Key Insights

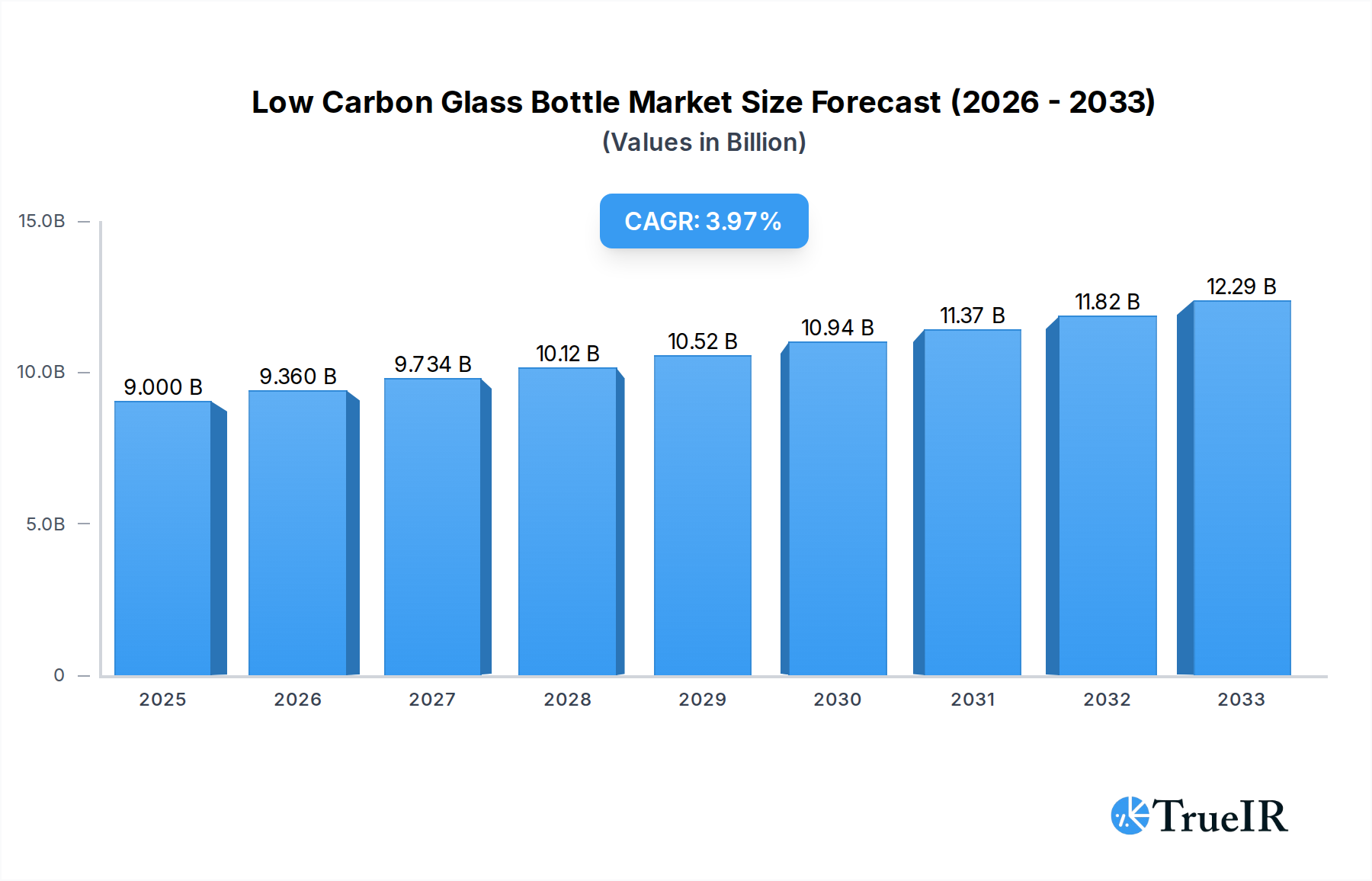

The global Low Carbon Glass Bottle market is poised for significant expansion, with an estimated market size of $9 billion in 2025. This growth is underpinned by a robust Compound Annual Growth Rate (CAGR) of 4% projected over the forecast period of 2025-2033. The increasing consumer and regulatory demand for sustainable packaging solutions is the primary catalyst driving this market. As industries worldwide face mounting pressure to reduce their carbon footprint, glass bottles, with their inherent recyclability and lower environmental impact compared to single-use plastics, are emerging as a preferred choice. Innovations in manufacturing processes, focusing on reducing energy consumption and utilizing recycled materials, are further enhancing the appeal and viability of low carbon glass bottles. The Food & Beverage industry, a dominant consumer of glass packaging, is leading the adoption of these sustainable alternatives, driven by evolving consumer preferences for eco-friendly products. The Medical sector also presents a growing opportunity, where the inert nature and recyclability of glass align with stringent healthcare standards and sustainability goals.

Low Carbon Glass Bottle Market Size (In Billion)

The market's trajectory is further shaped by several key trends. A prominent one is the advancement in lightweighting technologies, which reduces the amount of raw material and energy required for production without compromising bottle integrity. Increased investment in recycling infrastructure and improved collection rates are also crucial drivers, creating a more circular economy for glass packaging. Moreover, the development of novel low-emission manufacturing techniques, such as those employing hydrogen or electric furnaces, is playing a vital role in achieving genuine low-carbon production. However, the market faces certain restraints. The initial capital investment for adopting new low-carbon manufacturing technologies can be substantial, posing a hurdle for smaller players. Additionally, the energy intensity of glass production, even with advancements, remains a factor that needs continuous innovation to mitigate. Fluctuations in raw material costs, particularly for soda ash and silica sand, can also impact production expenses. Despite these challenges, the overarching shift towards sustainability and the inherent advantages of glass packaging are expected to propel the Low Carbon Glass Bottle market forward.

Low Carbon Glass Bottle Company Market Share

Here's a dynamic, SEO-optimized report description for the Low Carbon Glass Bottle Market, incorporating your specified details and structure.

Unlock the Future of Sustainable Packaging: A Comprehensive Analysis of the Global Low Carbon Glass Bottle Market (2019–2033)

This in-depth market research report provides a definitive analysis of the rapidly evolving Low Carbon Glass Bottle market. Delving into the period from 2019 to 2033, with a base year of 2025 and a forecast period extending from 2025 to 2033, this report offers unparalleled insights into market dynamics, growth opportunities, and competitive strategies. Leveraging high-volume keywords and an extensive dataset, this report is designed to enhance search rankings and engage key industry stakeholders, including manufacturers, suppliers, investors, and policymakers. The global market for low carbon glass bottles is projected to experience substantial growth, driven by increasing environmental consciousness, stringent regulations, and a growing demand for sustainable packaging solutions across diverse applications. The market size is expected to reach hundreds of billions by 2033.

Low Carbon Glass Bottle Market Structure & Competitive Landscape

The Low Carbon Glass Bottle Market is characterized by a moderate to high concentration, with key players like Verallia, Ardagh Glass Packaging, OI Glass, Encirc, Vidrala, Wiegand-Glas, Bacardi, and Molson Coors actively shaping its trajectory. Innovation is a primary driver, fueled by advancements in manufacturing processes, material science, and the integration of renewable energy sources in production. Regulatory impacts are significant, with governmental policies promoting circular economy principles and carbon emission reductions directly influencing market growth. Product substitutes, such as plastics and aluminum, pose a competitive challenge, but the superior sustainability credentials and premium appeal of glass are increasingly favored by consumers and brands. End-user segmentation reveals a dominant presence of the Food & Beverage Industry, followed by Medical applications and Others. Mergers and acquisitions (M&A) are a notable trend, with an estimated tens to hundreds of billions in deal values over the historical period, aimed at consolidating market share, expanding product portfolios, and enhancing technological capabilities. The competitive landscape is dynamic, with companies investing heavily in R&D to develop lighter-weight bottles, incorporate higher percentages of recycled glass (cullet), and optimize energy efficiency in their operations.

Low Carbon Glass Bottle Market Trends & Opportunities

The global Low Carbon Glass Bottle Market is poised for remarkable expansion, with an estimated compound annual growth rate (CAGR) of X.X% during the forecast period. This robust growth is underpinned by a confluence of powerful market trends and emerging opportunities that are redefining the packaging landscape. The overarching trend is the unequivocal shift towards sustainability. Consumers worldwide are increasingly making purchasing decisions based on environmental impact, creating a strong demand for products packaged in eco-friendly materials. This consumer-driven demand directly translates into a preference for low carbon glass bottles, which offer a significantly lower carbon footprint compared to traditional glass manufacturing. Furthermore, stringent environmental regulations enacted by governments globally are acting as powerful catalysts for the adoption of sustainable packaging. Policies aimed at reducing carbon emissions, promoting recycling, and fostering a circular economy are compelling manufacturers to invest in and utilize low carbon glass bottle solutions. The Food & Beverage Industry, a primary segment, is at the forefront of this transition, with major brands actively seeking to enhance their corporate social responsibility (CSR) profiles by adopting greener packaging. This includes a surge in demand for Drink Bottles and Wine Bottles manufactured with reduced emissions.

Technological advancements are also playing a pivotal role in unlocking market potential. Innovations in glass manufacturing, such as the increased use of electric furnaces powered by renewable energy, advanced insulation techniques, and the development of lighter yet stronger bottle designs, are significantly reducing the carbon intensity of production. The integration of artificial intelligence (AI) and automation in production lines is further optimizing efficiency and minimizing waste. The Medical sector is another key area for growth, where the inertness and perceived hygiene of glass, combined with a growing emphasis on sustainable healthcare practices, are driving adoption. The Others segment, encompassing cosmetics, pharmaceuticals, and specialty goods, also presents significant untapped opportunities as brands across various sectors seek to align with eco-conscious consumer values. The increasing focus on recycling infrastructure and closed-loop systems further bolsters the appeal of glass bottles, enhancing their circularity and reducing the need for virgin materials. Market penetration rates for low carbon glass bottles are steadily increasing, indicating a substantial shift away from less sustainable alternatives. The industry is witnessing proactive collaborations between glass manufacturers, brand owners, and recycling organizations to create robust and efficient supply chains for recycled glass, further enhancing the economic and environmental viability of low carbon glass bottles. The development of new glass compositions that require lower melting temperatures also presents a significant avenue for reduced energy consumption and, consequently, a lower carbon footprint. The market penetration is expected to cross XX% by 2033. The global market size is projected to reach hundreds of billions by the end of the forecast period.

Dominant Markets & Segments in Low Carbon Glass Bottle

The Food & Beverage Industry stands as the undisputed dominant segment within the Low Carbon Glass Bottle Market, driven by extensive global consumption and a strong brand commitment to sustainability. Within this broad category, Drink Bottles and Wine Bottles represent the largest sub-segments, directly benefiting from consumer preferences for environmentally conscious packaging and the inherent premium image associated with glass. The Medical segment is emerging as a significant growth area, propelled by the stringent requirements for product integrity and the increasing adoption of sustainable practices in healthcare. The Others segment, encompassing cosmetics, perfumes, and specialty food items, also contributes to market demand as brands leverage low carbon glass bottles to enhance their eco-friendly appeal.

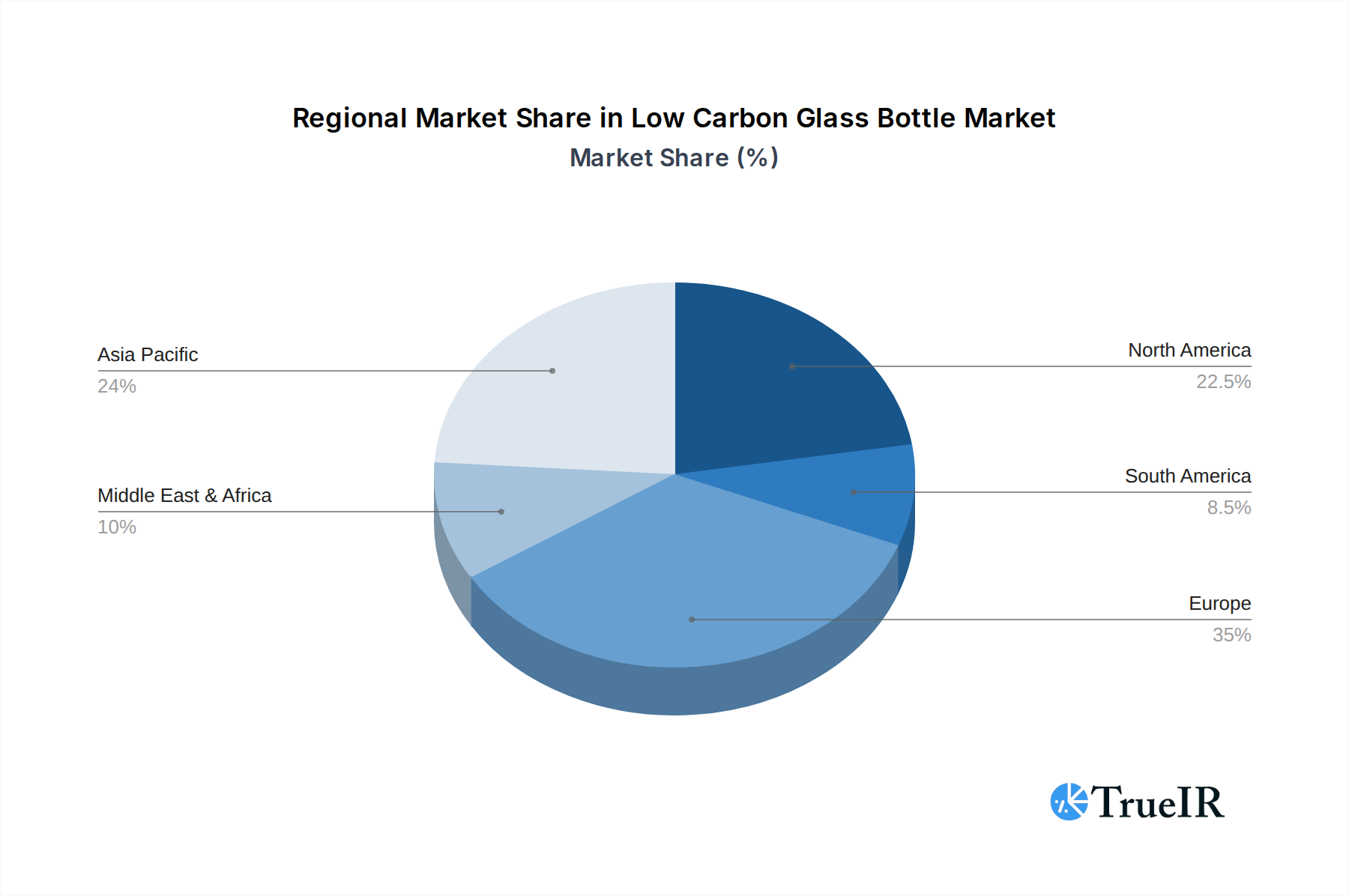

Geographically, Europe currently holds a dominant position, largely due to its proactive environmental policies, advanced recycling infrastructure, and a highly aware consumer base. Countries like Germany, France, and the UK are leading the charge in adopting sustainable packaging solutions. North America is rapidly catching up, with increasing regulatory pressure and growing consumer demand fueling market expansion. Asia Pacific is anticipated to exhibit the highest growth rate, driven by rapid industrialization, increasing environmental awareness, and the burgeoning middle class.

Key growth drivers for market dominance include:

- Stringent Environmental Regulations: Policies mandating carbon emission reductions and promoting circular economy principles are compelling industries to adopt low carbon packaging.

- Consumer Demand for Sustainability: Growing environmental consciousness among consumers translates into a preference for eco-friendly products, influencing brand packaging choices.

- Corporate Social Responsibility (CSR) Initiatives: Major corporations are investing in sustainable packaging to enhance their brand image and meet ESG (Environmental, Social, and Governance) goals.

- Advancements in Glass Manufacturing Technology: Innovations leading to lighter-weight bottles, increased use of recycled cullet, and energy-efficient production processes are making low carbon glass bottles more competitive.

- Superior Product Protection and Premium Appeal: Glass offers excellent barrier properties, preserves product quality, and conveys a premium perception, which is vital for many food, beverage, and cosmetic products.

The United States is expected to emerge as a leading country in terms of market size and growth within North America, driven by significant investments in sustainable infrastructure and a large consumer market. In the Food & Beverage Industry, the demand for beverage bottles, particularly for water, soft drinks, beer, and wine, is a primary growth catalyst. The increasing popularity of craft beverages further fuels the demand for aesthetically pleasing and sustainable glass packaging. The medical sector's reliance on sterile, inert, and non-reactive packaging makes glass a preferred material, and the shift towards sustainability in healthcare further solidifies the position of low carbon glass bottles in this segment. The Food & Beverage Industry is projected to contribute hundreds of billions to the global market value by 2033.

Low Carbon Glass Bottle Product Analysis

Innovations in low carbon glass bottles are centered on reducing their environmental impact throughout the lifecycle. Key advancements include the development of lighter-weight designs through optimized glass distribution and material science, which decreases energy consumption during manufacturing and transportation. The increased incorporation of recycled glass (cullet) – often exceeding XX% – is a critical factor, significantly lowering the melting temperature required and thus reducing energy usage and associated carbon emissions. Manufacturers are also exploring new glass formulations and advanced furnace technologies, such as electric melting powered by renewable energy sources, to further minimize the carbon footprint. These product innovations directly translate into competitive advantages by offering brands a demonstrably sustainable packaging solution that aligns with growing consumer and regulatory demands for eco-friendly products.

Key Drivers, Barriers & Challenges in Low Carbon Glass Bottle

The Low Carbon Glass Bottle Market is propelled by several key drivers. Technologically, advancements in energy-efficient manufacturing processes, including electric furnaces and increased cullet utilization, are critical. Economically, the growing consumer demand for sustainable products and increasing corporate ESG commitments are significant motivators. Policy-driven factors, such as government incentives for green manufacturing and stricter environmental regulations, are also playing a crucial role. For example, policies aimed at reducing landfill waste and promoting the circular economy directly favor glass recycling and reuse.

However, the market faces significant challenges and restraints. Supply chain issues, particularly concerning the consistent availability and quality of high-grade recycled glass (cullet), can hinder production. Regulatory hurdles, though often drivers, can also include complex permitting processes for new sustainable manufacturing facilities. Competitive pressures from alternative packaging materials like plastic and aluminum, which may offer lower upfront costs, remain a constant concern. The capital investment required for upgrading to low carbon manufacturing technologies also presents a barrier for smaller players. The energy intensity of traditional glass manufacturing is being addressed, but historical perceptions and the ongoing need for further innovation in this area continue to be a challenge. The cost of renewable energy procurement at scale can also be a factor impacting overall price competitiveness.

Growth Drivers in the Low Carbon Glass Bottle Market

The Low Carbon Glass Bottle Market is experiencing robust growth driven by several interconnected factors. Technologically, advancements in energy-efficient furnace designs, including electric and hybrid melting technologies powered by renewable energy, are significantly reducing emissions. The increasing capability to incorporate higher percentages of recycled glass (cullet), often exceeding XX%, in bottle production is a cornerstone of this growth, directly lowering the carbon footprint. Economically, the escalating consumer preference for sustainable packaging across all demographics is a powerful market force, compelling brands to adopt eco-friendly solutions. Corporate sustainability goals and stringent ESG reporting requirements are further solidifying the demand for low carbon glass bottles as companies strive to reduce their environmental impact. Regulatory frameworks worldwide, promoting circular economy principles, carbon neutrality targets, and extended producer responsibility (EPR) schemes, are creating a supportive environment for the widespread adoption of low carbon glass bottles.

Challenges Impacting Low Carbon Glass Bottle Growth

Despite the positive growth trajectory, the Low Carbon Glass Bottle Market encounters several key barriers and restraints. Regulatory complexities, while often driving adoption, can also manifest as difficulties in obtaining permits for new, advanced manufacturing facilities and navigating evolving waste management policies. Supply chain issues are paramount, with challenges including securing a consistent and high-quality supply of cullet for recycling, which can impact production volumes and product consistency. Furthermore, competition from alternative packaging materials, such as lightweight plastics and aluminum, remains a significant pressure, often competing on price and perceived convenience. The substantial capital investment required for upgrading existing manufacturing plants to incorporate low carbon technologies presents a financial hurdle for many companies. The energy intensity of glass manufacturing, even with improvements, remains a factor requiring continuous innovation and investment in renewable energy sources. The cost of sustainable energy procurement at scale can also impact the overall price competitiveness of low carbon glass bottles.

Key Players Shaping the Low Carbon Glass Bottle Market

- Encirc

- Bacardi

- Molson Coors

- Verallia

- Ardagh Glass Packaging

- Wiegand-Glas

- Vidrala

- OI Glass

Significant Low Carbon Glass Bottle Industry Milestones

- 2019: Increased global focus on plastic pollution drives heightened interest in glass as a sustainable alternative.

- 2020: Several major beverage companies announce ambitious carbon reduction targets, explicitly including packaging.

- 2021: Breakthroughs in electric furnace technology for glass melting gain commercial traction.

- 2022: European Union strengthens regulations on packaging waste and promotes circular economy models.

- 2023: Significant investments announced in advanced recycling infrastructure for glass.

- 2024: Development and commercialization of ultra-lightweight glass bottle designs with reduced carbon footprints.

Future Outlook for Low Carbon Glass Bottle Market

The future outlook for the Low Carbon Glass Bottle Market is exceptionally bright, characterized by sustained growth and increasing innovation. Strategic opportunities lie in further optimizing production processes through AI and renewable energy integration, leading to even lower carbon emissions. The expansion of closed-loop recycling systems and bottle-to-bottle recycling initiatives will enhance the circularity of glass packaging. As consumer demand for sustainable products intensifies and regulatory pressures continue to mount, the market penetration of low carbon glass bottles is set to accelerate. The Food & Beverage Industry, in particular, will continue to be a major growth catalyst, with brands increasingly leveraging low carbon glass packaging as a key differentiator. Emerging markets are also expected to contribute significantly to overall growth, driven by increasing environmental awareness and industrial development. The market is poised to reach hundreds of billions by 2033.

Low Carbon Glass Bottle Segmentation

-

1. Application

- 1.1. Food & Beverage Industry

- 1.2. Medical

- 1.3. Others

-

2. Types

- 2.1. Drink Bottle

- 2.2. Wine Bottle

- 2.3. Others

Low Carbon Glass Bottle Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Low Carbon Glass Bottle Regional Market Share

Geographic Coverage of Low Carbon Glass Bottle

Low Carbon Glass Bottle REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food & Beverage Industry

- 5.1.2. Medical

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Drink Bottle

- 5.2.2. Wine Bottle

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Low Carbon Glass Bottle Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food & Beverage Industry

- 6.1.2. Medical

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Drink Bottle

- 6.2.2. Wine Bottle

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Low Carbon Glass Bottle Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food & Beverage Industry

- 7.1.2. Medical

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Drink Bottle

- 7.2.2. Wine Bottle

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Low Carbon Glass Bottle Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food & Beverage Industry

- 8.1.2. Medical

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Drink Bottle

- 8.2.2. Wine Bottle

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Low Carbon Glass Bottle Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food & Beverage Industry

- 9.1.2. Medical

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Drink Bottle

- 9.2.2. Wine Bottle

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Low Carbon Glass Bottle Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food & Beverage Industry

- 10.1.2. Medical

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Drink Bottle

- 10.2.2. Wine Bottle

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Low Carbon Glass Bottle Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Food & Beverage Industry

- 11.1.2. Medical

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Drink Bottle

- 11.2.2. Wine Bottle

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Encirc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Bacardi

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Molson Coors

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Verallia

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ardagh Glass Packaging

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Wiegand-Glas

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Vidrala

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 OI Glass

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.1 Encirc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Low Carbon Glass Bottle Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Low Carbon Glass Bottle Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Low Carbon Glass Bottle Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Low Carbon Glass Bottle Volume (K), by Application 2025 & 2033

- Figure 5: North America Low Carbon Glass Bottle Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Low Carbon Glass Bottle Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Low Carbon Glass Bottle Revenue (billion), by Types 2025 & 2033

- Figure 8: North America Low Carbon Glass Bottle Volume (K), by Types 2025 & 2033

- Figure 9: North America Low Carbon Glass Bottle Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Low Carbon Glass Bottle Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Low Carbon Glass Bottle Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Low Carbon Glass Bottle Volume (K), by Country 2025 & 2033

- Figure 13: North America Low Carbon Glass Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Low Carbon Glass Bottle Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Low Carbon Glass Bottle Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Low Carbon Glass Bottle Volume (K), by Application 2025 & 2033

- Figure 17: South America Low Carbon Glass Bottle Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Low Carbon Glass Bottle Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Low Carbon Glass Bottle Revenue (billion), by Types 2025 & 2033

- Figure 20: South America Low Carbon Glass Bottle Volume (K), by Types 2025 & 2033

- Figure 21: South America Low Carbon Glass Bottle Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Low Carbon Glass Bottle Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Low Carbon Glass Bottle Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Low Carbon Glass Bottle Volume (K), by Country 2025 & 2033

- Figure 25: South America Low Carbon Glass Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Low Carbon Glass Bottle Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Low Carbon Glass Bottle Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Low Carbon Glass Bottle Volume (K), by Application 2025 & 2033

- Figure 29: Europe Low Carbon Glass Bottle Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Low Carbon Glass Bottle Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Low Carbon Glass Bottle Revenue (billion), by Types 2025 & 2033

- Figure 32: Europe Low Carbon Glass Bottle Volume (K), by Types 2025 & 2033

- Figure 33: Europe Low Carbon Glass Bottle Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Low Carbon Glass Bottle Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Low Carbon Glass Bottle Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Low Carbon Glass Bottle Volume (K), by Country 2025 & 2033

- Figure 37: Europe Low Carbon Glass Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Low Carbon Glass Bottle Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Low Carbon Glass Bottle Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Low Carbon Glass Bottle Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Low Carbon Glass Bottle Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Low Carbon Glass Bottle Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Low Carbon Glass Bottle Revenue (billion), by Types 2025 & 2033

- Figure 44: Middle East & Africa Low Carbon Glass Bottle Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Low Carbon Glass Bottle Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Low Carbon Glass Bottle Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Low Carbon Glass Bottle Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Low Carbon Glass Bottle Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Low Carbon Glass Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Low Carbon Glass Bottle Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Low Carbon Glass Bottle Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Low Carbon Glass Bottle Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Low Carbon Glass Bottle Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Low Carbon Glass Bottle Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Low Carbon Glass Bottle Revenue (billion), by Types 2025 & 2033

- Figure 56: Asia Pacific Low Carbon Glass Bottle Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Low Carbon Glass Bottle Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Low Carbon Glass Bottle Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Low Carbon Glass Bottle Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Low Carbon Glass Bottle Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Low Carbon Glass Bottle Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Low Carbon Glass Bottle Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Low Carbon Glass Bottle Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Low Carbon Glass Bottle Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Low Carbon Glass Bottle Revenue billion Forecast, by Types 2020 & 2033

- Table 4: Global Low Carbon Glass Bottle Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Low Carbon Glass Bottle Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Low Carbon Glass Bottle Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Low Carbon Glass Bottle Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Low Carbon Glass Bottle Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Low Carbon Glass Bottle Revenue billion Forecast, by Types 2020 & 2033

- Table 10: Global Low Carbon Glass Bottle Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Low Carbon Glass Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Low Carbon Glass Bottle Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Low Carbon Glass Bottle Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Low Carbon Glass Bottle Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Low Carbon Glass Bottle Revenue billion Forecast, by Types 2020 & 2033

- Table 22: Global Low Carbon Glass Bottle Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Low Carbon Glass Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Low Carbon Glass Bottle Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Low Carbon Glass Bottle Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Low Carbon Glass Bottle Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Low Carbon Glass Bottle Revenue billion Forecast, by Types 2020 & 2033

- Table 34: Global Low Carbon Glass Bottle Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Low Carbon Glass Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Low Carbon Glass Bottle Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Low Carbon Glass Bottle Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Low Carbon Glass Bottle Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Low Carbon Glass Bottle Revenue billion Forecast, by Types 2020 & 2033

- Table 58: Global Low Carbon Glass Bottle Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Low Carbon Glass Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Low Carbon Glass Bottle Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Low Carbon Glass Bottle Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Low Carbon Glass Bottle Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Low Carbon Glass Bottle Revenue billion Forecast, by Types 2020 & 2033

- Table 76: Global Low Carbon Glass Bottle Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Low Carbon Glass Bottle Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Low Carbon Glass Bottle Volume K Forecast, by Country 2020 & 2033

- Table 79: China Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Low Carbon Glass Bottle Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Low Carbon Glass Bottle Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Low Carbon Glass Bottle?

The projected CAGR is approximately 6%.

2. Which companies are prominent players in the Low Carbon Glass Bottle?

Key companies in the market include Encirc, Bacardi, Molson Coors, Verallia, Ardagh Glass Packaging, Wiegand-Glas, Vidrala, OI Glass.

3. What are the main segments of the Low Carbon Glass Bottle?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.21 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Low Carbon Glass Bottle," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Low Carbon Glass Bottle report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Low Carbon Glass Bottle?

To stay informed about further developments, trends, and reports in the Low Carbon Glass Bottle, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence