Key Insights

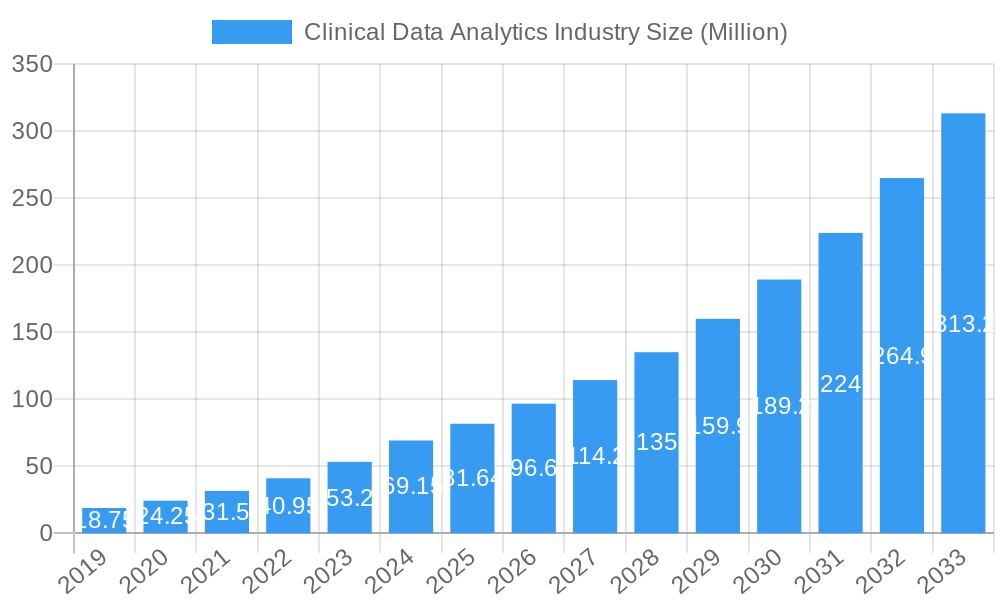

The global Clinical Data Analytics market is experiencing unprecedented growth, projected to reach a substantial market size of $81.64 million by 2025. This expansion is fueled by a remarkable Compound Annual Growth Rate (CAGR) of 27.53%, indicating a rapidly evolving landscape driven by the increasing adoption of advanced analytical tools across the healthcare spectrum. Key drivers for this surge include the imperative for enhanced quality improvement and clinical benchmarking, a growing demand for sophisticated clinical decision support systems to optimize patient care, and the necessity for robust regulatory reporting and compliance solutions. The trend towards precision health, leveraging big data and advanced analytics to tailor treatments to individual patient profiles, is also a significant catalyst. Furthermore, the widespread implementation of electronic health records (EHRs) has created a rich data ecosystem, ripe for analytical exploration, while the continuous advancements in artificial intelligence and machine learning are unlocking new possibilities for extracting actionable insights from complex healthcare datasets.

Clinical Data Analytics Industry Market Size (In Million)

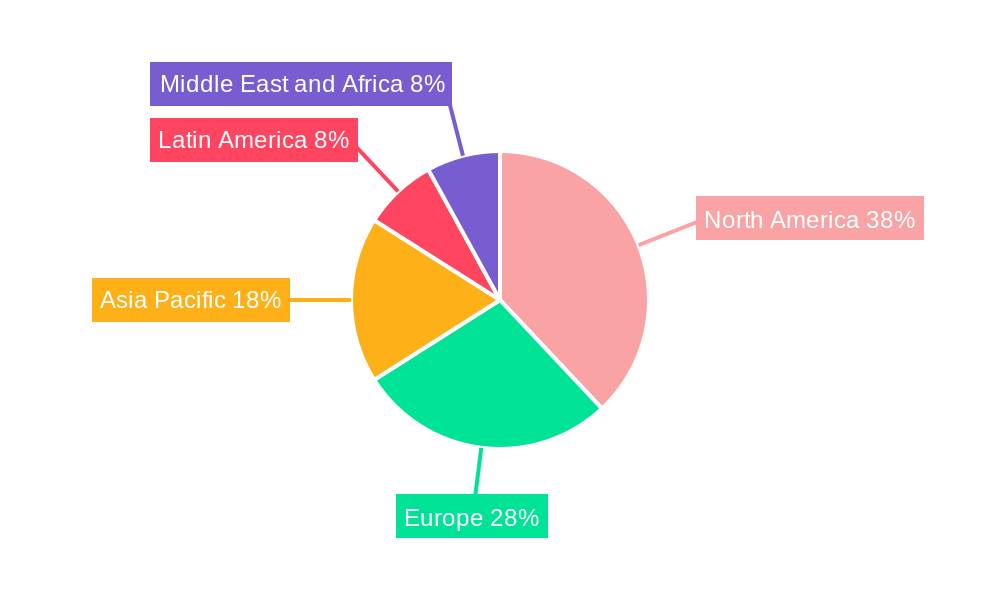

The market is segmented across diverse deployment models, with cloud-based solutions gaining significant traction due to their scalability, flexibility, and cost-effectiveness, alongside on-premise implementations for organizations with specific data security requirements. The application landscape is broad, encompassing critical areas such as quality improvement and clinical benchmarking, clinical decision support, regulatory reporting and compliance, comparative analytics, and the burgeoning field of precision health. Payers and providers represent the primary end-user verticals, both heavily investing in clinical data analytics to improve operational efficiency, reduce costs, and enhance patient outcomes. Geographically, North America is a dominant force, followed closely by Europe and the rapidly expanding Asia Pacific region, which is expected to witness significant growth due to increasing healthcare investments and digital transformation initiatives. While the market presents immense opportunities, potential restraints such as data privacy concerns, the need for skilled data scientists, and the integration challenges with legacy systems need to be strategically addressed by market players to fully capitalize on the growth trajectory.

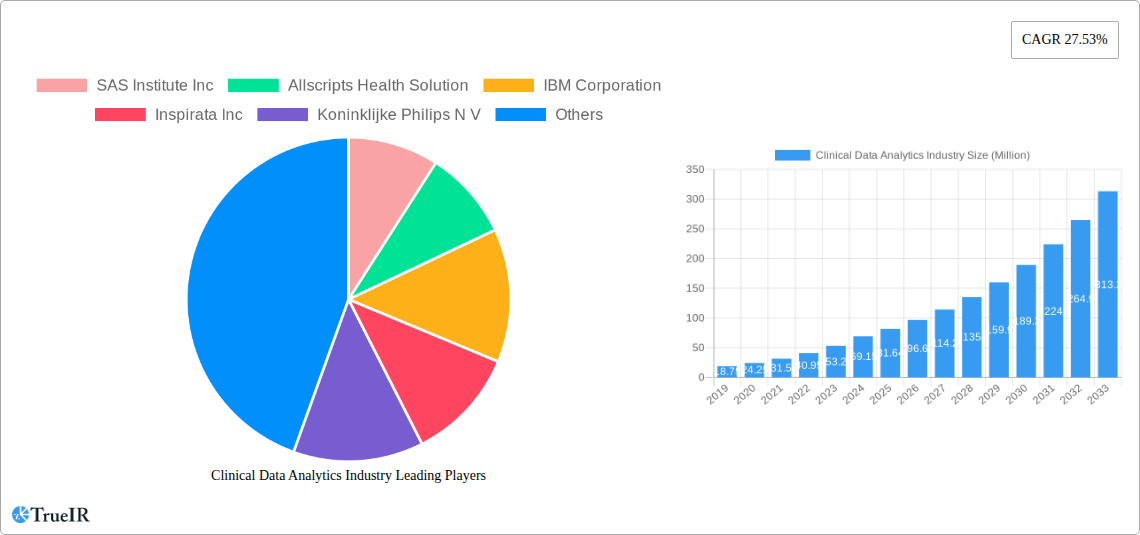

Clinical Data Analytics Industry Company Market Share

This comprehensive report provides an in-depth analysis of the global Clinical Data Analytics Industry, charting its evolution from 2019 to 2033. We delve into market dynamics, key trends, emerging opportunities, and the competitive landscape, offering critical insights for stakeholders aiming to navigate this rapidly expanding sector. Leveraging a robust study period, including historical data (2019–2024), a defined base year (2025), and an extensive forecast period (2025–2033), this report offers unparalleled foresight into market growth, technological advancements, and strategic imperatives.

Clinical Data Analytics Industry Market Structure & Competitive Landscape

The Clinical Data Analytics Industry is characterized by a moderately concentrated market structure, with key players investing heavily in research and development to drive innovation. The primary drivers of innovation include the increasing adoption of electronic health records (EHRs), the growing demand for personalized medicine, and the imperative for improved patient outcomes. Regulatory frameworks, while sometimes posing hurdles, also act as catalysts for data standardization and security, influencing market strategies. Product substitutes, such as traditional reporting tools, are gradually being eclipsed by advanced analytics platforms. End-user segmentation reveals a strong focus on providers and payers, with a growing emphasis on precision health applications. Mergers and Acquisitions (M&A) trends indicate a consolidation phase, with larger entities acquiring niche players to expand their service portfolios and market reach. Concentration ratios are estimated to be around 55% for the top five players. Over the study period, we anticipate approximately 300 M&A deals, significantly shaping market dynamics.

- Innovation Drivers: EHR adoption, personalized medicine, value-based care initiatives, AI/ML integration.

- Regulatory Impacts: Data privacy laws (e.g., HIPAA, GDPR), HITECH Act, evolving reimbursement models.

- End-User Focus: Providers (hospitals, clinics), Payers (insurance companies), Pharmaceutical companies, Research institutions.

- M&A Trends: Strategic acquisitions for technology enhancement, market expansion, and diversification.

Clinical Data Analytics Industry Market Trends & Opportunities

The Clinical Data Analytics Industry is poised for exponential growth, projected to reach a staggering market size of over $50 Million by the end of the forecast period. This surge is driven by a confluence of technological advancements, evolving consumer preferences for personalized healthcare, and intensifying competitive dynamics. The increasing digitization of healthcare, coupled with the growing volume of patient data generated daily, necessitates sophisticated analytical tools to derive actionable insights. Cloud-based deployment models are experiencing a substantial CAGR of approximately 15%, driven by their scalability, cost-effectiveness, and accessibility. On-premise solutions, while still relevant for highly sensitive data, are seeing a slower growth trajectory. The demand for applications like Quality Improvement and Clinical Benchmarking, Clinical Decision Support, and Regulatory Reporting and Compliance is rapidly escalating as healthcare organizations strive to enhance operational efficiency, improve patient safety, and meet stringent regulatory mandates. The advent of AI and machine learning is revolutionizing diagnostic capabilities and treatment planning, creating significant opportunities in Precision Health. The market penetration rate for advanced analytics solutions is expected to exceed 70% by 2033.

The global healthcare industry is undergoing a profound digital transformation, with clinical data analytics at its core. The sheer volume of health-related data, from electronic health records and medical imaging to wearable device outputs and genomic sequences, presents an unprecedented opportunity for extracting valuable insights. This data, when analyzed effectively, can lead to improved patient outcomes, reduced healthcare costs, and more efficient resource allocation. The market is witnessing a paradigm shift from reactive to proactive and predictive healthcare models, facilitated by sophisticated analytical tools. Furthermore, the growing emphasis on value-based care models incentivizes healthcare providers and payers to leverage data for outcome measurement and performance improvement.

Technological advancements, particularly in artificial intelligence (AI) and machine learning (ML), are accelerating the capabilities of clinical data analytics. These technologies enable the identification of complex patterns, prediction of disease outbreaks, personalization of treatment plans, and optimization of clinical trial designs. For instance, AI algorithms can analyze medical images with greater speed and accuracy than human radiologists, leading to earlier and more precise diagnoses. ML models can predict patient readmission risks, allowing for targeted interventions and preventing unnecessary hospitalizations. The integration of these technologies is not only enhancing the accuracy and efficiency of data analysis but also unlocking new frontiers in medical research and drug discovery.

Consumer preferences are also playing a crucial role in shaping the clinical data analytics market. Patients are increasingly becoming active participants in their healthcare journey, demanding more personalized and accessible care. This includes a desire for treatments tailored to their specific genetic makeup and lifestyle, as well as transparent information about their health status and treatment options. Clinical data analytics empowers providers to deliver this personalized experience by leveraging individual patient data to inform treatment decisions and patient engagement strategies. Wearable devices and health apps are further augmenting this trend by providing continuous streams of real-time health data, which can be analyzed to provide personalized health insights and recommendations.

Competitive dynamics within the industry are intensifying as established technology giants, specialized analytics firms, and healthcare IT providers vie for market share. This competition is fostering innovation and driving down costs, making advanced analytics solutions more accessible to a wider range of healthcare organizations. Strategic partnerships and collaborations are becoming increasingly common as companies seek to combine complementary expertise and expand their offerings. The market is also witnessing a growing demand for integrated platforms that can seamlessly manage and analyze data from disparate sources, offering a holistic view of patient health.

Dominant Markets & Segments in Clinical Data Analytics Industry

The Cloud deployment model is currently the dominant segment within the Clinical Data Analytics Industry, projected to continue its leadership throughout the forecast period. Its inherent scalability, cost-effectiveness, and ease of implementation make it the preferred choice for healthcare organizations of all sizes. The cloud infrastructure allows for rapid deployment of analytical tools and seamless integration with existing healthcare IT systems, fostering greater agility and responsiveness. This dominance is further bolstered by advancements in cloud security protocols, alleviating concerns regarding data privacy and compliance.

Among the applications, Quality Improvement and Clinical Benchmarking represents a significant growth driver. Healthcare providers are under immense pressure to demonstrate measurable improvements in patient care quality and operational efficiency. Clinical data analytics enables them to identify areas for improvement, track performance against benchmarks, and implement evidence-based interventions. Clinical Decision Support is another pivotal application, leveraging predictive analytics and AI to provide real-time recommendations to clinicians at the point of care, thereby enhancing diagnostic accuracy and treatment efficacy.

The Providers end-user vertical commands the largest market share, driven by the direct impact of clinical data analytics on patient care, operational management, and financial performance within hospitals, clinics, and health systems. Payers are also significant adopters, utilizing analytics for risk assessment, fraud detection, and optimizing reimbursement strategies. The increasing focus on Precision Health is fueling substantial growth in segments catering to personalized medicine, genomic analysis, and targeted therapies, further solidifying the importance of advanced analytics.

- Dominant Deployment Model: Cloud

- Growth Drivers: Scalability, cost-efficiency, ease of integration, enhanced security features.

- Market Penetration: Expected to exceed 80% by 2030.

- Leading Applications:

- Quality Improvement and Clinical Benchmarking: Focus on improving patient outcomes and operational efficiency.

- Clinical Decision Support: AI-powered recommendations for diagnosis and treatment.

- Regulatory Reporting and Compliance: Streamlining adherence to healthcare regulations.

- Comparative Analytics/Comparative Effectiveness: Evaluating treatment efficacy and cost-effectiveness.

- Precision Health: Tailoring treatments based on individual genetic and lifestyle factors.

- Primary End-User Vertical: Providers (hospitals, physician practices, health systems)

- Key Drivers: Need for improved patient care, operational efficiency, and cost containment.

- Emerging Growth Areas: Precision Health, Predictive Analytics for Population Health Management.

Clinical Data Analytics Industry Product Analysis

Clinical data analytics products are evolving beyond simple data aggregation and reporting. Innovations are centered on advanced AI and machine learning algorithms that enable predictive modeling, anomaly detection, and personalized insights. These products offer sophisticated dashboards, intuitive user interfaces, and seamless integration capabilities with diverse healthcare data sources, including EHRs, imaging systems, and genomic databases. Their competitive advantage lies in their ability to transform raw data into actionable intelligence, driving improved patient outcomes, operational efficiencies, and cost reductions. The market is witnessing a rise in specialized solutions for areas like population health management, real-time patient monitoring, and clinical trial optimization.

Key Drivers, Barriers & Challenges in Clinical Data Analytics Industry

Key Drivers:

- Surge in Healthcare Data: Proliferation of EHRs, IoT devices, and genomic sequencing generates massive datasets for analysis.

- Demand for Value-Based Care: Shift from fee-for-service to outcome-based reimbursement models necessitates data-driven performance evaluation.

- Advancements in AI and ML: Enhanced analytical capabilities for predictive modeling, personalized medicine, and faster diagnostics.

- Regulatory Mandates: Government initiatives and policies promoting data interoperability and evidence-based medicine.

Barriers & Challenges:

- Data Silos and Interoperability: Fragmented healthcare data systems hinder seamless integration and analysis.

- Data Privacy and Security Concerns: Strict regulations and the sensitive nature of health data pose significant challenges for data management and sharing.

- Workforce Skills Gap: Shortage of skilled data scientists and analysts with domain expertise in healthcare.

- High Implementation Costs: Initial investment in infrastructure, software, and training can be substantial for smaller organizations.

- Resistance to Change: Cultural barriers and skepticism towards adopting new technologies within healthcare institutions.

Growth Drivers in the Clinical Data Analytics Industry Market

The Clinical Data Analytics Industry is propelled by several robust growth drivers. The escalating volume of healthcare data, fueled by the widespread adoption of electronic health records (EHRs) and the proliferation of connected medical devices, provides the foundational fuel for analytics. The global shift towards value-based care models is a significant catalyst, incentivizing providers and payers to leverage data for outcome measurement and cost optimization. Furthermore, continuous advancements in Artificial Intelligence (AI) and Machine Learning (ML) are unlocking unprecedented analytical capabilities, enabling predictive diagnostics, personalized treatment plans, and population health management. Favorable government policies and mandates promoting data interoperability and the use of evidence-based medicine also contribute significantly to market expansion.

Challenges Impacting Clinical Data Analytics Industry Growth

Despite its promising trajectory, the Clinical Data Analytics Industry faces several significant challenges. Data interoperability remains a persistent hurdle, with fragmented healthcare IT systems creating data silos that impede seamless analysis. Stringent data privacy and security regulations, while essential, add complexity to data management and sharing initiatives. The industry also grapples with a shortage of skilled data scientists and analysts possessing both technical expertise and deep healthcare domain knowledge. The substantial initial investment required for implementing advanced analytics solutions can be a barrier for smaller healthcare organizations. Finally, cultural resistance to adopting new technologies within traditional healthcare settings can slow down the pace of adoption and innovation.

Key Players Shaping the Clinical Data Analytics Industry Market

- SAS Institute Inc

- Allscripts Health Solution

- IBM Corporation

- Inspirata Inc

- Koninklijke Philips N V

- Health Catalyst Inc

- Optum Inc

- Oracle Corporation

- CareEvolution Inc

- McKesson Corporation

Significant Clinical Data Analytics Industry Industry Milestones

- September 2023: Allscripts Healthcare, LLC announced a strategic collaboration to support primary care providers in improving patients’ health outcomes while strengthening their practices’ financial foundation, where Veradigm’s innovative solutions help to promote value-based care initiatives for healthcare providers and most importantly, the patients they serve.

- January 2023: American Hospital Dubai, a global healthcare industry platform, announced the launch of its new digital health information channel. The Digital Channel is a one-stop shop for knowledge and advice on healthcare topics, providing answers and solutions to all health and wellness concerns on a user-friendly digital platform, ushering in a new era in healthcare information. The digital channel, led by internationally certified doctors and specialists from American Hospital Dubai, will provide expert advice, in-depth insights, healthy lifestyle tips, and emerging healthcare developments, technologies, treatments, and breakthroughs. Furthermore, the channel's all-encompassing content includes healthy lifestyle education, guidance, tips, expert opinions and counseling, healthcare myths and realities, diet, nutrition, fitness, holistic health, and healthcare updates. It also provides information on medical breakthroughs, Med-Tech awareness, disease management, disease profiles, mental health, and the most recent treatments and medical technologies, such as AI and Robotics.

Future Outlook for Clinical Data Analytics Industry Market

The future outlook for the Clinical Data Analytics Industry is exceptionally bright, driven by continued technological innovation and an increasing imperative for data-driven healthcare. The integration of AI and ML will become more sophisticated, enabling hyper-personalization of treatments and predictive health interventions. The growth of the Internet of Medical Things (IoMT) will generate even larger volumes of real-time patient data, creating opportunities for continuous monitoring and proactive care. Strategic partnerships between technology providers, healthcare organizations, and research institutions will accelerate innovation and market penetration. The industry is poised to play a pivotal role in shaping a more efficient, equitable, and patient-centric healthcare ecosystem, with significant market potential estimated to reach over $100 Million by 2033.

Clinical Data Analytics Industry Segmentation

-

1. Deployment Model

- 1.1. Cloud

- 1.2. On-premise

-

2. Application

- 2.1. Quality Improvement and Clinical Benchmarking

- 2.2. Clinical Decision Support

- 2.3. Regulatory Reporting and Compliance

- 2.4. Comparative Analytics/Comparative Effectiveness

- 2.5. Precision Health

-

3. End-user Vertical

- 3.1. Payers

- 3.2. Providers

Clinical Data Analytics Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. Germany

- 2.2. United KIngdom

- 2.3. Italy

- 2.4. France

- 2.5. Spain

- 2.6. Rest of Europe

-

3. Asia Pacific

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. South Korea

- 3.5. Australia

- 3.6. Rest of Asia Pacific

-

4. Latin America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of Latin America

-

5. Middle East and Africa

- 5.1. GCC

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Clinical Data Analytics Industry Regional Market Share

Geographic Coverage of Clinical Data Analytics Industry

Clinical Data Analytics Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 27.53% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Focus on Population Health Management; Government Healthcare Policies; Clinical Data Analytics Enabling Personalized Patient Care; Growing Need to Contain Healthcare Expenditure

- 3.3. Market Restrains

- 3.3.1. Data Privacy and Security Concerns; High Cost of Implementation of EDI

- 3.4. Market Trends

- 3.4.1. Cloud Deployment Model to Hold a Dominant Position in the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Clinical Data Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Deployment Model

- 5.1.1. Cloud

- 5.1.2. On-premise

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Quality Improvement and Clinical Benchmarking

- 5.2.2. Clinical Decision Support

- 5.2.3. Regulatory Reporting and Compliance

- 5.2.4. Comparative Analytics/Comparative Effectiveness

- 5.2.5. Precision Health

- 5.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.3.1. Payers

- 5.3.2. Providers

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Deployment Model

- 6. North America Clinical Data Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Deployment Model

- 6.1.1. Cloud

- 6.1.2. On-premise

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Quality Improvement and Clinical Benchmarking

- 6.2.2. Clinical Decision Support

- 6.2.3. Regulatory Reporting and Compliance

- 6.2.4. Comparative Analytics/Comparative Effectiveness

- 6.2.5. Precision Health

- 6.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.3.1. Payers

- 6.3.2. Providers

- 6.1. Market Analysis, Insights and Forecast - by Deployment Model

- 7. Europe Clinical Data Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Deployment Model

- 7.1.1. Cloud

- 7.1.2. On-premise

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Quality Improvement and Clinical Benchmarking

- 7.2.2. Clinical Decision Support

- 7.2.3. Regulatory Reporting and Compliance

- 7.2.4. Comparative Analytics/Comparative Effectiveness

- 7.2.5. Precision Health

- 7.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 7.3.1. Payers

- 7.3.2. Providers

- 7.1. Market Analysis, Insights and Forecast - by Deployment Model

- 8. Asia Pacific Clinical Data Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Deployment Model

- 8.1.1. Cloud

- 8.1.2. On-premise

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Quality Improvement and Clinical Benchmarking

- 8.2.2. Clinical Decision Support

- 8.2.3. Regulatory Reporting and Compliance

- 8.2.4. Comparative Analytics/Comparative Effectiveness

- 8.2.5. Precision Health

- 8.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 8.3.1. Payers

- 8.3.2. Providers

- 8.1. Market Analysis, Insights and Forecast - by Deployment Model

- 9. Latin America Clinical Data Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Deployment Model

- 9.1.1. Cloud

- 9.1.2. On-premise

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Quality Improvement and Clinical Benchmarking

- 9.2.2. Clinical Decision Support

- 9.2.3. Regulatory Reporting and Compliance

- 9.2.4. Comparative Analytics/Comparative Effectiveness

- 9.2.5. Precision Health

- 9.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 9.3.1. Payers

- 9.3.2. Providers

- 9.1. Market Analysis, Insights and Forecast - by Deployment Model

- 10. Middle East and Africa Clinical Data Analytics Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Deployment Model

- 10.1.1. Cloud

- 10.1.2. On-premise

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Quality Improvement and Clinical Benchmarking

- 10.2.2. Clinical Decision Support

- 10.2.3. Regulatory Reporting and Compliance

- 10.2.4. Comparative Analytics/Comparative Effectiveness

- 10.2.5. Precision Health

- 10.3. Market Analysis, Insights and Forecast - by End-user Vertical

- 10.3.1. Payers

- 10.3.2. Providers

- 10.1. Market Analysis, Insights and Forecast - by Deployment Model

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 SAS Institute Inc

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Allscripts Health Solution

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 IBM Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Inspirata Inc

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Koninklijke Philips N V

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Health Catalyst Inc

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Optum Inc

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Oracle Corporation*List Not Exhaustive

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 CareEvolution Inc

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 McKesson Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.1 SAS Institute Inc

List of Figures

- Figure 1: Global Clinical Data Analytics Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Clinical Data Analytics Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 3: North America Clinical Data Analytics Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 4: North America Clinical Data Analytics Industry Revenue (Million), by Application 2025 & 2033

- Figure 5: North America Clinical Data Analytics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 6: North America Clinical Data Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 7: North America Clinical Data Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 8: North America Clinical Data Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Clinical Data Analytics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Clinical Data Analytics Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 11: Europe Clinical Data Analytics Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 12: Europe Clinical Data Analytics Industry Revenue (Million), by Application 2025 & 2033

- Figure 13: Europe Clinical Data Analytics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 14: Europe Clinical Data Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 15: Europe Clinical Data Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 16: Europe Clinical Data Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Clinical Data Analytics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Clinical Data Analytics Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 19: Asia Pacific Clinical Data Analytics Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 20: Asia Pacific Clinical Data Analytics Industry Revenue (Million), by Application 2025 & 2033

- Figure 21: Asia Pacific Clinical Data Analytics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Asia Pacific Clinical Data Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 23: Asia Pacific Clinical Data Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 24: Asia Pacific Clinical Data Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Pacific Clinical Data Analytics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Clinical Data Analytics Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 27: Latin America Clinical Data Analytics Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 28: Latin America Clinical Data Analytics Industry Revenue (Million), by Application 2025 & 2033

- Figure 29: Latin America Clinical Data Analytics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 30: Latin America Clinical Data Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 31: Latin America Clinical Data Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 32: Latin America Clinical Data Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Latin America Clinical Data Analytics Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Clinical Data Analytics Industry Revenue (Million), by Deployment Model 2025 & 2033

- Figure 35: Middle East and Africa Clinical Data Analytics Industry Revenue Share (%), by Deployment Model 2025 & 2033

- Figure 36: Middle East and Africa Clinical Data Analytics Industry Revenue (Million), by Application 2025 & 2033

- Figure 37: Middle East and Africa Clinical Data Analytics Industry Revenue Share (%), by Application 2025 & 2033

- Figure 38: Middle East and Africa Clinical Data Analytics Industry Revenue (Million), by End-user Vertical 2025 & 2033

- Figure 39: Middle East and Africa Clinical Data Analytics Industry Revenue Share (%), by End-user Vertical 2025 & 2033

- Figure 40: Middle East and Africa Clinical Data Analytics Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Clinical Data Analytics Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Clinical Data Analytics Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 2: Global Clinical Data Analytics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 3: Global Clinical Data Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 4: Global Clinical Data Analytics Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Clinical Data Analytics Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 6: Global Clinical Data Analytics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 7: Global Clinical Data Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 8: Global Clinical Data Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Canada Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Global Clinical Data Analytics Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 12: Global Clinical Data Analytics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 13: Global Clinical Data Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 14: Global Clinical Data Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 15: Germany Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: United KIngdom Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Italy Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: France Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Spain Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Rest of Europe Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Clinical Data Analytics Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 22: Global Clinical Data Analytics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 23: Global Clinical Data Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 24: Global Clinical Data Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: India Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: China Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: Japan Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: South Korea Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Australia Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Rest of Asia Pacific Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 31: Global Clinical Data Analytics Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 32: Global Clinical Data Analytics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 33: Global Clinical Data Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 34: Global Clinical Data Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 35: Brazil Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Argentina Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Rest of Latin America Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 38: Global Clinical Data Analytics Industry Revenue Million Forecast, by Deployment Model 2020 & 2033

- Table 39: Global Clinical Data Analytics Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Global Clinical Data Analytics Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 41: Global Clinical Data Analytics Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 42: GCC Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: South Africa Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: Rest of Middle East and Africa Clinical Data Analytics Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Clinical Data Analytics Industry?

The projected CAGR is approximately 27.53%.

2. Which companies are prominent players in the Clinical Data Analytics Industry?

Key companies in the market include SAS Institute Inc, Allscripts Health Solution, IBM Corporation, Inspirata Inc, Koninklijke Philips N V, Health Catalyst Inc, Optum Inc, Oracle Corporation*List Not Exhaustive, CareEvolution Inc, McKesson Corporation.

3. What are the main segments of the Clinical Data Analytics Industry?

The market segments include Deployment Model, Application, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 81.64 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Focus on Population Health Management; Government Healthcare Policies; Clinical Data Analytics Enabling Personalized Patient Care; Growing Need to Contain Healthcare Expenditure.

6. What are the notable trends driving market growth?

Cloud Deployment Model to Hold a Dominant Position in the Market.

7. Are there any restraints impacting market growth?

Data Privacy and Security Concerns; High Cost of Implementation of EDI.

8. Can you provide examples of recent developments in the market?

September 2023 - Allscripts Healthcare, LLC has announced a strategic collaboration to support primary care providers in improving patients’ health outcomes while strengthening their practices’ financial foundation, where Veradigm’s innovative solutions help to promote value-based care initiatives for healthcare providers and most importantly, the patients they serve.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Clinical Data Analytics Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Clinical Data Analytics Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Clinical Data Analytics Industry?

To stay informed about further developments, trends, and reports in the Clinical Data Analytics Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence