Key Insights

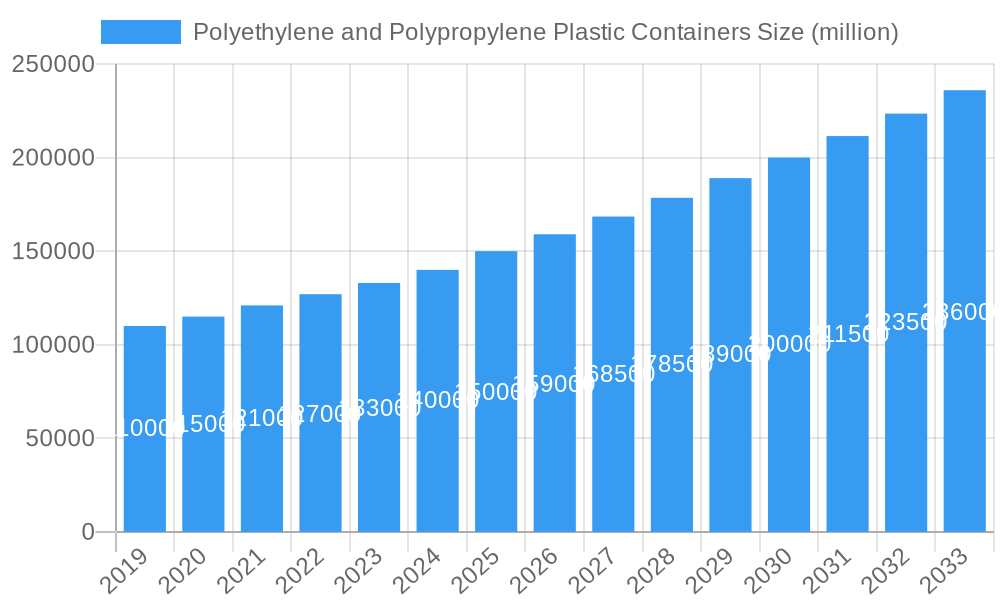

The global Polyethylene (PE) and Polypropylene (PP) Plastic Containers market is projected for substantial growth, reaching a market size of $229.67 billion by 2033, with a projected Compound Annual Growth Rate (CAGR) of 6.2% from the base year 2025 through 2033. The inherent versatility, durability, and cost-effectiveness of PE and PP containers drive their widespread adoption across diverse industries. The Food & Beverage sector is a key market, fueled by demand for convenient, safe, and appealing packaging. The Pharmaceutical industry also significantly contributes, utilizing these containers for secure storage and transport of medical supplies. Growing sustainability consciousness is shaping market trends, with a focus on innovative recycling initiatives and increasing adoption of post-consumer recycled (PCR) content.

Polyethylene and Polypropylene Plastic Containers Market Size (In Billion)

Key growth drivers include a rising middle class in emerging economies, particularly in the Asia Pacific region, boosting packaged goods consumption. Advancements in manufacturing technologies, leading to lighter and stronger container designs, enhance efficiency and reduce costs. The Fast-Moving Consumer Goods (FMCG) sector's continuous innovation also necessitates reliable packaging solutions. However, market growth faces challenges from stringent environmental regulations on single-use plastics and volatile raw material prices linked to crude oil. Despite these factors, the enduring advantages of PE and PP in product protection and shelf-life extension ensure their continued market leadership.

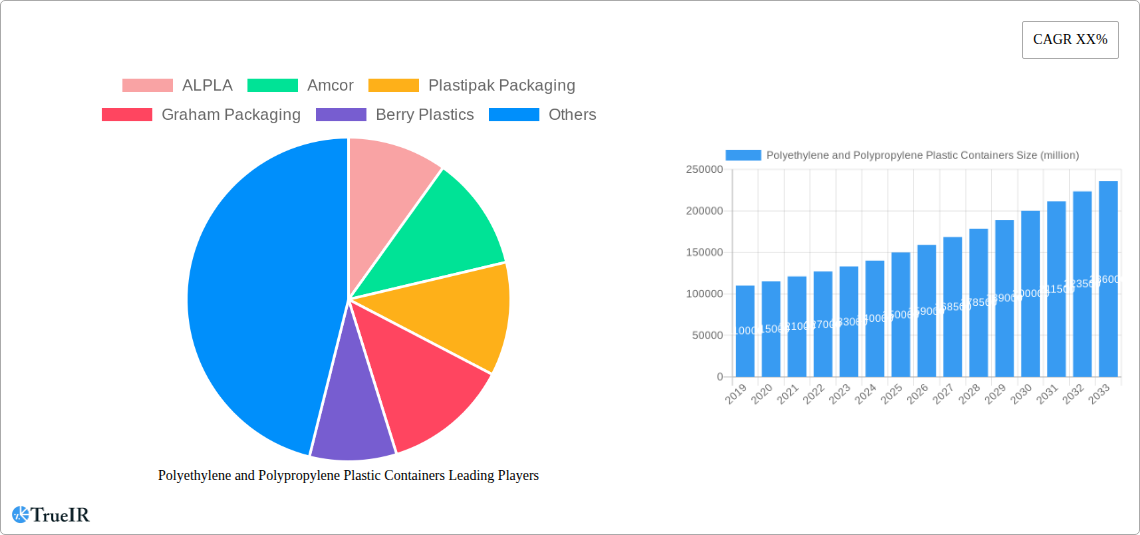

Polyethylene and Polypropylene Plastic Containers Company Market Share

This comprehensive market research report delivers an in-depth analysis of the global Polyethylene (PE) and Polypropylene (PP) Plastic Containers market. It forecasts a market size exceeding $229.67 billion by 2033, with a base year of 2025 and a forecast period up to 2033. The report provides crucial insights into market dynamics, trends, and opportunities, utilizing high-volume keywords such as "plastic packaging solutions," "PE containers," "PP containers," "food packaging," "pharmaceutical packaging," and "FMCG packaging" for optimal search engine visibility.

Polyethylene and Polypropylene Plastic Containers Market Structure & Competitive Landscape

The Polyethylene and Polypropylene Plastic Containers market is characterized by a moderate to high concentration, with leading players like Amcor, Plastipak Packaging, and Berry Plastics holding substantial market share. Innovation drivers are predominantly focused on enhanced barrier properties, lightweighting, and sustainable material development, responding to increasing consumer and regulatory demands. Regulatory impacts, particularly concerning single-use plastics and recycling mandates, are significantly shaping market strategies and investment. Product substitutes, such as glass and metal containers, pose a competitive threat, albeit often at a higher cost or with different performance characteristics. End-user segmentation reveals a strong reliance on the Food and Beverage Industry, followed by the Pharmaceutical Industry and the FMCG Industry, with the "Other Industry" segment also showing steady growth. Mergers and Acquisitions (M&A) activity is a key trend, with approximately 35 M&A deals recorded in the historical period, consolidating market power and expanding geographical reach. Key competitive advantages lie in cost-effectiveness, design flexibility, and advanced manufacturing capabilities.

- Market Concentration: Moderate to High.

- Innovation Drivers: Lightweighting, barrier properties, sustainability, recyclability.

- Regulatory Impacts: Single-use plastic bans, extended producer responsibility schemes.

- Product Substitutes: Glass, metal, paperboard containers.

- End-User Segmentation: Food & Beverage (highest share), Pharmaceutical, FMCG, Other.

- M&A Trends: Consolidation, strategic partnerships, capacity expansion.

- Quantifiable M&A Volume (Historical): Approximately 35 deals.

Polyethylene and Polypropylene Plastic Containers Market Trends & Opportunities

The global Polyethylene and Polypropylene Plastic Containers market is poised for robust growth, driven by an escalating demand for convenient, safe, and cost-effective packaging solutions across multiple industries. Market size growth is projected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.5% over the forecast period. Technological shifts are central to this expansion, with advancements in injection molding, blow molding, and extrusion techniques enabling the production of more complex, durable, and aesthetically pleasing containers. The increasing focus on lightweighting PE and PP containers not only reduces material costs but also contributes to lower transportation emissions, aligning with global sustainability initiatives. Consumer preferences are increasingly leaning towards products with extended shelf life and tamper-evident packaging, areas where plastic containers excel. The rise of e-commerce has also significantly boosted the demand for resilient and protective plastic packaging for shipping a wide range of goods. Competitive dynamics are intensifying, with companies investing heavily in R&D to develop bio-based and recycled content plastics, aiming to capture a larger share of the eco-conscious market. Opportunities abound in developing innovative dispensing mechanisms, smart packaging features that track product freshness, and specialized containers for niche applications within the pharmaceutical and chemical sectors. The penetration rate of plastic containers in emerging economies is also expected to rise substantially as disposable incomes increase and urbanization drives demand for packaged goods. The market penetration rate is estimated to reach over 70% by 2033.

Dominant Markets & Segments in Polyethylene and Polypropylene Plastic Containers

The Food and Beverage Industry stands as the dominant market segment for Polyethylene and Polypropylene Plastic Containers, driven by the pervasive need for safe, hygienic, and shelf-stable packaging for a vast array of consumables. This dominance is underpinned by the inherent properties of PE and PP, such as their chemical resistance, moisture barrier, and formability, making them ideal for everything from beverage bottles and food tubs to condiment squeeze bottles and dairy product containers. The sheer volume of food and beverage production globally, coupled with evolving consumer lifestyles that favor convenience and portability, ensures sustained demand.

- Key Growth Drivers in Food & Beverage:

- Infrastructure Development: Expanding food processing and distribution networks, particularly in emerging economies.

- Consumer Lifestyles: Increasing demand for ready-to-eat meals, single-serving portions, and on-the-go consumption.

- Food Safety Regulations: Stringent requirements for hygiene and prevention of contamination favor reliable plastic packaging.

- Innovation in Packaging: Development of active and intelligent packaging to extend shelf life and monitor freshness.

The Transparent container type holds a significant share within this segment, allowing consumers to visually assess product quality and quantity, thereby fostering trust and driving purchasing decisions. The Colorful segment, while also substantial, is often employed for branding and differentiation, especially in snack foods and confectionery.

The Pharmaceutical Industry represents another critical and high-growth segment. Here, the emphasis is on sterility, chemical inertness, and tamper-evident sealing. PE and PP are extensively used for medication bottles, blister packs, syringes, and diagnostic kits. The growing global healthcare expenditure and the continuous development of new drugs are key catalysts for this segment's expansion.

- Key Growth Drivers in Pharmaceutical:

- Global Healthcare Spending: Increasing investment in healthcare infrastructure and new drug development.

- Demand for Specialty Drugs: Growth in biologics and complex drug formulations requiring specialized packaging.

- Regulatory Compliance: Strict adherence to pharmaceutical packaging standards ensures the integrity and safety of medicines.

- Patient Convenience: Development of easy-to-open and child-resistant closures.

The FMCG Industry broadly encompasses a wide range of consumer goods, from personal care products and household cleaners to cosmetics. The versatility of PE and PP in creating a myriad of container shapes, sizes, and dispensing mechanisms makes them indispensable for this sector. The "Other Industry" segment includes applications in automotive fluids, industrial chemicals, and agricultural products, each contributing to the overall market demand.

Polyethylene and Polypropylene Plastic Containers Product Analysis

Polyethylene and Polypropylene plastic containers are defined by their exceptional versatility and cost-effectiveness. Innovations focus on improving barrier properties, enhancing impact resistance, and reducing material usage through advanced design and manufacturing techniques like monolayer and multilayer extrusion. Applications span a broad spectrum, from rigid bottles and jars for food and beverages to flexible pouches and tubs for pharmaceuticals and FMCG products. Competitive advantages stem from their inherent chemical stability, durability, lightweight nature, and excellent recyclability potential when properly managed. Market fit is further optimized through customization of color, clarity, and specific functional features, such as tamper-evident seals and specialized dispensing caps, directly addressing end-user needs for safety, convenience, and product integrity.

Key Drivers, Barriers & Challenges in Polyethylene and Polypropylene Plastic Containers

Key Drivers: The Polyethylene and Polypropylene Plastic Containers market is propelled by several key drivers, including the growing global population and increasing demand for packaged goods across the Food & Beverage, Pharmaceutical, and FMCG sectors. Technological advancements in polymer science and manufacturing processes contribute to lighter, stronger, and more sustainable container options. The inherent cost-effectiveness and versatility of PE and PP make them the preferred choice for many applications. Furthermore, government initiatives promoting recycling and the circular economy, alongside corporate sustainability goals, are driving innovation in post-consumer recycled (PCR) content integration.

Key Barriers & Challenges: Despite strong growth prospects, the market faces significant barriers and challenges. Increasing environmental concerns and regulatory pressure regarding plastic waste and pollution are leading to a push for alternatives and stricter disposal regulations. Supply chain disruptions, including fluctuating raw material prices and availability, can impact production costs and lead times. Intense competition from alternative packaging materials and other plastic types, along with the need for significant investment in recycling infrastructure, also present considerable hurdles. Overcoming consumer perception issues related to plastic sustainability remains an ongoing challenge for the industry.

Growth Drivers in the Polyethylene and Polypropylene Plastic Containers Market

The growth of the Polyethylene and Polypropylene Plastic Containers market is significantly influenced by several factors. Economically, rising disposable incomes and urbanization in emerging economies are fueling demand for packaged consumer goods. Technologically, advancements in polymer engineering are enabling the creation of more sophisticated and sustainable packaging solutions, including lightweighting and the incorporation of recycled content. Regulatory support for the circular economy and the development of improved recycling infrastructure are also critical drivers, encouraging the use of recyclable materials. The Food and Beverage sector's continuous demand for safe, convenient, and extended shelf-life packaging remains a primary growth catalyst.

Challenges Impacting Polyethylene and Polypropylene Plastic Containers Growth

The expansion of the Polyethylene and Polypropylene Plastic Containers market is constrained by several impactful challenges. Heightened environmental consciousness among consumers and governments has led to increased scrutiny of plastic waste, driving demand for biodegradable or easily recyclable alternatives. Stringent regulations on single-use plastics and mandatory recycling targets can impose additional compliance costs. Supply chain vulnerabilities, including volatility in the price of oil and natural gas (key feedstocks for PE and PP), pose a significant risk to profitability. Moreover, the complex global infrastructure required for effective collection, sorting, and recycling of plastic waste, alongside the competition from established materials like glass and metal, presents ongoing obstacles to sustained growth.

Key Players Shaping the Polyethylene and Polypropylene Plastic Containers Market

- ALPLA

- Amcor

- Plastipak Packaging

- Graham Packaging

- Berry Plastics

- Greiner Packaging

- Alpha Packaging

- Visy

- Zhongfu-Shenying Carbon Fiber

- Polycon Industries

- KW Plastics

- Boxmore Packaging

Significant Polyethylene and Polypropylene Plastic Containers Industry Milestones

- 2019/05: Amcor acquires Bemis, significantly expanding its flexible packaging and rigid container portfolio.

- 2020/01: Berry Global Group announces acquisition of RPC Group, enhancing its presence in rigid plastics in Europe.

- 2021/03: Introduction of new lightweighting technologies by major players, reducing material consumption by up to 15%.

- 2022/07: Increased investment in advanced recycling technologies, including chemical recycling, by industry leaders.

- 2023/02: Growing adoption of post-consumer recycled (PCR) content in food-grade packaging, driven by regulatory and consumer demand.

- 2024/06: Development of innovative barrier coatings for PE and PP to improve product shelf life without compromising recyclability.

Future Outlook for Polyethylene and Polypropylene Plastic Containers Market

The future outlook for the Polyethylene and Polypropylene Plastic Containers market is overwhelmingly positive, driven by continued innovation and adaptation to sustainability demands. Strategic opportunities lie in the development of advanced recycling solutions, including enhanced mechanical and chemical recycling processes, to create a truly circular economy for plastics. The growing demand for specialized packaging in the pharmaceutical and nutraceutical sectors, coupled with the convenience-driven growth of the food and beverage industry, will continue to fuel market expansion. Companies that prioritize sustainable material development, invest in lightweighting technologies, and demonstrate robust compliance with evolving regulations are best positioned to capitalize on the projected market growth, estimated to reach over $350 million by 2033 with a CAGR of approximately 5.5%.

Polyethylene and Polypropylene Plastic Containers Segmentation

-

1. Application

- 1.1. Food and Beverage Industry

- 1.2. Pharmaceutical Industry

- 1.3. FMCG Industry

- 1.4. Other Industry

-

2. Types

- 2.1. Colorful

- 2.2. Transparent

Polyethylene and Polypropylene Plastic Containers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

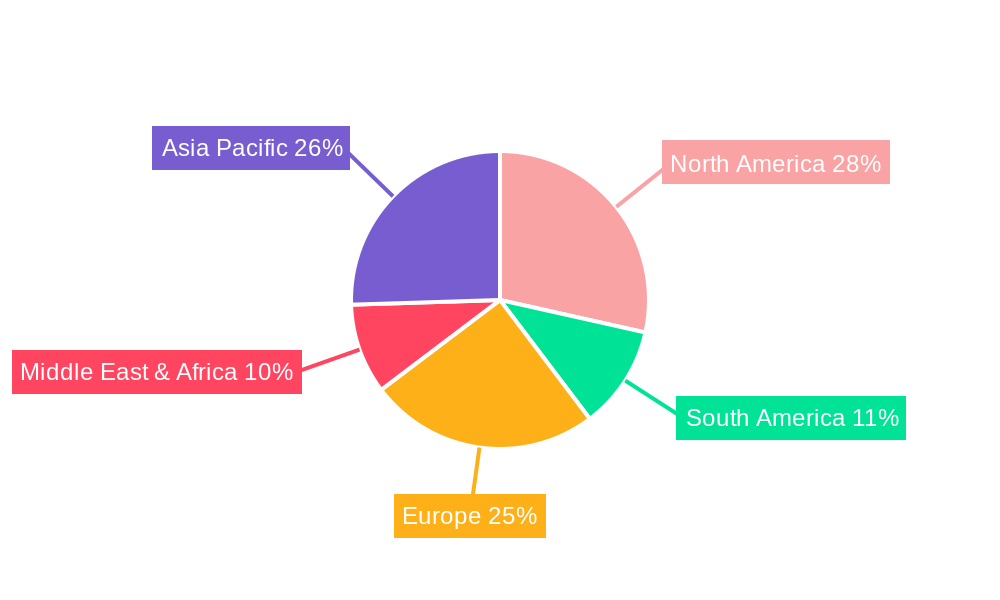

Polyethylene and Polypropylene Plastic Containers Regional Market Share

Geographic Coverage of Polyethylene and Polypropylene Plastic Containers

Polyethylene and Polypropylene Plastic Containers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food and Beverage Industry

- 5.1.2. Pharmaceutical Industry

- 5.1.3. FMCG Industry

- 5.1.4. Other Industry

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Colorful

- 5.2.2. Transparent

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Polyethylene and Polypropylene Plastic Containers Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food and Beverage Industry

- 6.1.2. Pharmaceutical Industry

- 6.1.3. FMCG Industry

- 6.1.4. Other Industry

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Colorful

- 6.2.2. Transparent

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Polyethylene and Polypropylene Plastic Containers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food and Beverage Industry

- 7.1.2. Pharmaceutical Industry

- 7.1.3. FMCG Industry

- 7.1.4. Other Industry

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Colorful

- 7.2.2. Transparent

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Polyethylene and Polypropylene Plastic Containers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food and Beverage Industry

- 8.1.2. Pharmaceutical Industry

- 8.1.3. FMCG Industry

- 8.1.4. Other Industry

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Colorful

- 8.2.2. Transparent

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Polyethylene and Polypropylene Plastic Containers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food and Beverage Industry

- 9.1.2. Pharmaceutical Industry

- 9.1.3. FMCG Industry

- 9.1.4. Other Industry

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Colorful

- 9.2.2. Transparent

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Polyethylene and Polypropylene Plastic Containers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food and Beverage Industry

- 10.1.2. Pharmaceutical Industry

- 10.1.3. FMCG Industry

- 10.1.4. Other Industry

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Colorful

- 10.2.2. Transparent

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Polyethylene and Polypropylene Plastic Containers Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Food and Beverage Industry

- 11.1.2. Pharmaceutical Industry

- 11.1.3. FMCG Industry

- 11.1.4. Other Industry

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Colorful

- 11.2.2. Transparent

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 ALPLA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Amcor

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Plastipak Packaging

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Graham Packaging

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Berry Plastics

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Greiner Packaging

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Alpha Packaging

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Visy

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Zhongfu-Shenying Carbon Fiber

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Polycon Industries

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 KW Plastics

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Boxmore Packaging

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.1 ALPLA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Polyethylene and Polypropylene Plastic Containers Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Polyethylene and Polypropylene Plastic Containers Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Polyethylene and Polypropylene Plastic Containers Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Polyethylene and Polypropylene Plastic Containers Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Polyethylene and Polypropylene Plastic Containers Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Polyethylene and Polypropylene Plastic Containers?

The projected CAGR is approximately 6.2%.

2. Which companies are prominent players in the Polyethylene and Polypropylene Plastic Containers?

Key companies in the market include ALPLA, Amcor, Plastipak Packaging, Graham Packaging, Berry Plastics, Greiner Packaging, Alpha Packaging, Visy, Zhongfu-Shenying Carbon Fiber, Polycon Industries, KW Plastics, Boxmore Packaging.

3. What are the main segments of the Polyethylene and Polypropylene Plastic Containers?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 229.67 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Polyethylene and Polypropylene Plastic Containers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Polyethylene and Polypropylene Plastic Containers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Polyethylene and Polypropylene Plastic Containers?

To stay informed about further developments, trends, and reports in the Polyethylene and Polypropylene Plastic Containers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence