Key Insights

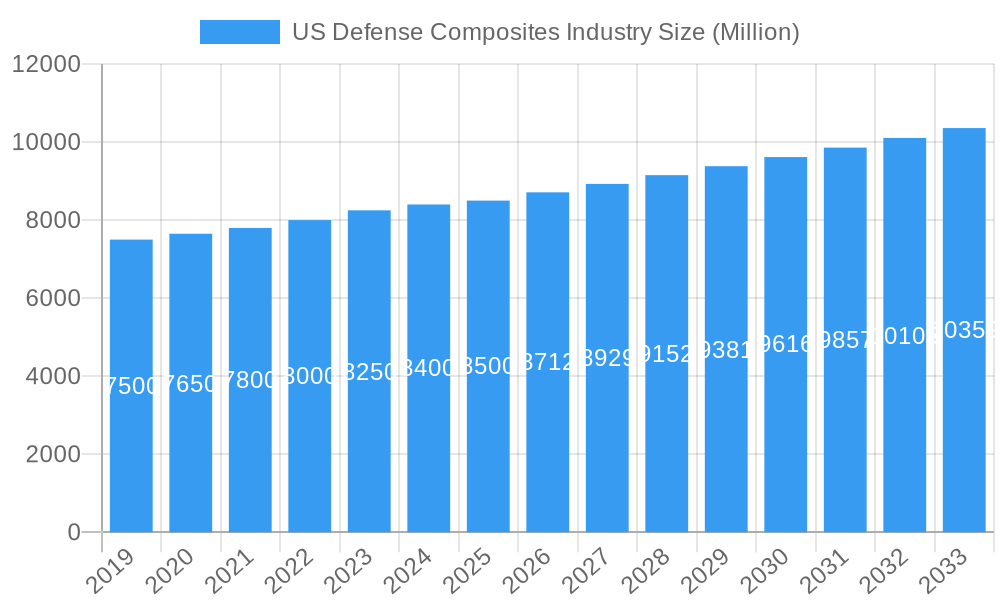

The US Defense Composites market is projected to experience robust expansion, fueled by escalating demand for lightweight, high-strength materials in critical defense systems. With an estimated market size of $10.3 billion in 2024 and a projected Compound Annual Growth Rate (CAGR) of 5.6%, industry growth is driven by the imperative for improved performance, fuel efficiency, and survivability in military applications. Key growth catalysts include the modernization of manned and unmanned aircraft fleets, the development of advanced naval vessels, and the demand for superior personnel protective equipment. Continuous pursuit of technological superiority in defense necessitates the adoption of cutting-edge composite materials offering exceptional strength-to-weight ratios over conventional metals. This trend is particularly pronounced in aerospace, where lighter aircraft enhance payload capacity and operational range, vital for offensive and defensive operations.

US Defense Composites Industry Market Size (In Billion)

Evolving geopolitical dynamics further influence market trajectory, stimulating increased defense expenditure and investment in advanced material research and development. While thermoset and thermoplastic composites maintain strong demand, ceramic matrix composites (CMCs) are gaining traction for high-temperature applications and enhanced thermal protection. However, high initial costs of advanced composites, coupled with specialized manufacturing process and skilled labor requirements, may present growth restraints. Additionally, stringent regulatory mandates and complex supply chain management for these specialized materials pose ongoing challenges. Despite these obstacles, the strategic significance of advanced composites in maintaining a US military technological edge ensures sustained market interest and development.

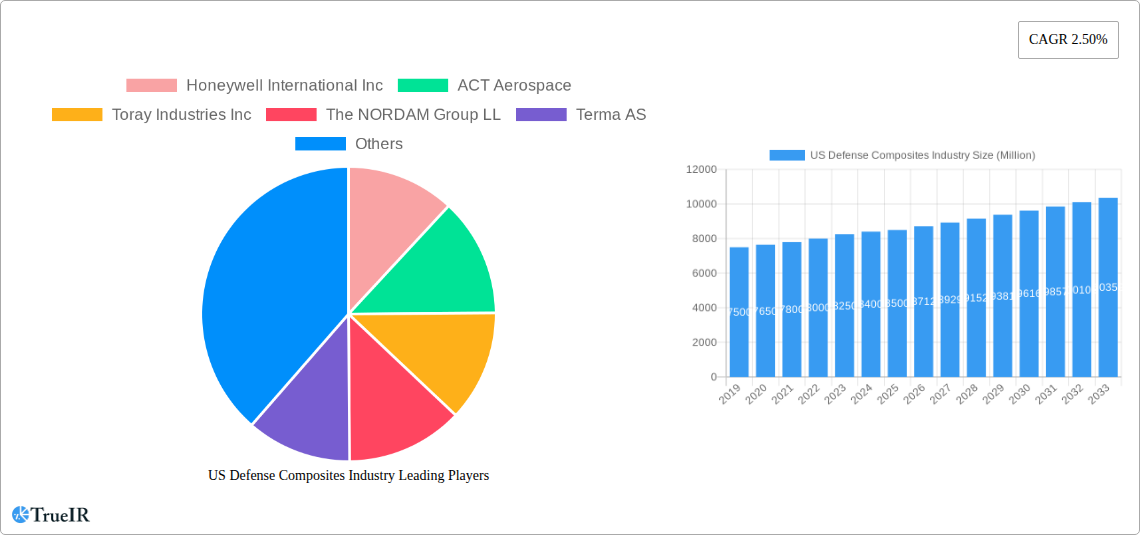

US Defense Composites Industry Company Market Share

This report provides an in-depth analysis of the US Defense Composites market, forecasting its evolution. Utilizing high-volume keywords such as "defense composites," "aerospace composites," "military applications," "advanced materials," and "US defense industry," this analysis is optimized for SEO performance, delivering actionable intelligence for industry stakeholders, procurement officers, researchers, and investors.

US Defense Composites Industry Market Structure & Competitive Landscape

The US Defense Composites Industry exhibits a moderately concentrated market structure, with a leading player's share estimated at around 25%. This concentration is driven by significant R&D investments, stringent qualification processes, and the high capital expenditure required for advanced manufacturing facilities. Innovation is a paramount driver, fueled by the continuous demand for lighter, stronger, and more durable materials to enhance the performance and survivability of defense platforms. Key innovation areas include advanced resin systems, novel fiber reinforcements, and additive manufacturing techniques for composite components. Regulatory impacts, primarily from the Department of Defense (DoD) and various security agencies, focus on material certification, supply chain security, and intellectual property protection, influencing product development and market entry strategies. Product substitutes, such as advanced metallic alloys and ceramics, present a competitive challenge, but the superior strength-to-weight ratio of composites in critical applications often outweighs these alternatives. End-user segmentation is dominated by the aerospace sector, followed by naval applications and land vehicles. Mergers and acquisitions (M&A) activity has been consistent, with an estimated 15 significant transactions between 2019 and 2024, aimed at consolidating market share, acquiring specialized technologies, and expanding product portfolios.

US Defense Composites Industry Market Trends & Opportunities

The US Defense Composites Industry is poised for robust growth, with an estimated market size of $5,500 Million in the base year 2025, projected to reach $9,200 Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period. This expansion is underpinned by several key trends. Firstly, the persistent global security challenges and the ongoing modernization of military fleets worldwide are driving sustained demand for high-performance composite materials. Unmanned Aerial Vehicles (UAVs) and next-generation fighter jets are increasingly reliant on composites for weight reduction, fuel efficiency, and enhanced maneuverability, representing a significant growth avenue. Secondly, advancements in resin technology, particularly in the development of high-temperature thermoset resins and advanced thermoplastic composites, are enabling wider applications in harsh operational environments. These innovations offer improved processability, recyclability, and impact resistance, addressing critical performance requirements.

Consumer preferences within the defense sector are evolving towards platforms that offer greater operational flexibility, reduced lifecycle costs, and enhanced stealth capabilities. Composites are uniquely positioned to meet these demands due to their inherent design flexibility and corrosion resistance, which translate to lower maintenance needs and extended service life. The competitive dynamics are characterized by a blend of established aerospace and defense giants and specialized composite manufacturers. Partnerships and collaborations between material suppliers, component manufacturers, and prime defense contractors are becoming increasingly common to accelerate product development and secure long-term contracts. Opportunities abound in the development of smart composites with integrated sensing capabilities for structural health monitoring, the application of composites in directed energy weapon systems, and the exploration of novel ceramic matrix composites for hypersonic applications. The increasing focus on sustainability within the defense sector also presents an opportunity for the development and adoption of bio-based or recyclable composite materials. The market penetration rate for advanced composites in new defense platforms is steadily increasing, reflecting their growing acceptance and proven performance benefits.

Dominant Markets & Segments in US Defense Composites Industry

The dominant segment within the US Defense Composites Industry is Manned and Unmanned Aircraft, accounting for an estimated 65% of the total market share in 2025. This dominance is driven by the unyielding demand for weight reduction in aircraft design to improve fuel efficiency, payload capacity, and operational range.

- Manned Aircraft: The development of next-generation fighter jets, bombers, and transport aircraft extensively utilizes composites for airframes, wings, and internal structures. The emphasis on stealth technology further amplifies the use of radar-absorbent composite materials.

- Unmanned Aircraft (UAVs): The exponential growth in the UAV market, from tactical reconnaissance drones to large autonomous combat platforms, is a primary growth catalyst. Composites enable the lightweight, durable, and aerodynamically efficient designs required for extended loiter times and complex mission profiles. The projected market size for UAV composites is estimated to reach $3,500 Million by 2033.

Naval Ships represent the second-largest segment, projected to capture 15% of the market share by 2025, with an estimated market value of $825 Million.

- Key Growth Drivers: The need for lighter, more corrosion-resistant structures in naval vessels to enhance speed and reduce maintenance costs is driving composite adoption. Composite materials are increasingly being used in superstructure, hulls, and internal components of frigates, destroyers, and submarines. The development of composite mine countermeasures vessels offers a significant niche opportunity.

Land Vehicles constitute approximately 10% of the market share, with a projected value of $550 Million in 2025.

- Key Growth Drivers: The demand for lighter, more survivable armored vehicles, including tanks and personnel carriers, fuels composite usage. Composites offer superior ballistic protection and weight savings compared to traditional armor. The development of specialized vehicles for logistics and reconnaissance also benefits from composite solutions.

Protective Equipment accounts for the remaining 10% of the market, valued at $550 Million in 2025.

- Key Growth Drivers: This segment includes advanced body armor, helmets, and fragmentation protection. The ongoing evolution of threats necessitates lighter yet more effective protective gear, making composites an essential material.

In terms of Resin Type, Thermoset Composites currently dominate the market, holding an estimated 70% share due to their established performance characteristics, particularly in structural applications requiring high strength and stiffness. However, Thermoplastic Composites are experiencing significant growth, projected to expand their market share to 25% by 2033, driven by their faster processing times, recyclability, and improved impact resistance, making them ideal for high-volume production and complex geometries. Ceramic Matrix Composites (CMCs), while currently representing a smaller niche market (estimated 5% share), are crucial for high-temperature applications, such as engine components and hypersonic vehicle parts, and are expected to see substantial growth in specialized defense sectors.

US Defense Composites Industry Product Analysis

The US Defense Composites Industry is characterized by continuous product innovation, focusing on enhancing material properties for extreme environments and advanced combat applications. Key advancements include the development of high-strength carbon fiber prepregs with superior fatigue resistance for next-generation aircraft structures, and the integration of self-healing resins for improved battlefield survivability of vehicles and equipment. Thermoplastic composite solutions are gaining traction for their rapid manufacturing capabilities, enabling faster deployment of components and reduced lifecycle costs. The competitive advantage lies in a combination of advanced material science, precise manufacturing processes, and the ability to meet stringent military specifications for performance, durability, and reliability.

Key Drivers, Barriers & Challenges in US Defense Composites Industry

Key Drivers: The primary forces propelling the US Defense Composites Industry include the continuous modernization of military assets driven by evolving geopolitical threats, demanding lighter and more resilient platforms. Technological advancements in material science, such as high-performance carbon fibers and advanced resin systems, offer enhanced performance benefits. Government initiatives and defense spending, particularly on next-generation aircraft and naval vessels, provide a significant economic impetus.

Barriers & Challenges: Significant challenges include the high initial cost of advanced composite materials and manufacturing processes, which can impact budget constraints. Stringent qualification and certification requirements by defense agencies create long development cycles. Supply chain disruptions, particularly for specialized raw materials like high-grade carbon fibers, can impact production timelines and costs. Additionally, the emergence of advanced metallic alloys and competitive material solutions presents an ongoing challenge to market share. The complexity of composite repair in field environments also requires specialized training and equipment.

Growth Drivers in the US Defense Composites Industry Market

Key growth drivers are centered on the persistent need for technological superiority in defense. The ongoing shift towards advanced aerospace platforms, including stealth aircraft and unmanned systems, directly translates to increased demand for lightweight, high-strength composite materials. Government investment in defense modernization programs, particularly those focused on next-generation capabilities, acts as a powerful economic engine. Furthermore, continuous innovation in material science, such as the development of advanced thermoset and thermoplastic resins with improved thermal and impact resistance, unlocks new application potentials. The increasing focus on reducing the lifecycle costs of military assets also favors composites due to their inherent durability and reduced maintenance requirements, further fueling market expansion.

Challenges Impacting US Defense Composites Industry Growth

Several challenges impact the growth trajectory of the US Defense Composites Industry. The high cost associated with the research, development, and manufacturing of advanced composites remains a significant barrier, especially for programs with tight budgets. Regulatory hurdles, including stringent qualification and certification processes, can lead to extended development timelines and increased overheads. Supply chain vulnerabilities, particularly for critical raw materials, pose a risk to consistent production and delivery. Competitive pressures from alternative advanced materials, such as high-strength metal alloys, necessitate continuous innovation and cost optimization within the composites sector. The need for specialized workforce training in composite design, manufacturing, and repair also presents an ongoing challenge.

Key Players Shaping the US Defense Composites Industry Market

- Honeywell International Inc

- ACT Aerospace

- Toray Industries Inc

- The NORDAM Group LLC

- Terma AS

- Advanced Composites Inc

- Leading Technology Composites Inc (LTC)

- Huntsman International LLC

- LMI AEROSPACE

- DuPont

- Solvay SA

- CFOAM LLC

- Hexcel Corporation

- Alpine Advanced Materials

- Sherwood Advanced Composite Technologies

Significant US Defense Composites Industry Industry Milestones

- 2019: Introduction of advanced, higher-modulus carbon fibers enabling lighter and stronger aircraft components.

- 2020: Increased adoption of additive manufacturing for composite parts, reducing lead times and enabling complex geometries for UAVs.

- 2021: Significant breakthroughs in resin systems for enhanced fire resistance and improved performance in extreme temperature environments.

- 2022: Expansion of thermoplastic composite applications in naval ship construction for reduced weight and improved corrosion resistance.

- 2023: Strategic acquisitions by major players to consolidate expertise in specialized composite technologies and expand market reach.

- 2024: Advancements in ceramic matrix composites for hypersonic vehicle applications, marking a critical step in high-speed defense technologies.

Future Outlook for US Defense Composites Industry Market

The future outlook for the US Defense Composites Industry is exceptionally promising, driven by an unwavering demand for enhanced military capabilities. Strategic opportunities lie in the continued development of advanced materials for next-generation platforms, particularly in the aerospace and naval sectors. The increasing integration of artificial intelligence and automation in defense systems will further necessitate lightweight and sophisticated composite structures. The growing emphasis on sustainability presents an avenue for the development and deployment of eco-friendly composite solutions. The market is expected to witness significant growth fueled by ongoing defense modernization efforts, technological innovation, and strategic collaborations among industry leaders.

US Defense Composites Industry Segmentation

-

1. Application

- 1.1. Manned and Unmanned Aircraft

- 1.2. Naval Ships

- 1.3. Land Vehicles

- 1.4. Protective Equipment

- 1.5. Other Applications

-

2. Resin Type

- 2.1. Thermoset Composites

- 2.2. Thermoplastic Composites

- 2.3. Ceramic Matrix Composites

US Defense Composites Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

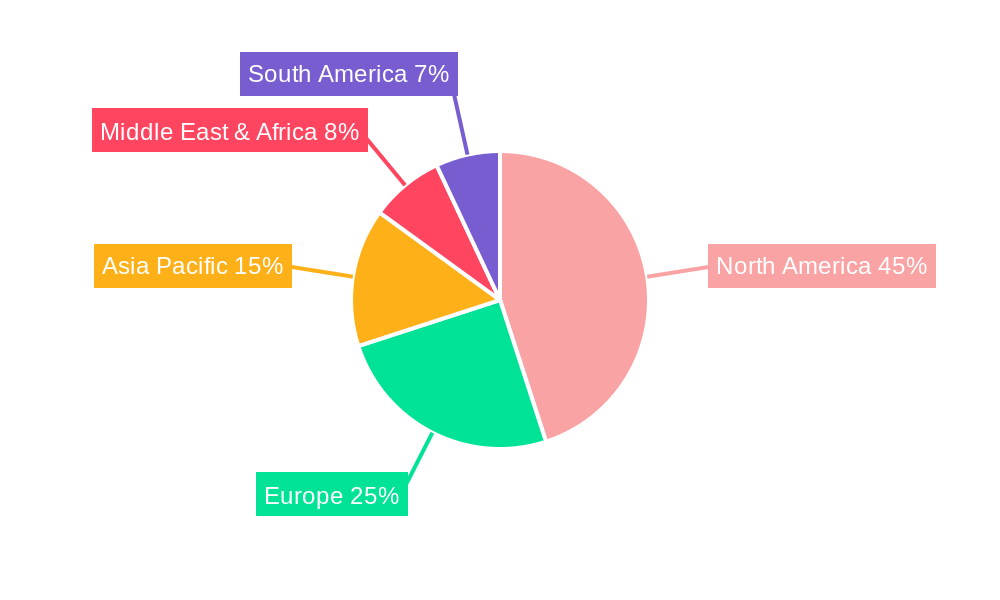

US Defense Composites Industry Regional Market Share

Geographic Coverage of US Defense Composites Industry

US Defense Composites Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.6% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Manned and Unmanned Aircraft

- 5.1.2. Naval Ships

- 5.1.3. Land Vehicles

- 5.1.4. Protective Equipment

- 5.1.5. Other Applications

- 5.2. Market Analysis, Insights and Forecast - by Resin Type

- 5.2.1. Thermoset Composites

- 5.2.2. Thermoplastic Composites

- 5.2.3. Ceramic Matrix Composites

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global US Defense Composites Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Manned and Unmanned Aircraft

- 6.1.2. Naval Ships

- 6.1.3. Land Vehicles

- 6.1.4. Protective Equipment

- 6.1.5. Other Applications

- 6.2. Market Analysis, Insights and Forecast - by Resin Type

- 6.2.1. Thermoset Composites

- 6.2.2. Thermoplastic Composites

- 6.2.3. Ceramic Matrix Composites

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America US Defense Composites Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Manned and Unmanned Aircraft

- 7.1.2. Naval Ships

- 7.1.3. Land Vehicles

- 7.1.4. Protective Equipment

- 7.1.5. Other Applications

- 7.2. Market Analysis, Insights and Forecast - by Resin Type

- 7.2.1. Thermoset Composites

- 7.2.2. Thermoplastic Composites

- 7.2.3. Ceramic Matrix Composites

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America US Defense Composites Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Manned and Unmanned Aircraft

- 8.1.2. Naval Ships

- 8.1.3. Land Vehicles

- 8.1.4. Protective Equipment

- 8.1.5. Other Applications

- 8.2. Market Analysis, Insights and Forecast - by Resin Type

- 8.2.1. Thermoset Composites

- 8.2.2. Thermoplastic Composites

- 8.2.3. Ceramic Matrix Composites

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe US Defense Composites Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Manned and Unmanned Aircraft

- 9.1.2. Naval Ships

- 9.1.3. Land Vehicles

- 9.1.4. Protective Equipment

- 9.1.5. Other Applications

- 9.2. Market Analysis, Insights and Forecast - by Resin Type

- 9.2.1. Thermoset Composites

- 9.2.2. Thermoplastic Composites

- 9.2.3. Ceramic Matrix Composites

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa US Defense Composites Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Manned and Unmanned Aircraft

- 10.1.2. Naval Ships

- 10.1.3. Land Vehicles

- 10.1.4. Protective Equipment

- 10.1.5. Other Applications

- 10.2. Market Analysis, Insights and Forecast - by Resin Type

- 10.2.1. Thermoset Composites

- 10.2.2. Thermoplastic Composites

- 10.2.3. Ceramic Matrix Composites

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific US Defense Composites Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Manned and Unmanned Aircraft

- 11.1.2. Naval Ships

- 11.1.3. Land Vehicles

- 11.1.4. Protective Equipment

- 11.1.5. Other Applications

- 11.2. Market Analysis, Insights and Forecast - by Resin Type

- 11.2.1. Thermoset Composites

- 11.2.2. Thermoplastic Composites

- 11.2.3. Ceramic Matrix Composites

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Honeywell International Inc

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 ACT Aerospace

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Toray Industries Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 The NORDAM Group LL

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Terma AS

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Advanced Composites Inc

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Leading Technology Composites Inc (LTC)

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Huntsman International LLC

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 LMI AEROSPACE

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 DuPont

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 Solvay SA

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 CFOAM LLC

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Hexcel Corporation

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Alpine Advanced Materials

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 Sherwood Advanced Composite Technologies

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.1 Honeywell International Inc

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global US Defense Composites Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America US Defense Composites Industry Revenue (billion), by Application 2025 & 2033

- Figure 3: North America US Defense Composites Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America US Defense Composites Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 5: North America US Defense Composites Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 6: North America US Defense Composites Industry Revenue (billion), by Country 2025 & 2033

- Figure 7: North America US Defense Composites Industry Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America US Defense Composites Industry Revenue (billion), by Application 2025 & 2033

- Figure 9: South America US Defense Composites Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America US Defense Composites Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 11: South America US Defense Composites Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 12: South America US Defense Composites Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: South America US Defense Composites Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe US Defense Composites Industry Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe US Defense Composites Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe US Defense Composites Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 17: Europe US Defense Composites Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 18: Europe US Defense Composites Industry Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe US Defense Composites Industry Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa US Defense Composites Industry Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa US Defense Composites Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa US Defense Composites Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 23: Middle East & Africa US Defense Composites Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 24: Middle East & Africa US Defense Composites Industry Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa US Defense Composites Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific US Defense Composites Industry Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific US Defense Composites Industry Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific US Defense Composites Industry Revenue (billion), by Resin Type 2025 & 2033

- Figure 29: Asia Pacific US Defense Composites Industry Revenue Share (%), by Resin Type 2025 & 2033

- Figure 30: Asia Pacific US Defense Composites Industry Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific US Defense Composites Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global US Defense Composites Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global US Defense Composites Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 3: Global US Defense Composites Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global US Defense Composites Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global US Defense Composites Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 6: Global US Defense Composites Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global US Defense Composites Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global US Defense Composites Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 12: Global US Defense Composites Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global US Defense Composites Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global US Defense Composites Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 18: Global US Defense Composites Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global US Defense Composites Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global US Defense Composites Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 30: Global US Defense Composites Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global US Defense Composites Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global US Defense Composites Industry Revenue billion Forecast, by Resin Type 2020 & 2033

- Table 39: Global US Defense Composites Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific US Defense Composites Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the US Defense Composites Industry?

The projected CAGR is approximately 5.6%.

2. Which companies are prominent players in the US Defense Composites Industry?

Key companies in the market include Honeywell International Inc, ACT Aerospace, Toray Industries Inc, The NORDAM Group LL, Terma AS, Advanced Composites Inc, Leading Technology Composites Inc (LTC), Huntsman International LLC, LMI AEROSPACE, DuPont, Solvay SA, CFOAM LLC, Hexcel Corporation, Alpine Advanced Materials, Sherwood Advanced Composite Technologies.

3. What are the main segments of the US Defense Composites Industry?

The market segments include Application, Resin Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 10.3 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

The Thermoplastic Composites Segment is Expected to Register the Highest Growth Rate During the Forecast Period.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "US Defense Composites Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the US Defense Composites Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the US Defense Composites Industry?

To stay informed about further developments, trends, and reports in the US Defense Composites Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence