Key Insights

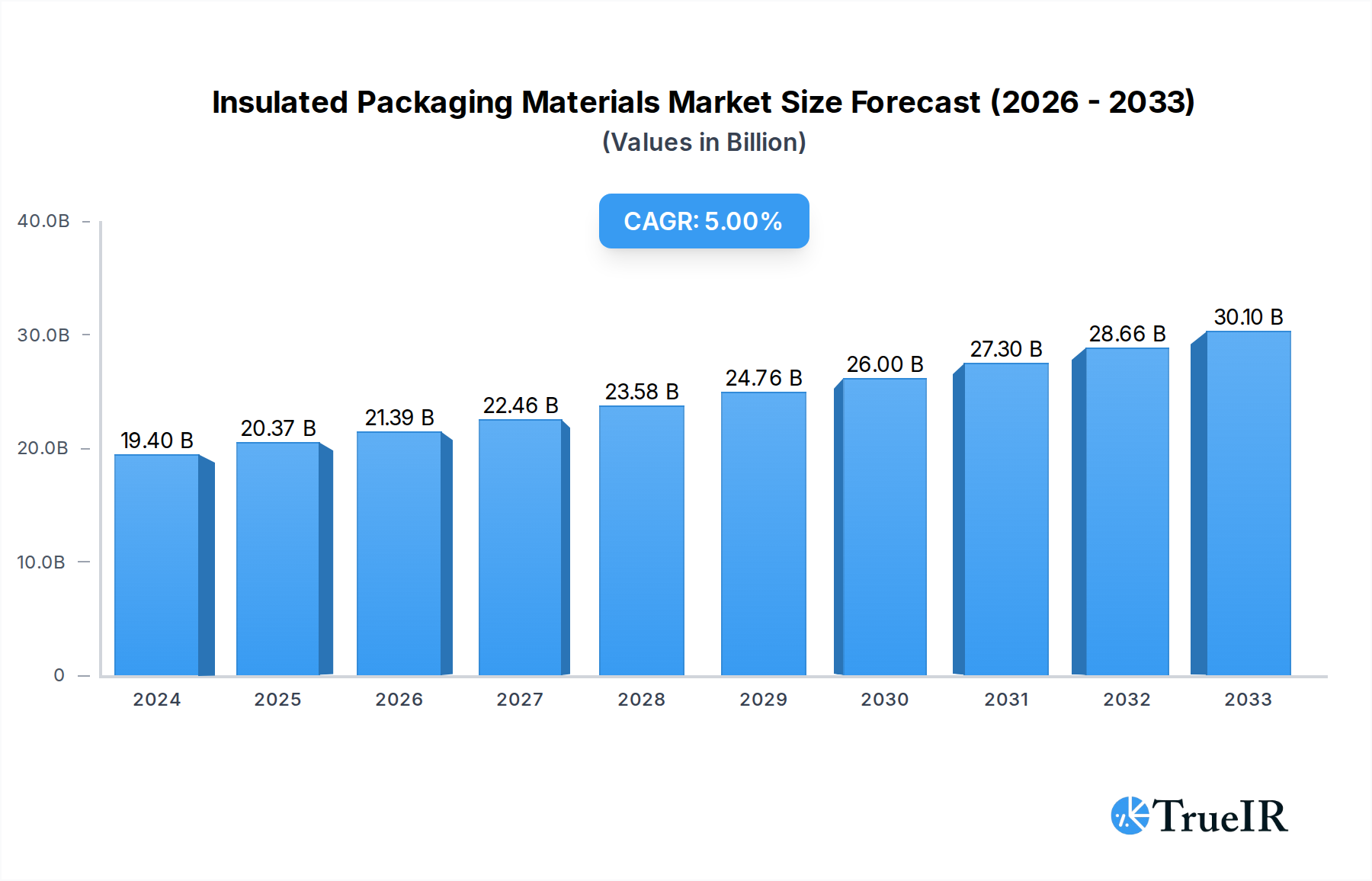

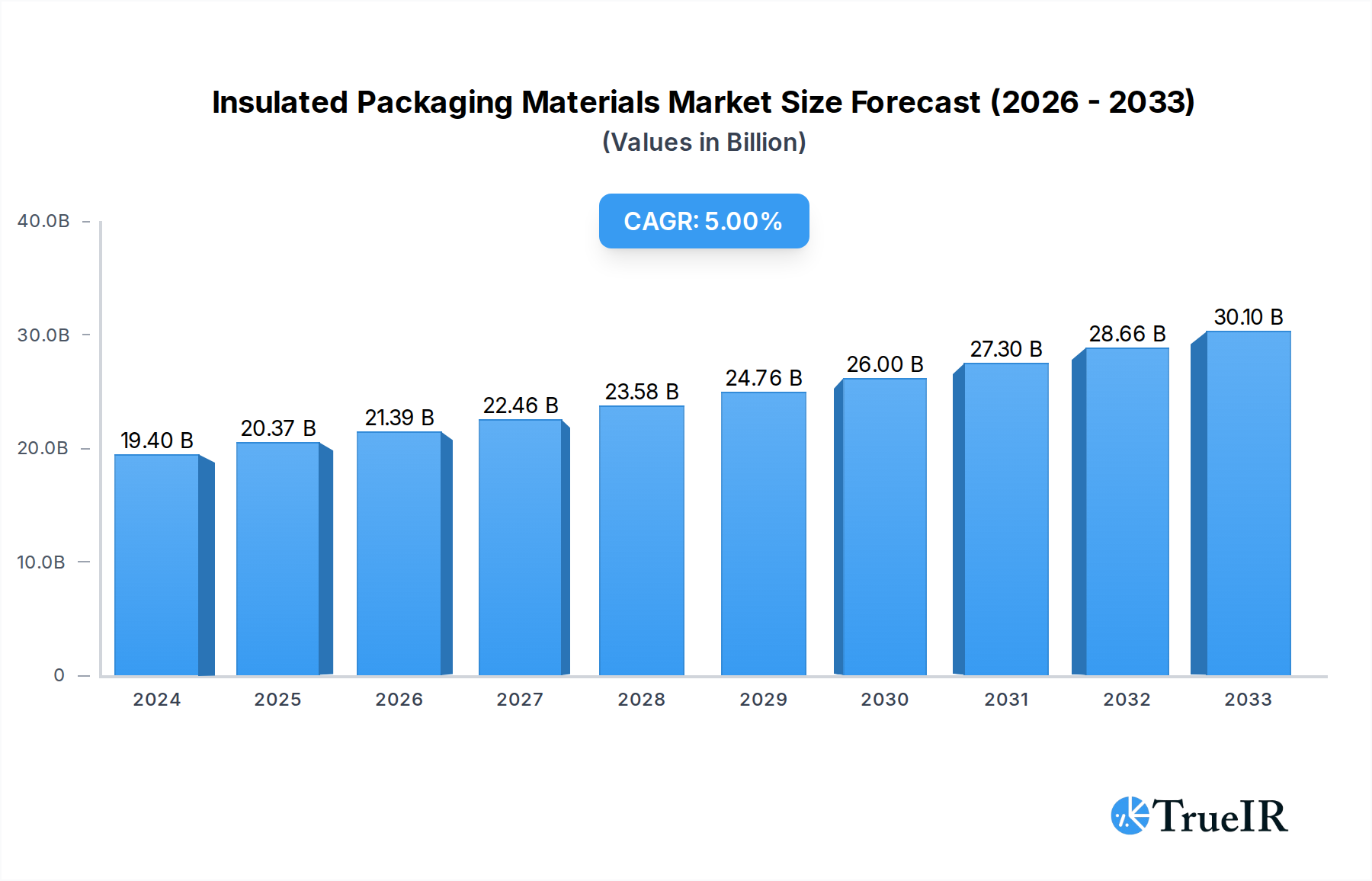

The global insulated packaging materials market is poised for significant expansion, projected to reach an estimated $19.4 billion in 2024, demonstrating a robust 5% Compound Annual Growth Rate (CAGR) through 2033. This upward trajectory is primarily fueled by the escalating demand for temperature-sensitive product protection across a multitude of sectors. The pharmaceutical industry stands out as a key driver, with the increasing global distribution of vaccines, biologics, and specialized medications necessitating reliable cold chain logistics. Similarly, the burgeoning e-commerce sector for groceries and meal kits, coupled with the growing consumer awareness regarding food safety and quality, is substantially boosting the demand for insulated packaging in the food and beverages segment. Furthermore, the cosmetic industry's focus on preserving product integrity, especially for high-value or temperature-sensitive formulations, also contributes to market growth. The overall expansion is underpinned by an increasing need for solutions that maintain specific temperature ranges during transit and storage, thereby minimizing spoilage, degradation, and efficacy loss.

Insulated Packaging Materials Market Size (In Billion)

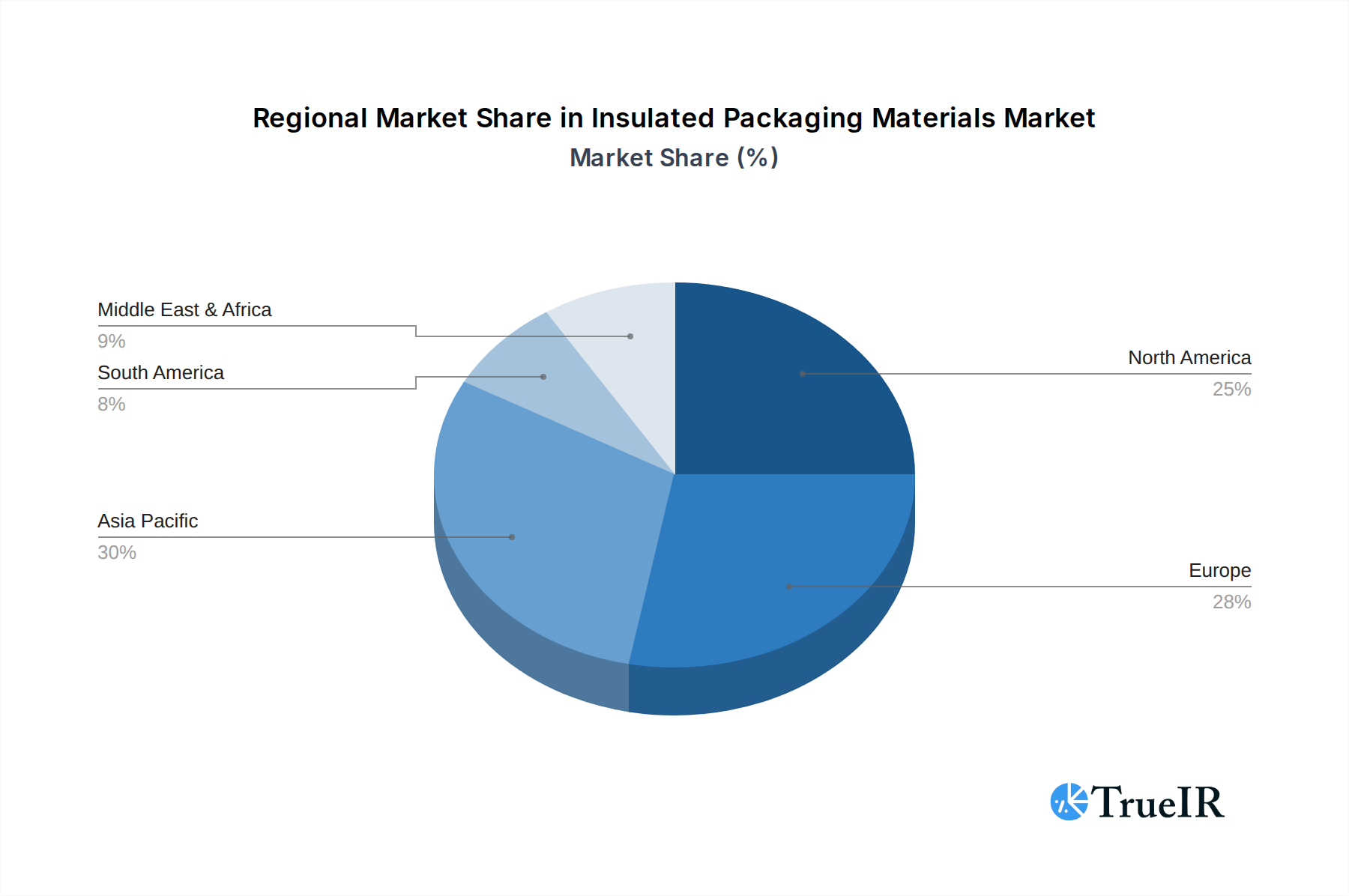

The market dynamics are further shaped by evolving trends in material innovation and sustainability. While traditional materials like plastic, wood, and corrugated cardboard continue to hold significant market share, there's a noticeable shift towards more eco-friendly and sustainable alternatives. Companies are increasingly investing in research and development to create bio-based, recyclable, and biodegradable insulated packaging solutions to align with environmental regulations and consumer preferences. This innovation is crucial in addressing market restraints such as the rising costs of raw materials and the logistical challenges associated with implementing sophisticated cold chain solutions, particularly in developing regions. Strategic collaborations and mergers among key players, such as Sealed Air and FEURER Group GmbH, are also shaping the competitive landscape, driving innovation and expanding market reach to cater to diverse regional demands across North America, Europe, Asia Pacific, and beyond.

Insulated Packaging Materials Company Market Share

Here's a dynamic, SEO-optimized report description for Insulated Packaging Materials, crafted with high-volume keywords and structured as requested.

This in-depth market research report provides a comprehensive analysis of the global Insulated Packaging Materials market, offering critical insights into its structure, dynamics, and future trajectory. With a detailed study period spanning from 2019 to 2033, including a base year of 2025 and a forecast period from 2025 to 2033, this report is an indispensable resource for stakeholders seeking to understand and capitalize on this rapidly evolving sector. The analysis delves into market size growth, technological innovations, shifting consumer preferences, and the intricate competitive landscape. We examine key market drivers, barriers, and challenges, alongside dominant market segments and product innovations, providing a holistic view of the industry.

Insulated Packaging Materials Market Structure & Competitive Landscape

The global insulated packaging materials market is characterized by a moderately consolidated structure, with a few key players holding significant market share. Major companies such as Sealed Air, FEURER Group GmbH, Sancell, The Wool Packaging Company Limited, CoolPac, Cascades Inc., ICEE Containers Pty Ltd, TemperPack, Icertech, and Insulated Products Corporation are at the forefront of innovation and market expansion. Innovation drivers are primarily centered around sustainability, enhanced thermal performance, and cost-effectiveness. Regulatory impacts, particularly those concerning environmental compliance and material safety, play a crucial role in shaping product development and market entry strategies. The availability of product substitutes, ranging from traditional insulation to advanced materials, presents both opportunities and challenges. End-user segmentation across Pharmaceutical, Food and Beverages, Cosmetic, Industrial, and Other applications reveals diverse demand patterns. Mergers and acquisitions (M&A) are a significant trend, with an estimated XXX billion in M&A volumes observed historically, indicating strategic consolidation and expansion efforts by leading enterprises aiming to enhance their product portfolios and geographical reach. For instance, the acquisition of smaller specialty packaging firms by larger corporations has been a recurring theme, boosting their market penetration and technological capabilities.

Insulated Packaging Materials Market Trends & Opportunities

The insulated packaging materials market is poised for substantial growth, driven by escalating demand across diverse applications and a growing emphasis on maintaining product integrity during transit and storage. The market size is projected to reach an impressive XXX billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX.XX% from the base year 2025. Key industry developments are shaping the market landscape, with a discernible shift towards sustainable and eco-friendly packaging solutions. This trend is fueled by increasing consumer awareness and stringent environmental regulations, pushing manufacturers to explore biodegradable and recyclable materials such as advanced molded pulp and plant-based foams. Technological advancements are also playing a pivotal role, with ongoing research and development focused on improving thermal insulation properties, increasing durability, and reducing the overall carbon footprint of packaging solutions. The integration of smart technologies, such as temperature monitoring sensors within packaging, is also emerging as a significant innovation, particularly for high-value sensitive goods like pharmaceuticals and specialized food products.

Consumer preferences are increasingly leaning towards packaging that offers superior protection against temperature fluctuations, thereby minimizing product spoilage and waste. This is especially evident in the pharmaceutical and food and beverage sectors, where the integrity of the product is paramount. The pharmaceutical industry, in particular, relies heavily on insulated packaging for the safe transportation of vaccines, biologics, and temperature-sensitive drugs, a segment expected to witness robust growth. Similarly, the food and beverage industry, driven by the expansion of e-commerce and the growing demand for fresh and frozen food delivery, presents a significant market opportunity for effective insulated packaging solutions.

The competitive dynamics are intensifying, with both established players and emerging startups vying for market share. Companies are investing heavily in research and development to introduce innovative materials and designs that offer enhanced performance and sustainability. Strategic collaborations and partnerships are also on the rise, as companies aim to leverage each other's expertise and expand their market reach. The expanding e-commerce sector, coupled with the increasing globalization of supply chains, further amplifies the demand for reliable and efficient insulated packaging solutions. Market penetration rates are expected to increase across all segments, as more businesses recognize the critical role of proper insulation in preserving product quality, reducing waste, and meeting regulatory requirements. The forecast period from 2025 to 2033 is anticipated to witness a surge in demand for customized and high-performance insulated packaging, catering to the specific needs of various industries and applications.

Dominant Markets & Segments in Insulated Packaging Materials

The Pharmaceutical application segment is identified as a dominant force within the global insulated packaging materials market. This dominance is driven by the stringent regulatory requirements and the inherent sensitivity of pharmaceutical products to temperature excursions. The critical need to maintain the efficacy and safety of vaccines, biologics, and temperature-sensitive drugs throughout the cold chain necessitates the use of high-performance insulated packaging. Key growth drivers in this segment include the expanding global healthcare infrastructure, the increasing development and distribution of biopharmaceuticals, and the growing prevalence of chronic diseases requiring specialized medication management. Policies promoting vaccine accessibility and the cold chain infrastructure development for drug distribution further bolster this segment's growth.

The Food and Beverages segment also represents a significant and rapidly expanding market. The surge in online grocery shopping, the demand for fresh and frozen meal delivery services, and the global expansion of the chilled and frozen food market are major contributors. The need to preserve the quality, freshness, and safety of perishable food items, from dairy and meat products to ready-to-eat meals, is driving the adoption of effective insulated packaging solutions. Growth drivers include evolving consumer lifestyles, increasing disposable incomes, and the expansion of cold chain logistics for food distribution. Government initiatives focused on reducing food waste also indirectly support the demand for superior insulated packaging.

From a Type perspective, Plastic insulated packaging materials, including expanded polystyrene (EPS) and polyurethane (PU) foams, continue to hold a substantial market share due to their excellent insulation properties, cost-effectiveness, and durability. However, there is a notable and growing trend towards more sustainable alternatives. Corrugated Cardboard insulated packaging, often enhanced with natural insulation materials like paper or molded pulp, is gaining traction as a more environmentally friendly option, driven by sustainability mandates and corporate social responsibility initiatives. The Others category, encompassing materials like molded pulp and natural fibers such as wool, is experiencing significant growth, reflecting the industry's commitment to innovation and eco-conscious solutions.

Geographically, North America and Europe are currently dominant markets, owing to their well-established pharmaceutical and food industries, advanced cold chain logistics, and stringent quality control regulations. However, the Asia-Pacific region is projected to exhibit the highest growth rate in the forecast period, driven by rapid industrialization, a burgeoning middle class with increasing demand for perishable goods, and significant investments in healthcare and e-commerce infrastructure. Key growth drivers in this region include government policies supporting the development of logistics and cold chain capabilities, and the increasing adoption of advanced packaging technologies by local manufacturers.

Insulated Packaging Materials Product Analysis

Product innovations in insulated packaging materials are largely driven by the dual demands of enhanced thermal performance and sustainability. Companies are developing advanced materials that offer superior insulation with reduced thickness and weight, leading to cost savings in shipping and reduced material usage. Examples include advanced vacuum insulated panels (VIPs) for critical temperature control applications, and novel bio-based foams derived from corn starch or sugarcane, offering comparable insulation to traditional plastics with a significantly lower environmental impact. The competitive advantage lies in offering tailored solutions for specific temperature ranges and durations, catering to the precise needs of the pharmaceutical and high-value food sectors. Integration of features like moisture resistance and tamper-evident seals further enhances product appeal and market fit.

Key Drivers, Barriers & Challenges in Insulated Packaging Materials

Key Drivers:

- Growing E-commerce and Cold Chain Logistics: The expansion of online retail, particularly for groceries and pharmaceuticals, necessitates reliable insulated packaging to maintain product integrity.

- Demand for Sustainable Packaging: Increasing consumer and regulatory pressure for eco-friendly solutions is driving innovation in biodegradable and recyclable insulated materials.

- Strict Temperature Control Requirements: The pharmaceutical and biotech industries have stringent needs for maintaining specific temperature ranges during transport, boosting demand for high-performance insulation.

- Food Safety Regulations: Enhanced regulations concerning food spoilage and safety are compelling food producers and distributors to invest in superior insulated packaging.

- Technological Advancements: Innovations in material science and manufacturing processes are leading to more efficient, cost-effective, and sustainable insulated packaging options.

Barriers and Challenges:

- Cost of Advanced Materials: High-performance and sustainable insulated packaging materials can sometimes be more expensive than traditional options, posing a barrier for price-sensitive segments.

- Supply Chain Disruptions: Global supply chain volatility and the availability of raw materials can impact production costs and lead times for insulated packaging manufacturers.

- Regulatory Complexities: Navigating diverse and evolving environmental regulations across different regions can be challenging for global players. For example, varying restrictions on plastic use can necessitate frequent product reformulation.

- Competitive Pressures: Intense competition among established players and new entrants can lead to price wars and pressure on profit margins.

- End-of-Life Management: While efforts are being made to improve recyclability, the disposal and end-of-life management of some insulated packaging materials remain a challenge, impacting overall sustainability perceptions.

Growth Drivers in the Insulated Packaging Materials Market

The insulated packaging materials market is propelled by several significant growth drivers. Technological advancements are at the forefront, with continuous innovation in material science leading to the development of more efficient and sustainable insulation solutions. For example, the introduction of next-generation vacuum insulated panels (VIPs) offers superior thermal performance with a reduced material footprint, catering to stringent temperature control needs. Economically, the burgeoning global e-commerce sector, particularly for perishable goods like pharmaceuticals and fresh foods, is a massive growth catalyst. Policy-driven initiatives aimed at reducing food waste and promoting sustainable packaging practices globally are further encouraging the adoption of advanced insulated solutions. The increasing emphasis on supply chain resilience and the need to mitigate product spoilage in transit are also key economic factors driving market expansion.

Challenges Impacting Insulated Packaging Materials Growth

The growth of the insulated packaging materials market is not without its hurdles. Regulatory complexities, particularly concerning the use of plastics and waste disposal, can present significant challenges for manufacturers operating in diverse global markets. For instance, varying regulations on single-use plastics necessitate adaptive product development and market strategies. Supply chain issues, including raw material availability and price volatility, can impact production costs and lead times. Competitive pressures are intense, with a crowded market of established players and emerging innovators constantly vying for market share, which can lead to price erosion. Furthermore, the perceived higher cost of some advanced or sustainable insulated packaging solutions compared to conventional alternatives can act as a restraint, especially for smaller businesses or price-sensitive markets. The effective implementation and management of end-of-life disposal and recycling programs for these materials also remain an ongoing challenge.

Key Players Shaping the Insulated Packaging Materials Market

- Sealed Air

- FEURER Group GmbH

- Sancell

- The Wool Packaging Company Limited

- CoolPac

- Cascades Inc.

- ICEE Containers Pty Ltd

- TemperPack

- Icertech

- Insulated Products Corporation

Significant Insulated Packaging Materials Industry Milestones

- 2020: Launch of advanced biodegradable molded pulp solutions by key players, addressing growing sustainability demands.

- 2021: Increased adoption of vacuum insulated panels (VIPs) in pharmaceutical cold chain logistics for ultra-low temperature shipments.

- 2022: Significant investment in R&D for plant-based and compostable insulation materials, signaling a shift away from traditional plastics.

- 2023: Expansion of e-commerce packaging solutions by major companies, including integrated temperature monitoring features.

- 2023: Strategic mergers and acquisitions to consolidate market share and expand technological capabilities in specialized insulation materials.

- 2024: Rollout of innovative corrugated cardboard insulation with enhanced thermal barrier properties.

- 2024: Development of smart packaging solutions with embedded IoT sensors for real-time temperature tracking.

Future Outlook for Insulated Packaging Materials Market

The future outlook for the insulated packaging materials market is exceptionally promising, fueled by an confluence of compelling growth catalysts. The relentless expansion of e-commerce, coupled with the increasing demand for temperature-sensitive products such as pharmaceuticals and specialty foods, will continue to be a primary growth engine. Strategic opportunities lie in the ongoing development and commercialization of truly sustainable and circular economy-aligned packaging solutions, including advanced bioplastics, recycled content integration, and enhanced biodegradability. Market potential is also significant in emerging economies where cold chain infrastructure is rapidly developing. Companies that can offer cost-effective, high-performance, and environmentally responsible insulated packaging solutions are poised for substantial growth and market leadership in the coming years.

Insulated Packaging Materials Segmentation

-

1. Application

- 1.1. Pharmaceutical

- 1.2. Food and Beverages

- 1.3. Cosmetic

- 1.4. Industrial

- 1.5. Others

-

2. Type

- 2.1. Plastic

- 2.2. Wood

- 2.3. Corrugated Cardboard

- 2.4. Others

Insulated Packaging Materials Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Insulated Packaging Materials Regional Market Share

Geographic Coverage of Insulated Packaging Materials

Insulated Packaging Materials REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pharmaceutical

- 5.1.2. Food and Beverages

- 5.1.3. Cosmetic

- 5.1.4. Industrial

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Plastic

- 5.2.2. Wood

- 5.2.3. Corrugated Cardboard

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Insulated Packaging Materials Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pharmaceutical

- 6.1.2. Food and Beverages

- 6.1.3. Cosmetic

- 6.1.4. Industrial

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Plastic

- 6.2.2. Wood

- 6.2.3. Corrugated Cardboard

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Insulated Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pharmaceutical

- 7.1.2. Food and Beverages

- 7.1.3. Cosmetic

- 7.1.4. Industrial

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Plastic

- 7.2.2. Wood

- 7.2.3. Corrugated Cardboard

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Insulated Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pharmaceutical

- 8.1.2. Food and Beverages

- 8.1.3. Cosmetic

- 8.1.4. Industrial

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Plastic

- 8.2.2. Wood

- 8.2.3. Corrugated Cardboard

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Insulated Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pharmaceutical

- 9.1.2. Food and Beverages

- 9.1.3. Cosmetic

- 9.1.4. Industrial

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Plastic

- 9.2.2. Wood

- 9.2.3. Corrugated Cardboard

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Insulated Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pharmaceutical

- 10.1.2. Food and Beverages

- 10.1.3. Cosmetic

- 10.1.4. Industrial

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Plastic

- 10.2.2. Wood

- 10.2.3. Corrugated Cardboard

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Insulated Packaging Materials Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Pharmaceutical

- 11.1.2. Food and Beverages

- 11.1.3. Cosmetic

- 11.1.4. Industrial

- 11.1.5. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Plastic

- 11.2.2. Wood

- 11.2.3. Corrugated Cardboard

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Sealed Air

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 FEURER Group GmbH

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Sancell

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 The Wool Packaging Company Limited

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 CoolPac

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Cascades Inc.

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 ICEE Containers Pty Ltd

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 TemperPack

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Icertech

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Insulated Products Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.1 Sealed Air

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Insulated Packaging Materials Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Insulated Packaging Materials Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Insulated Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Insulated Packaging Materials Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Insulated Packaging Materials Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Insulated Packaging Materials Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Insulated Packaging Materials Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Insulated Packaging Materials Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Insulated Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Insulated Packaging Materials Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Insulated Packaging Materials Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Insulated Packaging Materials Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Insulated Packaging Materials Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Insulated Packaging Materials Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Insulated Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Insulated Packaging Materials Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Insulated Packaging Materials Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Insulated Packaging Materials Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Insulated Packaging Materials Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Insulated Packaging Materials Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Insulated Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Insulated Packaging Materials Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Insulated Packaging Materials Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Insulated Packaging Materials Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Insulated Packaging Materials Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Insulated Packaging Materials Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Insulated Packaging Materials Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Insulated Packaging Materials Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Insulated Packaging Materials Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Insulated Packaging Materials Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Insulated Packaging Materials Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Insulated Packaging Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Insulated Packaging Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Insulated Packaging Materials Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Insulated Packaging Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Insulated Packaging Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Insulated Packaging Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Insulated Packaging Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Insulated Packaging Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Insulated Packaging Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Insulated Packaging Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Insulated Packaging Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Insulated Packaging Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Insulated Packaging Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Insulated Packaging Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Insulated Packaging Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Insulated Packaging Materials Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Insulated Packaging Materials Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Insulated Packaging Materials Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Insulated Packaging Materials Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Insulated Packaging Materials?

The projected CAGR is approximately 5%.

2. Which companies are prominent players in the Insulated Packaging Materials?

Key companies in the market include Sealed Air, FEURER Group GmbH, Sancell, The Wool Packaging Company Limited, CoolPac, Cascades Inc., ICEE Containers Pty Ltd, TemperPack, Icertech, Insulated Products Corporation.

3. What are the main segments of the Insulated Packaging Materials?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 17.41 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Insulated Packaging Materials," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Insulated Packaging Materials report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Insulated Packaging Materials?

To stay informed about further developments, trends, and reports in the Insulated Packaging Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence