Key Insights

The Medical High-Fidelity Simulation market is poised for substantial growth, with an estimated market size of $1.26 billion in 2025, projected to expand at a robust Compound Annual Growth Rate (CAGR) of 16.3% through 2033. This rapid expansion is fueled by an increasing global emphasis on improving patient safety, enhancing clinical skills among healthcare professionals, and the growing demand for advanced medical training solutions. The integration of these sophisticated simulation technologies is becoming indispensable for medical institutions and hospitals looking to provide realistic, hands-on training experiences without risk to patients. This allows for the effective management of complex medical scenarios, reducing errors, and ultimately leading to better patient outcomes. The market is also benefiting from continuous technological advancements, including the development of more lifelike simulators and the integration of artificial intelligence and virtual reality, further driving adoption across various medical specialties.

Medical High-Fidelity Simulation Market Size (In Billion)

The market's upward trajectory is further propelled by key drivers such as the rising incidence of chronic diseases requiring specialized medical interventions and the subsequent need for highly skilled healthcare providers. Furthermore, stringent regulatory requirements for healthcare professional training and the growing adoption of simulation-based learning in medical curricula are significant contributors. While the market enjoys strong growth, potential restraints include the high initial investment cost of advanced simulation equipment and the need for ongoing technical support and maintenance. However, these challenges are being mitigated by the long-term cost-effectiveness of simulations in reducing medical errors and improving training efficiency. The market is segmented into applications like hospitals and medical colleges, with a growing demand for both highly realistic patient simulators and mixed reality simulation technologies, catering to diverse training needs. Leading companies are actively investing in research and development to innovate and capture a larger market share in this dynamic sector.

Medical High-Fidelity Simulation Company Market Share

Medical High-Fidelity Simulation Market: A Comprehensive Analysis and Future Outlook (2019–2033)

This in-depth report provides a comprehensive analysis of the global Medical High-Fidelity Simulation market, encompassing market structure, trends, opportunities, dominant segments, product innovations, key drivers, challenges, and a detailed look at the competitive landscape. Leveraging high-volume keywords and detailed quantitative data, this report is essential for industry stakeholders seeking to understand market dynamics and capitalize on future growth. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033.

Medical High-Fidelity Simulation Market Structure & Competitive Landscape

The global Medical High-Fidelity Simulation market exhibits a moderately concentrated structure, with a few dominant players holding significant market share, estimated at approximately 60% of the total market value. Innovation drivers are primarily fueled by advancements in artificial intelligence (AI), augmented reality (AR), and virtual reality (VR) technologies, leading to increasingly realistic and immersive simulation experiences. Regulatory impacts are largely positive, with growing government initiatives and accreditation bodies emphasizing the importance of simulation-based training for healthcare professionals to improve patient safety and clinical outcomes. Product substitutes are limited, with high-fidelity simulations offering unparalleled realism and experiential learning opportunities that basic simulation methods cannot replicate. End-user segmentation highlights a strong demand from hospitals and medical colleges, which are increasingly investing in these advanced training tools. Mergers and acquisitions (M&A) trends are notable, with an estimated volume of 15 significant M&A activities observed within the historical period (2019-2024), indicating industry consolidation and strategic partnerships aimed at expanding product portfolios and market reach. The concentration ratio for the top 5 players is projected to be around 55% by the end of the forecast period.

Medical High-Fidelity Simulation Market Trends & Opportunities

The Medical High-Fidelity Simulation market is experiencing robust growth, projected to reach a valuation of over one billion dollars by the end of the forecast period. The compound annual growth rate (CAGR) for the market is estimated at a healthy 12.5% during the forecast period. This growth is propelled by a confluence of technological advancements, evolving healthcare education methodologies, and an increasing emphasis on patient safety and competency-based training. Technological shifts are a primary catalyst, with the integration of AI for more dynamic and responsive patient scenarios, and the widespread adoption of mixed reality (MR) and virtual reality (VR) technologies creating highly immersive and realistic training environments. These advancements enable trainees to practice complex procedures and manage critical events in a safe, controlled setting, significantly enhancing skill acquisition and retention.

Consumer preferences are shifting towards more personalized and adaptive learning experiences. High-fidelity simulators that can offer customized training modules and real-time performance feedback are gaining traction. The demand for simulation in various medical specialties, from surgical training to emergency response, is expanding, reflecting the need for continuous professional development and the introduction of new medical technologies and techniques. Competitive dynamics are characterized by intense innovation, with companies investing heavily in R&D to develop more sophisticated and cost-effective simulation solutions. The market penetration rate for high-fidelity simulation in developed economies is already substantial, estimated at over 70% in major healthcare institutions. However, significant growth opportunities lie in emerging markets, where the adoption of advanced simulation technologies is still in its nascent stages but poised for rapid expansion due to growing healthcare infrastructure and an increasing focus on quality healthcare delivery. The market penetration in emerging economies is expected to grow from approximately 30% to over 60% by 2033. Furthermore, the increasing adoption of simulation for remote and distributed learning models presents a significant opportunity, especially in light of the recent global health events that highlighted the need for flexible and accessible training solutions. The integration of haptic feedback technologies and advanced physiological modeling further enhances the realism and effectiveness of these simulations, creating a compelling value proposition for healthcare institutions and educators worldwide.

Dominant Markets & Segments in Medical High-Fidelity Simulation

The Hospital segment is currently the dominant application within the Medical High-Fidelity Simulation market, representing over 55% of the total market share. This dominance is driven by the continuous need for advanced clinical skills training, professional development, and in-situ simulation for improving patient care and safety protocols. Hospitals are increasingly investing in high-fidelity simulators to train their staff on complex medical procedures, rare conditions, and emergency response scenarios, thereby reducing medical errors and enhancing patient outcomes.

- Key Growth Drivers in the Hospital Segment:

- Patient Safety Initiatives: Mandates and accreditation requirements from bodies like the Joint Commission are pushing hospitals to adopt simulation-based training to minimize adverse events.

- Technological Integration: The seamless integration of advanced simulators with existing hospital IT infrastructure facilitates data collection, performance tracking, and skill assessment.

- Procedural Complexity: The introduction of new surgical techniques and medical devices necessitates rigorous training, which high-fidelity simulators effectively provide.

- Cost-Effectiveness: While initial investment is high, the long-term cost savings from reduced errors, shorter training times, and fewer real-patient training incidents make it an attractive option.

Within the Types of simulation, Highly Realistic Patient Simulators hold the largest market share, estimated at over 65%. These simulators meticulously replicate human anatomy, physiology, and responses, offering an unparalleled level of realism for hands-on training.

- Key Growth Drivers for Highly Realistic Patient Simulators:

- Authenticity: Their ability to mimic real patient conditions, including vital signs, sounds, and physiological responses, provides an invaluable learning experience.

- Versatility: These simulators can be used for a wide range of training scenarios, from basic life support to advanced trauma management and critical care.

- Skill Mastery: Trainees can repeatedly practice complex procedures and critical decision-making in a risk-free environment, fostering muscle memory and confidence.

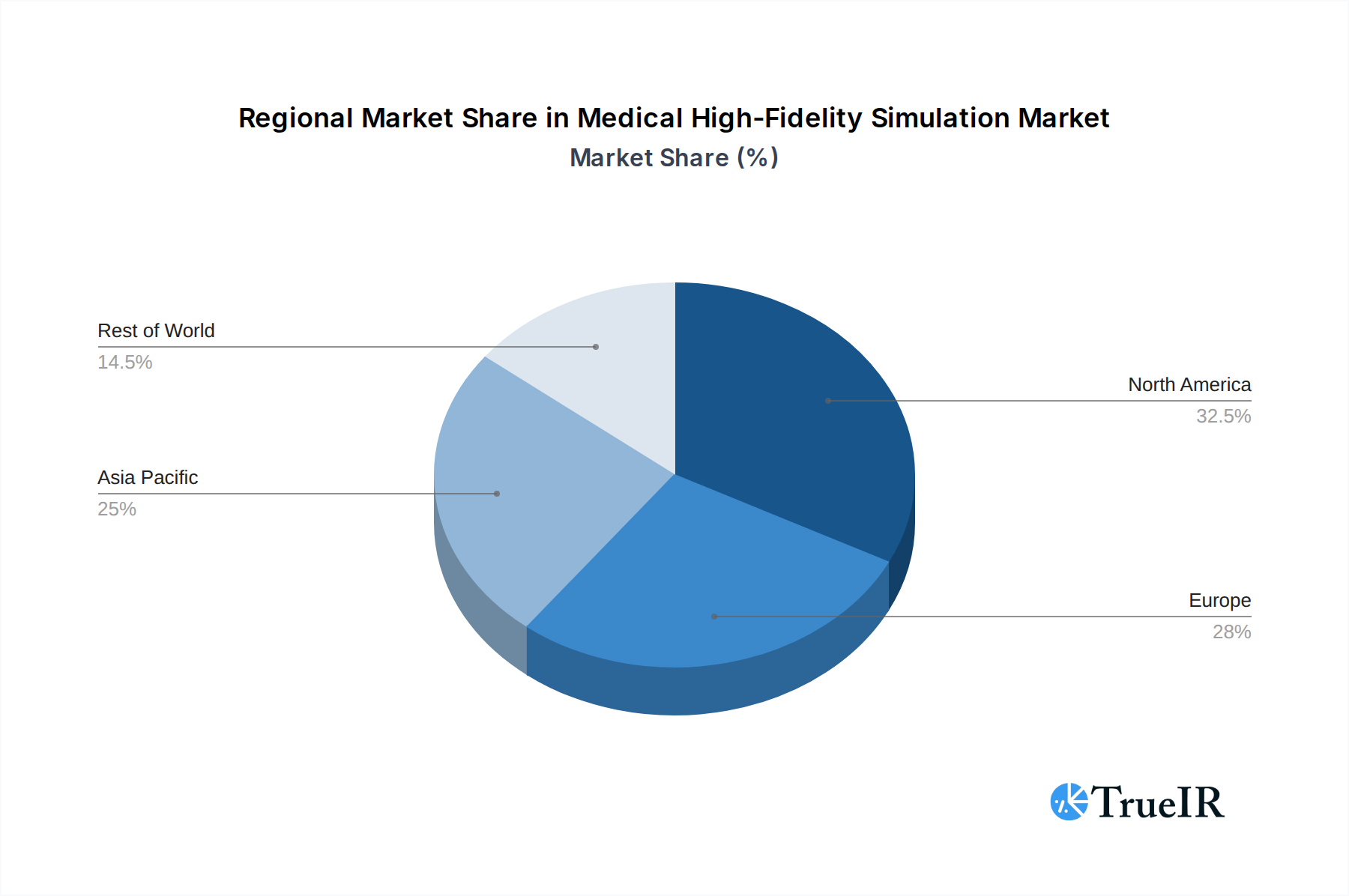

The Medical College segment is also a significant contributor, accounting for approximately 35% of the market. Educational institutions are embracing high-fidelity simulation as a vital component of their medical curricula, providing students with practical experience before they encounter real patients. The demand for Mixed Reality Simulation is also growing rapidly, albeit from a smaller base, driven by its potential to combine physical and virtual environments for enhanced learning experiences. Geographically, North America is the leading market due to its advanced healthcare infrastructure, significant R&D investments, and strong emphasis on medical education and patient safety.

Medical High-Fidelity Simulation Product Analysis

Medical high-fidelity simulation products are characterized by sophisticated technological integration, offering unparalleled realism and immersive learning experiences. Innovations are focused on developing advanced physiological models, haptic feedback systems, and AI-driven scenario generation to closely mimic real-life patient encounters. These products, ranging from full-body patient simulators to task-specific simulators and mixed reality platforms, are designed to enhance clinical decision-making, procedural proficiency, and team communication. Their competitive advantage lies in their ability to provide a safe, repeatable, and objective platform for skill acquisition and assessment, ultimately leading to improved patient outcomes. The market is seeing a surge in products that incorporate AI for adaptive learning and performance analytics, further solidifying their indispensability in modern medical training.

Key Drivers, Barriers & Challenges in Medical High-Fidelity Simulation

Key Drivers: The Medical High-Fidelity Simulation market is propelled by several key factors. Technological advancements, particularly in AI, VR, and AR, are enabling the creation of more realistic and interactive simulation experiences. The growing emphasis on patient safety and the reduction of medical errors, driven by regulatory bodies and healthcare accreditation standards, is a significant impetus. Furthermore, the increasing adoption of competency-based medical education and the need for continuous professional development among healthcare practitioners are fueling demand. Economic factors, such as the long-term cost-effectiveness of simulation training in reducing errors and improving efficiency, also play a crucial role.

Challenges & Restraints: Despite the positive outlook, the market faces several challenges. The high initial cost of acquisition and maintenance for advanced high-fidelity simulators can be a significant barrier, especially for smaller institutions or those in developing economies. Rapid technological obsolescence necessitates continuous investment in upgrades, further impacting cost-effectiveness. Regulatory hurdles related to the accreditation and standardization of simulation-based training can also create complexities. Supply chain disruptions, though less prevalent in the long term, can impact the availability of critical components. Intense competitive pressures among key players can lead to price wars, affecting profit margins.

Growth Drivers in the Medical High-Fidelity Simulation Market

Several key factors are driving the growth of the Medical High-Fidelity Simulation market. Technological innovation, including advancements in AI, VR, and AR, is crucial, enabling more realistic and interactive simulation experiences. For instance, AI-powered patient simulators can dynamically respond to trainee actions, mimicking complex physiological changes. Economic drivers, such as the long-term cost savings associated with reduced medical errors and improved training efficiency, make simulation a financially viable investment for healthcare institutions. Policy-driven factors, including government initiatives promoting evidence-based training and patient safety, further accelerate adoption. The increasing demand for continuous professional development and the integration of simulation into medical school curricula are also significant growth catalysts.

Challenges Impacting Medical High-Fidelity Simulation Growth

The growth of the Medical High-Fidelity Simulation market is not without its challenges. The substantial upfront cost of sophisticated simulators and associated software can be a significant barrier, particularly for smaller healthcare facilities and those in emerging economies. The rapid pace of technological evolution also means that simulation equipment can become outdated quickly, requiring continuous investment in upgrades and replacements. Regulatory complexities, including the lack of standardized accreditation for simulation programs in some regions, can hinder widespread adoption. Supply chain disruptions for specialized components can occasionally impact production and delivery timelines. Moreover, competitive pressures among a growing number of market players can lead to pricing challenges and affect profitability.

Key Players Shaping the Medical High-Fidelity Simulation Market

- Laerdal

- CAE

- Kyoto Kagaku

- Limbs&Things

- Simulaids

- Gaumard

- Mentice

- Surgical Science

- Simulab

- Tellyes

- Shanghai Honglian

- Yimo Keji

- Shanghai Kangren

- Shanghai Yilian

- Shanghai Boyou

- Shanghai Zhineng

Significant Medical High-Fidelity Simulation Industry Milestones

- 2019: Launch of advanced AI-powered virtual patients by CAE, enhancing diagnostic and treatment scenario realism.

- 2020 (April): Gaumard introduces the first fully integrated COVID-19 simulation solution for emergency response training.

- 2021 (November): Surgical Science acquires Mimic Technologies, expanding its robotic surgery simulation portfolio.

- 2022 (June): Laerdal Medical announces a strategic partnership with Kawa Medical to integrate advanced imaging simulation into its offerings.

- 2023 (January): Mentice launches a new generation of endovascular simulation platforms with enhanced haptic feedback.

- 2024 (May): The emergence of several Chinese manufacturers like Tellyes and Shanghai Honglian with increasingly sophisticated and cost-effective simulation solutions.

Future Outlook for Medical High-Fidelity Simulation Market

The future outlook for the Medical High-Fidelity Simulation market is exceptionally positive, driven by continued technological innovation and an unwavering commitment to enhancing healthcare quality. The integration of AI, VR, and AR will lead to even more immersive and adaptive training environments. We anticipate a significant increase in the adoption of mixed reality simulations, bridging the gap between virtual and real-world clinical practice. The market will witness further expansion in emerging economies as awareness of simulation benefits grows and cost-effective solutions become more accessible. Strategic opportunities lie in developing personalized training modules tailored to individual learning needs and in expanding the application of simulation beyond traditional medical education to include areas like patient education and remote patient monitoring. The market is poised for sustained double-digit growth, fueled by its proven ability to improve patient safety, clinical outcomes, and the overall efficiency of healthcare delivery systems worldwide.

Medical High-Fidelity Simulation Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Medical College

- 1.3. Others

-

2. Types

- 2.1. Highly Realistic Patient Simulator

- 2.2. Mixed Reality Simulation

Medical High-Fidelity Simulation Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Medical High-Fidelity Simulation Regional Market Share

Geographic Coverage of Medical High-Fidelity Simulation

Medical High-Fidelity Simulation REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 16.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Medical High-Fidelity Simulation Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Medical College

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Highly Realistic Patient Simulator

- 5.2.2. Mixed Reality Simulation

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Medical High-Fidelity Simulation Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Medical College

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Highly Realistic Patient Simulator

- 6.2.2. Mixed Reality Simulation

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Medical High-Fidelity Simulation Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Medical College

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Highly Realistic Patient Simulator

- 7.2.2. Mixed Reality Simulation

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Medical High-Fidelity Simulation Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Medical College

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Highly Realistic Patient Simulator

- 8.2.2. Mixed Reality Simulation

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Medical High-Fidelity Simulation Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Medical College

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Highly Realistic Patient Simulator

- 9.2.2. Mixed Reality Simulation

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Medical High-Fidelity Simulation Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Medical College

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Highly Realistic Patient Simulator

- 10.2.2. Mixed Reality Simulation

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Laerdal

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 CAE

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Kyoto Kagaku

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Limbs&Things

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Simulaids

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Gaumard

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Mentice

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Surgical Science

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Simulab

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tellyes

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Shanghai Honglian

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Yimo Keji

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Shanghai Kangren

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Shanghai Yilian

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Shanghai Boyou

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Shanghai Zhineng

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 Laerdal

List of Figures

- Figure 1: Global Medical High-Fidelity Simulation Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Medical High-Fidelity Simulation Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Medical High-Fidelity Simulation Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Medical High-Fidelity Simulation Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Medical High-Fidelity Simulation Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Medical High-Fidelity Simulation Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Medical High-Fidelity Simulation Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Medical High-Fidelity Simulation Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Medical High-Fidelity Simulation Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Medical High-Fidelity Simulation Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Medical High-Fidelity Simulation Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Medical High-Fidelity Simulation Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Medical High-Fidelity Simulation Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Medical High-Fidelity Simulation Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Medical High-Fidelity Simulation Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Medical High-Fidelity Simulation Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Medical High-Fidelity Simulation Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Medical High-Fidelity Simulation Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Medical High-Fidelity Simulation Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Medical High-Fidelity Simulation Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Medical High-Fidelity Simulation Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Medical High-Fidelity Simulation Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Medical High-Fidelity Simulation Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Medical High-Fidelity Simulation Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Medical High-Fidelity Simulation Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Medical High-Fidelity Simulation Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Medical High-Fidelity Simulation Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Medical High-Fidelity Simulation Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Medical High-Fidelity Simulation Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Medical High-Fidelity Simulation Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Medical High-Fidelity Simulation Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Medical High-Fidelity Simulation Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Medical High-Fidelity Simulation Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Medical High-Fidelity Simulation?

The projected CAGR is approximately 16.3%.

2. Which companies are prominent players in the Medical High-Fidelity Simulation?

Key companies in the market include Laerdal, CAE, Kyoto Kagaku, Limbs&Things, Simulaids, Gaumard, Mentice, Surgical Science, Simulab, Tellyes, Shanghai Honglian, Yimo Keji, Shanghai Kangren, Shanghai Yilian, Shanghai Boyou, Shanghai Zhineng.

3. What are the main segments of the Medical High-Fidelity Simulation?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 1.26 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 2900.00, USD 4350.00, and USD 5800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Medical High-Fidelity Simulation," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Medical High-Fidelity Simulation report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Medical High-Fidelity Simulation?

To stay informed about further developments, trends, and reports in the Medical High-Fidelity Simulation, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence