Key Insights

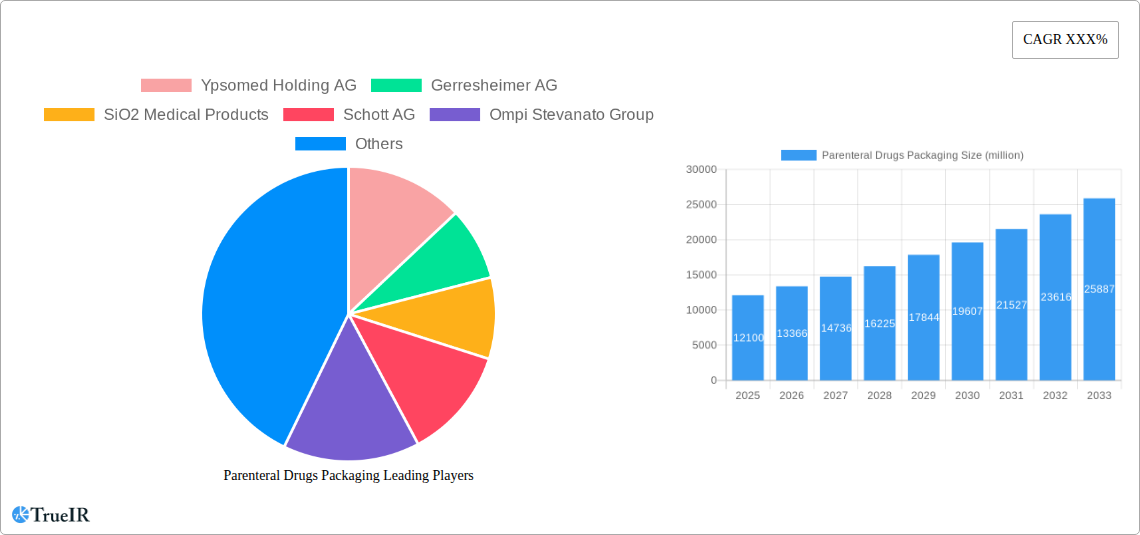

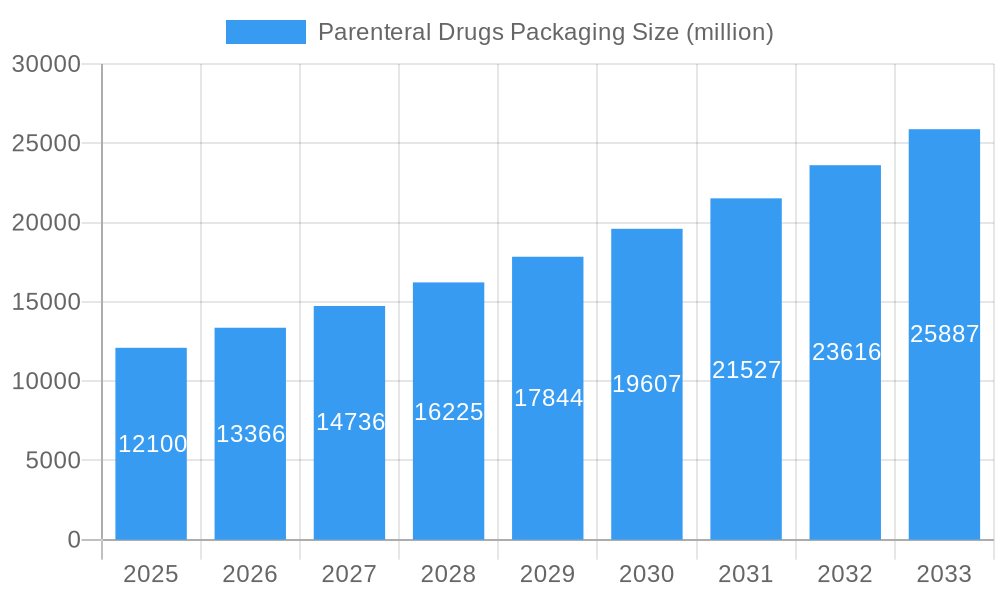

The global market for Parenteral Drugs Packaging is poised for significant expansion, projected to reach $12.1 billion in 2025. This growth is fueled by a robust Compound Annual Growth Rate (CAGR) of 10.51% anticipated between 2019 and 2033. The increasing prevalence of chronic diseases, a burgeoning elderly population, and the continuous development of novel biologic drugs are primary drivers of this upward trajectory. Furthermore, the demand for advanced drug delivery systems, such as pre-filled syringes and advanced vial technologies, is escalating, pushing the market towards innovative packaging solutions that ensure drug stability, safety, and efficacy. The shift towards biologics and specialty injectables, which often require specialized containment and administration, further bolsters the need for high-quality parenteral packaging. Technological advancements in materials science and manufacturing processes are also contributing to the development of more sophisticated and cost-effective packaging options.

Parenteral Drugs Packaging Market Size (In Billion)

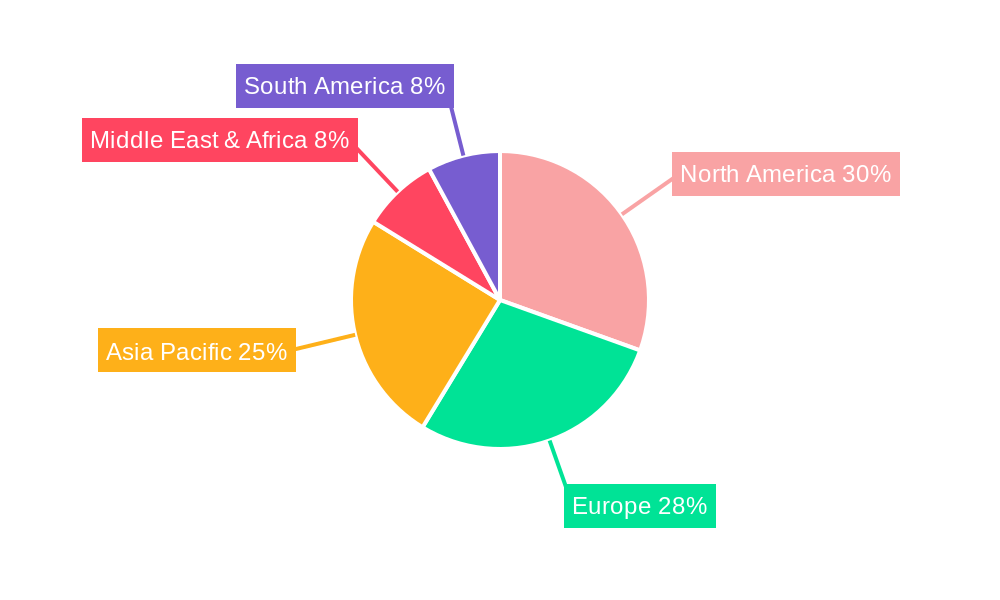

The market is segmented into Polyvinyl Chloride (PVC) and Polyolefin types, with Polyolefin gaining traction due to its enhanced chemical inertness and lower leachables compared to PVC, particularly crucial for sensitive biologic formulations. Applications are broadly categorized into Large Volume Parenteral (LVP) and Small Volume Parenteral (SVP) solutions. The increasing adoption of SVP for targeted therapies and personalized medicine is a notable trend. While market growth is strong, challenges such as stringent regulatory requirements for pharmaceutical packaging and the need for advanced sterilization techniques can act as moderating factors. However, the overarching demand for safe, reliable, and convenient parenteral drug administration is expected to outweigh these restraints, driving sustained market expansion across key regions like North America, Europe, and the rapidly growing Asia Pacific.

Parenteral Drugs Packaging Company Market Share

Here's a dynamic, SEO-optimized report description for Parenteral Drugs Packaging, designed for immediate use without modification.

Parenteral Drugs Packaging Market Structure & Competitive Landscape

The global parenteral drugs packaging market, valued at over $10 billion in 2025, exhibits a moderately concentrated structure. Leading players like Ypsomed Holding AG, Gerresheimer AG, Schott AG, and West Pharmaceutical Services hold significant market share, driven by their robust product portfolios and extensive distribution networks. Innovation remains a key differentiator, with continuous advancements in material science and drug delivery systems influencing market dynamics. Regulatory impacts, particularly stringent quality control and safety standards from agencies like the FDA and EMA, shape product development and market entry strategies. The threat of product substitutes, such as oral drug delivery systems for certain therapeutic areas, is managed through the development of specialized parenteral packaging solutions that enhance drug stability and patient compliance. End-user segmentation, primarily by application (Large Volume Parenteral (LVP) and Small Volume Parenteral (SVP)) and type (Polyvinyl Chloride (PVC), Polyolefin), reveals distinct growth trajectories. Mergers and acquisitions (M&A) activity, with an estimated 20+ major M&A transactions annually contributing over $1 billion to market consolidation, are a prominent trend, allowing companies to expand their geographic reach, acquire new technologies, and strengthen their competitive positions. The market is characterized by a blend of established global giants and agile niche players, all vying for market dominance through strategic partnerships, technological innovation, and a keen understanding of evolving pharmaceutical needs.

Parenteral Drugs Packaging Market Trends & Opportunities

The parenteral drugs packaging market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from 2025 to 2033, with the market size expected to surpass $20 billion by the end of the forecast period. This expansion is fueled by a confluence of evolving pharmaceutical landscapes, an aging global population, and a growing prevalence of chronic diseases demanding advanced therapeutic interventions. Technological shifts are profoundly influencing packaging solutions, with an increasing demand for pre-filled syringes, vials with advanced stoppers, and innovative drug delivery devices that enhance patient convenience and therapeutic efficacy. The transition towards more sustainable and environmentally friendly packaging materials, such as advanced polyolefins and novel biodegradable polymers, is gaining traction, driven by both regulatory mandates and growing consumer preference for eco-conscious products. The increasing focus on personalized medicine and biologics necessitates specialized packaging that can maintain drug integrity, prevent contamination, and ensure accurate dosage delivery, creating significant opportunities for specialized packaging manufacturers. Furthermore, the growing adoption of advanced sterilization techniques and barrier properties in packaging materials is crucial for protecting sensitive parenteral drugs from degradation and microbial contamination. The competitive dynamics are intensifying, with companies investing heavily in research and development to secure patents and introduce next-generation packaging solutions. Market penetration rates are highest in developed economies but are rapidly increasing in emerging markets due to improving healthcare infrastructure and rising disposable incomes, opening new avenues for market expansion. The demand for sterile, safe, and efficient parenteral drug packaging is a constant, and manufacturers who can innovate and adapt to these evolving trends will be best positioned for sustained success in this multi-billion dollar industry.

Dominant Markets & Segments in Parenteral Drugs Packaging

The global parenteral drugs packaging market is segmented by Application into Large Volume Parenteral (LVP) and Small Volume Parenteral (SVP), and by Type into Polyvinyl Chloride (PVC) and Polyolefin. The Small Volume Parenteral (SVP) segment is currently dominant, accounting for over 60% of the market value, driven by the burgeoning biopharmaceutical sector and the increasing demand for injectable drugs for chronic disease management, oncology, and immunology.

- Key Growth Drivers for SVP:

- Rise of Biologics and Biosimilars: These complex therapeutic agents often require specialized, high-barrier packaging to maintain their stability and efficacy, with SVP solutions being ideal.

- Increasing Demand for Pre-filled Syringes and Auto-injectors: These convenient dosage forms, predominantly used for SVP, are favored for patient self-administration and improved compliance in chronic condition management.

- Growth in Specialty Pharmaceuticals: The development of highly targeted therapies for niche indications, often administered via injection, further bolsters the SVP segment.

- Technological Advancements in Syringe and Vial Manufacturing: Innovations in materials, coatings, and design are enhancing the safety and functionality of SVP packaging.

Within the Type segmentation, Polyolefin packaging is emerging as a dominant and high-growth segment, projected to capture a significant share of the market. While PVC has historically been a staple, concerns regarding plasticizers and environmental impact are driving a shift towards polyolefins, including polypropylene and polyethylene.

- Key Growth Drivers for Polyolefin:

- Enhanced Chemical Resistance and Inertness: Polyolefins offer superior compatibility with a wide range of drug formulations, minimizing leachable and extractable concerns.

- Improved Flexibility and Shatter Resistance: Compared to glass, polyolefin-based containers are lighter and less prone to breakage, reducing risks during handling and transport.

- Sustainability Initiatives: Polyolefins are often recyclable and can be manufactured with lower carbon footprints, aligning with global sustainability goals.

- Regulatory Favorability: Increasing scrutiny on PVC components is leading manufacturers to opt for polyolefin alternatives that meet stringent regulatory requirements.

North America and Europe currently lead the parenteral drugs packaging market due to established pharmaceutical industries and high healthcare spending. However, the Asia-Pacific region is experiencing the fastest growth, driven by expanding healthcare infrastructure, increasing pharmaceutical manufacturing capabilities, and rising domestic demand for advanced therapeutics. Government policies promoting domestic drug production and investments in R&D infrastructure are significant growth catalysts in these emerging markets.

Parenteral Drugs Packaging Product Analysis

Product innovation in parenteral drugs packaging is centered on enhancing drug stability, patient safety, and ease of use. Key advancements include the development of advanced barrier materials for vials and pre-filled syringes, crucial for protecting sensitive biologics and vaccines from oxygen, moisture, and light. Innovations in stoppers and seals are addressing concerns about extractables and leachables, ensuring drug purity. The rise of integrated drug delivery systems, such as smart auto-injectors and wearable devices, represents a significant product evolution, offering improved patient compliance and precise dosing. Companies are focusing on materials like advanced polyolefins and glass alternatives that offer superior inertness and shatter resistance, while also meeting sustainability demands.

Key Drivers, Barriers & Challenges in Parenteral Drugs Packaging

Key Drivers: The parenteral drugs packaging market is propelled by several critical factors. The escalating demand for biologics and biosimilars, which necessitate specialized and high-performance packaging, is a primary driver. Advances in drug delivery technologies, such as pre-filled syringes and auto-injectors, are enhancing patient convenience and adherence, thereby boosting market growth. The increasing prevalence of chronic diseases and an aging global population contribute to a sustained need for injectable medications. Furthermore, stringent regulatory requirements for drug safety and efficacy are driving innovation in high-quality, sterile packaging solutions.

Barriers & Challenges: Despite robust growth, the market faces significant challenges. The complex and evolving regulatory landscape, requiring extensive validation and adherence to global standards, presents a considerable hurdle. Supply chain disruptions, including raw material shortages and logistics complexities, can impact production timelines and costs. Intense competition among established players and emerging manufacturers leads to price pressures. Additionally, the high cost of specialized packaging materials and manufacturing technologies can be a barrier to entry and adoption, particularly for smaller pharmaceutical companies.

Growth Drivers in the Parenteral Drugs Packaging Market

The parenteral drugs packaging market's growth is primarily propelled by the exponential rise in the development and production of biologics and biosimilars, demanding sophisticated packaging to preserve their complex molecular structures and ensure efficacy. The increasing patient preference for self-administration, fueled by the convenience offered by pre-filled syringes and advanced auto-injectors, further accelerates demand. Public health initiatives aimed at combating infectious diseases and managing chronic conditions globally necessitate a continuous supply of injectable pharmaceuticals, directly translating to increased packaging requirements. Moreover, technological advancements in drug formulation and delivery systems are creating new markets for specialized packaging solutions designed to maintain drug stability and sterility throughout their lifecycle.

Challenges Impacting Parenteral Drugs Packaging Growth

The parenteral drugs packaging industry grapples with several formidable challenges that can impede growth. Navigating the intricate and ever-changing global regulatory frameworks, which mandate rigorous safety, quality, and traceability standards, necessitates substantial investment in compliance and validation. Supply chain vulnerabilities, including the availability of critical raw materials and the logistical complexities of transporting sterile products, pose significant risks to consistent production and timely delivery. The highly competitive market environment exerts considerable pricing pressure, demanding cost-effective solutions without compromising quality. Furthermore, the substantial capital investment required for state-of-the-art manufacturing facilities and advanced packaging technologies can be a substantial barrier for new entrants and smaller players.

Key Players Shaping the Parenteral Drugs Packaging Market

- Ypsomed Holding AG

- Gerresheimer AG

- SiO2 Medical Products

- Schott AG

- Ompi Stevanato Group

- Becton Dickinson and Company

- MeadWestvaco Corporation

- Unilife Corporation Inc

- West Pharmaceutical Services

- Terumo Corporation

- Berry Plastics Corporation

- Owens-Illinois

- RPC Group

- Graphic Packaging Group

Significant Parenteral Drugs Packaging Industry Milestones

- 2019: Introduction of advanced aseptic filling technologies for biologics, significantly enhancing product sterility and shelf-life.

- 2020: Increased demand for pre-filled syringes due to the COVID-19 pandemic, driving substantial production increases and supply chain adaptations.

- 2021: Growing adoption of sustainability initiatives, with a significant focus on recyclable and biodegradable materials in parenteral packaging.

- 2022: Major acquisitions in the syringe and vial manufacturing sectors, consolidating market share among key players.

- 2023: Emergence of novel drug delivery devices, such as connected auto-injectors, for enhanced patient monitoring and therapy management.

- 2024: Advancements in inert coating technologies for glass vials, improving compatibility with highly sensitive drug formulations.

Future Outlook for Parenteral Drugs Packaging Market

The future outlook for the parenteral drugs packaging market is exceptionally promising, driven by continuous innovation in drug development and delivery systems. The burgeoning field of personalized medicine will necessitate highly customized and secure packaging solutions. The persistent demand for biologics, vaccines, and gene therapies will ensure a sustained need for advanced sterile packaging that guarantees drug integrity and patient safety. Key growth catalysts include the further integration of smart technologies for drug tracking and patient compliance, alongside a robust move towards sustainable and circular economy principles in packaging material sourcing and disposal. Companies that can adeptly navigate regulatory complexities and invest in advanced manufacturing technologies will be well-positioned to capitalize on this expanding multi-billion dollar market.

Parenteral Drugs Packaging Segmentation

-

1. Application

- 1.1. Large Volume Parenteral (LVP)

- 1.2. Small Volume Parenteral (SVP)

-

2. Type

- 2.1. Polyvinyl Chloride (PVC)

- 2.2. Polyolefin

Parenteral Drugs Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Parenteral Drugs Packaging Regional Market Share

Geographic Coverage of Parenteral Drugs Packaging

Parenteral Drugs Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.63% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Large Volume Parenteral (LVP)

- 5.1.2. Small Volume Parenteral (SVP)

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Polyvinyl Chloride (PVC)

- 5.2.2. Polyolefin

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Parenteral Drugs Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Large Volume Parenteral (LVP)

- 6.1.2. Small Volume Parenteral (SVP)

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Polyvinyl Chloride (PVC)

- 6.2.2. Polyolefin

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Parenteral Drugs Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Large Volume Parenteral (LVP)

- 7.1.2. Small Volume Parenteral (SVP)

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Polyvinyl Chloride (PVC)

- 7.2.2. Polyolefin

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Parenteral Drugs Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Large Volume Parenteral (LVP)

- 8.1.2. Small Volume Parenteral (SVP)

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Polyvinyl Chloride (PVC)

- 8.2.2. Polyolefin

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Parenteral Drugs Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Large Volume Parenteral (LVP)

- 9.1.2. Small Volume Parenteral (SVP)

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Polyvinyl Chloride (PVC)

- 9.2.2. Polyolefin

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Parenteral Drugs Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Large Volume Parenteral (LVP)

- 10.1.2. Small Volume Parenteral (SVP)

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Polyvinyl Chloride (PVC)

- 10.2.2. Polyolefin

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Parenteral Drugs Packaging Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Large Volume Parenteral (LVP)

- 11.1.2. Small Volume Parenteral (SVP)

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Polyvinyl Chloride (PVC)

- 11.2.2. Polyolefin

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Ypsomed Holding AG

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Gerresheimer AG

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 SiO2 Medical Products

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Schott AG

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Ompi Stevanato Group

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Becton Dickinson and Company

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 MeadWestvaco Corporation

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Unilife Corporation Inc

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 West Pharmaceutical Services

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Terumo Corporation

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Berry Plastics Corporation

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Owens-Illinois

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 RPC Group

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Graphic Packaging Group

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 Ypsomed Holding AG

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Parenteral Drugs Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Global Parenteral Drugs Packaging Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 4: North America Parenteral Drugs Packaging Volume (K), by Application 2025 & 2033

- Figure 5: North America Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Parenteral Drugs Packaging Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 8: North America Parenteral Drugs Packaging Volume (K), by Type 2025 & 2033

- Figure 9: North America Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Parenteral Drugs Packaging Volume Share (%), by Type 2025 & 2033

- Figure 11: North America Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 12: North America Parenteral Drugs Packaging Volume (K), by Country 2025 & 2033

- Figure 13: North America Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Parenteral Drugs Packaging Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 16: South America Parenteral Drugs Packaging Volume (K), by Application 2025 & 2033

- Figure 17: South America Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Parenteral Drugs Packaging Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 20: South America Parenteral Drugs Packaging Volume (K), by Type 2025 & 2033

- Figure 21: South America Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 22: South America Parenteral Drugs Packaging Volume Share (%), by Type 2025 & 2033

- Figure 23: South America Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 24: South America Parenteral Drugs Packaging Volume (K), by Country 2025 & 2033

- Figure 25: South America Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Parenteral Drugs Packaging Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 28: Europe Parenteral Drugs Packaging Volume (K), by Application 2025 & 2033

- Figure 29: Europe Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Parenteral Drugs Packaging Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 32: Europe Parenteral Drugs Packaging Volume (K), by Type 2025 & 2033

- Figure 33: Europe Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 34: Europe Parenteral Drugs Packaging Volume Share (%), by Type 2025 & 2033

- Figure 35: Europe Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 36: Europe Parenteral Drugs Packaging Volume (K), by Country 2025 & 2033

- Figure 37: Europe Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Parenteral Drugs Packaging Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 40: Middle East & Africa Parenteral Drugs Packaging Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Parenteral Drugs Packaging Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 44: Middle East & Africa Parenteral Drugs Packaging Volume (K), by Type 2025 & 2033

- Figure 45: Middle East & Africa Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 46: Middle East & Africa Parenteral Drugs Packaging Volume Share (%), by Type 2025 & 2033

- Figure 47: Middle East & Africa Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 48: Middle East & Africa Parenteral Drugs Packaging Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Parenteral Drugs Packaging Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Parenteral Drugs Packaging Revenue (billion), by Application 2025 & 2033

- Figure 52: Asia Pacific Parenteral Drugs Packaging Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Parenteral Drugs Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Parenteral Drugs Packaging Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Parenteral Drugs Packaging Revenue (billion), by Type 2025 & 2033

- Figure 56: Asia Pacific Parenteral Drugs Packaging Volume (K), by Type 2025 & 2033

- Figure 57: Asia Pacific Parenteral Drugs Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 58: Asia Pacific Parenteral Drugs Packaging Volume Share (%), by Type 2025 & 2033

- Figure 59: Asia Pacific Parenteral Drugs Packaging Revenue (billion), by Country 2025 & 2033

- Figure 60: Asia Pacific Parenteral Drugs Packaging Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Parenteral Drugs Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Parenteral Drugs Packaging Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Parenteral Drugs Packaging Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global Parenteral Drugs Packaging Volume K Forecast, by Type 2020 & 2033

- Table 5: Global Parenteral Drugs Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Global Parenteral Drugs Packaging Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 8: Global Parenteral Drugs Packaging Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global Parenteral Drugs Packaging Volume K Forecast, by Type 2020 & 2033

- Table 11: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Global Parenteral Drugs Packaging Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: United States Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Canada Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: Mexico Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 20: Global Parenteral Drugs Packaging Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 22: Global Parenteral Drugs Packaging Volume K Forecast, by Type 2020 & 2033

- Table 23: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Global Parenteral Drugs Packaging Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Brazil Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Argentina Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 32: Global Parenteral Drugs Packaging Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 34: Global Parenteral Drugs Packaging Volume K Forecast, by Type 2020 & 2033

- Table 35: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 36: Global Parenteral Drugs Packaging Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 40: Germany Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: France Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: Italy Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Spain Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 48: Russia Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 50: Benelux Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 52: Nordics Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 56: Global Parenteral Drugs Packaging Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 58: Global Parenteral Drugs Packaging Volume K Forecast, by Type 2020 & 2033

- Table 59: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 60: Global Parenteral Drugs Packaging Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 62: Turkey Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 64: Israel Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 66: GCC Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 68: North Africa Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 70: South Africa Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Parenteral Drugs Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 74: Global Parenteral Drugs Packaging Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Parenteral Drugs Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 76: Global Parenteral Drugs Packaging Volume K Forecast, by Type 2020 & 2033

- Table 77: Global Parenteral Drugs Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 78: Global Parenteral Drugs Packaging Volume K Forecast, by Country 2020 & 2033

- Table 79: China Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 80: China Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 82: India Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 84: Japan Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 86: South Korea Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 90: Oceania Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Parenteral Drugs Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Parenteral Drugs Packaging Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Parenteral Drugs Packaging?

The projected CAGR is approximately 4.63%.

2. Which companies are prominent players in the Parenteral Drugs Packaging?

Key companies in the market include Ypsomed Holding AG, Gerresheimer AG, SiO2 Medical Products, Schott AG, Ompi Stevanato Group, Becton Dickinson and Company, MeadWestvaco Corporation, Unilife Corporation Inc, West Pharmaceutical Services, Terumo Corporation, Berry Plastics Corporation, Owens-Illinois, RPC Group, Graphic Packaging Group.

3. What are the main segments of the Parenteral Drugs Packaging?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.39 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Parenteral Drugs Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Parenteral Drugs Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Parenteral Drugs Packaging?

To stay informed about further developments, trends, and reports in the Parenteral Drugs Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence