Key Insights

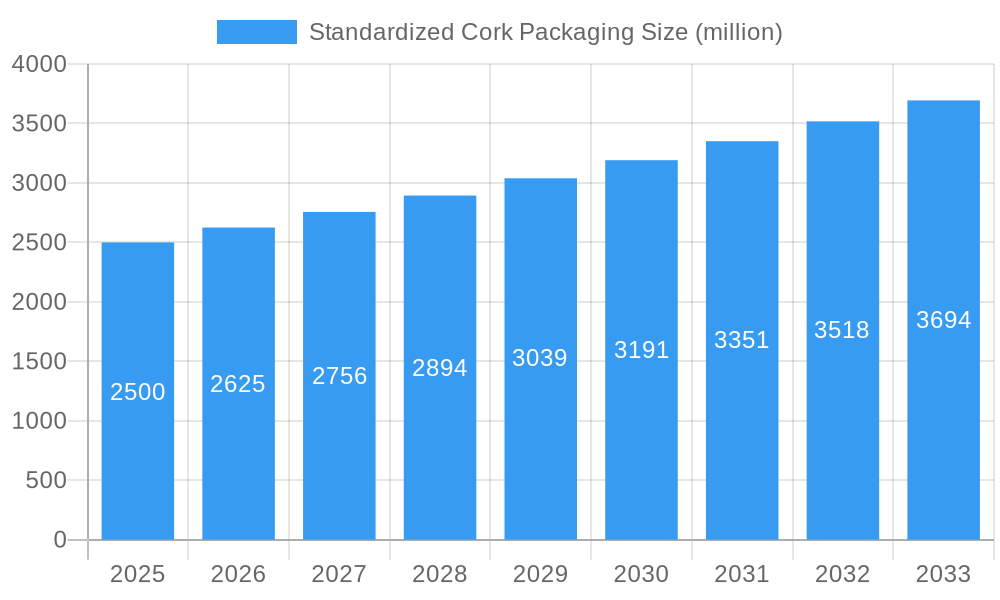

The global Standardized Cork Packaging market is poised for robust expansion, projected to reach approximately USD 2.5 billion in 2025 and exhibit a Compound Annual Growth Rate (CAGR) of 5% through 2033. This sustained growth is primarily fueled by the escalating demand for natural and sustainable packaging solutions across various industries. The inherent eco-friendliness of cork, being a renewable and biodegradable material, aligns perfectly with increasing consumer and regulatory preferences for environmentally responsible products. Key drivers include the premium image associated with cork, particularly in the wine and spirits sector, where it signifies quality and heritage. Furthermore, advancements in cork processing and manufacturing technologies are leading to the development of innovative cork packaging formats and enhanced performance characteristics, broadening its appeal beyond traditional applications. The cosmetics and personal care industry is increasingly adopting cork for its natural aesthetics and tactile appeal, while other burgeoning applications in food preservation and niche industrial uses contribute to market diversification.

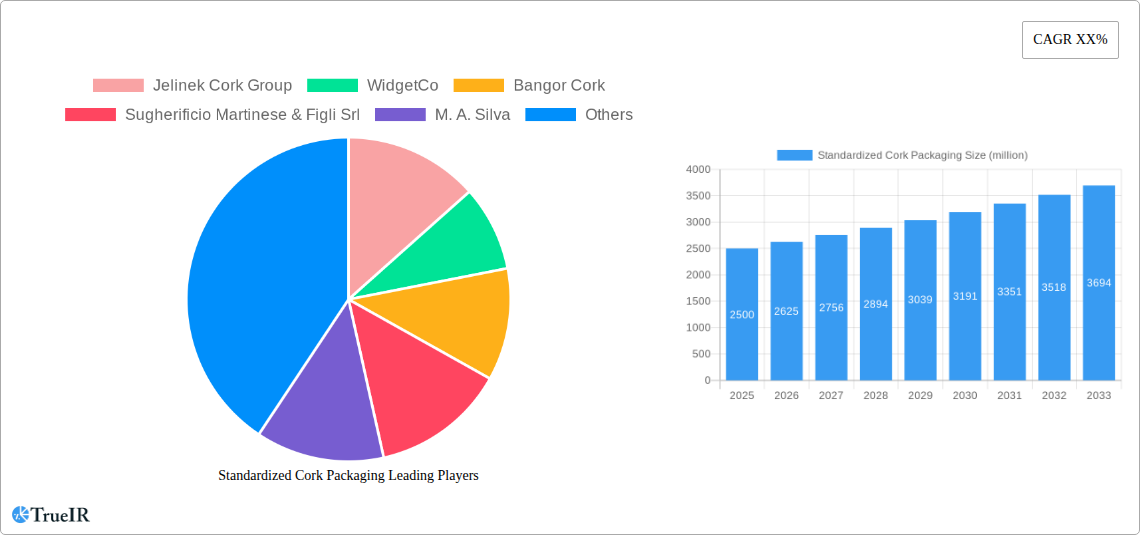

Standardized Cork Packaging Market Size (In Billion)

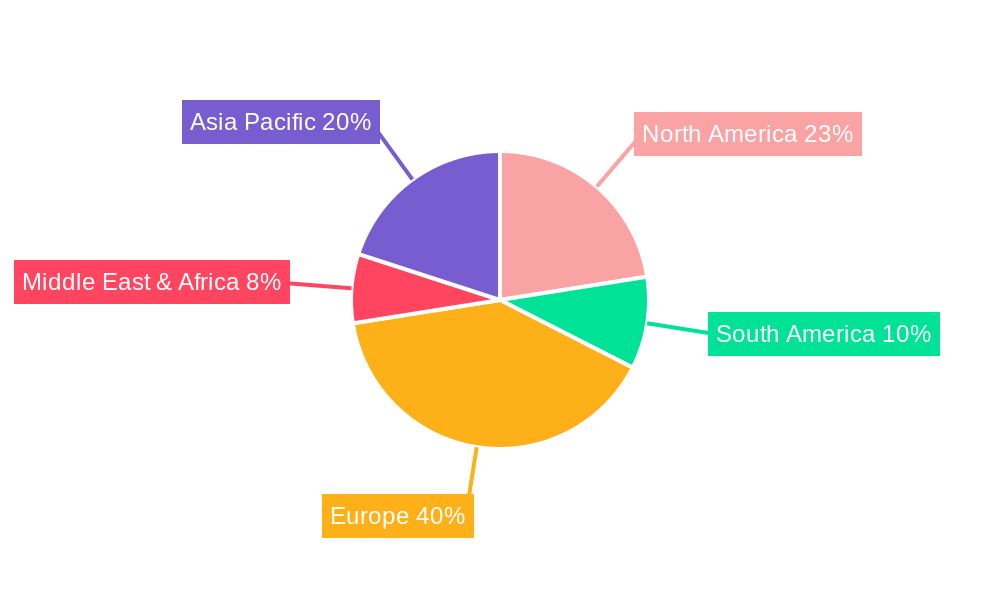

Despite its positive trajectory, the market faces certain restraints, including the susceptibility of natural cork to natural defects and the ongoing competition from synthetic alternatives like polymers and metal closures, which often boast lower costs and greater consistency. However, the development of polymerized and composite cork variants is effectively addressing some of these challenges, offering improved sealing properties, reduced taint potential, and greater durability. The market segmentation reveals that while the Food and Beverages sector, particularly wine, remains the dominant application, the Cosmetics and Personal Care segment is exhibiting significant growth potential. Geographically, Europe, with its established wine industry and strong emphasis on sustainability, is expected to continue leading the market, closely followed by North America, which is witnessing a surge in craft beverage production and a growing consumer base seeking premium and eco-conscious packaging. Asia Pacific, driven by rising disposable incomes and an increasing awareness of sustainable practices, presents a substantial long-term growth opportunity.

Standardized Cork Packaging Company Market Share

Standardized Cork Packaging Market Report: Comprehensive Analysis and Future Projections

This report offers an in-depth analysis of the global standardized cork packaging market, covering its structure, trends, opportunities, and competitive landscape from 2019 to 2033. Leveraging high-volume keywords such as "cork packaging solutions," "sustainable packaging materials," "natural cork stoppers," and "wine cork industry," this research aims to provide unparalleled insights for industry stakeholders. The study encompasses a historical period of 2019–2024, a base year of 2025, and a forecast period extending to 2033, with an estimated year also set at 2025.

Standardized Cork Packaging Market Structure & Competitive Landscape

The global standardized cork packaging market is characterized by a moderate to high level of concentration, with a few dominant players holding significant market share, estimated at approximately 70% of the total market value. Key innovation drivers include the increasing demand for sustainable and eco-friendly packaging solutions, advancements in cork processing technologies, and the rising popularity of premium beverages and artisanal food products. Regulatory impacts, while generally favorable towards natural and sustainable materials, can vary by region concerning food contact and environmental standards. Product substitutes, primarily synthetic stoppers and screw caps, present ongoing competition, though natural cork retains a strong preference in premium segments due to perceived quality and tradition. End-user segmentation reveals a substantial reliance on the Food and Beverages sector, followed by Cosmetics and Personal Care, and a smaller but growing "Others" category encompassing pharmaceuticals and specialty goods. Merger and acquisition (M&A) trends indicate strategic consolidation, with an estimated volume of over $500 million in M&A activities recorded over the historical period, aimed at expanding product portfolios and market reach.

Standardized Cork Packaging Market Trends & Opportunities

The standardized cork packaging market is experiencing robust growth, with a projected Compound Annual Growth Rate (CAGR) of approximately 5.2% from 2025 to 2033. This expansion is fueled by a confluence of evolving consumer preferences and significant technological advancements. Consumers are increasingly prioritizing sustainable and natural packaging materials, driven by growing environmental consciousness and a desire for authentic brand experiences. Cork, with its renewable, biodegradable, and carbon-neutral properties, perfectly aligns with these demands, positioning it favorably against synthetic alternatives. The market penetration of standardized cork packaging, currently estimated at around 45% in its core applications, is expected to rise as manufacturers and brands increasingly adopt these eco-friendly solutions.

Technological shifts are playing a pivotal role in enhancing the performance and versatility of cork packaging. Innovations in cork processing, such as advanced washing, treatment, and agglomeration techniques, have led to improved consistency, reduced taint potential, and enhanced sealing capabilities. These advancements are crucial for meeting the stringent quality requirements of the Food and Beverages sector, particularly for wine and spirits, where cork stoppers are traditionally favored for their ability to allow controlled micro-oxygenation, contributing to aging and flavor development. Furthermore, developments in micro-granulated cork and polymerized cork technologies are opening new avenues for applications beyond traditional stoppers, catering to the needs of the Cosmetics and Personal Care industries with aesthetically pleasing and functional packaging.

Competitive dynamics within the market are intensifying, with established players investing heavily in research and development to optimize production processes and introduce novel cork-based packaging formats. The focus is shifting towards creating customized solutions that offer both aesthetic appeal and superior functionality, catering to niche market demands. Opportunities abound for companies that can leverage the inherent sustainability of cork to build strong brand narratives and connect with environmentally conscious consumers. The increasing adoption of e-commerce also presents an opportunity for optimized cork packaging solutions that ensure product integrity during transit. The "Others" segment, though smaller, is exhibiting significant growth potential, particularly in areas like premium food products and high-end cosmetic formulations that emphasize natural ingredients and sophisticated packaging.

Dominant Markets & Segments in Standardized Cork Packaging

The Food and Beverages segment stands as the undisputed leader in the standardized cork packaging market, commanding an estimated market share of over 75% in 2025. This dominance is intrinsically linked to the traditional and ongoing preference for natural cork closures in the wine industry, where it is valued for its ability to facilitate controlled aging through micro-oxygenation, a critical factor in developing complex flavor profiles. Beyond wine, cork's use extends to spirits, olive oils, gourmet vinegars, and specialty food items, where its natural aesthetics and perceived premium quality enhance brand value. The strong infrastructure supporting cork harvesting and processing in key wine-producing regions globally underpins this segment's enduring strength. Furthermore, favorable policies promoting sustainable and natural packaging materials in major food-exporting nations provide a consistent growth impetus.

Within the types of standardized cork packaging, Natural Cork continues to be the most prevalent, holding an estimated 60% market share in 2025. This is due to its established reputation, perceived quality, and specific performance characteristics, particularly in high-value applications. Polymerized Cork, accounting for approximately 25% of the market, is gaining traction due to its enhanced consistency, improved barrier properties, and suitability for longer shelf-life products. Composite Cork, with an estimated 15% share, offers a cost-effective solution for various applications where the premium characteristics of natural cork are not paramount.

The Cosmetics and Personal Care segment represents the second-largest application, with an estimated market share of 20% in 2025. This segment's growth is driven by the increasing consumer demand for natural, sustainable, and aesthetically appealing packaging in beauty and wellness products. Cork stoppers and components offer a unique tactile experience and a connection to nature, aligning with brand positioning that emphasizes organic, cruelty-free, and eco-friendly formulations. The versatility of cork allows for its incorporation into unique bottle designs and closures, adding a touch of artisanal luxury.

The "Others" segment, encompassing applications like pharmaceuticals, specialty chemicals, and educational materials, is currently the smallest but exhibits the highest growth potential, with an estimated CAGR of 7.5% from 2025 to 2033. This growth is fueled by the expanding use of cork in niche markets seeking sustainable, biocompatible, and insulating properties. For instance, cork's natural antimicrobial properties are being explored for certain pharmaceutical packaging, while its lightweight and insulating characteristics are finding applications in specialized industrial packaging.

Standardized Cork Packaging Product Analysis

Standardized cork packaging is continuously evolving with innovative product developments designed to enhance functionality, sustainability, and aesthetic appeal. Natural cork stoppers remain the benchmark for premium wine and spirits, offering a unique porous structure that allows for controlled micro-oxygenation, crucial for aging. Advancements in cleaning and treatment processes for natural cork have significantly reduced the incidence of TCA (trichloroanisole) taint. Polymerized cork, created by binding cork granules with food-grade polymers, offers improved consistency and reduced permeability, making it ideal for a broader range of beverages and food products, including those requiring extended shelf life. Composite cork, a blend of natural cork and synthetic materials, provides a cost-effective yet functional solution for various packaging needs. Emerging innovations include cork-based closures with integrated dispensing mechanisms and decorative elements, catering to the premium segments of the cosmetics and personal care markets. These advancements collectively bolster the competitive advantage of cork packaging by meeting diverse application requirements and sustainability mandates.

Key Drivers, Barriers & Challenges in Standardized Cork Packaging

The standardized cork packaging market is propelled by several key drivers, most notably the escalating global demand for sustainable and eco-friendly packaging solutions. Consumer preferences are increasingly leaning towards renewable and biodegradable materials, with cork's inherent carbon-neutral status and recyclability being significant advantages. Technological advancements in cork processing, such as improved cleaning, granulation, and bonding techniques, are enhancing the performance and expanding the applicability of cork-based packaging. Furthermore, the enduring appeal of cork in premium segments, particularly for wine and spirits, due to its perceived quality and contribution to aging, continues to drive market growth. Regulatory support for sustainable materials in various regions also acts as a positive catalyst.

However, the market faces significant challenges and restraints. Fluctuations in the supply of raw cork, influenced by climate change and agricultural factors, can lead to price volatility. The perception of natural cork taint, although largely mitigated by modern processing, remains a concern for some consumers and industry players. Competition from synthetic closures, such as screw caps and plastic stoppers, which often offer lower price points and perceived convenience, poses a constant threat. Stringent quality control measures and adherence to international food safety standards require continuous investment and can present regulatory hurdles for smaller manufacturers. Supply chain disruptions, as experienced in recent years, can also impact the availability and cost of cork products, affecting market accessibility.

Growth Drivers in the Standardized Cork Packaging Market

The growth of the standardized cork packaging market is primarily driven by the escalating global consciousness towards environmental sustainability. Consumers and businesses alike are actively seeking packaging materials that are renewable, biodegradable, and have a low carbon footprint, a niche where cork excels due to its natural origin and carbon-sequestering properties. Technological advancements in cork processing and manufacturing are continuously improving the quality, consistency, and functionality of cork closures and packaging components, making them competitive across a wider range of applications. Economic factors, such as the growing disposable income in emerging economies, are fueling demand for premium food and beverage products, where cork packaging is often associated with higher quality and heritage. Moreover, supportive governmental policies and initiatives promoting the use of eco-friendly packaging materials worldwide are creating a more favorable market environment for cork-based solutions.

Challenges Impacting Standardized Cork Packaging Growth

Despite its inherent advantages, the standardized cork packaging market encounters several significant barriers and restraints. The inherent variability in the natural cork supply, susceptible to climatic conditions and agricultural yields, can lead to price instability and supply chain uncertainties. While advancements have largely addressed it, the historical perception of 'cork taint' (TCA contamination) continues to be a lingering concern for certain premium segments, necessitating rigorous quality control protocols. Intense competition from alternative closure materials, such as screw caps and synthetic stoppers, which often offer lower initial costs and perceived ease of use, exerts considerable pricing pressure. Furthermore, the complex regulatory landscape governing food-contact materials and sustainability claims across different international markets can present compliance challenges and increase operational costs for manufacturers.

Key Players Shaping the Standardized Cork Packaging Market

- Jelinek Cork Group

- WidgetCo

- Bangor Cork

- Sugherificio Martinese & Figli Srl

- M. A. Silva

- Diam Bouchage SAS

- Amorim Cork America

- J. C. RIBEIRO

- Korkindustrie GmbH & Co. KG

- Advance Cork International

- PORTOCORK AMERICA

- Lafitte Cork Group

- Cutting Edge Converted Products

- Berlin Packaging

- Pace Products LLC

- HELIX

- Fudy Solutions Inc

- HZ cork

- Teals Prairie and Co.

- GAP Packaging

- Hauser Packaging

Significant Standardized Cork Packaging Industry Milestones

- 2019: Increased adoption of sustainable packaging initiatives by major beverage companies, leading to a surge in demand for natural cork.

- 2020: Development of advanced cleaning and treatment techniques for natural cork, significantly reducing TCA taint issues.

- 2021: Expansion of polymerized cork applications beyond traditional stoppers into specialized industrial packaging.

- 2022: Strategic mergers and acquisitions among key players to consolidate market share and expand product portfolios.

- 2023: Growing consumer preference for artisanal and natural products driving innovation in composite cork packaging for cosmetics.

- 2024: Increased investment in R&D for biodegradable cork-based alternatives to single-use plastics.

Future Outlook for Standardized Cork Packaging Market

The future outlook for the standardized cork packaging market is exceptionally positive, driven by the escalating global imperative for sustainable and eco-friendly solutions. The inherent renewability, biodegradability, and carbon-neutral attributes of cork align perfectly with evolving consumer demands and stringent environmental regulations. Strategic opportunities lie in further technological innovation to enhance cork's performance characteristics, expand its application range into new sectors such as advanced pharmaceuticals and biodegradable composites, and develop customized packaging solutions that offer both premium aesthetics and superior functionality. Continued investment in sustainable sourcing and advanced processing will be critical to maintaining cost-competitiveness and mitigating supply chain vulnerabilities, ensuring cork's sustained prominence as a leading material in the global packaging landscape.

Standardized Cork Packaging Segmentation

-

1. Application

- 1.1. Food and Beverages

- 1.2. Cosmetics and Personal care

- 1.3. Others

-

2. Types

- 2.1. Natural Cork

- 2.2. Polymerized Cork

- 2.3. Composite Cork

Standardized Cork Packaging Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Standardized Cork Packaging Regional Market Share

Geographic Coverage of Standardized Cork Packaging

Standardized Cork Packaging REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Food and Beverages

- 5.1.2. Cosmetics and Personal care

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Natural Cork

- 5.2.2. Polymerized Cork

- 5.2.3. Composite Cork

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Standardized Cork Packaging Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Food and Beverages

- 6.1.2. Cosmetics and Personal care

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Natural Cork

- 6.2.2. Polymerized Cork

- 6.2.3. Composite Cork

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Standardized Cork Packaging Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Food and Beverages

- 7.1.2. Cosmetics and Personal care

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Natural Cork

- 7.2.2. Polymerized Cork

- 7.2.3. Composite Cork

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Standardized Cork Packaging Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Food and Beverages

- 8.1.2. Cosmetics and Personal care

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Natural Cork

- 8.2.2. Polymerized Cork

- 8.2.3. Composite Cork

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Standardized Cork Packaging Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Food and Beverages

- 9.1.2. Cosmetics and Personal care

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Natural Cork

- 9.2.2. Polymerized Cork

- 9.2.3. Composite Cork

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Standardized Cork Packaging Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Food and Beverages

- 10.1.2. Cosmetics and Personal care

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Natural Cork

- 10.2.2. Polymerized Cork

- 10.2.3. Composite Cork

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Standardized Cork Packaging Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Food and Beverages

- 11.1.2. Cosmetics and Personal care

- 11.1.3. Others

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Natural Cork

- 11.2.2. Polymerized Cork

- 11.2.3. Composite Cork

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Jelinek Cork Group

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 WidgetCo

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Bangor Cork

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Sugherificio Martinese & Figli Srl

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 M. A. Silva

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Diam Bouchage SAS

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Amorim Cork America

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 J. C. RIBEIRO

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Korkindustrie GmbH & Co. KG

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Advance Cork International

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 PORTOCORK AMERICA

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Lafitte Cork Group

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Cutting Edge Converted Products

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Berlin Packaging

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Pace Products LLC

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 HELIX

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Fudy Solutions Inc

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 HZ cork

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Teals Prairie and Co.

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 GAP Packaging

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 Hauser Packaging

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.1 Jelinek Cork Group

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Standardized Cork Packaging Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Standardized Cork Packaging Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Standardized Cork Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Standardized Cork Packaging Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Standardized Cork Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Standardized Cork Packaging Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Standardized Cork Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Standardized Cork Packaging Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Standardized Cork Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Standardized Cork Packaging Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Standardized Cork Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Standardized Cork Packaging Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Standardized Cork Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Standardized Cork Packaging Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Standardized Cork Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Standardized Cork Packaging Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Standardized Cork Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Standardized Cork Packaging Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Standardized Cork Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Standardized Cork Packaging Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Standardized Cork Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Standardized Cork Packaging Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Standardized Cork Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Standardized Cork Packaging Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Standardized Cork Packaging Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Standardized Cork Packaging Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Standardized Cork Packaging Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Standardized Cork Packaging Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Standardized Cork Packaging Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Standardized Cork Packaging Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Standardized Cork Packaging Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Standardized Cork Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Standardized Cork Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Standardized Cork Packaging Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Standardized Cork Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Standardized Cork Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Standardized Cork Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Standardized Cork Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Standardized Cork Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Standardized Cork Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Standardized Cork Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Standardized Cork Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Standardized Cork Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Standardized Cork Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Standardized Cork Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Standardized Cork Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Standardized Cork Packaging Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Standardized Cork Packaging Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Standardized Cork Packaging Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Standardized Cork Packaging Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Standardized Cork Packaging?

The projected CAGR is approximately 5.7%.

2. Which companies are prominent players in the Standardized Cork Packaging?

Key companies in the market include Jelinek Cork Group, WidgetCo, Bangor Cork, Sugherificio Martinese & Figli Srl, M. A. Silva, Diam Bouchage SAS, Amorim Cork America, J. C. RIBEIRO, Korkindustrie GmbH & Co. KG, Advance Cork International, PORTOCORK AMERICA, Lafitte Cork Group, Cutting Edge Converted Products, Berlin Packaging, Pace Products LLC, HELIX, Fudy Solutions Inc, HZ cork, Teals Prairie and Co., GAP Packaging, Hauser Packaging.

3. What are the main segments of the Standardized Cork Packaging?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.8 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Standardized Cork Packaging," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Standardized Cork Packaging report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Standardized Cork Packaging?

To stay informed about further developments, trends, and reports in the Standardized Cork Packaging, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence