Key Insights

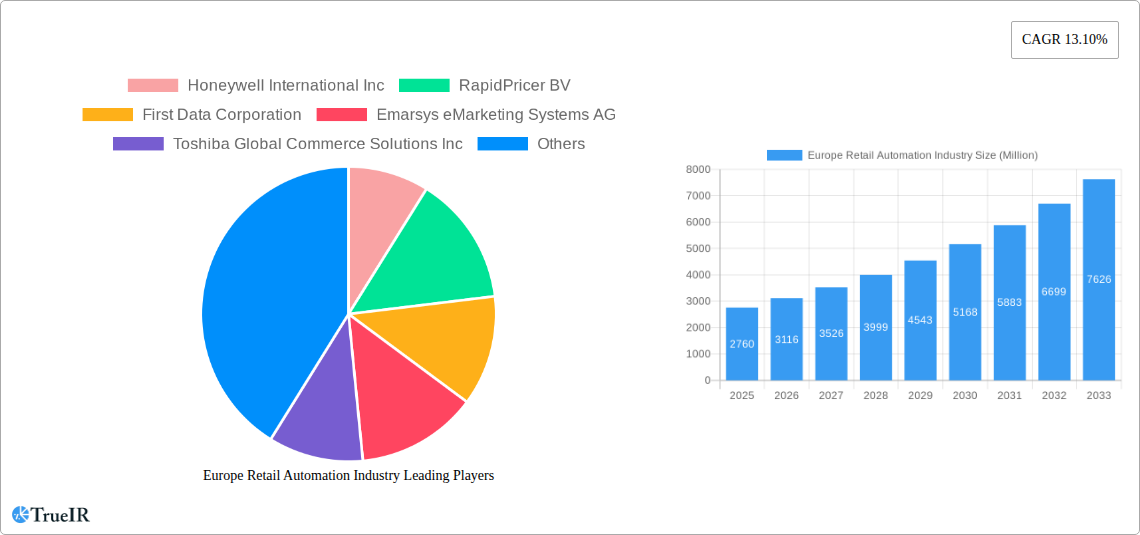

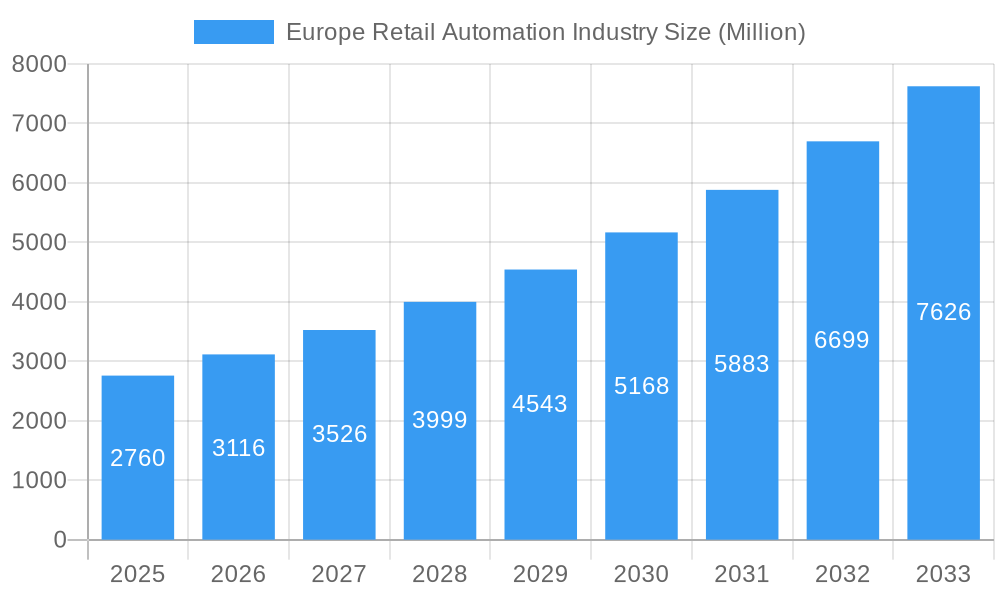

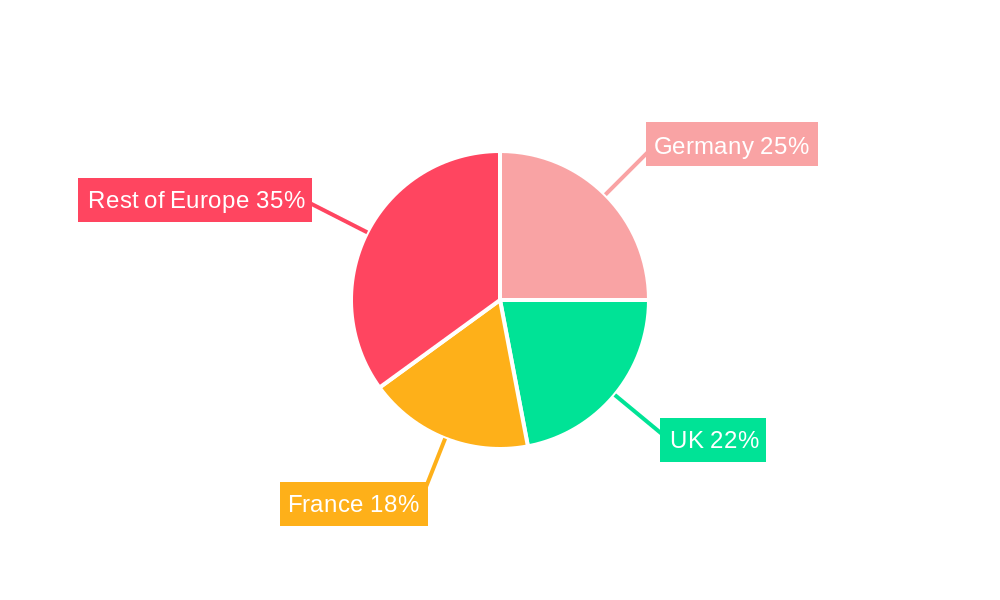

The European retail automation market, valued at €2.76 billion in 2025, is experiencing robust growth, projected to expand at a compound annual growth rate (CAGR) of 13.10% from 2025 to 2033. This surge is driven by several key factors. The increasing need for enhanced operational efficiency and reduced labor costs within the retail sector is a primary driver. Retailers are increasingly adopting automated solutions, such as self-checkout kiosks, inventory management systems, and automated pricing tools, to improve customer experience, streamline operations, and gain a competitive edge. Furthermore, the rising adoption of omnichannel strategies and the need for seamless integration between online and offline retail experiences is fueling demand for sophisticated automation systems. The integration of artificial intelligence (AI) and machine learning (ML) in retail automation is also a significant trend, enabling predictive analytics, personalized customer service, and optimized supply chain management. While initial investment costs can be a restraint, the long-term return on investment (ROI) associated with improved efficiency and reduced operational expenses makes automation increasingly attractive. The market is segmented by end-user (grocery, general merchandise, hospitality), geography (United Kingdom, Germany, France, Rest of Europe), and type (hardware, software). Germany, the UK, and France represent the largest national markets, fueled by robust retail sectors and early adoption of automation technologies. Major players like Honeywell, RapidPricer, NCR, and Zebra Technologies are driving innovation and market competition, continuously developing advanced solutions to meet evolving retail needs.

Europe Retail Automation Industry Market Size (In Billion)

The projected growth trajectory suggests a significant market expansion over the forecast period. The strong CAGR indicates a consistent increase in investment in retail automation across diverse retail segments. The ongoing technological advancements and increasing focus on enhancing customer experiences will further propel market growth. However, potential challenges include the need for robust cybersecurity measures to protect sensitive customer and business data, and the requirement for skilled labor to implement and maintain complex automation systems. Nevertheless, the overall outlook for the European retail automation market remains positive, with significant opportunities for growth and innovation in the coming years. The continued focus on improving efficiency, optimizing operations, and enhancing customer experience will ensure the sustained adoption of automation technologies within the European retail landscape.

Europe Retail Automation Industry Company Market Share

This dynamic report provides a detailed analysis of the Europe Retail Automation Industry, offering invaluable insights for businesses, investors, and stakeholders seeking to navigate this rapidly evolving market. The report covers the period 2019-2033, with a focus on the estimated year 2025 and a forecast period of 2025-2033. Expect comprehensive data and analysis across key segments, including hardware, software, and end-user applications. The market is projected to reach xx Million by 2033, exhibiting significant growth potential.

Europe Retail Automation Industry Market Structure & Competitive Landscape

The European retail automation market is characterized by a moderately concentrated landscape with several major players holding significant market share. While precise concentration ratios require detailed competitive analysis which is not included in this brief, the presence of multinational corporations like Honeywell International Inc and NCR Corporation indicates a degree of consolidation. However, the market also accommodates numerous smaller, specialized companies focusing on niche segments and innovative technologies.

Innovation Drivers: Technological advancements like AI, IoT, and robotics are primary drivers, pushing automation across various retail functions. The demand for enhanced efficiency, improved customer experience, and optimized supply chain management further accelerates market growth.

Regulatory Impacts: EU regulations concerning data privacy (GDPR), worker safety, and environmental sustainability impact market development. Compliance costs and evolving regulations create both challenges and opportunities for innovation.

Product Substitutes: While automation solutions directly improve processes, indirect substitutes include manual labor, although the ongoing labor shortages in Europe increasingly favors automation solutions.

End-User Segmentation: The market is segmented by end-user industries, predominantly encompassing grocery, general merchandise, and hospitality. Each segment exhibits specific automation needs and adoption rates.

M&A Trends: The industry has witnessed significant merger and acquisition activity in recent years. While exact figures are not available for inclusion in this summary, the trend suggests consolidation and expansion into new markets driven by technology-acquisition strategies. The overall deal value during 2019–2024 is estimated to be around xx Million.

Europe Retail Automation Industry Market Trends & Opportunities

The European retail automation market is experiencing substantial growth, driven by a confluence of factors. Market size experienced a CAGR of xx% during the historical period (2019-2024) and is projected to maintain a healthy CAGR of xx% during the forecast period (2025-2033), reaching an estimated xx Million by 2033. This growth reflects the increasing adoption of automation technologies across various retail segments.

Technological shifts, such as the integration of AI and cloud computing, are enabling more sophisticated automation solutions, improving efficiency and customer experience. Consumer preferences for seamless and personalized shopping experiences are also driving demand. The intensified competition among retailers fuels investments in automation to gain a competitive edge.

Dominant Markets & Segments in Europe Retail Automation Industry

The UK, Germany, and France represent the largest national markets within Europe for retail automation, driven by factors such as established retail infrastructure, higher disposable incomes, and technological advancements. The "Rest of Europe" segment also shows significant growth potential.

- By End User: Grocery stores lead in automation adoption, followed closely by general merchandise retailers. The hospitality sector is showing increasing interest.

- By Country: The UK holds a leading position due to high retail density and technological adoption, followed by Germany and France.

- By Type: Hardware solutions currently dominate the market. However, the software segment is experiencing rapid growth due to advancements in AI and data analytics.

Key Growth Drivers:

- Strong retail infrastructure supporting seamless technology integration.

- Government initiatives and funding for digital transformation in the retail sector.

- Increasing consumer demand for efficient and personalized shopping experiences.

Europe Retail Automation Industry Product Analysis

The market offers a wide range of automated solutions, including self-checkout kiosks, inventory management systems, robotic process automation (RPA), and AI-powered analytics platforms. Technological advancements focus on enhancing user experience, streamlining operations, and optimizing resource allocation, improving efficiency, and reducing costs, making these solutions attractive to retailers.

Key Drivers, Barriers & Challenges in Europe Retail Automation Industry

Key Drivers: The primary drivers include labor shortages, the need for enhanced efficiency and cost optimization, and the rising demand for personalized customer experiences. Technological advancements in AI, robotics, and IoT are also crucial drivers.

Challenges and Restraints: High initial investment costs, concerns about job displacement, data security and privacy issues, and integration complexities pose significant challenges. Supply chain disruptions and regulatory uncertainties further impact market growth. The impact of these restraints is estimated to reduce overall market growth by approximately xx% by 2033.

Growth Drivers in the Europe Retail Automation Industry Market

The key drivers for growth are similar to the ones mentioned above: labor shortages, the push for operational efficiency, and the pursuit of personalized customer experiences. Technological innovation, especially in AI and robotics, remains a potent catalyst for expansion. The positive regulatory environment in some European countries also fosters growth.

Challenges Impacting Europe Retail Automation Industry Growth

Significant hurdles include the high upfront costs of implementing automation solutions, the need for skilled labor for integration and maintenance, and ongoing concerns regarding data security and privacy. Regulatory complexities and potential supply chain disruptions remain further obstacles.

Key Players Shaping the Europe Retail Automation Industry Market

- Honeywell International Inc

- RapidPricer BV

- First Data Corporation

- Emarsys eMarketing Systems AG

- Toshiba Global Commerce Solutions Inc

- NCR Corporation

- Fujitsu Limited

- Zebra Technologies Corp

- Diebold Nixdorf Incorporated

- Datalogic SpA

Significant Europe Retail Automation Industry Industry Milestones

- November 2022: Adapta Robotics and Carrefour launched ERIS, a retail robot for inventory management in Romania.

- November 2022: Pudu Robotics and Carrefour trialled BellaBot (Kerfus) for delivery services in Poland, resulting in increased sales.

- January 2023: Currys partnered with UX Global to trial KettyBot, a customer assistance robot in the UK.

Future Outlook for Europe Retail Automation Industry Market

The future outlook for the European retail automation market is extremely positive. Continued technological advancements, the increasing adoption of AI and robotics across diverse retail operations, and the need for enhanced operational efficiencies will collectively propel market expansion. Strategic partnerships, acquisitions, and the development of innovative solutions will further shape the market's trajectory in the coming years. This translates to robust growth potential, creating various opportunities for existing players and new entrants alike.

Europe Retail Automation Industry Segmentation

-

1. Type

-

1.1. Hardware

- 1.1.1. POS System

- 1.1.2. Self-checkout System

- 1.1.3. RFID and Barcode Scanners

- 1.1.4. Other Hardware Types

- 1.2. Software

-

1.1. Hardware

-

2. End User

- 2.1. Grocery

- 2.2. General Merchandise

- 2.3. Hospitality

Europe Retail Automation Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Retail Automation Industry Regional Market Share

Geographic Coverage of Europe Retail Automation Industry

Europe Retail Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.10% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Demand for Quality and Fast Service; Automated Technologies Being More Widely Used in the Retail Business

- 3.3. Market Restrains

- 3.3.1. Technical and Security Concerns

- 3.4. Market Trends

- 3.4.1. Grocery Retailers are Expected to Hold a Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Retail Automation Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Hardware

- 5.1.1.1. POS System

- 5.1.1.2. Self-checkout System

- 5.1.1.3. RFID and Barcode Scanners

- 5.1.1.4. Other Hardware Types

- 5.1.2. Software

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Grocery

- 5.2.2. General Merchandise

- 5.2.3. Hospitality

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Honeywell International Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 RapidPricer BV

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 First Data Corporation

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Emarsys eMarketing Systems AG

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Toshiba Global Commerce Solutions Inc

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 NCR Corporation

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Fujitsu Limited

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Zebra Technologies Corp

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Diebold Nixdorf Incorporated

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Datalogic SpA

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Honeywell International Inc

List of Figures

- Figure 1: Europe Retail Automation Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Retail Automation Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Retail Automation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: Europe Retail Automation Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 3: Europe Retail Automation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Europe Retail Automation Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: Europe Retail Automation Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 6: Europe Retail Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: France Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Retail Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Retail Automation Industry?

The projected CAGR is approximately 13.10%.

2. Which companies are prominent players in the Europe Retail Automation Industry?

Key companies in the market include Honeywell International Inc, RapidPricer BV, First Data Corporation, Emarsys eMarketing Systems AG, Toshiba Global Commerce Solutions Inc, NCR Corporation, Fujitsu Limited, Zebra Technologies Corp, Diebold Nixdorf Incorporated, Datalogic SpA.

3. What are the main segments of the Europe Retail Automation Industry?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 2.76 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Demand for Quality and Fast Service; Automated Technologies Being More Widely Used in the Retail Business.

6. What are the notable trends driving market growth?

Grocery Retailers are Expected to Hold a Significant Market Share.

7. Are there any restraints impacting market growth?

Technical and Security Concerns.

8. Can you provide examples of recent developments in the market?

January 2023 - Currys, the UK-based retailer, partnered with a digital display specialist UX Global (UXG), to trial KettyBot, the robot for customer assistance. China's Pudu Robotics develops KettyBot. The robot will significantly help customers who know what they want but need a little assistance finding it in the store. This way, customers will save time while enhancing their in-store experience.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Retail Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Retail Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Retail Automation Industry?

To stay informed about further developments, trends, and reports in the Europe Retail Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence