Key Insights

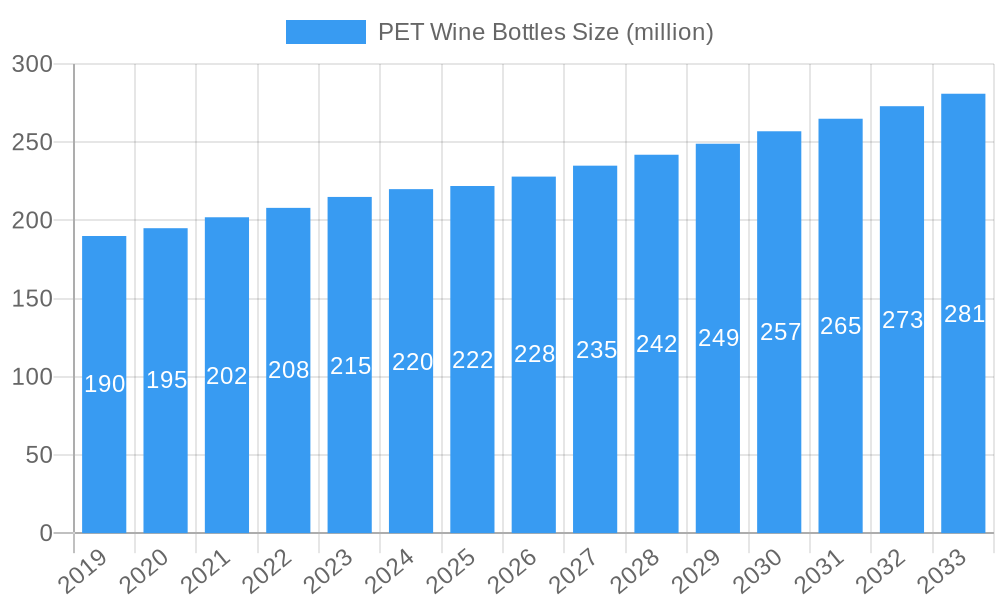

The global PET wine bottle market is poised for substantial growth, projected to reach $222 million by 2025, with a Compound Annual Growth Rate (CAGR) of 3.5% anticipated between 2019 and 2033. This steady expansion is primarily fueled by the increasing consumer preference for lightweight, shatter-resistant, and more sustainable packaging alternatives to traditional glass. The "Others" application segment, likely encompassing RTD (Ready-to-Drink) beverages and spirits packaged in PET, is expected to be a significant contributor to market value. Furthermore, the growing adoption of PET bottles for beer, driven by convenience and safety considerations, also plays a crucial role. This shift is further propelled by advancements in PET barrier technologies, enhancing product shelf-life and preserving the quality of beverages. Key market players are actively investing in innovative designs and sustainable solutions to cater to evolving consumer demands and regulatory landscapes.

PET Wine Bottles Market Size (In Million)

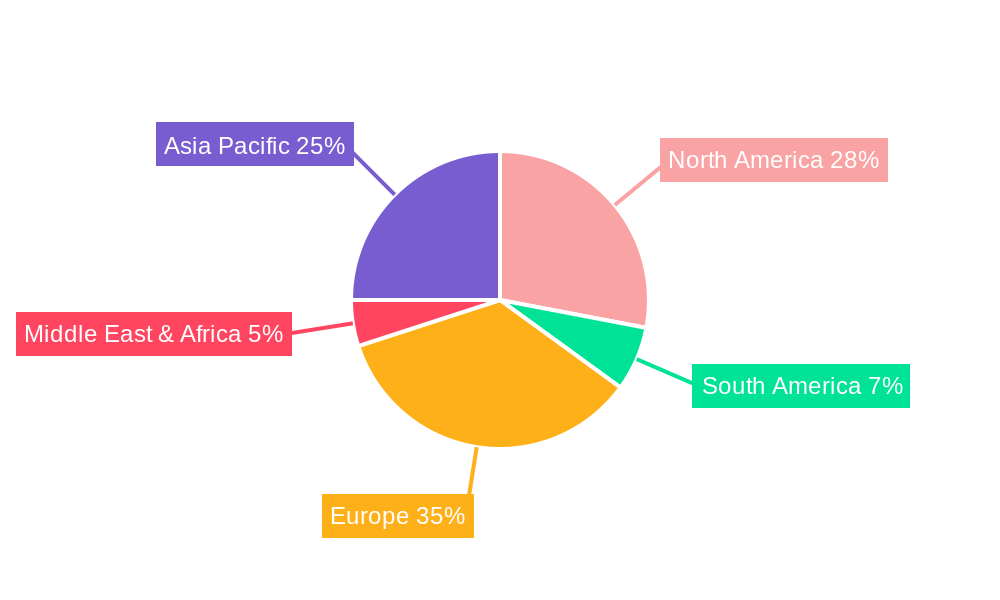

The market's trajectory is also shaped by emerging trends such as the rise of single-serve wine portions and the increasing e-commerce sales of alcoholic beverages, where the durability and lighter weight of PET bottles offer distinct logistical advantages. While the market is robust, certain restraints may include consumer perception regarding the premium feel of glass versus PET, particularly for high-end wines, and the ongoing development of more advanced and eco-friendly materials like recycled PET (rPET) and bio-based plastics, which could influence investment and consumer choices. The broader adoption of these advanced materials is a significant trend that will likely drive innovation and competition within the PET wine bottle industry. Geographically, regions like Asia Pacific, with its rapidly expanding middle class and increasing consumption of wine and beer, are expected to present significant growth opportunities, complementing the established markets in North America and Europe.

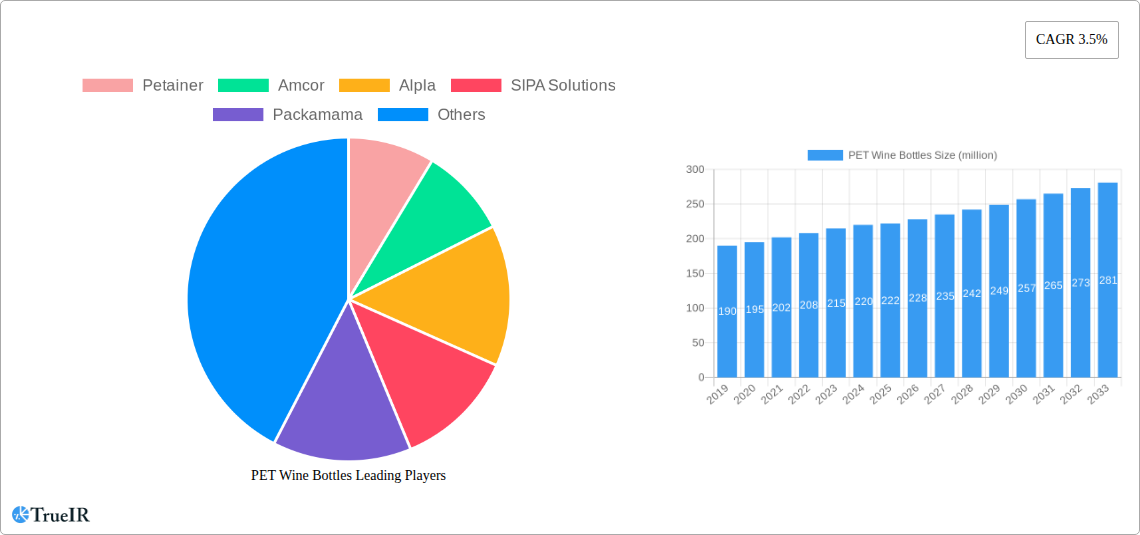

PET Wine Bottles Company Market Share

PET Wine Bottles Market Structure & Competitive Landscape

The global PET wine bottle market is characterized by a moderate to high concentration, with a few key players dominating a significant market share exceeding fifty million dollars. Innovation remains a crucial differentiator, driven by advancements in barrier technologies, lightweighting, and sustainable materials, aiming to overcome traditional perceptions of PET as a secondary choice for wine packaging. Regulatory impacts are increasingly influencing market dynamics, with a growing emphasis on recyclability mandates and Extended Producer Responsibility (EPR) schemes across various regions, particularly in North America and Europe, pushing for a circular economy. Product substitutes, primarily glass bottles, continue to pose a challenge, especially for premium wine segments, although PET bottles are gaining traction for their shatterproof nature, reduced weight for logistics, and cost-effectiveness in specific applications like single-serve formats and outdoor events. End-user segmentation reveals a bifurcated market: the convenience-driven consumer segment actively seeks the benefits of PET for everyday consumption and portability, while the connoisseur segment remains largely loyal to glass for perceived quality and aging potential. Merger and acquisition (M&A) activity has been observed, with an estimated volume of over fifty transactions in the historical period (2019-2024), aimed at consolidating market presence, acquiring innovative technologies, and expanding geographic reach. Key companies actively participating in M&A include Amcor and Berry Global, signaling a strategic intent to bolster their portfolios and competitive standing in this evolving packaging sector. The market is projected to see continued consolidation as companies seek economies of scale and enhanced innovation capabilities to navigate the complex landscape.

PET Wine Bottles Market Trends & Opportunities

The PET wine bottle market is experiencing a transformative phase, driven by a convergence of sustainability mandates, evolving consumer preferences, and technological innovation. The market size, estimated to be in the billions of dollars, is projected to witness robust growth at a Compound Annual Growth Rate (CAGR) of approximately five percent during the forecast period of 2025–2033. This expansion is fueled by an increasing adoption of PET bottles in segments that traditionally favored glass, such as ready-to-drink (RTD) beverages and specific wine varietals. The market penetration rate of PET wine bottles is steadily increasing, particularly in regions with favorable regulatory environments and a strong focus on lightweight packaging solutions.

Technological advancements are playing a pivotal role in enhancing the appeal of PET wine bottles. Innovations in barrier technology, such as multi-layer PET structures and advanced coatings, are effectively addressing concerns related to oxygen and CO2 permeability, thereby improving shelf life and preserving wine quality. This has opened up new avenues for PET in the packaging of wines that require longer storage and transport times. Furthermore, the development of advanced recycling technologies and the increasing availability of recycled PET (rPET) are significantly boosting the sustainability credentials of PET wine bottles, aligning with global environmental goals and consumer demand for eco-friendly packaging.

Consumer preferences are also undergoing a significant shift. There is a growing demand for convenient, portable, and shatterproof packaging options, especially for casual consumption, outdoor activities, and single-serve portions. PET wine bottles perfectly meet these demands, offering a safer and lighter alternative to glass. The increasing popularity of wine in various formats, including smaller sizes and multipacks, further strengthens the case for PET.

The competitive landscape is dynamic, with established packaging giants and innovative niche players vying for market share. Companies are investing heavily in research and development to introduce superior barrier properties, aesthetic appeal, and sustainable solutions. This competitive intensity is driving down costs and fostering innovation, making PET wine bottles a more attractive proposition for a wider range of wine producers. The focus on circular economy principles is also creating opportunities for companies that can offer closed-loop solutions and demonstrate commitment to rPET integration. The shift towards lighter-weight packaging also presents significant logistical advantages, reducing transportation costs and carbon footprint, a factor increasingly considered by both producers and consumers. The market is poised for substantial growth as these trends continue to shape the industry, offering a promising future for PET wine bottle manufacturers and adopters.

Dominant Markets & Segments in PET Wine Bottles

The global PET wine bottle market exhibits distinct regional dominance and segment penetration, driven by a confluence of economic, regulatory, and consumer-driven factors. Asia Pacific, with an estimated market size exceeding one billion dollars, is emerging as a dominant region, propelled by rapid economic growth, an expanding middle class with increasing disposable incomes, and a burgeoning wine consumption culture. Government initiatives promoting sustainable packaging and the presence of major manufacturing hubs further bolster this dominance. Within Asia Pacific, China represents a significant market, driven by its vast population and the increasing adoption of wine as a beverage of choice.

From an application perspective, Red Wine and White Wine segments collectively account for the largest share of the PET wine bottle market, estimated at over sixty percent of the total market value. This is attributed to the broad appeal and widespread consumption of these wine types across diverse demographics and occasions. The growing trend of single-serve wine portions and convenience packaging further fuels demand for PET bottles in these categories. The Beer segment, while a significant player in the broader beverage packaging market, represents a smaller, yet growing, segment for PET wine bottles, particularly for niche craft beers or premium offerings where shatterproof and lightweight characteristics are valued. The "Others" segment, encompassing aperitifs, fortified wines, and flavored wine coolers, also contributes to market growth, driven by innovation and the demand for specialized packaging solutions.

In terms of capacity, the 500–1,000 ML segment is the largest and fastest-growing, estimated to capture over forty-five percent of the market share. This size range perfectly aligns with standard wine bottle equivalents and caters to both individual consumption and small group gatherings. The increasing demand for premium single-serve wine options, often in sizes below 500 ML, is also driving growth in the <500 ML segment, which is projected to expand at a CAGR of over six percent. The >1,000 ML segment, while smaller, serves niche markets and bulk packaging needs, contributing to the overall market diversification.

Key growth drivers in these dominant segments include:

- Infrastructure Development: Enhanced logistics and distribution networks in emerging economies facilitate wider market access for PET wine bottles.

- Favorable Policies: Government policies promoting recycling and the use of recycled content in packaging provide a significant impetus for PET adoption.

- Consumer Demographics: The rise of the millennial and Gen Z demographics, who are more inclined towards convenience, portability, and sustainable choices, is a critical growth factor.

- Technological Advancements: Continuous improvements in barrier technologies and lightweighting of PET bottles are addressing traditional concerns, making them a more viable option for a wider range of wines.

- Cost-Effectiveness: Compared to glass, PET offers significant cost advantages in production, transportation, and reduced breakage, making it attractive for producers and consumers alike.

PET Wine Bottles Product Analysis

Product innovation in PET wine bottles is primarily focused on enhancing barrier properties to mimic those of glass, thereby extending wine shelf life and preserving delicate flavors. This includes the development of advanced multilayer structures incorporating oxygen scavengers and UV blockers, as well as the application of novel coatings. Lightweighting remains a key competitive advantage, reducing shipping costs and environmental impact. Furthermore, aesthetic innovations, such as sophisticated embossing, printing capabilities, and the introduction of colored PET, are allowing brands to create premium visual appeal, challenging the traditional dominance of glass in perceived quality. The market fit for these innovations is expanding from single-serve convenience formats to larger formats for everyday consumption and outdoor use, with an increasing emphasis on the use of recycled PET (rPET) to meet growing sustainability demands.

Key Drivers, Barriers & Challenges in PET Wine Bottles

Key Drivers:

- Sustainability Mandates: Growing global pressure for eco-friendly packaging, coupled with stricter regulations on plastic use and recycling targets, is a primary driver for the adoption of recyclable PET and rPET.

- Consumer Demand for Convenience: The increasing preference for lightweight, shatterproof, and portable packaging for on-the-go consumption, picnics, and events directly fuels the demand for PET wine bottles.

- Technological Advancements: Innovations in PET barrier technologies and lightweighting techniques are improving wine preservation and reducing material usage, making PET a more viable alternative to glass.

- Cost-Effectiveness: PET offers significant cost savings in production, transportation, and breakage reduction compared to glass, making it an attractive option for wineries, especially smaller producers.

Barriers & Challenges:

- Perception of Quality: A significant barrier remains the consumer perception that PET is inferior to glass for aging and premium wine storage, particularly for high-value vintages.

- Regulatory Hurdles: Varying national and regional regulations regarding plastic packaging, particularly concerning food contact materials and recyclability standards, can create complexity and compliance challenges.

- Supply Chain Volatility: Fluctuations in the price and availability of raw materials, especially virgin and recycled PET, can impact production costs and supply chain stability.

- Competitive Pressure from Glass: The established brand equity and long-standing tradition of glass packaging in the wine industry present a formidable competitive challenge.

Growth Drivers in the PET Wine Bottles Market

The PET wine bottle market is propelled by a dynamic interplay of economic, technological, and regulatory factors. Increasing consumer demand for convenience and portability, driven by lifestyle changes and a growing preference for outdoor activities, is a significant growth catalyst. Technologically, advancements in barrier properties, such as oxygen and moisture barriers, are effectively extending the shelf life of wine in PET, addressing a historical limitation. The growing global emphasis on sustainability, with governments implementing stricter recycling mandates and promoting the use of recycled content, directly favors PET's recyclability and lightweight advantages over glass. Furthermore, the cost-effectiveness of PET in terms of production and transportation offers a competitive edge, particularly for mass-market wines and smaller producers.

Challenges Impacting PET Wine Bottles Growth

Despite promising growth, the PET wine bottle market faces several critical challenges. A persistent barrier is the ingrained consumer perception of PET as a lower-quality packaging material compared to glass, especially for premium wines and those intended for aging. Regulatory complexities and inconsistencies across different regions regarding plastic packaging and food-contact safety can hinder widespread adoption and market entry. Supply chain vulnerabilities, including potential fluctuations in the availability and cost of raw materials, particularly recycled PET, pose a risk to production stability and pricing. Moreover, intense competition from established glass packaging manufacturers, who benefit from brand loyalty and traditional appeal, continues to exert pressure on the PET segment.

Key Players Shaping the PET Wine Bottles Market

- Petainer

- Amcor

- Alpla

- SIPA Solutions

- Packamama

- SGT

- Berry Global

- PDG Plastiques

- Frapak Packaging

- Young Shang Plastic Industry Co.,Ltd.

Significant PET Wine Bottles Industry Milestones

- 2019: Introduction of advanced oxygen-scavenging PET barrier technologies, significantly improving wine shelf-life in plastic bottles.

- 2020: Major beverage companies announce ambitious sustainability goals, including increased use of recycled PET (rPET) in their packaging portfolios.

- 2021: European Union strengthens its commitment to a circular economy, with new directives encouraging higher recycling rates and the use of recycled materials.

- 2022: Development of novel lightweighting PET resins and bottle designs, leading to further reductions in material usage and transportation emissions.

- 2023: Expansion of on-the-go wine consumption trends, with a surge in demand for single-serve and portable PET wine bottles.

- 2024: Increased investment in advanced chemical recycling technologies for PET, promising higher quality rPET for food-grade applications.

Future Outlook for PET Wine Bottles Market

The future outlook for the PET wine bottle market is overwhelmingly positive, driven by escalating demand for sustainable and convenient packaging solutions. Continued innovation in barrier technology will further bridge the gap with glass, enabling PET to capture a larger share of premium wine segments. The increasing availability and adoption of high-quality recycled PET (rPET) will significantly enhance the environmental credentials of these bottles, aligning perfectly with global sustainability targets and growing consumer preference for eco-conscious products. Strategic collaborations between PET manufacturers and wineries, alongside supportive governmental policies, will accelerate market penetration. The market is poised for substantial growth, fueled by an expanding global wine consumption base and the inherent advantages of PET in terms of weight, safety, and cost-effectiveness, presenting significant opportunities for industry stakeholders.

PET Wine Bottles Segmentation

-

1. Application

- 1.1. Red Wine

- 1.2. White Wine

- 1.3. Beer

- 1.4. Others

-

2. Types

- 2.1. Capacity:<500ML

- 2.2. Capacity:500-1,000ML

- 2.3. Capacity:>1,000ML

PET Wine Bottles Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

PET Wine Bottles Regional Market Share

Geographic Coverage of PET Wine Bottles

PET Wine Bottles REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Red Wine

- 5.1.2. White Wine

- 5.1.3. Beer

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Capacity:<500ML

- 5.2.2. Capacity:500-1,000ML

- 5.2.3. Capacity:>1,000ML

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global PET Wine Bottles Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Red Wine

- 6.1.2. White Wine

- 6.1.3. Beer

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Capacity:<500ML

- 6.2.2. Capacity:500-1,000ML

- 6.2.3. Capacity:>1,000ML

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America PET Wine Bottles Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Red Wine

- 7.1.2. White Wine

- 7.1.3. Beer

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Capacity:<500ML

- 7.2.2. Capacity:500-1,000ML

- 7.2.3. Capacity:>1,000ML

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America PET Wine Bottles Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Red Wine

- 8.1.2. White Wine

- 8.1.3. Beer

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Capacity:<500ML

- 8.2.2. Capacity:500-1,000ML

- 8.2.3. Capacity:>1,000ML

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe PET Wine Bottles Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Red Wine

- 9.1.2. White Wine

- 9.1.3. Beer

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Capacity:<500ML

- 9.2.2. Capacity:500-1,000ML

- 9.2.3. Capacity:>1,000ML

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa PET Wine Bottles Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Red Wine

- 10.1.2. White Wine

- 10.1.3. Beer

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Capacity:<500ML

- 10.2.2. Capacity:500-1,000ML

- 10.2.3. Capacity:>1,000ML

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific PET Wine Bottles Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Red Wine

- 11.1.2. White Wine

- 11.1.3. Beer

- 11.1.4. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Capacity:<500ML

- 11.2.2. Capacity:500-1,000ML

- 11.2.3. Capacity:>1,000ML

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Petainer

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Amcor

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Alpla

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 SIPA Solutions

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Packamama

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 SGT

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Berry Global

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 PDG Plastiques

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Frapak Packaging

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Young Shang Plastic Industry Co.

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Ltd.

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.1 Petainer

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global PET Wine Bottles Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: North America PET Wine Bottles Revenue (million), by Application 2025 & 2033

- Figure 3: North America PET Wine Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America PET Wine Bottles Revenue (million), by Types 2025 & 2033

- Figure 5: North America PET Wine Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America PET Wine Bottles Revenue (million), by Country 2025 & 2033

- Figure 7: North America PET Wine Bottles Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America PET Wine Bottles Revenue (million), by Application 2025 & 2033

- Figure 9: South America PET Wine Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America PET Wine Bottles Revenue (million), by Types 2025 & 2033

- Figure 11: South America PET Wine Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America PET Wine Bottles Revenue (million), by Country 2025 & 2033

- Figure 13: South America PET Wine Bottles Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe PET Wine Bottles Revenue (million), by Application 2025 & 2033

- Figure 15: Europe PET Wine Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe PET Wine Bottles Revenue (million), by Types 2025 & 2033

- Figure 17: Europe PET Wine Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe PET Wine Bottles Revenue (million), by Country 2025 & 2033

- Figure 19: Europe PET Wine Bottles Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa PET Wine Bottles Revenue (million), by Application 2025 & 2033

- Figure 21: Middle East & Africa PET Wine Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa PET Wine Bottles Revenue (million), by Types 2025 & 2033

- Figure 23: Middle East & Africa PET Wine Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa PET Wine Bottles Revenue (million), by Country 2025 & 2033

- Figure 25: Middle East & Africa PET Wine Bottles Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific PET Wine Bottles Revenue (million), by Application 2025 & 2033

- Figure 27: Asia Pacific PET Wine Bottles Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific PET Wine Bottles Revenue (million), by Types 2025 & 2033

- Figure 29: Asia Pacific PET Wine Bottles Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific PET Wine Bottles Revenue (million), by Country 2025 & 2033

- Figure 31: Asia Pacific PET Wine Bottles Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global PET Wine Bottles Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global PET Wine Bottles Revenue million Forecast, by Types 2020 & 2033

- Table 3: Global PET Wine Bottles Revenue million Forecast, by Region 2020 & 2033

- Table 4: Global PET Wine Bottles Revenue million Forecast, by Application 2020 & 2033

- Table 5: Global PET Wine Bottles Revenue million Forecast, by Types 2020 & 2033

- Table 6: Global PET Wine Bottles Revenue million Forecast, by Country 2020 & 2033

- Table 7: United States PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 8: Canada PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 9: Mexico PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 10: Global PET Wine Bottles Revenue million Forecast, by Application 2020 & 2033

- Table 11: Global PET Wine Bottles Revenue million Forecast, by Types 2020 & 2033

- Table 12: Global PET Wine Bottles Revenue million Forecast, by Country 2020 & 2033

- Table 13: Brazil PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: Argentina PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Global PET Wine Bottles Revenue million Forecast, by Application 2020 & 2033

- Table 17: Global PET Wine Bottles Revenue million Forecast, by Types 2020 & 2033

- Table 18: Global PET Wine Bottles Revenue million Forecast, by Country 2020 & 2033

- Table 19: United Kingdom PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 20: Germany PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 21: France PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 22: Italy PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 23: Spain PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 24: Russia PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 25: Benelux PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Nordics PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Global PET Wine Bottles Revenue million Forecast, by Application 2020 & 2033

- Table 29: Global PET Wine Bottles Revenue million Forecast, by Types 2020 & 2033

- Table 30: Global PET Wine Bottles Revenue million Forecast, by Country 2020 & 2033

- Table 31: Turkey PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 32: Israel PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 33: GCC PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 34: North Africa PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 35: South Africa PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 37: Global PET Wine Bottles Revenue million Forecast, by Application 2020 & 2033

- Table 38: Global PET Wine Bottles Revenue million Forecast, by Types 2020 & 2033

- Table 39: Global PET Wine Bottles Revenue million Forecast, by Country 2020 & 2033

- Table 40: China PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 41: India PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: Japan PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 43: South Korea PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: ASEAN PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 45: Oceania PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific PET Wine Bottles Revenue (million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the PET Wine Bottles?

The projected CAGR is approximately 3.5%.

2. Which companies are prominent players in the PET Wine Bottles?

Key companies in the market include Petainer, Amcor, Alpla, SIPA Solutions, Packamama, SGT, Berry Global, PDG Plastiques, Frapak Packaging, Young Shang Plastic Industry Co., Ltd..

3. What are the main segments of the PET Wine Bottles?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 222 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "PET Wine Bottles," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the PET Wine Bottles report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the PET Wine Bottles?

To stay informed about further developments, trends, and reports in the PET Wine Bottles, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence