Key Insights

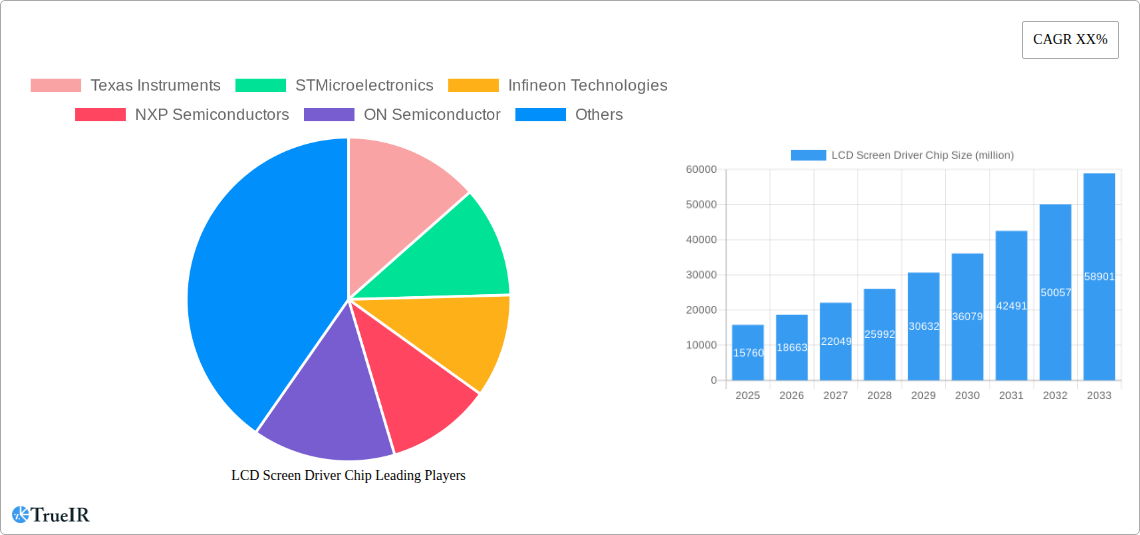

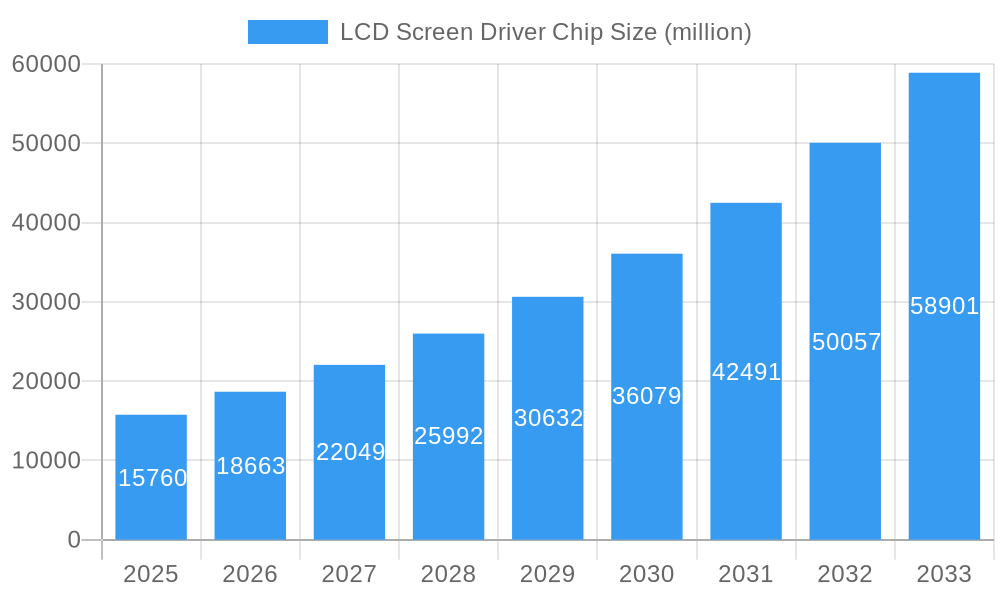

The global LCD Screen Driver Chip market is poised for substantial expansion, projected to reach an estimated $15.76 billion in 2025. This growth is fueled by a robust CAGR of 18.5% anticipated over the forecast period. The increasing demand for advanced display technologies across consumer electronics, automotive, and commercial sectors significantly drives this market. Key applications such as Family Entertainment, encompassing smart TVs, gaming consoles, and other interactive home devices, are witnessing accelerated adoption of high-performance LCD driver chips. Furthermore, the Commercial Display segment, which includes digital signage, medical imaging, and industrial monitors, is also a significant contributor, benefiting from the ongoing digital transformation and the need for sophisticated visual interfaces. The evolution towards higher resolutions, faster refresh rates, and improved power efficiency in LCD panels directly translates to a greater demand for innovative and specialized driver chip solutions.

LCD Screen Driver Chip Market Size (In Billion)

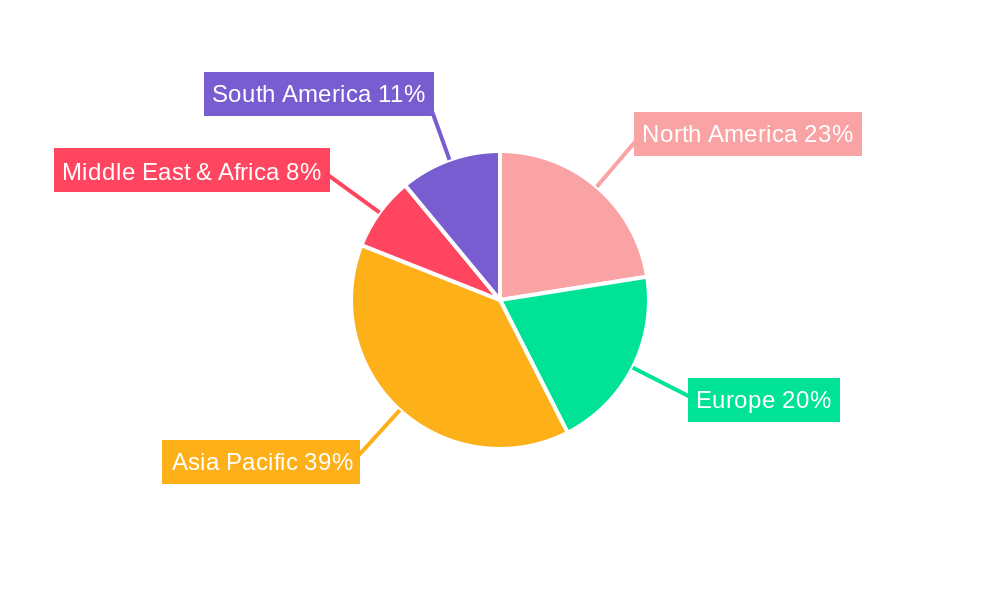

The market's trajectory is further shaped by technological advancements within different types of LCD driver chips, with Dual Channel, Four Channel, and Six Channel configurations catering to a spectrum of display requirements. While growth is robust, certain factors could influence its pace. Supply chain complexities and the rising cost of raw materials might present temporary challenges. However, the relentless pursuit of miniaturization, enhanced integration, and the development of energy-efficient solutions by leading companies like Texas Instruments, STMicroelectronics, and Infineon Technologies are expected to largely mitigate these restraints. The geographical landscape indicates strong market presence and growth in Asia Pacific, driven by its manufacturing prowess and vast consumer base, followed closely by North America and Europe, where technological innovation and premium product adoption are prominent. The continuous innovation in display technology ensures a sustained demand for these crucial components.

LCD Screen Driver Chip Company Market Share

The global LCD screen driver chip market exhibits a moderately concentrated structure, with key players like Texas Instruments, STMicroelectronics, and Infineon Technologies holding significant market share. Innovation remains a primary driver, with constant advancements in resolution, power efficiency, and integration capabilities pushing product development. Regulatory impacts are increasingly influencing manufacturing standards and environmental compliance, particularly concerning hazardous materials and energy consumption. The threat of product substitutes, while present from emerging display technologies like OLED, is mitigated by the established cost-effectiveness and widespread adoption of LCD technology. End-user segmentation reveals a strong reliance on both Family Entertainment and Commercial Display applications, each with unique driver requirements. Mergers and acquisitions (M&A) trends are active, with larger entities consolidating to enhance their product portfolios and expand their geographical reach. For instance, there have been approximately 0.1 billion M&A deals in the past five years, indicating a consolidation drive. Concentration ratios are estimated to be around 60% for the top five players, underscoring the competitive dynamics.

LCD Screen Driver Chip Market Trends & Opportunities

The LCD screen driver chip market is poised for substantial expansion, driven by a confluence of technological innovation, evolving consumer preferences, and the pervasive integration of visual displays across diverse sectors. The market size is projected to reach over $10 billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 6.5% during the forecast period (2025–2033). Technological shifts are a cornerstone of this growth. The increasing demand for higher resolutions, such as 4K and 8K, necessitates sophisticated driver ICs capable of managing a vast number of pixels with precision and speed. Furthermore, advancements in display technologies like mini-LED and micro-LED backlighting are creating new opportunities for specialized driver chips that can offer enhanced brightness, contrast, and power efficiency. Consumer preferences are increasingly leaning towards larger, more immersive display experiences in both home entertainment and mobile devices. This trend fuels the demand for driver chips that can support advanced features like adaptive refresh rates, HDR (High Dynamic Range), and reduced latency for gaming and interactive applications. The competitive landscape is characterized by fierce innovation and strategic partnerships. Companies are investing heavily in research and development to integrate more functionality onto single chips, reducing component count and system costs. This includes the integration of power management ICs, timing controllers, and other peripheral functions alongside the core driver circuitry. The expanding market penetration rates, especially in emerging economies, are a testament to the ubiquitous nature of LCD technology. From smart appliances and automotive displays to industrial control panels and medical equipment, LCD screens are becoming integral to a wide array of products, thereby driving consistent demand for their driver chips. The continuous evolution of display technology, coupled with the insatiable consumer appetite for richer visual experiences, positions the LCD screen driver chip market for sustained and robust growth.

Dominant Markets & Segments in LCD Screen Driver Chip

The Commercial Display segment is a dominant force within the LCD screen driver chip market, driven by the widespread deployment of digital signage, interactive kiosks, and professional displays across retail, corporate, and public spaces. The estimated market share for this segment is projected to be approximately 45% by 2033. Key growth drivers include the ongoing digital transformation initiatives across industries, the increasing need for dynamic and engaging customer experiences, and the development of smart city infrastructure. Government policies supporting digitalization and the adoption of advanced information display systems further bolster this segment. Geographically, North America and Europe currently lead in terms of adoption and technological advancement within commercial displays, though Asia-Pacific is rapidly catching up due to significant investments in retail modernization and smart infrastructure projects.

Within the Application breakdown, Family Entertainment also represents a substantial and growing segment, accounting for an estimated 35% of the market by 2033. This growth is fueled by the proliferation of smart TVs, gaming consoles, and home theater systems. Factors contributing to this dominance include the increasing disposable income, the growing popularity of streaming services, and the desire for immersive home entertainment experiences. Technological advancements that enable higher resolutions, faster refresh rates, and improved color accuracy are critical for this segment.

Regarding Types, the Four Channel driver ICs are experiencing significant traction, holding an estimated 30% of the market by 2033, largely due to their versatility and suitability for a broad range of display sizes and resolutions. Their ability to efficiently drive a substantial number of pixels makes them ideal for mid-range to high-end consumer electronics and commercial displays. The Dual Channel segment, while mature, continues to serve the demand for cost-effective solutions in smaller displays and basic applications, maintaining an estimated 25% market share. The Six Channel and Other categories are expected to grow with specialized applications demanding higher channel counts for ultra-high-resolution or unique display configurations, collectively contributing to the remaining market share. The continuous innovation in driver IC architecture, aiming for higher integration and reduced power consumption, will further shape the dominance of these types in the coming years.

LCD Screen Driver Chip Product Analysis

LCD screen driver chips are at the forefront of visual display technology, enabling the crisp and vibrant images we see daily. Product innovations focus on increasing pixel density support, improving power efficiency for battery-powered devices, and enhancing signal integrity for faster refresh rates and reduced latency. Competitive advantages are gained through superior integration, reducing the bill of materials for manufacturers, and offering advanced features like built-in gamma correction and noise reduction. The market fit for these chips spans from compact smartphone displays to massive commercial video walls, with ongoing development aimed at supporting emerging display technologies and pushing the boundaries of visual fidelity and performance.

Key Drivers, Barriers & Challenges in LCD Screen Driver Chip

Key Drivers, Barriers & Challenges in LCD Screen Driver Chip

Key Drivers:

- Surging Demand for High-Resolution Displays: The relentless pursuit of sharper, more immersive visuals across consumer electronics (smartphones, TVs, gaming) and commercial applications (digital signage, automotive) is a primary growth catalyst.

- Technological Advancements in Display Technologies: Innovations like Mini-LED and Micro-LED backlighting require more advanced and power-efficient driver ICs, creating new market opportunities.

- Growing Automotive Display Market: The increasing integration of sophisticated in-car infotainment and dashboard displays fuels demand for robust and reliable driver chips.

- Expansion of IoT and Smart Devices: The proliferation of smart home devices, wearables, and industrial IoT sensors with embedded displays necessitates a wide range of driver solutions.

Barriers & Challenges:

- Supply Chain Disruptions and Geopolitical Tensions: Semiconductor shortages, trade wars, and logistical challenges can significantly impact production capacity, lead times, and component costs.

- Intensifying Competition and Price Pressures: The highly competitive market, with numerous global players, leads to constant pressure on profit margins and necessitates continuous cost optimization.

- Evolving Regulatory Landscape: Stricter environmental regulations regarding material usage and energy efficiency can impact manufacturing processes and product design.

- Technological Obsolescence: Rapid advancements in display technology, particularly the rise of alternative display types like OLED, pose a long-term threat and require continuous R&D investment to remain competitive.

Growth Drivers in the LCD Screen Driver Chip Market

The LCD screen driver chip market is propelled by several key factors. Technologically, the incessant demand for higher resolutions (4K, 8K) and improved visual quality, such as HDR, drives innovation in chip design for enhanced pixel management and signal processing. Economically, the expanding consumer electronics market, particularly in emerging economies, and the robust growth of the automotive display sector create significant volume opportunities. Government initiatives promoting digitalization and smart infrastructure further stimulate the adoption of LCD displays, thereby increasing the demand for their respective driver chips.

Challenges Impacting LCD Screen Driver Chip Growth

Despite the positive outlook, several challenges impede the growth of the LCD screen driver chip market. Supply chain vulnerabilities, including raw material shortages and geopolitical instability, create production bottlenecks and price volatility, impacting manufacturers and end-users alike. Intense competition among a multitude of global players often leads to price erosion and reduced profit margins, necessitating significant investment in cost-effective solutions and operational efficiency. Furthermore, evolving regulatory frameworks concerning environmental compliance and energy efficiency can add complexity and cost to product development and manufacturing processes, demanding adaptability and adherence to new standards.

Key Players Shaping the LCD Screen Driver Chip Market

- Texas Instruments

- STMicroelectronics

- Infineon Technologies

- NXP Semiconductors

- ON Semiconductor

- ROHM Semiconductor

- Allegro MicroSystems

- Toshiba

- Panasonic

- Maxim Integrated

- Microchip Technology

- Diodes Incorporated

- Melexis

- New Japan Radio

- FM

- Fortior Tech

- ICOFCHINA

- Dongwoon Anatech

- Dialog Semiconductor

- H&M Semiconductor

Significant LCD Screen Driver Chip Industry Milestones

- 2019: Introduction of advanced driver ICs supporting 10-bit color depth for enhanced visual fidelity.

- 2020: Increased integration of timing controllers (TCON) onto driver chipsets, reducing system complexity and cost.

- 2021: Emergence of driver solutions optimized for Mini-LED backlighting, enabling higher contrast ratios.

- 2022: Enhanced focus on power efficiency with ultra-low-power modes for portable and battery-operated devices.

- 2023: Significant advancements in driver ICs for automotive applications, supporting higher resolutions and wider operating temperatures.

- Q1 2024: Introduction of driver chips with improved flicker-free technology for reduced eye strain in prolonged viewing.

- Q2 2024: Increased adoption of advanced packaging technologies to improve thermal performance and miniaturization.

- Q3 2024: Growing emphasis on driver solutions for foldable and flexible display applications.

- Q4 2024: Developments in driver ICs for augmented reality (AR) and virtual reality (VR) headsets utilizing LCD technology.

- 2025: Anticipated launch of driver ICs supporting even higher pixel densities and refresh rates for next-generation displays.

- 2026: Expected integration of AI-driven image enhancement features directly into driver chipsets.

- 2027: Further consolidation of peripheral functions onto single-chip driver solutions.

- 2028: Increased adoption of advanced materials and manufacturing processes for improved performance and sustainability.

- 2029: Emergence of driver ICs optimized for specialized industrial and medical imaging applications.

- 2030: Continued innovation in power management for next-generation energy-efficient displays.

- 2031: Development of driver solutions for ultra-large-format commercial displays.

- 2032: Advancements in driver ICs to support emerging display technologies beyond current LCD advancements.

- 2033: Projected widespread adoption of highly integrated, intelligent driver solutions across all major LCD applications.

Future Outlook for LCD Screen Driver Chip Market

The future of the LCD screen driver chip market is characterized by sustained innovation and an expanding application spectrum. Growth catalysts include the relentless pursuit of higher display resolutions and refresh rates, coupled with the increasing demand for power-efficient solutions in an energy-conscious world. The continued integration of advanced features like adaptive sync and HDR capabilities will further enhance visual experiences. Strategic opportunities lie in the burgeoning automotive display market and the ongoing expansion of the Internet of Things (IoT), which will necessitate a diverse range of driver ICs. The market is poised for robust growth, driven by technological advancements and the ever-present consumer and industry desire for superior visual performance.

LCD Screen Driver Chip Segmentation

-

1. Application

- 1.1. Family Entertainment

- 1.2. Commercial Display

- 1.3. Other

-

2. Types

- 2.1. Dual Channel

- 2.2. Four Channel

- 2.3. Six Channel

- 2.4. Other

LCD Screen Driver Chip Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

LCD Screen Driver Chip Regional Market Share

Geographic Coverage of LCD Screen Driver Chip

LCD Screen Driver Chip REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global LCD Screen Driver Chip Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Family Entertainment

- 5.1.2. Commercial Display

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Dual Channel

- 5.2.2. Four Channel

- 5.2.3. Six Channel

- 5.2.4. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America LCD Screen Driver Chip Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Family Entertainment

- 6.1.2. Commercial Display

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Dual Channel

- 6.2.2. Four Channel

- 6.2.3. Six Channel

- 6.2.4. Other

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America LCD Screen Driver Chip Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Family Entertainment

- 7.1.2. Commercial Display

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Dual Channel

- 7.2.2. Four Channel

- 7.2.3. Six Channel

- 7.2.4. Other

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe LCD Screen Driver Chip Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Family Entertainment

- 8.1.2. Commercial Display

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Dual Channel

- 8.2.2. Four Channel

- 8.2.3. Six Channel

- 8.2.4. Other

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa LCD Screen Driver Chip Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Family Entertainment

- 9.1.2. Commercial Display

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Dual Channel

- 9.2.2. Four Channel

- 9.2.3. Six Channel

- 9.2.4. Other

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific LCD Screen Driver Chip Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Family Entertainment

- 10.1.2. Commercial Display

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Dual Channel

- 10.2.2. Four Channel

- 10.2.3. Six Channel

- 10.2.4. Other

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Texas Instruments

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 STMicroelectronics

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Infineon Technologies

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 NXP Semiconductors

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ON Semiconductor

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 ROHM Semiconductor

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Allegro MicroSystems

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Toshiba

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Panasonic

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Maxim Integrated

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Microchip Technology

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Diodes Incorporated

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Melexis

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 New Japan Radio

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 FM

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Fortior Tech

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 ICOFCHINA

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Dongwoon Anatech

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.19 Dialog Semiconductor

- 11.2.19.1. Overview

- 11.2.19.2. Products

- 11.2.19.3. SWOT Analysis

- 11.2.19.4. Recent Developments

- 11.2.19.5. Financials (Based on Availability)

- 11.2.20 H&M Semiconductor

- 11.2.20.1. Overview

- 11.2.20.2. Products

- 11.2.20.3. SWOT Analysis

- 11.2.20.4. Recent Developments

- 11.2.20.5. Financials (Based on Availability)

- 11.2.1 Texas Instruments

List of Figures

- Figure 1: Global LCD Screen Driver Chip Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America LCD Screen Driver Chip Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America LCD Screen Driver Chip Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America LCD Screen Driver Chip Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America LCD Screen Driver Chip Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America LCD Screen Driver Chip Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America LCD Screen Driver Chip Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America LCD Screen Driver Chip Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America LCD Screen Driver Chip Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America LCD Screen Driver Chip Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America LCD Screen Driver Chip Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America LCD Screen Driver Chip Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America LCD Screen Driver Chip Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe LCD Screen Driver Chip Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe LCD Screen Driver Chip Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe LCD Screen Driver Chip Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe LCD Screen Driver Chip Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe LCD Screen Driver Chip Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe LCD Screen Driver Chip Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa LCD Screen Driver Chip Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa LCD Screen Driver Chip Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa LCD Screen Driver Chip Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa LCD Screen Driver Chip Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa LCD Screen Driver Chip Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa LCD Screen Driver Chip Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific LCD Screen Driver Chip Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific LCD Screen Driver Chip Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific LCD Screen Driver Chip Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific LCD Screen Driver Chip Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific LCD Screen Driver Chip Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific LCD Screen Driver Chip Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global LCD Screen Driver Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global LCD Screen Driver Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global LCD Screen Driver Chip Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global LCD Screen Driver Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global LCD Screen Driver Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global LCD Screen Driver Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global LCD Screen Driver Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global LCD Screen Driver Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global LCD Screen Driver Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global LCD Screen Driver Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global LCD Screen Driver Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global LCD Screen Driver Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global LCD Screen Driver Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global LCD Screen Driver Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global LCD Screen Driver Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global LCD Screen Driver Chip Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global LCD Screen Driver Chip Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global LCD Screen Driver Chip Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific LCD Screen Driver Chip Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the LCD Screen Driver Chip?

The projected CAGR is approximately 7%.

2. Which companies are prominent players in the LCD Screen Driver Chip?

Key companies in the market include Texas Instruments, STMicroelectronics, Infineon Technologies, NXP Semiconductors, ON Semiconductor, ROHM Semiconductor, Allegro MicroSystems, Toshiba, Panasonic, Maxim Integrated, Microchip Technology, Diodes Incorporated, Melexis, New Japan Radio, FM, Fortior Tech, ICOFCHINA, Dongwoon Anatech, Dialog Semiconductor, H&M Semiconductor.

3. What are the main segments of the LCD Screen Driver Chip?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "LCD Screen Driver Chip," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the LCD Screen Driver Chip report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the LCD Screen Driver Chip?

To stay informed about further developments, trends, and reports in the LCD Screen Driver Chip, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence