Key Insights

The European Military Aviation Market is projected for robust growth, expected to reach USD 67.81 billion by 2025, exhibiting a Compound Annual Growth Rate (CAGR) of 2.98% through 2033. This expansion is driven by heightened geopolitical instability and ongoing defense modernization initiatives across European nations. Significant investments are being made in sophisticated fighter jets, advanced surveillance aircraft, and versatile helicopters to bolster national defense postures and ensure regional security. Demand for multi-role aircraft, capable of diverse missions including air-to-air combat, ground attack, and reconnaissance, is a primary growth catalyst. Advancements in rotorcraft technology, particularly multi-mission helicopters for troop transport, medical evacuation, and attack operations, also contribute to market dynamism. Leading industry players such as Airbus SE, Lockheed Martin Corporation, and Dassault Aviation are spearheading innovation and securing key contracts.

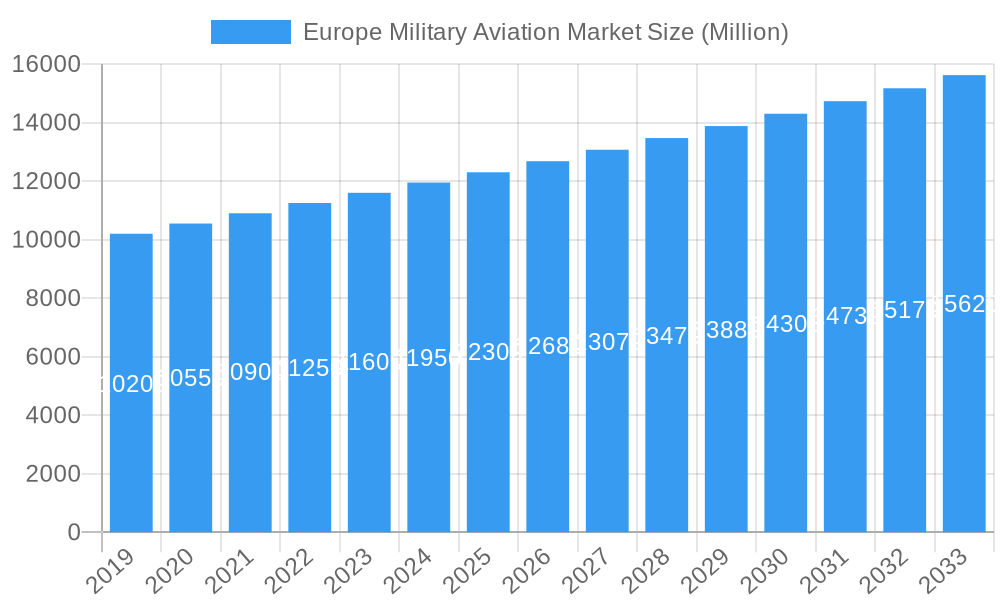

Europe Military Aviation Market Market Size (In Billion)

Market dynamics are further influenced by the escalating adoption of Unmanned Aerial Vehicles (UAVs) and the integration of cutting-edge electronic warfare and communication systems into both new and existing platforms. The systematic replacement of aging aircraft fleets with more technologically advanced and fuel-efficient models is another significant driver. Nevertheless, substantial acquisition and maintenance costs for advanced military aircraft, alongside complex defense procurement regulatory frameworks, present market restraints. Despite these challenges, the sustained commitment of European countries to enhance their aerial defense capabilities, coupled with continuous technological innovation and strategic collaborations, will ensure sustained growth and innovation in the European Military Aviation Market throughout the forecast period.

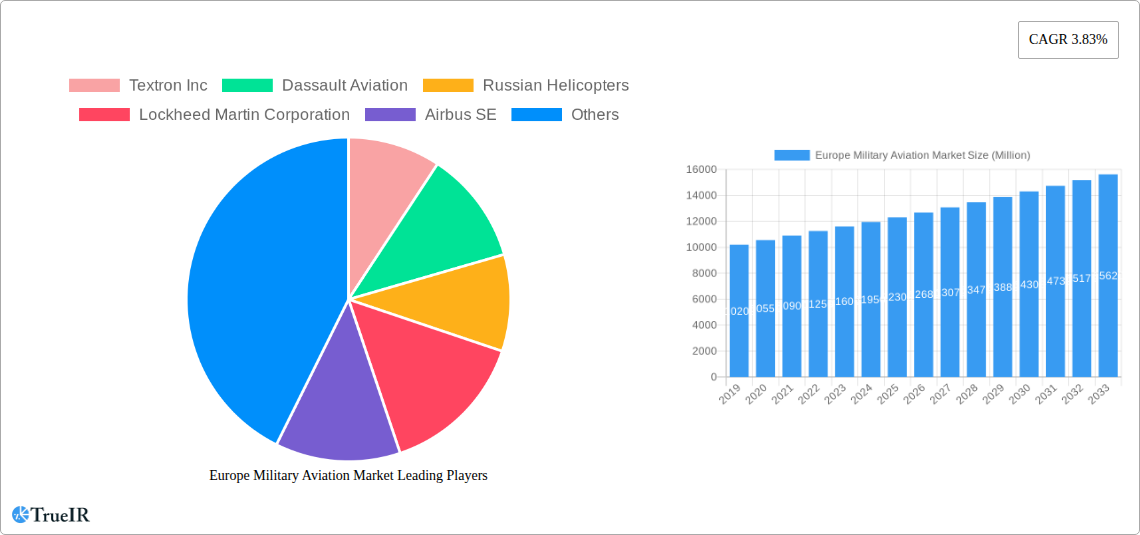

Europe Military Aviation Market Company Market Share

Europe Military Aviation Market: Comprehensive Market Analysis Report (2019–2033)

Unlock critical insights into the evolving Europe Military Aviation Market with this in-depth analysis. Covering the historical period of 2019–2024 and a robust forecast period of 2025–2033, with a base year of 2025, this report provides an indispensable resource for stakeholders navigating this dynamic sector. We delve into market size, growth drivers, technological advancements, competitive landscapes, and future opportunities. This report is meticulously designed for immediate use without further modification, leveraging high-volume SEO keywords to maximize visibility and reach industry professionals.

Europe Military Aviation Market Market Structure & Competitive Landscape

The Europe Military Aviation Market exhibits a moderately concentrated structure, driven by a handful of established global defense contractors and a growing number of specialized European players. Innovation is a key driver, fueled by ongoing defense modernization programs across European nations and a persistent need for advanced capabilities in areas such as air superiority, intelligence, surveillance, and reconnaissance (ISR), and strategic airlift. Regulatory impacts are significant, with strict procurement processes, export controls, and evolving defense policies shaping market access and product development. Product substitutes are limited in the military aviation sector due to highly specialized requirements and long development cycles, although advancements in drone technology and directed energy weapons present potential long-term disruptive forces. End-user segmentation primarily revolves around national defense ministries, which dictate procurement needs based on geopolitical threats and strategic objectives. Mergers and acquisitions (M&A) trends are evident as companies seek to consolidate capabilities, expand market share, and achieve economies of scale. For instance, strategic alliances and joint ventures are common to share development costs for complex platforms. Concentration ratios are influenced by the dominant share held by major players in high-value segments like fighter aircraft and heavy-lift helicopters. The competitive landscape is characterized by intense R&D investment, a focus on indigenous production capabilities, and strategic partnerships for technological advancement. The market is characterized by a limited number of large, well-established companies and a more fragmented segment of smaller, specialized suppliers.

Europe Military Aviation Market Market Trends & Opportunities

The Europe Military Aviation Market is projected to experience significant growth, with an estimated market size of approximately $XX Billion in 2025 and a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period of 2025–2033. This expansion is underpinned by several key trends. A primary driver is the sustained increase in defense spending across European nations, spurred by evolving geopolitical dynamics and a renewed emphasis on collective security. This heightened investment is translating into demand for advanced fixed-wing aircraft, including multi-role combat aircraft and modern transport platforms, as well as sophisticated rotorcraft for a myriad of missions. Technological shifts are profoundly impacting the market, with a strong emphasis on digitalization, artificial intelligence (AI), autonomous systems, and next-generation propulsion technologies. The integration of these technologies is aimed at enhancing operational efficiency, improving situational awareness, and reducing crew workload in both fixed-wing and rotorcraft segments. Consumer preferences, in this context, are dictated by military requirements for interoperability, survivability, and cost-effectiveness throughout the lifecycle of an asset. Advanced avionics, stealth capabilities, and enhanced electronic warfare suites are becoming increasingly critical. Competitive dynamics are characterized by strategic collaborations between established defense giants and emerging technology providers to foster innovation and maintain a competitive edge. The market is also witnessing a growing demand for upgrades and modernization of existing fleets, offering substantial opportunities for companies specializing in life-extension programs and system enhancements. Furthermore, the increasing focus on sustainable aviation fuels and eco-friendly manufacturing processes is emerging as a significant trend, influencing procurement decisions and R&D priorities. Opportunities abound in the development of unmanned aerial systems (UAS) and their integration with manned platforms, offering enhanced ISR capabilities and force protection. The development of advanced training aircraft that incorporate simulation technologies and prepare pilots for complex modern warfare scenarios is another area of significant growth. The demand for specialized rotorcraft, such as multi-mission helicopters equipped with advanced sensor suites and weaponry, is also on the rise, driven by requirements for tactical troop transport, special operations, and casualty evacuation. Market penetration rates for cutting-edge technologies are expected to climb steadily as defense budgets continue to prioritize modernization and the adoption of advanced capabilities.

Dominant Markets & Segments in Europe Military Aviation Market

The Europe Military Aviation Market is a complex ecosystem with distinct regions and segments demonstrating varying levels of dominance and growth potential. Fixed-Wing Aircraft consistently represent a dominant segment, driven by their versatility in strategic and tactical operations. Within this, Multi-Role Aircraft command a significant market share due to their ability to perform a wide array of missions, from air-to-air combat and air-to-ground attack to reconnaissance and electronic warfare. The ongoing modernization efforts by NATO members and other European nations to counter evolving threats have led to substantial investments in advanced fighter jets and strategic bombers. Key growth drivers for this sub-segment include the development of fifth and sixth-generation fighter aircraft, enhanced avionics, and integration of directed energy weapons.

Transport Aircraft also hold substantial importance, particularly in light of increased geopolitical instability and the need for rapid force projection and logistical support. Military airlift capabilities are crucial for deployment of troops, equipment, and humanitarian aid, driving demand for modern, fuel-efficient, and robust transport aircraft. Government policies prioritizing strategic mobility and interoperability among allied forces are key enablers for this segment's growth.

The Rotorcraft segment, while generally smaller in overall market value compared to fixed-wing aircraft, is critical for tactical operations. Multi-Mission Helicopters are experiencing strong demand, serving roles such as attack, reconnaissance, utility, and search and rescue. The modularity and adaptability of these platforms make them indispensable assets for modern military operations. Growth in this area is fueled by advancements in rotorcraft technology, including improved speed, range, payload capacity, and the integration of sophisticated sensor and weapon systems.

Training Aircraft are also a vital component, ensuring a steady supply of well-trained pilots for increasingly complex aviation platforms. The trend towards advanced simulation and integrated training solutions supports the demand for modern, cost-effective training aircraft that can replicate real-world combat scenarios.

Geographically, Western Europe is expected to remain the dominant region due to the robust defense budgets of countries like Germany, France, the United Kingdom, and Italy. These nations are at the forefront of military modernization initiatives, investing heavily in next-generation platforms and technologies. Government policies favoring indigenous defense industries and fostering international collaboration within the EU and NATO frameworks further strengthen their market position.

Europe Military Aviation Market Product Analysis

Product innovation in the Europe Military Aviation Market is characterized by a relentless pursuit of enhanced performance, greater operational flexibility, and superior survivability. Key advancements include the integration of artificial intelligence and machine learning for improved decision-making, autonomous operations, and predictive maintenance. Next-generation avionics suites, offering enhanced situational awareness through fused sensor data and advanced display technologies, are becoming standard. Stealth technologies, advanced materials for reduced radar cross-section and weight, and sophisticated electronic warfare systems are critical competitive advantages, particularly for multi-role aircraft. In the rotorcraft segment, innovations focus on improved speed, range, payload capacity, and reduced acoustic signatures, alongside enhanced survivability features such as advanced armor and countermeasures. The application of these products spans a wide spectrum, from air superiority and deep strike missions for fixed-wing aircraft to tactical troop transport, reconnaissance, and combat support for rotorcraft. The competitive advantage for manufacturers lies in their ability to deliver platforms that meet stringent military specifications, offer lifecycle cost savings, and provide a demonstrable technological edge.

Key Drivers, Barriers & Challenges in Europe Military Aviation Market

Key Drivers: The Europe Military Aviation Market is propelled by several significant factors. Geopolitical tensions and the perceived need for enhanced national security are primary drivers, leading to increased defense spending and modernization programs. Technological advancements, such as AI, autonomous systems, and advanced materials, offer opportunities for capability enhancement and operational efficiency, driving demand for next-generation platforms. Government policies supporting indigenous defense industries, fostering international collaboration within NATO and EU frameworks, and prioritizing strategic autonomy further stimulate market growth. Economic factors, including national GDP growth and defense budget allocations, play a crucial role in determining procurement volumes.

Barriers & Challenges: The market faces several critical barriers and challenges. Stringent regulatory frameworks, including complex procurement processes, export controls, and evolving safety standards, can significantly lengthen development and deployment timelines and increase costs. Supply chain disruptions, exacerbated by global events and component sourcing complexities, pose a substantial risk to production schedules and cost management. Intense competition among established players and emerging technology providers pressures profit margins and necessitates continuous innovation. High research and development costs for advanced military aviation technologies require significant upfront investment. Furthermore, the long lifecycle of military assets and the need for interoperability with existing fleets can create inertia and limit the adoption of entirely new systems. The budgetary constraints faced by some European nations also present a significant restraint.

Growth Drivers in the Europe Military Aviation Market Market

The Europe Military Aviation Market is experiencing robust growth driven by several pivotal factors. The escalating geopolitical landscape and renewed focus on defense modernization programs across Europe are compelling nations to invest in advanced air capabilities. Technological innovation, particularly in areas like artificial intelligence, unmanned systems, and advanced sensor integration, is a significant catalyst, enabling enhanced operational effectiveness and offering new strategic advantages. Government policies supporting indigenous defense manufacturing, fostering interoperability through initiatives like the European Defence Fund, and promoting strategic partnerships are crucial growth enablers. The continuous need for fleet upgrades and life-extension programs for existing assets also contributes to sustained market activity.

Challenges Impacting Europe Military Aviation Market Growth

Challenges impacting Europe Military Aviation Market growth are multifaceted. Stringent regulatory environments and lengthy procurement cycles often create significant delays and cost overruns in acquisition programs. Global supply chain vulnerabilities, particularly for specialized components and raw materials, can disrupt production schedules and increase manufacturing costs, as seen with recent global events. Intense competition among established defense contractors and the emergence of new technology providers necessitate continuous and substantial investment in research and development, placing financial pressure on companies. Furthermore, the high cost of developing and acquiring advanced military aircraft, coupled with the complex integration requirements of new technologies into existing force structures, presents significant financial and logistical hurdles for many nations.

Key Players Shaping the Europe Military Aviation Market Market

- Airbus SE

- Lockheed Martin Corporation

- The Boeing Company

- Dassault Aviation

- Leonardo S p A

- Russian Helicopters

- Textron Inc

- United Aircraft Corporation

- Pilatus Aircraft Ltd

- ATR

- MD Helicopters LLC

- Hughes Helicopters

Significant Europe Military Aviation Market Industry Milestones

- June 2023: Airbus Flight Academy Europe, a subsidiary of Airbus that supplies training services for the pilots and civilian cadets of the French Armed Forces, signed a memorandum of understanding (MoU) with AURA AERO. This collaboration aims to explore future training solutions and sustainable aviation practices.

- May 2023: The US State Department approved a potential sale of CH-47 Chinook helicopters, engines, and associated equipment worth USD 8.5 billion to Germany. This significant deal underscores the ongoing demand for heavy-lift transport capabilities and strengthens transatlantic defense ties.

- March 2023: Boeing was awarded a contract by the US government to manufacture 184 AH-64E Apache attack helicopters. The US government announced USD 1.95 million for this contract, indicating that these helicopters will be delivered to the US military and international customers, including Australia and Egypt, as part of the Foreign Military Sales (FMS) program. Contract completion is expected by the end of 2027, highlighting the sustained demand for advanced attack rotorcraft.

Future Outlook for Europe Military Aviation Market Market

The future outlook for the Europe Military Aviation Market is one of continued expansion and technological evolution. The persistent need for advanced defense capabilities, driven by a complex geopolitical environment, will ensure sustained investment in military aviation platforms. Key growth catalysts include the ongoing development and integration of artificial intelligence, autonomous systems, and advanced cyber warfare capabilities across both fixed-wing and rotorcraft segments. The drive towards greater interoperability within NATO and the European Union will foster collaborative development and procurement efforts. Opportunities will also arise from the increasing focus on sustainable aviation technologies and the modernization of existing fleets with digital enhancements and survivability upgrades. The market is poised to witness significant advancements in unmanned aerial systems and their integration into manned platforms, further shaping the future of military operations and offering substantial growth potential for innovative companies.

Europe Military Aviation Market Segmentation

-

1. Sub Aircraft Type

-

1.1. Fixed-Wing Aircraft

- 1.1.1. Multi-Role Aircraft

- 1.1.2. Training Aircraft

- 1.1.3. Transport Aircraft

- 1.1.4. Others

-

1.2. Rotorcraft

- 1.2.1. Multi-Mission Helicopter

- 1.2.2. Transport Helicopter

-

1.1. Fixed-Wing Aircraft

Europe Military Aviation Market Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

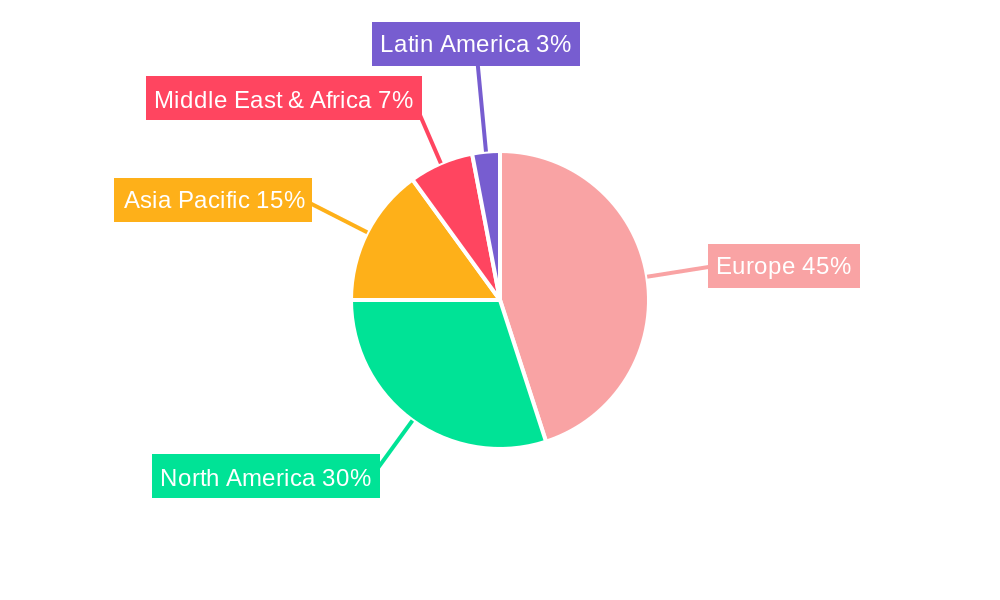

Europe Military Aviation Market Regional Market Share

Geographic Coverage of Europe Military Aviation Market

Europe Military Aviation Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.98% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 5.1.1. Fixed-Wing Aircraft

- 5.1.1.1. Multi-Role Aircraft

- 5.1.1.2. Training Aircraft

- 5.1.1.3. Transport Aircraft

- 5.1.1.4. Others

- 5.1.2. Rotorcraft

- 5.1.2.1. Multi-Mission Helicopter

- 5.1.2.2. Transport Helicopter

- 5.1.1. Fixed-Wing Aircraft

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 6. Europe Military Aviation Market Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 6.1.1. Fixed-Wing Aircraft

- 6.1.1.1. Multi-Role Aircraft

- 6.1.1.2. Training Aircraft

- 6.1.1.3. Transport Aircraft

- 6.1.1.4. Others

- 6.1.2. Rotorcraft

- 6.1.2.1. Multi-Mission Helicopter

- 6.1.2.2. Transport Helicopter

- 6.1.1. Fixed-Wing Aircraft

- 6.1. Market Analysis, Insights and Forecast - by Sub Aircraft Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Textron Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Dassault Aviation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Russian Helicopters

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Lockheed Martin Corporation

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Airbus SE

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 MD Helicopters LLC

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 United Aircraft Corporatio

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Pilatus Aircraft Ltd

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Leonardo S p A

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 ATR

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Hughes Helicopters

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 The Boeing Company

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Textron Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Military Aviation Market Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Military Aviation Market Share (%) by Company 2025

List of Tables

- Table 1: Europe Military Aviation Market Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 2: Europe Military Aviation Market Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Europe Military Aviation Market Revenue billion Forecast, by Sub Aircraft Type 2020 & 2033

- Table 4: Europe Military Aviation Market Revenue billion Forecast, by Country 2020 & 2033

- Table 5: United Kingdom Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: Germany Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: France Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Italy Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Spain Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Netherlands Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 11: Belgium Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 12: Sweden Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Norway Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Poland Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Denmark Europe Military Aviation Market Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Military Aviation Market?

The projected CAGR is approximately 2.98%.

2. Which companies are prominent players in the Europe Military Aviation Market?

Key companies in the market include Textron Inc, Dassault Aviation, Russian Helicopters, Lockheed Martin Corporation, Airbus SE, MD Helicopters LLC, United Aircraft Corporatio, Pilatus Aircraft Ltd, Leonardo S p A, ATR, Hughes Helicopters, The Boeing Company.

3. What are the main segments of the Europe Military Aviation Market?

The market segments include Sub Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 67.81 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

June 2023: Airbus Flight Academy Europe, a subsidiary of Airbus that supplies training services for the pilots and civilian cadets of the French Armed Forces, signed a memorandum of understanding (MoU) with AURA AERO.May 2023: The US State Department approved a potential sale of CH-47 Chinook helicopters, engines, and equipment worth USD 8.5 billion to Germany.March 2023: Boeing has been awarded a contract by the US government to manufacture 184 AH-64E Apache attack helicopters for the US military and international customers. The US government announced USD 1.95 million, indicating that the helicopter will be delivered to the US military and overseas buyers - specifically Australia and Egypt - as a part of the paramilitary process to the Foreign Service (FMS) from the US government. Contract completion is expected by the end of 2027.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Military Aviation Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Military Aviation Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Military Aviation Market?

To stay informed about further developments, trends, and reports in the Europe Military Aviation Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence