Key Insights

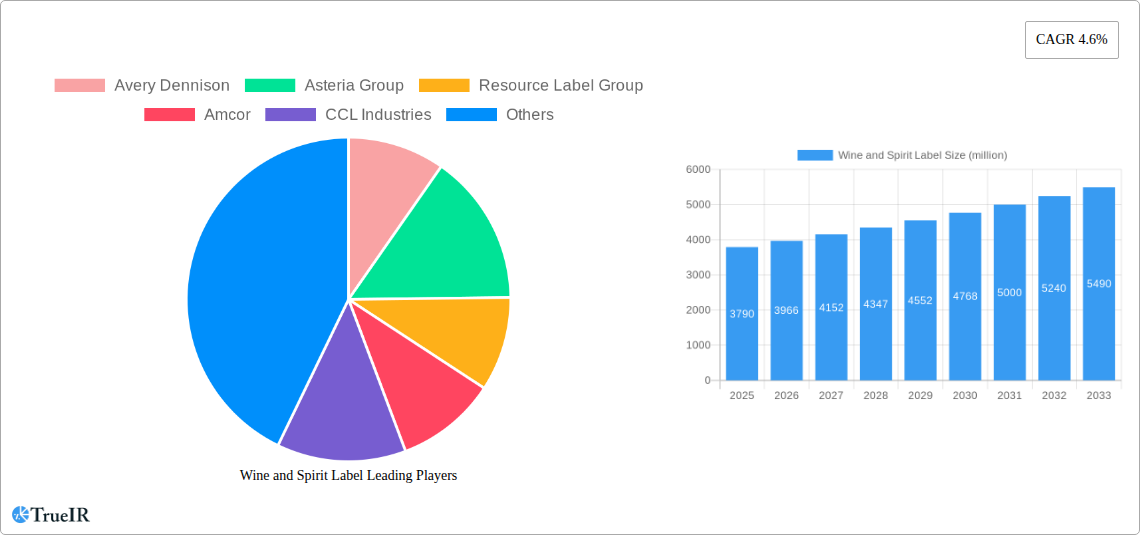

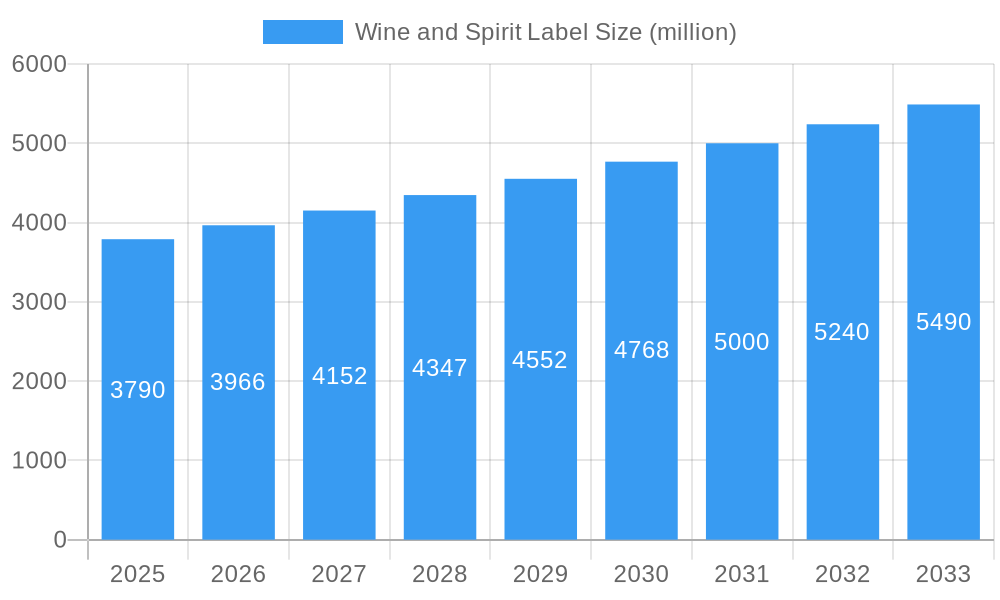

The global Wine and Spirit Label market is poised for robust growth, projected to reach $3790 million in value by 2025 and expand at a Compound Annual Growth Rate (CAGR) of 4.6% through 2033. This expansion is fueled by several key drivers, including the increasing global consumption of wine and spirits, a growing trend towards premiumization and sophisticated packaging within these sectors, and the rising demand for visually appealing and informative labels that convey brand identity and origin. The market is segmented by application into Wine and Spirit labels, with further categorization by types including Paper Labels, Foil Labels, and Others, indicating a diverse range of material preferences and aesthetic demands. The Asia Pacific region is expected to witness the most significant growth, driven by a burgeoning middle class, increased disposable incomes, and a growing appreciation for Western alcoholic beverages. North America and Europe, while mature markets, will continue to represent substantial shares due to established consumption patterns and a focus on innovation in label design and functionality.

Wine and Spirit Label Market Size (In Billion)

The growth trajectory of the Wine and Spirit Label market is also influenced by evolving consumer preferences, with a notable shift towards sustainable and eco-friendly packaging solutions. This trend is pushing manufacturers to innovate with recycled materials, biodegradable options, and advanced printing techniques that minimize environmental impact. However, the market also faces certain restraints, such as fluctuations in raw material costs, particularly for paper and foil, and the increasing stringency of labeling regulations in various regions, which can add to production complexities and costs. Despite these challenges, the competitive landscape is dynamic, featuring prominent players like Avery Dennison, Amcor, and CCL Industries, alongside several specialized label manufacturers. These companies are investing in research and development to offer advanced label solutions, including those with anti-counterfeiting features and enhanced shelf appeal, to capture a larger market share. The continued evolution of design aesthetics and functional requirements will shape the future of this essential market segment.

Wine and Spirit Label Company Market Share

Wine and Spirit Label Market Structure & Competitive Landscape

The global wine and spirit label market exhibits a moderately concentrated structure, with a few dominant players alongside a substantial number of smaller, specialized manufacturers. Key companies like Avery Dennison, Amcor, CCL Industries, and Multi-Color Corporation hold significant market share due to their extensive production capabilities, global reach, and robust R&D investments. The market's dynamism is fueled by continuous innovation in label materials, printing technologies (including advanced digital printing and embellishments), and smart labeling solutions that enhance brand differentiation and consumer engagement.

Regulatory impacts are primarily associated with food-grade materials, traceability requirements (especially for spirits), and increasingly, sustainability mandates that favor eco-friendly label options. Product substitutes, while limited in their ability to fully replicate the aesthetic and functional qualities of premium labels, can include direct printing on bottles or simpler packaging solutions for lower-tier products. End-user segmentation highlights the distinct needs of the wine industry, which often prioritizes premium aesthetics and historical branding, versus the spirit industry, where anti-counterfeiting features and regulatory compliance are paramount. Merger and acquisition (M&A) activity remains a significant trend, with larger entities acquiring smaller, innovative firms to expand their product portfolios, technological expertise, and geographic footprint. For instance, the period from 2019-2024 has seen an estimated $200 million in M&A deals within this sector, consolidating market power and driving strategic growth.

Key Competitive Factors:

- Technological Innovation: Advancements in printing, materials, and security features.

- Brand Differentiation: Ability to offer unique aesthetic and tactile experiences.

- Sustainability: Growing demand for recycled, recyclable, and biodegradable label solutions.

- Regulatory Compliance: Adherence to global and regional labeling standards.

- Supply Chain Efficiency: Reliable and cost-effective sourcing and delivery.

Wine and Spirit Label Market Trends & Opportunities

The wine and spirit label market is projected for robust growth, driven by an estimated XX% compound annual growth rate (CAGR) over the forecast period of 2025–2033. The market size is expected to expand from approximately $5,000 million in the base year of 2025 to over $7,000 million by the end of the forecast period. This expansion is underpinned by several interconnected trends.

Technological shifts are profoundly reshaping the industry. The increasing adoption of digital printing technologies allows for greater flexibility, shorter production runs, and enhanced customization, catering to the growing demand for personalized and limited-edition products. Innovations in specialty inks, holographic foils, embossing, debossing, and tactile finishes are enabling brands to create more sophisticated and memorable packaging that captures consumer attention on crowded retail shelves. Furthermore, the integration of smart labeling technologies, such as QR codes and NFC tags, is opening new avenues for consumer engagement, providing access to brand stories, provenance information, cocktail recipes, and even authentication services, thereby increasing brand loyalty and combating counterfeiting.

Consumer preferences are evolving significantly. There's a discernible shift towards premiumization, with consumers willing to pay more for products that offer a superior sensory experience, which heavily relies on label design and quality. Sustainability is no longer a niche concern but a mainstream expectation. This translates into a growing demand for labels made from recycled content, sustainably sourced paper, and biodegradable or compostable materials. Brands are increasingly seeking label solutions that align with their environmental, social, and governance (ESG) commitments, creating a substantial opportunity for label manufacturers who can offer credible and innovative eco-friendly options. The rising global consumption of wine and spirits, particularly in emerging economies, also directly fuels market expansion. As disposable incomes rise and Western lifestyle trends influence purchasing habits, the demand for bottled wine and spirits, and consequently their labels, continues to climb.

The competitive landscape is characterized by intense rivalry, with companies vying for market share through product innovation, strategic partnerships, and acquisitions. The pursuit of differentiation is leading to a greater emphasis on unique design elements and functional features. Opportunities abound for companies that can effectively combine aesthetic appeal with advanced functionality, such as tamper-evident features and anti-counterfeiting technologies, particularly crucial in the high-value spirits segment. The increasing focus on e-commerce and direct-to-consumer (DTC) sales models also presents new challenges and opportunities for label design, emphasizing durability for shipping and eye-catching visuals for online product listings. The global wine and spirit label market is thus poised for significant evolution, driven by a confluence of technological advancements, changing consumer desires, and the persistent pursuit of brand distinction.

Dominant Markets & Segments in Wine and Spirit Label

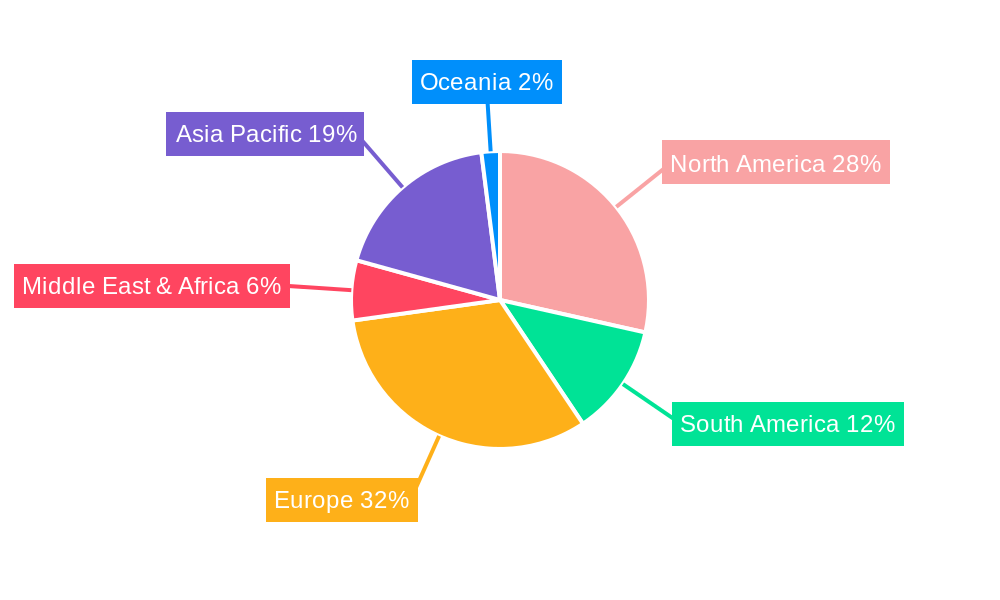

The global wine and spirit label market is characterized by distinct regional strengths and segment dominance, each driven by a unique set of factors. Europe, with its centuries-old winemaking traditions and established spirit distilleries, currently holds the dominant position in terms of market value and volume, contributing an estimated 40% to the global market share. Countries like France, Italy, Spain, and the UK are major consumers and producers of wine and spirits, leading to a high demand for sophisticated and premium labeling solutions. The strong emphasis on heritage, appellation designations, and brand storytelling in these regions fuels a consistent demand for high-quality paper labels with intricate printing techniques and embellishments.

Within the broader wine and spirit label market, the Wine Application segment is the larger contributor, accounting for approximately 60% of the market. This dominance is driven by the sheer volume of wine production and consumption globally, coupled with the wine industry's long-standing tradition of investing in visually appealing and informative labels that convey prestige and origin.

In terms of label types, the Paper Label segment leads the market, representing around 70% of the total demand. Paper labels remain the preferred choice due to their versatility, cost-effectiveness, and excellent printability, allowing for a wide range of finishes and designs. They are fundamental for both everyday wines and higher-end spirits, offering a canvas for intricate artwork, branding, and regulatory information.

However, significant growth is observed in other segments. The Spirit Application segment, while smaller at approximately 30% of the market, is experiencing higher growth rates, driven by the premiumization of spirits, the rise of craft distilleries, and the critical need for anti-counterfeiting features. High-value spirits often utilize more advanced labeling technologies, including holographic elements, security inks, and tamper-evident seals, contributing to a higher average selling price per label.

The Foil Label segment, though smaller in overall market share (estimated at 15%), is a critical growth driver, particularly for premium wine and spirit brands. Foil stamping adds a touch of luxury and sophistication, enhancing visual appeal and brand perception. The "Others" segment, which includes synthetic labels, textured materials, and smart labels with integrated technology, is the fastest-growing sub-segment, projected to grow at a CAGR of XX% over the forecast period. This expansion is fueled by technological innovation and the increasing demand for unique branding and functional features like RFID tags for inventory management and authentication.

Key growth drivers in dominant regions like Europe include established infrastructure for wine and spirit production, strong consumer demand, and supportive policies that promote regional specialties and quality certifications. In emerging markets, economic growth, increasing disposable incomes, and the globalization of beverage consumption patterns are driving demand for both wine and spirits, and consequently their labels. Government regulations regarding labeling transparency and product information also play a crucial role in shaping market demand for specific label types.

Wine and Spirit Label Product Analysis

The wine and spirit label market is witnessing a surge in product innovations focused on enhancing brand appeal, ensuring authenticity, and promoting sustainability. Advancements in printing technologies, such as high-definition digital printing and specialized embellishment techniques like foiling, embossing, and tactile varnishes, allow for visually striking and premium-feeling labels. Material science is also crucial, with the development of specialized papers, durable synthetics, and eco-friendly options like recycled content or biodegradable films. Security features, including hidden inks, holograms, and tamper-evident seals, are gaining prominence, particularly in the spirit segment, to combat counterfeiting. Competitive advantages are derived from the ability to offer integrated solutions that combine aesthetic excellence with functional security and sustainability, catering to brand owners' evolving needs for differentiation and consumer trust.

Key Drivers, Barriers & Challenges in Wine and Spirit Label

Key Drivers:

- Premiumization Trend: Growing consumer demand for high-quality, visually appealing products drives investment in sophisticated labels.

- E-commerce Growth: Increased online sales necessitate durable, eye-catching labels that stand out digitally and withstand shipping.

- Sustainability Initiatives: Consumer and regulatory pressure favors eco-friendly label materials and production processes.

- Technological Advancements: Innovations in printing, materials, and smart labeling offer new opportunities for differentiation and functionality.

- Emerging Market Expansion: Rising disposable incomes and Western consumption patterns in developing economies boost demand.

Key Barriers & Challenges:

- Supply Chain Volatility: Fluctuations in raw material costs (e.g., paper, inks, adhesives) and availability can impact pricing and lead times.

- Regulatory Complexities: Varying international labeling regulations and evolving requirements for alcohol content, ingredients, and origin can be challenging to navigate.

- Intense Competition: The market is highly competitive, leading to price pressures and the need for continuous innovation to maintain market share.

- Economic Downturns: Reduced consumer spending during economic recessions can negatively impact demand for premium beverages and, consequently, their labels.

- Counterfeiting Threats: Sophisticated counterfeiting operations require ongoing investment in advanced security labeling solutions.

Growth Drivers in the Wine and Spirit Label Market

Several key drivers are propelling the wine and spirit label market forward. The persistent global trend of premiumization in both wine and spirits directly fuels the demand for sophisticated and aesthetically superior labels that enhance brand perception and consumer allure. The expansion of e-commerce and direct-to-consumer (DTC) sales channels presents a significant opportunity, requiring labels that are not only visually appealing online but also durable enough to withstand the rigors of shipping. Sustainability is a paramount driver, with growing consumer and regulatory pressure pushing for the adoption of eco-friendly materials such as recycled paper, compostable films, and water-based inks. Furthermore, technological advancements in digital printing, specialty inks, and intelligent labeling solutions (e.g., QR codes, NFC tags) are enabling greater customization, brand storytelling, and enhanced consumer engagement, creating new avenues for value creation and competitive advantage. The increasing number of craft distilleries and boutique wineries, each seeking unique brand identities, also contributes to the demand for specialized and innovative labeling.

Challenges Impacting Wine and Spirit Label Growth

Despite robust growth, the wine and spirit label market faces several significant challenges. Supply chain disruptions and volatility in raw material costs, including paper pulp, specialty films, and inks, can lead to increased production expenses and unpredictable lead times, impacting profitability and customer satisfaction. Navigating complex and evolving international regulatory landscapes regarding alcohol content, ingredient disclosure, origin labeling, and anti-counterfeiting measures presents a constant hurdle for global manufacturers and brands. The market is characterized by intense competition, with numerous players vying for market share, leading to significant pricing pressures and the imperative for continuous innovation to differentiate products and services. Economic downturns and geopolitical uncertainties can lead to reduced consumer discretionary spending, directly affecting demand for premium beverages and, by extension, their associated labeling costs. Lastly, the ongoing threat of sophisticated product counterfeiting, particularly in the high-value spirits segment, necessitates continuous investment in advanced security features, adding to production costs and complexity.

Key Players Shaping the Wine and Spirit Label Market

- Avery Dennison

- Asteria Group

- Resource Label Group

- Amcor

- CCL Industries

- LINTEC

- Berry Global

- Cenveo

- Multi-Color Corporation

- Klckner Pentaplast

- Reflex Group

- Ultra

- UPM Global

- Inovar Packaging Group

- Smith and McLaurin

- QLM Group

- Labelys

- Prakash Labels

- Autajon Group

- G3 Enterprises

- ID Images

- Weber Packaging Solutions

Significant Wine and Spirit Label Industry Milestones

- 2019: Increased adoption of digital printing technologies for shorter runs and customization.

- 2020: Growing emphasis on sustainable and eco-friendly label materials due to rising environmental awareness.

- 2021: Significant M&A activity as larger players acquire innovative smaller companies to expand capabilities (estimated $XX million in deals).

- 2022: Introduction of advanced anti-counterfeiting features and smart labeling solutions like NFC and QR codes becoming more mainstream.

- 2023: Heightened focus on tactile finishes and embellishments to enhance premium brand perception.

- Early 2024: Increased investment in supply chain resilience and diversification of raw material sourcing.

Future Outlook for Wine and Spirit Label Market

The future outlook for the wine and spirit label market is exceptionally promising, driven by sustained growth catalysts and strategic opportunities. The continued premiumization of both wine and spirits, coupled with the rapid expansion of e-commerce and DTC sales, will drive demand for visually striking and functional labels that can perform across digital and physical platforms. A paramount growth catalyst will be the escalating focus on sustainability, pushing for innovations in recycled, biodegradable, and compostable label materials, creating significant market potential for eco-conscious manufacturers. Furthermore, technological advancements in digital printing, augmented reality (AR) integrated labels, and increasingly sophisticated security features will unlock new avenues for brand storytelling, consumer engagement, and product authentication. The market is poised for continued innovation, with a strong emphasis on creating labels that offer a compelling blend of aesthetic appeal, functional performance, and environmental responsibility, ensuring robust growth through the forecast period.

Wine and Spirit Label Segmentation

-

1. Application

- 1.1. Wine

- 1.2. Spirit

-

2. Types

- 2.1. Paper Label

- 2.2. Foil Label

- 2.3. Others

Wine and Spirit Label Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Wine and Spirit Label Regional Market Share

Geographic Coverage of Wine and Spirit Label

Wine and Spirit Label REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Wine

- 5.1.2. Spirit

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Paper Label

- 5.2.2. Foil Label

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Wine and Spirit Label Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Wine

- 6.1.2. Spirit

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Paper Label

- 6.2.2. Foil Label

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Wine and Spirit Label Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Wine

- 7.1.2. Spirit

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Paper Label

- 7.2.2. Foil Label

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Wine and Spirit Label Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Wine

- 8.1.2. Spirit

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Paper Label

- 8.2.2. Foil Label

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Wine and Spirit Label Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Wine

- 9.1.2. Spirit

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Paper Label

- 9.2.2. Foil Label

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Wine and Spirit Label Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Wine

- 10.1.2. Spirit

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Paper Label

- 10.2.2. Foil Label

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Wine and Spirit Label Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Wine

- 11.1.2. Spirit

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Paper Label

- 11.2.2. Foil Label

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Avery Dennison

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Asteria Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Resource Label Group

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Amcor

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 CCL Industries

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 LINTEC

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Berry Global

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Cenveo

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 Multi-Color Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Klckner Pentaplast

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Reflex Group

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Ultra

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 UPM Global

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Inovar Packaging Group

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Smith and McLaurin

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 QLM Group

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 Labelys

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 Prakash Labels

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 Autajon Group

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 G3 Enterprises

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 ID Images

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Weber Packaging Solutions

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.1 Avery Dennison

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Wine and Spirit Label Revenue Breakdown (million, %) by Region 2025 & 2033

- Figure 2: Global Wine and Spirit Label Volume Breakdown (K, %) by Region 2025 & 2033

- Figure 3: North America Wine and Spirit Label Revenue (million), by Application 2025 & 2033

- Figure 4: North America Wine and Spirit Label Volume (K), by Application 2025 & 2033

- Figure 5: North America Wine and Spirit Label Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Wine and Spirit Label Volume Share (%), by Application 2025 & 2033

- Figure 7: North America Wine and Spirit Label Revenue (million), by Types 2025 & 2033

- Figure 8: North America Wine and Spirit Label Volume (K), by Types 2025 & 2033

- Figure 9: North America Wine and Spirit Label Revenue Share (%), by Types 2025 & 2033

- Figure 10: North America Wine and Spirit Label Volume Share (%), by Types 2025 & 2033

- Figure 11: North America Wine and Spirit Label Revenue (million), by Country 2025 & 2033

- Figure 12: North America Wine and Spirit Label Volume (K), by Country 2025 & 2033

- Figure 13: North America Wine and Spirit Label Revenue Share (%), by Country 2025 & 2033

- Figure 14: North America Wine and Spirit Label Volume Share (%), by Country 2025 & 2033

- Figure 15: South America Wine and Spirit Label Revenue (million), by Application 2025 & 2033

- Figure 16: South America Wine and Spirit Label Volume (K), by Application 2025 & 2033

- Figure 17: South America Wine and Spirit Label Revenue Share (%), by Application 2025 & 2033

- Figure 18: South America Wine and Spirit Label Volume Share (%), by Application 2025 & 2033

- Figure 19: South America Wine and Spirit Label Revenue (million), by Types 2025 & 2033

- Figure 20: South America Wine and Spirit Label Volume (K), by Types 2025 & 2033

- Figure 21: South America Wine and Spirit Label Revenue Share (%), by Types 2025 & 2033

- Figure 22: South America Wine and Spirit Label Volume Share (%), by Types 2025 & 2033

- Figure 23: South America Wine and Spirit Label Revenue (million), by Country 2025 & 2033

- Figure 24: South America Wine and Spirit Label Volume (K), by Country 2025 & 2033

- Figure 25: South America Wine and Spirit Label Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Wine and Spirit Label Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Wine and Spirit Label Revenue (million), by Application 2025 & 2033

- Figure 28: Europe Wine and Spirit Label Volume (K), by Application 2025 & 2033

- Figure 29: Europe Wine and Spirit Label Revenue Share (%), by Application 2025 & 2033

- Figure 30: Europe Wine and Spirit Label Volume Share (%), by Application 2025 & 2033

- Figure 31: Europe Wine and Spirit Label Revenue (million), by Types 2025 & 2033

- Figure 32: Europe Wine and Spirit Label Volume (K), by Types 2025 & 2033

- Figure 33: Europe Wine and Spirit Label Revenue Share (%), by Types 2025 & 2033

- Figure 34: Europe Wine and Spirit Label Volume Share (%), by Types 2025 & 2033

- Figure 35: Europe Wine and Spirit Label Revenue (million), by Country 2025 & 2033

- Figure 36: Europe Wine and Spirit Label Volume (K), by Country 2025 & 2033

- Figure 37: Europe Wine and Spirit Label Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Wine and Spirit Label Volume Share (%), by Country 2025 & 2033

- Figure 39: Middle East & Africa Wine and Spirit Label Revenue (million), by Application 2025 & 2033

- Figure 40: Middle East & Africa Wine and Spirit Label Volume (K), by Application 2025 & 2033

- Figure 41: Middle East & Africa Wine and Spirit Label Revenue Share (%), by Application 2025 & 2033

- Figure 42: Middle East & Africa Wine and Spirit Label Volume Share (%), by Application 2025 & 2033

- Figure 43: Middle East & Africa Wine and Spirit Label Revenue (million), by Types 2025 & 2033

- Figure 44: Middle East & Africa Wine and Spirit Label Volume (K), by Types 2025 & 2033

- Figure 45: Middle East & Africa Wine and Spirit Label Revenue Share (%), by Types 2025 & 2033

- Figure 46: Middle East & Africa Wine and Spirit Label Volume Share (%), by Types 2025 & 2033

- Figure 47: Middle East & Africa Wine and Spirit Label Revenue (million), by Country 2025 & 2033

- Figure 48: Middle East & Africa Wine and Spirit Label Volume (K), by Country 2025 & 2033

- Figure 49: Middle East & Africa Wine and Spirit Label Revenue Share (%), by Country 2025 & 2033

- Figure 50: Middle East & Africa Wine and Spirit Label Volume Share (%), by Country 2025 & 2033

- Figure 51: Asia Pacific Wine and Spirit Label Revenue (million), by Application 2025 & 2033

- Figure 52: Asia Pacific Wine and Spirit Label Volume (K), by Application 2025 & 2033

- Figure 53: Asia Pacific Wine and Spirit Label Revenue Share (%), by Application 2025 & 2033

- Figure 54: Asia Pacific Wine and Spirit Label Volume Share (%), by Application 2025 & 2033

- Figure 55: Asia Pacific Wine and Spirit Label Revenue (million), by Types 2025 & 2033

- Figure 56: Asia Pacific Wine and Spirit Label Volume (K), by Types 2025 & 2033

- Figure 57: Asia Pacific Wine and Spirit Label Revenue Share (%), by Types 2025 & 2033

- Figure 58: Asia Pacific Wine and Spirit Label Volume Share (%), by Types 2025 & 2033

- Figure 59: Asia Pacific Wine and Spirit Label Revenue (million), by Country 2025 & 2033

- Figure 60: Asia Pacific Wine and Spirit Label Volume (K), by Country 2025 & 2033

- Figure 61: Asia Pacific Wine and Spirit Label Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Pacific Wine and Spirit Label Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Wine and Spirit Label Revenue million Forecast, by Application 2020 & 2033

- Table 2: Global Wine and Spirit Label Volume K Forecast, by Application 2020 & 2033

- Table 3: Global Wine and Spirit Label Revenue million Forecast, by Types 2020 & 2033

- Table 4: Global Wine and Spirit Label Volume K Forecast, by Types 2020 & 2033

- Table 5: Global Wine and Spirit Label Revenue million Forecast, by Region 2020 & 2033

- Table 6: Global Wine and Spirit Label Volume K Forecast, by Region 2020 & 2033

- Table 7: Global Wine and Spirit Label Revenue million Forecast, by Application 2020 & 2033

- Table 8: Global Wine and Spirit Label Volume K Forecast, by Application 2020 & 2033

- Table 9: Global Wine and Spirit Label Revenue million Forecast, by Types 2020 & 2033

- Table 10: Global Wine and Spirit Label Volume K Forecast, by Types 2020 & 2033

- Table 11: Global Wine and Spirit Label Revenue million Forecast, by Country 2020 & 2033

- Table 12: Global Wine and Spirit Label Volume K Forecast, by Country 2020 & 2033

- Table 13: United States Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 14: United States Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 15: Canada Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 16: Canada Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 17: Mexico Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 18: Mexico Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 19: Global Wine and Spirit Label Revenue million Forecast, by Application 2020 & 2033

- Table 20: Global Wine and Spirit Label Volume K Forecast, by Application 2020 & 2033

- Table 21: Global Wine and Spirit Label Revenue million Forecast, by Types 2020 & 2033

- Table 22: Global Wine and Spirit Label Volume K Forecast, by Types 2020 & 2033

- Table 23: Global Wine and Spirit Label Revenue million Forecast, by Country 2020 & 2033

- Table 24: Global Wine and Spirit Label Volume K Forecast, by Country 2020 & 2033

- Table 25: Brazil Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 26: Brazil Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 27: Argentina Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 28: Argentina Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 29: Rest of South America Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 30: Rest of South America Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 31: Global Wine and Spirit Label Revenue million Forecast, by Application 2020 & 2033

- Table 32: Global Wine and Spirit Label Volume K Forecast, by Application 2020 & 2033

- Table 33: Global Wine and Spirit Label Revenue million Forecast, by Types 2020 & 2033

- Table 34: Global Wine and Spirit Label Volume K Forecast, by Types 2020 & 2033

- Table 35: Global Wine and Spirit Label Revenue million Forecast, by Country 2020 & 2033

- Table 36: Global Wine and Spirit Label Volume K Forecast, by Country 2020 & 2033

- Table 37: United Kingdom Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 38: United Kingdom Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 39: Germany Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 40: Germany Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 41: France Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 42: France Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 43: Italy Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 44: Italy Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 45: Spain Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 46: Spain Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 47: Russia Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 48: Russia Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 49: Benelux Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 50: Benelux Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 51: Nordics Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 52: Nordics Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 53: Rest of Europe Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 54: Rest of Europe Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 55: Global Wine and Spirit Label Revenue million Forecast, by Application 2020 & 2033

- Table 56: Global Wine and Spirit Label Volume K Forecast, by Application 2020 & 2033

- Table 57: Global Wine and Spirit Label Revenue million Forecast, by Types 2020 & 2033

- Table 58: Global Wine and Spirit Label Volume K Forecast, by Types 2020 & 2033

- Table 59: Global Wine and Spirit Label Revenue million Forecast, by Country 2020 & 2033

- Table 60: Global Wine and Spirit Label Volume K Forecast, by Country 2020 & 2033

- Table 61: Turkey Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 62: Turkey Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 63: Israel Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 64: Israel Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 65: GCC Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 66: GCC Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 67: North Africa Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 68: North Africa Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 69: South Africa Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 70: South Africa Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 71: Rest of Middle East & Africa Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 72: Rest of Middle East & Africa Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 73: Global Wine and Spirit Label Revenue million Forecast, by Application 2020 & 2033

- Table 74: Global Wine and Spirit Label Volume K Forecast, by Application 2020 & 2033

- Table 75: Global Wine and Spirit Label Revenue million Forecast, by Types 2020 & 2033

- Table 76: Global Wine and Spirit Label Volume K Forecast, by Types 2020 & 2033

- Table 77: Global Wine and Spirit Label Revenue million Forecast, by Country 2020 & 2033

- Table 78: Global Wine and Spirit Label Volume K Forecast, by Country 2020 & 2033

- Table 79: China Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 80: China Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 81: India Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 82: India Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 83: Japan Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 84: Japan Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 85: South Korea Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 86: South Korea Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 87: ASEAN Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 88: ASEAN Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 89: Oceania Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 90: Oceania Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

- Table 91: Rest of Asia Pacific Wine and Spirit Label Revenue (million) Forecast, by Application 2020 & 2033

- Table 92: Rest of Asia Pacific Wine and Spirit Label Volume (K) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wine and Spirit Label?

The projected CAGR is approximately 4.6%.

2. Which companies are prominent players in the Wine and Spirit Label?

Key companies in the market include Avery Dennison, Asteria Group, Resource Label Group, Amcor, CCL Industries, LINTEC, Berry Global, Cenveo, Multi-Color Corporation, Klckner Pentaplast, Reflex Group, Ultra, UPM Global, Inovar Packaging Group, Smith and McLaurin, QLM Group, Labelys, Prakash Labels, Autajon Group, G3 Enterprises, ID Images, Weber Packaging Solutions.

3. What are the main segments of the Wine and Spirit Label?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 3790 million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3950.00, USD 5925.00, and USD 7900.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million and volume, measured in K.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wine and Spirit Label," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wine and Spirit Label report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wine and Spirit Label?

To stay informed about further developments, trends, and reports in the Wine and Spirit Label, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence