Key Insights

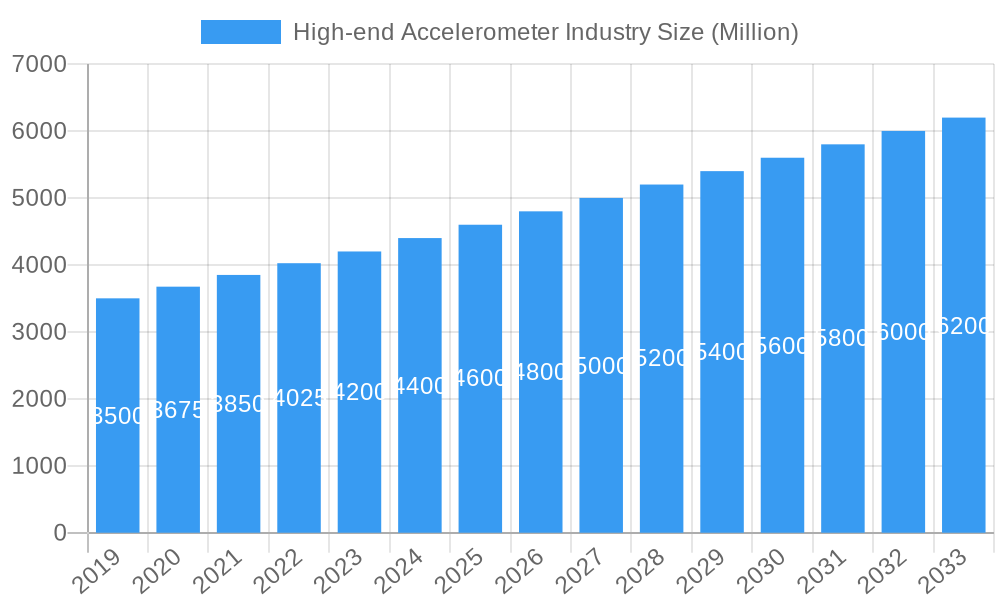

The High-end Accelerometer market is projected to experience substantial growth, reaching an estimated <7.92 billion> by 2033, with a Compound Annual Growth Rate (CAGR) of <9.8%> from the base year <2025>. Key drivers include the escalating demand for high-precision measurement in industrial automation, the critical requirements for advanced navigation and guidance in defense and aerospace, and the burgeoning need for enhanced safety and autonomous capabilities in the automotive sector. These high-end accelerometers, renowned for their superior accuracy, reliability, and performance under demanding conditions, are increasingly integral to these vital industries. Ongoing advancements in sensor technology, miniaturization, and performance optimization are further accelerating market adoption.

High-end Accelerometer Industry Market Size (In Billion)

The market is segmented across diverse applications, including industrial automation, defense, aerospace, land/naval systems, tactical, navigation, industrial and mining, and automotive sectors. Prominent industry leaders such as Rockwell Collins Inc., Moog Inc., Thales Group, and Honeywell Aerospace Inc. are spearheading the development and provision of these sophisticated solutions. While significant growth is anticipated, challenges such as elevated development costs and integration complexities may present hurdles. Nevertheless, the pervasive drive towards greater automation, sophisticated control systems, and the continuous pursuit of superior performance across numerous industries are expected to propel the high-end accelerometer market forward.

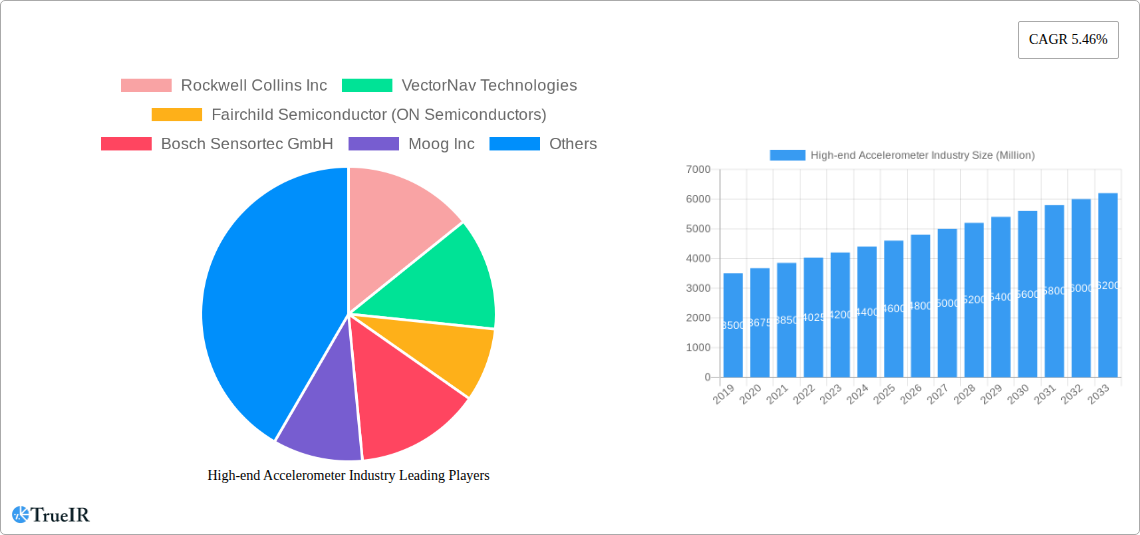

High-end Accelerometer Industry Company Market Share

This in-depth report examines the dynamic High-end Accelerometer industry, analyzing market drivers, key stakeholders, and future trajectories. The analysis covers historical trends from 2019 to 2024, with the <2025> serving as the base year, and forecasts market expansion, technological innovations, and emerging opportunities from 2025 to 2033.

High-end Accelerometer Industry Market Structure & Competitive Landscape

The high-end accelerometer market exhibits a moderate to high level of concentration, driven by significant R&D investments and stringent performance requirements. Key innovation drivers include miniaturization, enhanced accuracy, reduced power consumption, and increased environmental resilience for demanding applications. Regulatory impacts, particularly in aerospace and defense, mandate rigorous testing and certification, creating barriers to entry for new players. Product substitutes, such as gyroscopes and IMUs (Inertial Measurement Units) that integrate accelerometers, influence market positioning. End-user segmentation across industrial applications, defense, aerospace, and land/naval sectors dictates specific product development and marketing strategies. Merger and acquisition (M&A) trends are prevalent, with companies like Honeywell Aerospace Inc and Northrop Grumman Corporation engaging in strategic consolidations to expand their portfolios and market reach. M&A volumes in the historical period (2019-2024) are estimated to be in the hundreds of millions, reflecting a consolidating market. Concentration ratios for the top players are estimated to be between 60-70%.

High-end Accelerometer Industry Market Trends & Opportunities

The high-end accelerometer market is poised for significant expansion, projected to reach a market size of over $5 Billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 7.5% during the forecast period (2025–2033). This robust growth is fueled by increasing demand for precision sensing solutions in critical sectors. Technological shifts are central to this upward trajectory, with advancements in MEMS (Micro-Electro-Mechanical Systems) technology leading to smaller, more power-efficient, and highly accurate accelerometers. The integration of high-end accelerometers into complex systems for navigation, guidance, and control in aerospace and defense platforms is a primary growth catalyst. Consumer preferences, while less direct in the high-end segment, influence broader technological trends, pushing for greater integration and higher performance. Competitive dynamics are characterized by a focus on advanced feature sets, reliability, and customized solutions. The market penetration rate for advanced high-end accelerometers in specialized industrial and defense applications is steadily increasing, driven by the imperative for enhanced operational efficiency and safety. Emerging opportunities lie in the development of next-generation inertial sensing technologies, including fiber optic gyroscopes integrated with accelerometers, and advancements in quantum sensing for unparalleled accuracy. The increasing complexity of autonomous systems in both defense and industrial automation further amplifies the demand for sophisticated high-end accelerometer solutions. The automotive sector, while historically dominated by lower-end accelerometers, is witnessing an increasing adoption of higher-fidelity sensors for advanced driver-assistance systems (ADAS) and autonomous driving, representing a nascent but promising growth avenue. Furthermore, the growing emphasis on predictive maintenance in industrial settings, utilizing vibration analysis enabled by accurate accelerometers, opens up substantial market potential. The defense sector's continuous need for advanced navigation and targeting systems, coupled with the aerospace industry's stringent safety and performance requirements, will continue to be the bedrock of market growth.

Dominant Markets & Segments in High-end Accelerometer Industry

The Defense segment is a dominant market within the High-end Accelerometer Industry, driven by continuous innovation and substantial government investment in advanced military technologies. This segment includes applications such as missile guidance systems, aircraft navigation, unmanned aerial vehicles (UAVs), and naval vessel stabilization. The Aerospace segment also holds significant market share, with high-end accelerometers crucial for aircraft flight control systems, navigation, structural health monitoring, and satellite orientation. The inherent need for extreme reliability, accuracy, and resilience to harsh environments in these sectors positions them as key growth drivers.

Within the broader High-end(Industrial Applications, Defense, Aerospace, Land/Naval) segmentation:

- Defense: Key growth drivers include evolving geopolitical landscapes, increasing defense budgets in major economies, and the demand for superior situational awareness and precision targeting. Government policies supporting domestic defense manufacturing and R&D further bolster this segment.

- Aerospace: Growth is propelled by the increasing demand for commercial aircraft, the expansion of space exploration initiatives, and the development of next-generation defense aircraft. Stringent safety regulations and the pursuit of fuel efficiency necessitate advanced sensing capabilities.

- Industrial Applications: This segment encompasses critical sectors like oil and gas exploration, mining, civil engineering, and advanced manufacturing. Growth is driven by the need for accurate monitoring of equipment health, precise control in automated processes, and robust navigation in challenging terrains.

- Land/Naval: Applications include vehicle navigation, robotics, seismic monitoring, and the stabilization of naval vessels. Infrastructure development and the increasing automation of logistics and transportation further contribute to growth.

The High-end(Tactical, Navigation, Industrial and Mining, Automotive) segmentation also reveals key trends:

- Navigation: High-end accelerometers are indispensable for inertial navigation systems (INS) that provide accurate positioning and orientation data, independent of external signals like GPS, especially in denied environments.

- Tactical: This segment is crucial for precision-guided munitions, reconnaissance systems, and battlefield management, demanding rapid response and high accuracy.

- Industrial and Mining: The robust nature and high precision of high-end accelerometers make them ideal for monitoring vibration, inclination, and motion in heavy machinery, ensuring operational efficiency and safety.

- Automotive: While previously a lower-end segment, the increasing sophistication of ADAS and the advent of autonomous driving are driving the adoption of higher-fidelity accelerometers for precise motion sensing and control.

The high-end accelerometer industry is expected to see continued dominance from applications requiring the utmost precision and reliability, with Defense and Aerospace segments leading market share, followed by sophisticated industrial and emerging automotive applications.

High-end Accelerometer Industry Product Analysis

Product innovation in the high-end accelerometer industry centers on enhancing sensitivity, reducing noise, improving bandwidth, and miniaturization. Companies are developing accelerometers with resolutions in the micro-g range and bandwidths extending to tens of kHz, crucial for precise vibration analysis and inertial navigation. Competitive advantages stem from superior performance specifications, integration capabilities with other sensors (IMUs), and ruggedized designs for extreme environments. Advanced materials and fabrication techniques are enabling smaller form factors and lower power consumption, expanding application possibilities in portable devices and space-constrained systems. Market fit is achieved through tailored solutions for the stringent requirements of the aerospace, defense, and industrial sectors.

Key Drivers, Barriers & Challenges in High-end Accelerometer Industry

Key Drivers:

- Technological Advancements: Miniaturization of MEMS, increased accuracy, and reduced power consumption are propelling adoption.

- Growing Defense & Aerospace Spending: Continued investment in advanced navigation, guidance, and control systems.

- Industrial Automation & IoT: Demand for precise motion sensing in robotics, predictive maintenance, and smart manufacturing.

- Autonomous Systems: Essential for navigation and control in self-driving vehicles and drones.

Barriers & Challenges:

- High R&D Costs: Significant investment required for developing cutting-edge accelerometer technology.

- Stringent Certification Requirements: Especially in aerospace and defense, leading to long development cycles and high costs.

- Supply Chain Volatility: Potential disruptions in the supply of specialized components and raw materials.

- Intense Competition: From established players and emerging technologies, driving price pressures.

Growth Drivers in the High-end Accelerometer Industry Market

The high-end accelerometer industry is primarily propelled by relentless technological innovation, with advancements in MEMS enabling smaller, more accurate, and power-efficient sensors. Economic factors, such as increasing global defense expenditure and investment in infrastructure projects, significantly boost demand. Regulatory drivers, particularly in aerospace and defense, mandate the use of high-reliability components, further stimulating growth. The burgeoning adoption of autonomous systems across various sectors, from automotive to industrial robotics, is a critical catalyst.

Challenges Impacting High-end Accelerometer Industry Growth

The high-end accelerometer industry faces several challenges that can impact growth. Regulatory complexities, particularly stringent certification processes for aerospace and defense applications, extend product development timelines and increase costs. Supply chain disruptions, ranging from raw material shortages to geopolitical influences, can affect production and delivery schedules. Competitive pressures are intense, with both established players and new entrants vying for market share, leading to potential price erosion. The high cost of advanced accelerometer technology can also act as a barrier to adoption in price-sensitive applications.

Key Players Shaping the High-end Accelerometer Industry Market

- Analog Devices Inc

- Bosch Sensortec GmbH

- Fairchild Semiconductor (ON Semiconductors)

- Honeywell Aerospace Inc

- Moog Inc

- Northrop Grumman Corporation

- Rockwell Collins Inc

- Safran Group (SAGEM)

- STMicroelectronics NV

- Thales Group

- VectorNav Technologies

Significant High-end Accelerometer Industry Industry Milestones

- 2019: Launch of next-generation inertial measurement units with enhanced accelerometer performance by key players.

- 2020: Increased adoption of ruggedized accelerometers in defense applications due to evolving geopolitical situations.

- 2021: Advancements in MEMS technology leading to micro-g resolution accelerometers becoming more accessible.

- 2022: Growing demand for accelerometers in industrial IoT for predictive maintenance solutions.

- 2023: Significant R&D investments by major companies focusing on quantum-grade accelerometer technology.

- 2024: Increased M&A activity as companies seek to consolidate market share and expand product portfolios.

Future Outlook for High-end Accelerometer Industry Market

The high-end accelerometer industry is projected for sustained growth, driven by an insatiable demand for precision sensing in defense, aerospace, and advanced industrial applications. Future opportunities lie in the development of even more compact, power-efficient, and highly accurate sensors, including those leveraging quantum technologies for unparalleled performance. The expansion of autonomous systems and the increasing complexity of modern machinery will continue to fuel the need for sophisticated inertial measurement solutions, ensuring a robust market outlook.

High-end Accelerometer Industry Segmentation

-

1. Type

-

1.1. High-end

- 1.1.1. Industrial Applications

- 1.1.2. Defense

- 1.1.3. Aerospace

- 1.1.4. Land/Naval

-

1.2. High-end

- 1.2.1. Tactical

- 1.2.2. Navigation

- 1.2.3. Industrial and Mining

- 1.2.4. Automotive

- 1.3. High-end

-

1.1. High-end

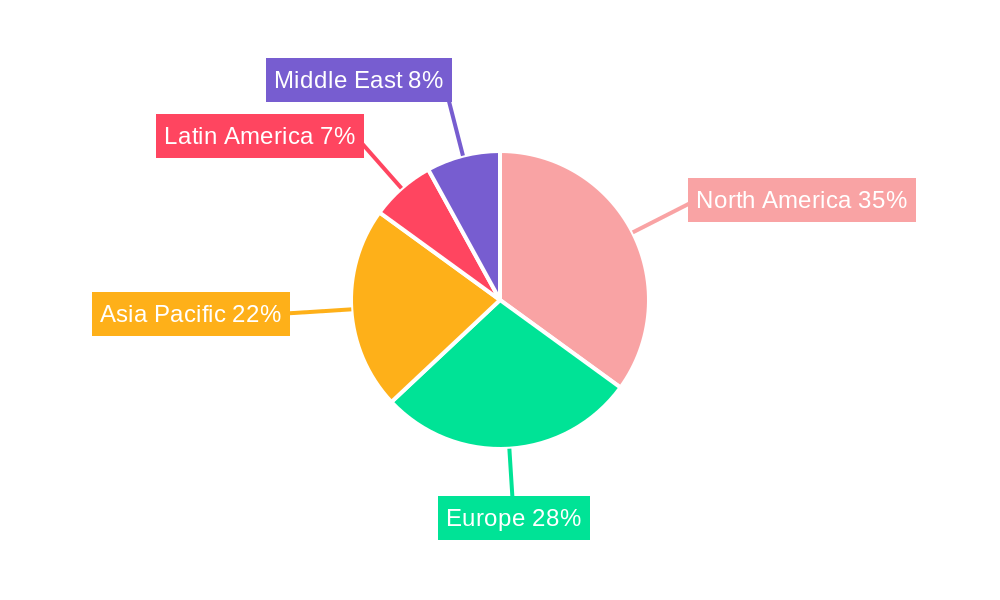

High-end Accelerometer Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East

High-end Accelerometer Industry Regional Market Share

Geographic Coverage of High-end Accelerometer Industry

High-end Accelerometer Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Emergence of MEMS Technology; Inclination of Growth toward Defense and Aerospace; Technological Advancements in Navigation Systems

- 3.3. Market Restrains

- 3.3.1 ; Operational Complexity

- 3.3.2 coupled with High Maintenance Costs

- 3.4. Market Trends

- 3.4.1. High-end Inertial Measurement Units is Expected to Hold Major Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global High-end Accelerometer Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. High-end

- 5.1.1.1. Industrial Applications

- 5.1.1.2. Defense

- 5.1.1.3. Aerospace

- 5.1.1.4. Land/Naval

- 5.1.2. High-end

- 5.1.2.1. Tactical

- 5.1.2.2. Navigation

- 5.1.2.3. Industrial and Mining

- 5.1.2.4. Automotive

- 5.1.3. High-end

- 5.1.1. High-end

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Asia Pacific

- 5.2.4. Latin America

- 5.2.5. Middle East

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America High-end Accelerometer Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. High-end

- 6.1.1.1. Industrial Applications

- 6.1.1.2. Defense

- 6.1.1.3. Aerospace

- 6.1.1.4. Land/Naval

- 6.1.2. High-end

- 6.1.2.1. Tactical

- 6.1.2.2. Navigation

- 6.1.2.3. Industrial and Mining

- 6.1.2.4. Automotive

- 6.1.3. High-end

- 6.1.1. High-end

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Europe High-end Accelerometer Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. High-end

- 7.1.1.1. Industrial Applications

- 7.1.1.2. Defense

- 7.1.1.3. Aerospace

- 7.1.1.4. Land/Naval

- 7.1.2. High-end

- 7.1.2.1. Tactical

- 7.1.2.2. Navigation

- 7.1.2.3. Industrial and Mining

- 7.1.2.4. Automotive

- 7.1.3. High-end

- 7.1.1. High-end

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Asia Pacific High-end Accelerometer Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. High-end

- 8.1.1.1. Industrial Applications

- 8.1.1.2. Defense

- 8.1.1.3. Aerospace

- 8.1.1.4. Land/Naval

- 8.1.2. High-end

- 8.1.2.1. Tactical

- 8.1.2.2. Navigation

- 8.1.2.3. Industrial and Mining

- 8.1.2.4. Automotive

- 8.1.3. High-end

- 8.1.1. High-end

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Latin America High-end Accelerometer Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. High-end

- 9.1.1.1. Industrial Applications

- 9.1.1.2. Defense

- 9.1.1.3. Aerospace

- 9.1.1.4. Land/Naval

- 9.1.2. High-end

- 9.1.2.1. Tactical

- 9.1.2.2. Navigation

- 9.1.2.3. Industrial and Mining

- 9.1.2.4. Automotive

- 9.1.3. High-end

- 9.1.1. High-end

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Middle East High-end Accelerometer Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. High-end

- 10.1.1.1. Industrial Applications

- 10.1.1.2. Defense

- 10.1.1.3. Aerospace

- 10.1.1.4. Land/Naval

- 10.1.2. High-end

- 10.1.2.1. Tactical

- 10.1.2.2. Navigation

- 10.1.2.3. Industrial and Mining

- 10.1.2.4. Automotive

- 10.1.3. High-end

- 10.1.1. High-end

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Rockwell Collins Inc

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 VectorNav Technologies

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Fairchild Semiconductor (ON Semiconductors)

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Bosch Sensortec GmbH

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Moog Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Thales Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 STMicroelectronics NV

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Safran Group (SAGEM

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Analog Devices Inc

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Honeywell Aerospace Inc

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Northrop Grumman Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Rockwell Collins Inc

List of Figures

- Figure 1: Global High-end Accelerometer Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America High-end Accelerometer Industry Revenue (billion), by Type 2025 & 2033

- Figure 3: North America High-end Accelerometer Industry Revenue Share (%), by Type 2025 & 2033

- Figure 4: North America High-end Accelerometer Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: North America High-end Accelerometer Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe High-end Accelerometer Industry Revenue (billion), by Type 2025 & 2033

- Figure 7: Europe High-end Accelerometer Industry Revenue Share (%), by Type 2025 & 2033

- Figure 8: Europe High-end Accelerometer Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: Europe High-end Accelerometer Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Asia Pacific High-end Accelerometer Industry Revenue (billion), by Type 2025 & 2033

- Figure 11: Asia Pacific High-end Accelerometer Industry Revenue Share (%), by Type 2025 & 2033

- Figure 12: Asia Pacific High-end Accelerometer Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Asia Pacific High-end Accelerometer Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Latin America High-end Accelerometer Industry Revenue (billion), by Type 2025 & 2033

- Figure 15: Latin America High-end Accelerometer Industry Revenue Share (%), by Type 2025 & 2033

- Figure 16: Latin America High-end Accelerometer Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: Latin America High-end Accelerometer Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East High-end Accelerometer Industry Revenue (billion), by Type 2025 & 2033

- Figure 19: Middle East High-end Accelerometer Industry Revenue Share (%), by Type 2025 & 2033

- Figure 20: Middle East High-end Accelerometer Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East High-end Accelerometer Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global High-end Accelerometer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Global High-end Accelerometer Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global High-end Accelerometer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 4: Global High-end Accelerometer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: Global High-end Accelerometer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 6: Global High-end Accelerometer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 7: Global High-end Accelerometer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Global High-end Accelerometer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 9: Global High-end Accelerometer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 10: Global High-end Accelerometer Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 11: Global High-end Accelerometer Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 12: Global High-end Accelerometer Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the High-end Accelerometer Industry?

The projected CAGR is approximately 9.8%.

2. Which companies are prominent players in the High-end Accelerometer Industry?

Key companies in the market include Rockwell Collins Inc, VectorNav Technologies, Fairchild Semiconductor (ON Semiconductors), Bosch Sensortec GmbH, Moog Inc, Thales Group, STMicroelectronics NV, Safran Group (SAGEM, Analog Devices Inc, Honeywell Aerospace Inc, Northrop Grumman Corporation.

3. What are the main segments of the High-end Accelerometer Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.92 billion as of 2022.

5. What are some drivers contributing to market growth?

; Emergence of MEMS Technology; Inclination of Growth toward Defense and Aerospace; Technological Advancements in Navigation Systems.

6. What are the notable trends driving market growth?

High-end Inertial Measurement Units is Expected to Hold Major Share.

7. Are there any restraints impacting market growth?

; Operational Complexity. coupled with High Maintenance Costs.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "High-end Accelerometer Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the High-end Accelerometer Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the High-end Accelerometer Industry?

To stay informed about further developments, trends, and reports in the High-end Accelerometer Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence