, Georgia-Pacific, Rengo.

3. What are the main segments of the Industrial Heavy Duty Corrugated Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 78.5 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Industrial Heavy Duty Corrugated Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Industrial Heavy Duty Corrugated Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Industrial Heavy Duty Corrugated Packaging?

To stay informed about further developments, trends, and reports in the Industrial Heavy Duty Corrugated Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence