Key Insights

The global Scuff Resistant Packaging market is projected for substantial growth, expected to reach $15.21 billion by 2025, with an estimated Compound Annual Growth Rate (CAGR) of 7.4% through 2033. This expansion is driven by escalating demand in key sectors such as Food & Beverages and Retail & Consumer Goods, where product integrity and presentation are critical. Growing manufacturer awareness of the necessity to prevent cosmetic damage during transit and handling is accelerating adoption. The automotive and cosmetics industries further contribute to market momentum, prioritizing component protection and premium packaging respectively. The "Others" segment, representing specialized industrial applications, also offers significant growth potential.

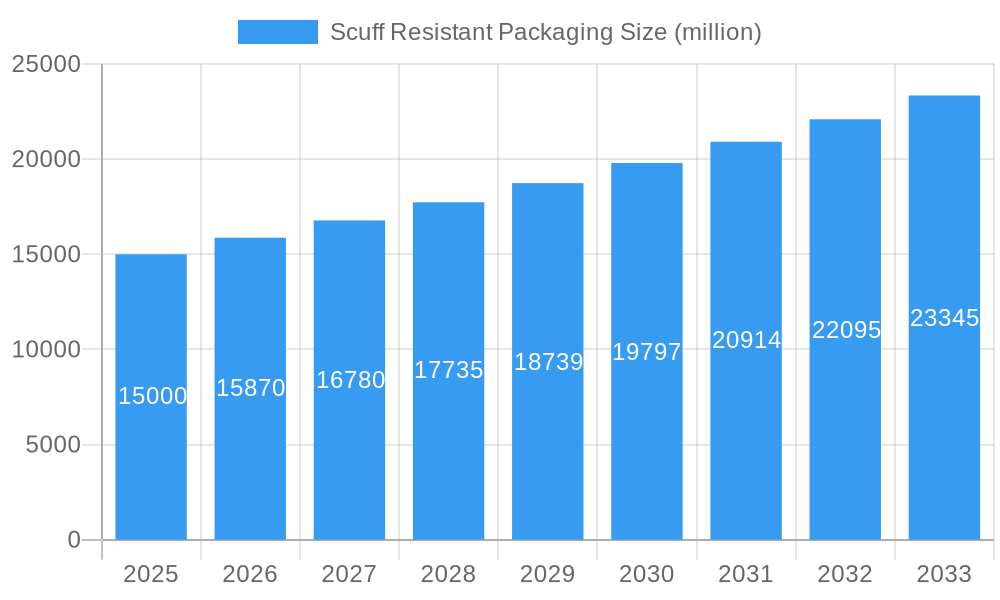

Scuff Resistant Packaging Market Size (In Billion)

Key trends influencing the scuff-resistant packaging market include the integration of advanced coating technologies and material science for enhanced abrasion resistance without sacrificing flexibility or recyclability. The adoption of sustainable, eco-friendly materials is a significant focus, driven by environmental regulations and consumer demand. While challenges such as higher initial costs for specialized materials and potential recycling complexities exist, the benefits of reduced product returns, improved brand image, and supply chain efficiency are expected to drive sustained investment and innovation.

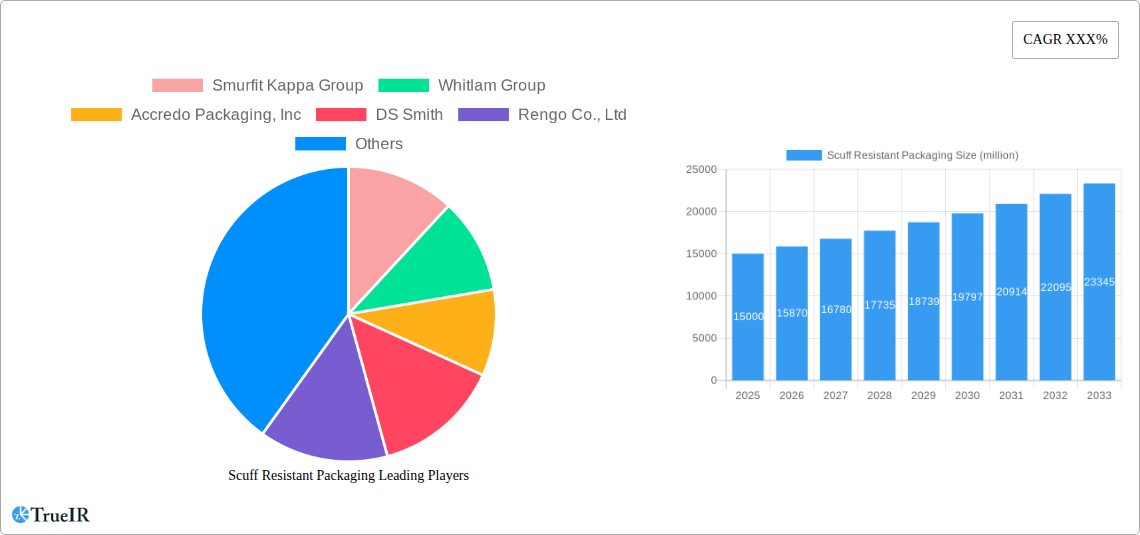

Scuff Resistant Packaging Company Market Share

Scuff Resistant Packaging Market: A Comprehensive Industry Analysis and Forecast (2019-2033)

This in-depth report provides a dynamic and SEO-optimized analysis of the global scuff resistant packaging market. Leveraging high-volume keywords and comprehensive data, it offers critical insights for industry stakeholders, including manufacturers, suppliers, investors, and end-users. The study encompasses a detailed examination of market structure, competitive landscape, emerging trends, dominant segments, product innovations, key growth drivers, challenges, and a forward-looking outlook, with a particular focus on the period from 2019 to 2033, with 2025 as the base and estimated year.

Scuff Resistant Packaging Market Structure & Competitive Landscape

The scuff resistant packaging market exhibits a moderate to high concentration, with several key players dominating significant portions of the global share. Innovation serves as a primary driver, with companies investing heavily in R&D to develop advanced materials and coatings that offer superior scratch and abrasion resistance. Regulatory impacts, while present, are primarily focused on sustainability and material safety, indirectly influencing the adoption of advanced scuff resistant solutions. Product substitutes, such as enhanced conventional packaging or alternative protective solutions, exist but often fall short of the integrated protective qualities offered by dedicated scuff resistant materials. End-user segmentation highlights the varied demands across industries like Food & Beverages and Electronics, influencing material selection and product development. Mergers and acquisitions (M&A) activity has been moderate, with strategic consolidations aimed at expanding market reach, acquiring new technologies, and enhancing product portfolios. For instance, the past five years have seen approximately 5-10 significant M&A deals, with an estimated cumulative deal value exceeding one million dollars, aimed at consolidating market positions and fostering innovation. Concentration ratios, particularly in specialized niche segments, can reach up to 60-70% for the top three players.

Scuff Resistant Packaging Market Trends & Opportunities

The global scuff resistant packaging market is poised for substantial growth, driven by an escalating demand for enhanced product protection and visual appeal across a multitude of industries. Projections indicate a Compound Annual Growth Rate (CAGR) of approximately 7-9% over the forecast period of 2025–2033, translating into a market size that could surpass several million dollars by 2033. Technological shifts are at the forefront, with advancements in polymer science and coating technologies leading to the development of more durable, aesthetically pleasing, and environmentally friendly scuff resistant solutions. The rise of high-definition printing and digital embellishments necessitates packaging that can maintain its pristine appearance throughout the supply chain, thus fueling the adoption of scuff resistant materials. Consumer preferences are increasingly leaning towards premium, unblemished product presentation, especially in sectors like cosmetics and electronics, where visual appeal is intrinsically linked to perceived product quality. This trend is a significant market penetration driver. Competitive dynamics are characterized by an intense focus on product differentiation through enhanced performance characteristics, such as increased resistance to chemicals, UV radiation, and extreme temperatures, alongside improved scuff resistance. The development of sustainable and recyclable scuff resistant packaging options is also emerging as a critical trend, aligning with global environmental initiatives and consumer demand for eco-friendly products. Opportunities abound in developing customized solutions for niche applications, such as the automotive sector for interior components and the pharmaceutical industry for tamper-evident and protection-focused primary packaging. The expanding e-commerce landscape, with its inherent challenges of increased handling and transit, presents another vast avenue for growth as businesses seek to minimize product damage and returns.

Dominant Markets & Segments in Scuff Resistant Packaging

The Food & Beverages segment is a dominant force within the scuff resistant packaging market, driven by the need to preserve product freshness, prevent visual damage to attractive packaging, and ensure safety throughout complex distribution networks. The sheer volume of products, coupled with stringent hygiene and aesthetic requirements, makes this sector a prime beneficiary of advanced scuff resistant solutions. In parallel, the Retail and Consumer Goods segment exhibits robust growth, fueled by the constant introduction of new products, the importance of shelf appeal, and the increasing prevalence of direct-to-consumer shipping where packaging integrity is paramount. The Electronics segment also holds significant sway, as the high value and delicate nature of electronic devices necessitate superior protection against scratches and scuffs during manufacturing, shipping, and handling.

Within the Type segmentation, Polyester (PET) and Polypropylene (OPP) are expected to command the largest market shares due to their versatility, cost-effectiveness, and inherent barrier properties, which can be further enhanced with scuff resistant coatings. Nylon finds its niche in applications requiring exceptional toughness and puncture resistance, often in demanding environments.

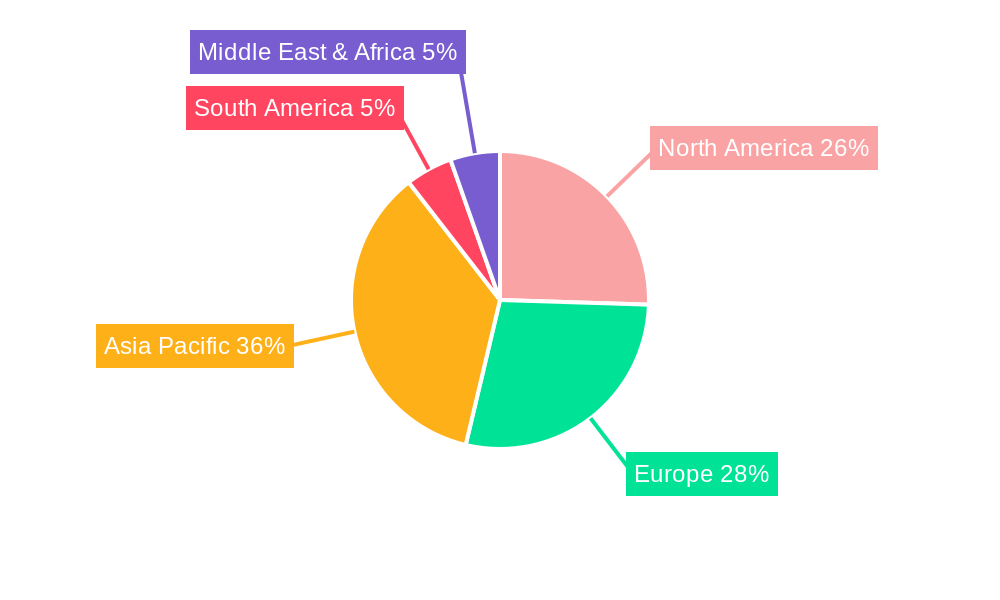

Geographically, North America and Europe are anticipated to remain dominant markets, characterized by advanced manufacturing capabilities, high consumer spending, and a strong emphasis on product quality. However, the Asia-Pacific region is poised for the most rapid growth. This surge is attributed to the burgeoning manufacturing sector, a rapidly expanding middle class with increasing disposable income, and significant investments in infrastructure development, including advanced warehousing and logistics networks. Government policies promoting industrialization and consumer protection also play a crucial role in driving the adoption of high-performance packaging solutions in these emerging economies. The growth drivers in these dominant regions and segments include:

- Food & Beverages:

- Demand for extended shelf life and visual appeal of packaged foods.

- Stringent regulations for food safety and hygiene.

- Growth of the ready-to-eat and convenience food market.

- Retail and Consumer Goods:

- High product differentiation and brand competition on shelves.

- Booming e-commerce sector requiring robust transit packaging.

- Increasing consumer focus on premium product presentation.

- Electronics:

- High value of goods and need to prevent cosmetic damage.

- Sophisticated product designs that are susceptible to scuffing.

- Globalized supply chains with multiple handling points.

- Polyester (PET) & Polypropylene (OPP):

- Cost-effectiveness and excellent printability.

- Good barrier properties against moisture and oxygen.

- Wide availability and established manufacturing processes.

- Asia-Pacific Region:

- Rapid industrialization and manufacturing hub status.

- Growing middle-class population and increased consumer spending.

- Government initiatives supporting advanced packaging technologies.

Scuff Resistant Packaging Product Analysis

Innovations in scuff resistant packaging are primarily focused on enhancing surface durability, improving aesthetic appeal, and integrating sustainable features. Advanced coating technologies, including hard coats and specialized polymer formulations, are being developed to provide superior resistance to abrasion and scratching without compromising flexibility or printability. These advancements allow for the creation of packaging that maintains its pristine appearance throughout the product lifecycle, from manufacturing to consumer unboxing. The competitive advantage lies in offering solutions that not only protect the product but also elevate the brand image through enhanced visual presentation and tactile experience. Market fit is achieved by tailoring these innovations to specific end-use requirements, such as the demanding conditions of the automotive industry or the premium aesthetic needs of the cosmetics sector.

Key Drivers, Barriers & Challenges in Scuff Resistant Packaging

Key Drivers, Barriers & Challenges in Scuff Resistant Packaging

The scuff resistant packaging market is propelled by several key drivers. Technological advancements in polymer science and coating technologies are leading to more effective and versatile scuff resistant solutions. The growing demand for enhanced product protection to minimize damage during transit and handling, especially with the rise of e-commerce, is a significant economic driver. Furthermore, increasing consumer expectations for premium product presentation and brand integrity directly influence the adoption of these advanced packaging materials. Regulatory pushes towards sustainable packaging solutions, while a challenge, also drive innovation in developing eco-friendly scuff resistant alternatives.

Conversely, the market faces significant barriers and challenges. The initial cost of implementing advanced scuff resistant packaging solutions can be higher than conventional alternatives, posing an economic restraint for smaller businesses. Supply chain complexities, including the sourcing of specialized raw materials and ensuring consistent quality, can create hurdles. Regulatory complexities, particularly regarding the recyclability and end-of-life management of certain composite scuff resistant materials, require careful navigation. Intense competitive pressures from established packaging providers and the constant need for innovation to stay ahead of market demands also present ongoing challenges, with estimated impacts on market share that can fluctuate by several percentage points annually based on competitor strategies.

Growth Drivers in the Scuff Resistant Packaging Market

Key growth drivers in the scuff resistant packaging market include the escalating demand for premium product presentation, particularly in the cosmetics, electronics, and luxury goods sectors. Technological innovations in material science, leading to enhanced scratch and abrasion resistance, are crucial economic and technological drivers. The expanding e-commerce landscape, with its inherent need to protect goods during multiple transit points, further fuels growth. Government initiatives promoting product quality and consumer satisfaction also play a supportive role. For example, the increasing focus on reducing product returns due to cosmetic damage in the electronics sector directly translates into a demand for robust scuff resistant packaging.

Challenges Impacting Scuff Resistant Packaging Growth

Challenges impacting scuff resistant packaging growth include the higher initial investment costs compared to conventional packaging, which can be a significant barrier for SMEs. Regulatory complexities surrounding the recyclability and disposal of certain advanced scuff resistant materials require ongoing attention and innovation to ensure compliance with environmental standards. Supply chain disruptions, including fluctuations in raw material availability and pricing, can impact production and profitability. Furthermore, intense competition necessitates continuous investment in R&D to maintain a competitive edge and address the evolving demands of end-use industries, potentially leading to price pressures and reduced profit margins for less innovative players.

Key Players Shaping the Scuff Resistant Packaging Market

- Smurfit Kappa Group

- Whitlam Group

- Accredo Packaging, Inc

- DS Smith

- Rengo Co., Ltd

- Georgia-Pacific LLC.

Significant Scuff Resistant Packaging Industry Milestones

- 2019: Launch of new, highly durable scuff resistant coatings with enhanced UV protection by leading chemical manufacturers.

- 2020: Increased adoption of scuff resistant films for premium food and beverage packaging to maintain shelf appeal.

- 2021: Major electronics manufacturers begin specifying scuff resistant packaging as standard for high-end devices.

- 2022: Advancements in sustainable scuff resistant barrier coatings for flexible packaging solutions.

- 2023: Strategic partnerships formed between material suppliers and packaging converters to co-develop customized scuff resistant solutions.

- 2024 (Estimated): Introduction of bio-based scuff resistant polymers with comparable performance to traditional plastics.

Future Outlook for Scuff Resistant Packaging Market

The future outlook for the scuff resistant packaging market is exceptionally bright, driven by an unwavering demand for superior product protection and enhanced consumer experiences. Strategic opportunities lie in the continued development of sustainable and recyclable scuff resistant materials that meet stringent environmental regulations and consumer preferences. The market potential is vast, particularly with the ongoing expansion of the e-commerce sector and the increasing focus on premiumization across various consumer goods categories. Innovations in smart packaging integrating scuff resistance with other functionalities like track-and-trace capabilities will also shape future growth, offering significant market potential for forward-thinking companies.

Scuff Resistant Packaging Segmentation

-

1. Application

- 1.1. Food & Beverages

- 1.2. Retail and Consumer goods

- 1.3. Automotive

- 1.4. Cosmetics

- 1.5. Pharmaceuticals

- 1.6. Electronics

- 1.7. Others

-

2. Type

- 2.1. Polyester (PET)

- 2.2. Polypropylene (OPP)

- 2.3. Nylon

- 2.4. Others

Scuff Resistant Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Scuff Resistant Packaging Regional Market Share

Geographic Coverage of Scuff Resistant Packaging

Scuff Resistant Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food & Beverages

- 5.1.2. Retail and Consumer goods

- 5.1.3. Automotive

- 5.1.4. Cosmetics

- 5.1.5. Pharmaceuticals

- 5.1.6. Electronics

- 5.1.7. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Polyester (PET)

- 5.2.2. Polypropylene (OPP)

- 5.2.3. Nylon

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Scuff Resistant Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food & Beverages

- 6.1.2. Retail and Consumer goods

- 6.1.3. Automotive

- 6.1.4. Cosmetics

- 6.1.5. Pharmaceuticals

- 6.1.6. Electronics

- 6.1.7. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Polyester (PET)

- 6.2.2. Polypropylene (OPP)

- 6.2.3. Nylon

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Scuff Resistant Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food & Beverages

- 7.1.2. Retail and Consumer goods

- 7.1.3. Automotive

- 7.1.4. Cosmetics

- 7.1.5. Pharmaceuticals

- 7.1.6. Electronics

- 7.1.7. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Polyester (PET)

- 7.2.2. Polypropylene (OPP)

- 7.2.3. Nylon

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Scuff Resistant Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food & Beverages

- 8.1.2. Retail and Consumer goods

- 8.1.3. Automotive

- 8.1.4. Cosmetics

- 8.1.5. Pharmaceuticals

- 8.1.6. Electronics

- 8.1.7. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Polyester (PET)

- 8.2.2. Polypropylene (OPP)

- 8.2.3. Nylon

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Scuff Resistant Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food & Beverages

- 9.1.2. Retail and Consumer goods

- 9.1.3. Automotive

- 9.1.4. Cosmetics

- 9.1.5. Pharmaceuticals

- 9.1.6. Electronics

- 9.1.7. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Polyester (PET)

- 9.2.2. Polypropylene (OPP)

- 9.2.3. Nylon

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Scuff Resistant Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food & Beverages

- 10.1.2. Retail and Consumer goods

- 10.1.3. Automotive

- 10.1.4. Cosmetics

- 10.1.5. Pharmaceuticals

- 10.1.6. Electronics

- 10.1.7. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Polyester (PET)

- 10.2.2. Polypropylene (OPP)

- 10.2.3. Nylon

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Scuff Resistant Packaging Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Food & Beverages

- 11.1.2. Retail and Consumer goods

- 11.1.3. Automotive

- 11.1.4. Cosmetics

- 11.1.5. Pharmaceuticals

- 11.1.6. Electronics

- 11.1.7. Others

- 11.2. Market Analysis, Insights and Forecast - by Type

- 11.2.1. Polyester (PET)

- 11.2.2. Polypropylene (OPP)

- 11.2.3. Nylon

- 11.2.4. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Smurfit Kappa Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Whitlam Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Accredo Packaging Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 DS Smith

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Rengo Co. Ltd

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Georgia-Pacific LLC.

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.1 Smurfit Kappa Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Scuff Resistant Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Scuff Resistant Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Scuff Resistant Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Scuff Resistant Packaging Revenue (billion), by Type 2025 & 2033

- Figure 5: North America Scuff Resistant Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 6: North America Scuff Resistant Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Scuff Resistant Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Scuff Resistant Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Scuff Resistant Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Scuff Resistant Packaging Revenue (billion), by Type 2025 & 2033

- Figure 11: South America Scuff Resistant Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 12: South America Scuff Resistant Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Scuff Resistant Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Scuff Resistant Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Scuff Resistant Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Scuff Resistant Packaging Revenue (billion), by Type 2025 & 2033

- Figure 17: Europe Scuff Resistant Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 18: Europe Scuff Resistant Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Scuff Resistant Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Scuff Resistant Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Scuff Resistant Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Scuff Resistant Packaging Revenue (billion), by Type 2025 & 2033

- Figure 23: Middle East & Africa Scuff Resistant Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 24: Middle East & Africa Scuff Resistant Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Scuff Resistant Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Scuff Resistant Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Scuff Resistant Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Scuff Resistant Packaging Revenue (billion), by Type 2025 & 2033

- Figure 29: Asia Pacific Scuff Resistant Packaging Revenue Share (%), by Type 2025 & 2033

- Figure 30: Asia Pacific Scuff Resistant Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Scuff Resistant Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Scuff Resistant Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Scuff Resistant Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 3: Global Scuff Resistant Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Scuff Resistant Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Scuff Resistant Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global Scuff Resistant Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Scuff Resistant Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Scuff Resistant Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global Scuff Resistant Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Scuff Resistant Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Scuff Resistant Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 18: Global Scuff Resistant Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Scuff Resistant Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Scuff Resistant Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 30: Global Scuff Resistant Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Scuff Resistant Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Scuff Resistant Packaging Revenue billion Forecast, by Type 2020 & 2033

- Table 39: Global Scuff Resistant Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Scuff Resistant Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Scuff Resistant Packaging?

The projected CAGR is approximately 7.4%.

2. Which companies are prominent players in the Scuff Resistant Packaging?

Key companies in the market include Smurfit Kappa Group, Whitlam Group, Accredo Packaging, Inc, DS Smith, Rengo Co., Ltd, Georgia-Pacific LLC..

3. What are the main segments of the Scuff Resistant Packaging?

The market segments include Application, Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 15.21 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Scuff Resistant Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Scuff Resistant Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Scuff Resistant Packaging?

To stay informed about further developments, trends, and reports in the Scuff Resistant Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence