Key Insights

The Omnichannel in Healthcare market is poised for significant expansion, projected to reach $2.3 billion in 2025 with a robust CAGR of 12.1% during the forecast period of 2025-2033. This dynamic growth is propelled by an increasing demand for seamless patient journeys and enhanced healthcare experiences across multiple touchpoints. Key drivers include the rising adoption of digital health technologies, the imperative for improved patient engagement and retention, and the growing need for personalized care delivery. The shift towards value-based healthcare models also incentivizes providers to invest in integrated platforms that foster better communication and coordination between patients and clinicians. Emerging trends such as the integration of AI-powered chatbots for initial patient triage, the expansion of telehealth services, and the development of patient portals that offer comprehensive health management tools are further fueling this market's trajectory. The consolidation of patient data across various channels, from online appointments to in-person visits and remote monitoring, is becoming paramount for delivering efficient and effective care.

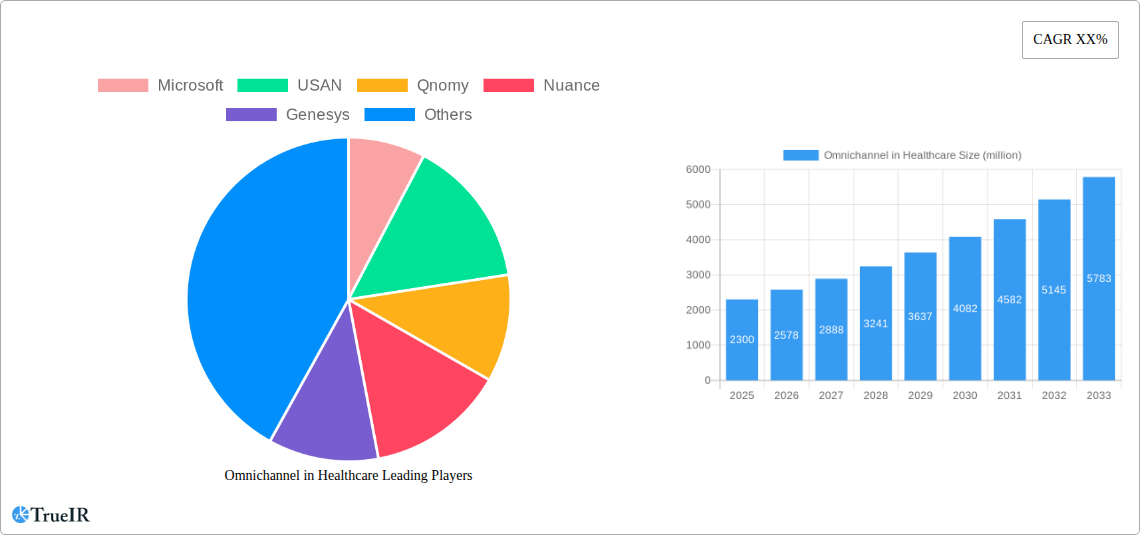

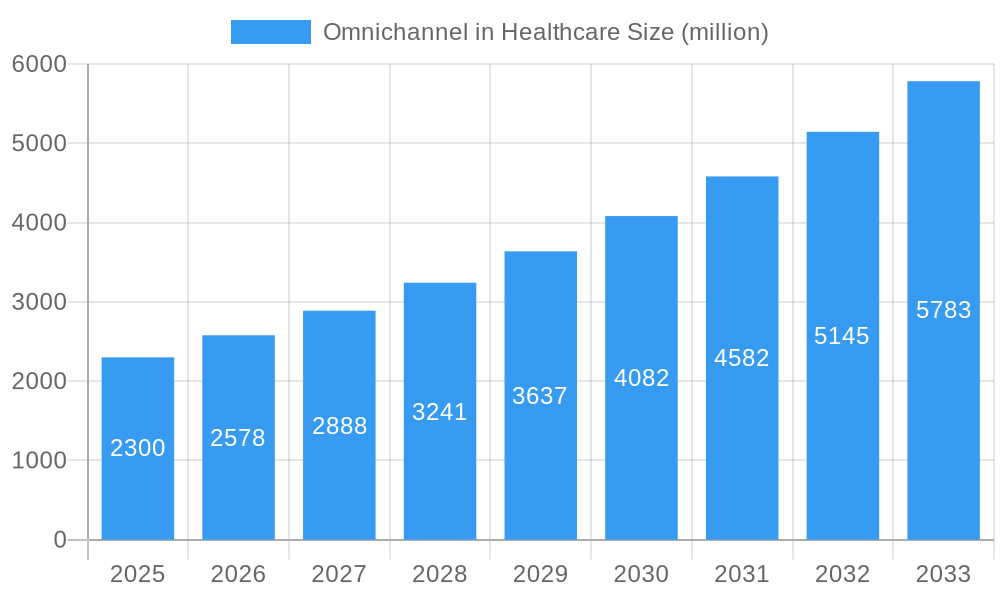

Omnichannel in Healthcare Market Size (In Billion)

Despite the promising outlook, certain restraints could temper growth, including stringent data privacy regulations (like HIPAA and GDPR) which necessitate substantial investment in secure infrastructure and compliance measures. Interoperability challenges between disparate healthcare IT systems also pose a hurdle, often leading to data silos and hindering the creation of a truly unified patient experience. Furthermore, the initial cost of implementing comprehensive omnichannel solutions can be a significant barrier for smaller healthcare organizations. However, the long-term benefits of improved patient satisfaction, operational efficiencies, and reduced readmission rates are increasingly outweighing these concerns. The market is segmented across various applications, with Hospitals and Pharmacies being major end-users, and divided into Software and Service types, catering to a wide spectrum of healthcare needs. Leading companies are actively investing in R&D and strategic collaborations to capture market share in this evolving landscape.

Omnichannel in Healthcare Company Market Share

Omnichannel in Healthcare: Driving Seamless Patient Experiences and Operational Efficiency

This comprehensive report delves deep into the burgeoning Omnichannel in Healthcare market, a critical sector revolutionizing patient engagement, care delivery, and operational excellence. Leveraging advanced technologies and integrated communication strategies, healthcare providers are transforming fragmented patient journeys into unified, personalized experiences. This report provides an in-depth analysis of market dynamics, future trends, key players, and strategic insights essential for stakeholders navigating this rapidly evolving landscape.

Omnichannel in Healthcare Market Structure & Competitive Landscape

The Omnichannel in Healthcare market exhibits a moderately concentrated structure, with a blend of large, established technology giants and specialized healthcare solution providers vying for market share. Innovation drivers are primarily fueled by the escalating demand for enhanced patient experience, the push for operational efficiency, and the increasing adoption of digital health technologies. Regulatory impacts, particularly data privacy (e.g., HIPAA compliance), significantly shape market strategies, necessitating secure and compliant omnichannel solutions. Product substitutes, while present in the form of single-channel solutions, are increasingly being eclipsed by integrated omnichannel platforms. End-user segmentation spans hospitals, pharmacies, and other healthcare settings, each with unique requirements. Mergers and acquisitions (M&A) are a notable trend, as companies aim to expand their service portfolios, gain technological advantages, and broaden their market reach. For instance, recent M&A volumes indicate a significant investment in consolidating omnichannel capabilities within the healthcare ecosystem. Concentration ratios suggest a dynamic competitive environment where strategic partnerships and technological integration are paramount for sustained growth.

Omnichannel in Healthcare Market Trends & Opportunities

The Omnichannel in Healthcare market is experiencing robust growth, projected to reach billions in the forecast period of 2025–2033. This expansion is driven by a confluence of factors, including the persistent shift towards patient-centric care models, the increasing prevalence of chronic diseases necessitating continuous engagement, and the imperative for healthcare organizations to improve operational efficiency and reduce costs. Technological advancements are at the forefront of this transformation. The integration of Artificial Intelligence (AI) and Machine Learning (ML) into patient communication platforms is enabling hyper-personalized interactions, predictive analytics for proactive care, and intelligent routing of inquiries. The proliferation of mobile health (mHealth) applications, wearable devices, and telehealth services has further accelerated the adoption of omnichannel strategies, allowing patients to interact with healthcare providers across various touchpoints seamlessly, whether it's booking appointments, accessing medical records, or receiving remote consultations.

Consumer preferences are also playing a pivotal role. Patients, accustomed to seamless digital experiences in other industries, now expect the same level of convenience and accessibility from their healthcare providers. This includes the ability to communicate via their preferred channels—be it a mobile app, website chat, email, or phone—without losing context or having to repeat information. This demand for consistent and integrated experiences is compelling healthcare organizations to invest in omnichannel solutions that can manage these diverse interactions effectively.

The competitive landscape is characterized by intense innovation and strategic alliances. Companies are focusing on developing platforms that offer end-to-end patient journey management, from initial inquiry and appointment scheduling to post-treatment follow-up and chronic care management. This includes solutions that integrate patient portals, CRM systems, contact center technologies, and digital marketing tools. The market penetration rate of advanced omnichannel solutions is steadily increasing as healthcare providers recognize their value in improving patient satisfaction, enhancing clinical outcomes, and optimizing resource allocation. The market size is estimated to be in the billions, with a projected Compound Annual Growth Rate (CAGR) that underscores the significant opportunities for growth and innovation in the coming years.

Dominant Markets & Segments in Omnichannel in Healthcare

The Omnichannel in Healthcare market demonstrates significant dominance within the Hospital application segment. Hospitals, as central hubs of patient care, are at the forefront of adopting integrated communication strategies to manage patient flow, appointment scheduling, pre-admission processes, and post-discharge follow-ups. The complexity of hospital operations, involving multiple departments and diverse patient needs, necessitates robust omnichannel solutions that can streamline communication and improve care coordination. Infrastructure development in hospitals, including the implementation of electronic health records (EHRs) and patient management systems, provides a strong foundation for integrating omnichannel capabilities. Furthermore, supportive policies aimed at enhancing patient experience and promoting digital health adoption within hospital settings further fuel this segment's growth.

The Pharmacy segment also represents a key area of growth, driven by the increasing demand for convenient prescription refills, medication adherence programs, and personalized pharmacy services. Omnichannel solutions enable pharmacies to offer seamless online ordering, curbside pickup, home delivery, and virtual pharmacist consultations, catering to the evolving needs of consumers seeking convenience and accessibility.

In terms of Types, the Software segment is the primary driver of market dominance, encompassing a wide array of platforms, applications, and tools designed to facilitate omnichannel interactions. This includes patient engagement platforms, customer relationship management (CRM) systems, AI-powered chatbots, telehealth software, and communication analytics tools. The development and deployment of sophisticated software are crucial for enabling the seamless integration of various communication channels and data sources.

The Service segment, while integral, follows closely behind software. This includes implementation services, consulting, system integration, and ongoing support provided by technology vendors and specialized service providers. These services are essential for helping healthcare organizations effectively deploy and manage their omnichannel solutions, ensuring optimal performance and ROI.

The Others application segment, encompassing clinics, long-term care facilities, and specialized healthcare providers, is also witnessing increasing adoption, albeit at a slightly slower pace than hospitals. These entities are increasingly recognizing the benefits of omnichannel strategies in improving patient engagement and operational efficiency, particularly in managing appointment scheduling, patient inquiries, and care coordination. The interplay between infrastructure readiness, evolving policies, and the drive for improved patient outcomes consistently positions the hospital segment and the software type as the leading forces in the omnichannel healthcare market.

Omnichannel in Healthcare Product Analysis

Omnichannel in Healthcare solutions are characterized by a focus on seamless patient journey orchestration, integrating diverse digital and physical touchpoints. Key product innovations include AI-powered chatbots for instant query resolution, virtual assistants for appointment scheduling and medication reminders, and secure messaging platforms for direct patient-provider communication. These products offer competitive advantages by enhancing patient engagement, improving operational efficiency, and reducing administrative burdens. Advanced analytics capabilities are also crucial, providing insights into patient behavior and communication patterns to enable personalized care delivery and optimize service offerings. The market fit is driven by the growing demand for connected healthcare experiences that are accessible, convenient, and patient-centric, leveraging technological advancements to bridge communication gaps.

Key Drivers, Barriers & Challenges in Omnichannel in Healthcare

Key Drivers, Barriers & Challenges in Omnichannel in Healthcare

Key Drivers:

- Patient-Centricity Demand: The escalating expectation for personalized and convenient healthcare experiences is a primary driver.

- Technological Advancements: AI, ML, cloud computing, and mobile technologies are enabling more sophisticated and integrated omnichannel solutions.

- Operational Efficiency Imperative: Healthcare organizations are seeking solutions to streamline workflows, reduce costs, and optimize resource allocation.

- Data Interoperability Push: The growing need to connect disparate health data systems to provide a unified patient view.

Barriers & Challenges:

- Data Security & Privacy Concerns: Ensuring compliance with stringent regulations like HIPAA is paramount and complex.

- Legacy System Integration: Integrating new omnichannel platforms with existing, often outdated, healthcare IT infrastructure poses significant challenges.

- Implementation Costs & ROI Justification: The substantial investment required for omnichannel solutions necessitates clear demonstrations of return on investment.

- Workforce Training & Adoption: Ensuring healthcare staff are adequately trained and comfortable using new omnichannel tools is crucial for successful adoption.

- Fragmented Healthcare Ecosystem: The inherent complexity of the healthcare industry, with its numerous stakeholders and diverse processes, can hinder seamless integration.

Growth Drivers in the Omnichannel in Healthcare Market

The Omnichannel in Healthcare market is propelled by several significant growth drivers. Technologically, the rapid advancements in Artificial Intelligence (AI) and Machine Learning (ML) are enabling more sophisticated patient engagement tools, such as personalized communication and predictive analytics for proactive care. The increasing adoption of cloud-based solutions facilitates scalability and accessibility of omnichannel platforms. Economically, the pressure on healthcare providers to improve operational efficiency and reduce costs is a major catalyst, as omnichannel strategies can streamline administrative tasks and optimize patient flow. Furthermore, evolving regulatory landscapes that encourage digital health adoption and patient empowerment, such as telehealth reimbursement policies, are creating a more conducive environment for growth. The growing consumer demand for convenient, personalized, and accessible healthcare experiences, akin to those in other service industries, is a powerful market force driving investment in omnichannel solutions.

Challenges Impacting Omnichannel in Healthcare Growth

Despite the promising growth, several challenges impact the expansion of the Omnichannel in Healthcare market. Regulatory complexities surrounding data privacy and security, particularly adherence to HIPAA and similar global standards, remain a significant hurdle, demanding robust compliance measures and secure infrastructure. Supply chain issues, while perhaps less direct than in physical product industries, can manifest in delays in software development, hardware deployment, and the availability of skilled IT personnel to implement and manage these complex systems. Competitive pressures from both established technology players and innovative startups are intense, requiring continuous investment in research and development to maintain a competitive edge. Furthermore, the inertia of legacy IT systems within many healthcare organizations presents a substantial barrier to seamless integration, often leading to protracted implementation timelines and increased costs. Resistance to change among healthcare professionals and the need for extensive training can also slow down adoption rates.

Key Players Shaping the Omnichannel in Healthcare Market

- Microsoft

- USAN

- Qnomy

- Nuance

- Genesys

- Compart

- Wipro

- TTEC Holdings

- PDI

- Arvato

- Evolve IP

- Adobe

- MuleSoft

Significant Omnichannel in Healthcare Industry Milestones

- 2019: Increased focus on patient portals and mobile app integration for appointment booking and record access.

- 2020: Accelerated adoption of telehealth and remote patient monitoring solutions due to the global pandemic.

- 2021: Emergence of AI-powered chatbots and virtual assistants for initial patient triage and information dissemination.

- 2022: Greater emphasis on data analytics for personalizing patient communication and predicting health needs.

- 2023: Advancements in secure messaging platforms and integration with wearable health devices for continuous care.

- 2024: Growing adoption of unified communication platforms by healthcare systems for seamless internal and external interactions.

Future Outlook for Omnichannel in Healthcare Market

The future outlook for the Omnichannel in Healthcare market is exceptionally promising, characterized by continued innovation and market expansion. Strategic opportunities lie in further leveraging AI and machine learning to create hyper-personalized patient experiences, enabling proactive interventions and predictive health management. The integration of the Internet of Medical Things (IoMT) will allow for real-time data collection and analysis, further enhancing care coordination and patient outcomes. As healthcare systems increasingly prioritize patient satisfaction and operational efficiency, the demand for comprehensive, integrated omnichannel solutions will surge. The market potential is significant, driven by the ongoing digital transformation of healthcare and the persistent need to provide accessible, convenient, and effective care across all touchpoints. This will foster a more connected and patient-centric healthcare ecosystem.

Omnichannel in Healthcare Segmentation

-

1. Application

- 1.1. Hospital

- 1.2. Pharmacy

- 1.3. Others

-

2. Types

- 2.1. Software

- 2.2. Service

Omnichannel in Healthcare Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

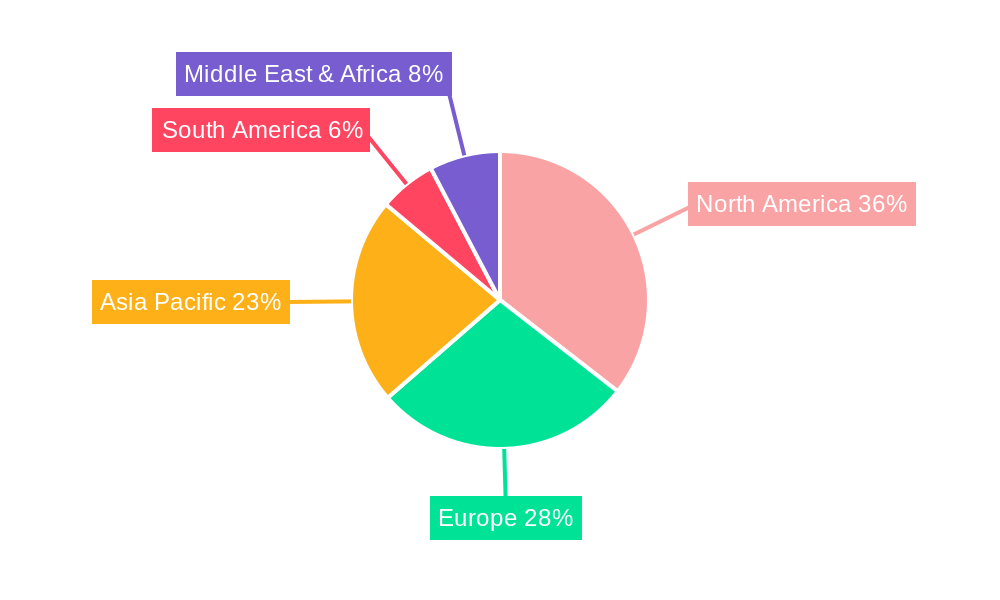

Omnichannel in Healthcare Regional Market Share

Geographic Coverage of Omnichannel in Healthcare

Omnichannel in Healthcare REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Omnichannel in Healthcare Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Hospital

- 5.1.2. Pharmacy

- 5.1.3. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Software

- 5.2.2. Service

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Omnichannel in Healthcare Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Hospital

- 6.1.2. Pharmacy

- 6.1.3. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Software

- 6.2.2. Service

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Omnichannel in Healthcare Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Hospital

- 7.1.2. Pharmacy

- 7.1.3. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Software

- 7.2.2. Service

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Omnichannel in Healthcare Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Hospital

- 8.1.2. Pharmacy

- 8.1.3. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Software

- 8.2.2. Service

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Omnichannel in Healthcare Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Hospital

- 9.1.2. Pharmacy

- 9.1.3. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Software

- 9.2.2. Service

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Omnichannel in Healthcare Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Hospital

- 10.1.2. Pharmacy

- 10.1.3. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Software

- 10.2.2. Service

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Microsoft

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 USAN

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Qnomy

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Nuance

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Genesys

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Compart

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Wipro

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 TTEC Holdings

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 PDI

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Arvato

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Evolve IP

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Adobe

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 MuleSoft

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 Microsoft

List of Figures

- Figure 1: Global Omnichannel in Healthcare Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Omnichannel in Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Omnichannel in Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Omnichannel in Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Omnichannel in Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Omnichannel in Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Omnichannel in Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Omnichannel in Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Omnichannel in Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Omnichannel in Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Omnichannel in Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Omnichannel in Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Omnichannel in Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Omnichannel in Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Omnichannel in Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Omnichannel in Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Omnichannel in Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Omnichannel in Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Omnichannel in Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Omnichannel in Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Omnichannel in Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Omnichannel in Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Omnichannel in Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Omnichannel in Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Omnichannel in Healthcare Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Omnichannel in Healthcare Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Omnichannel in Healthcare Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Omnichannel in Healthcare Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Omnichannel in Healthcare Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Omnichannel in Healthcare Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Omnichannel in Healthcare Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Omnichannel in Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Omnichannel in Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Omnichannel in Healthcare Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Omnichannel in Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Omnichannel in Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Omnichannel in Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Omnichannel in Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Omnichannel in Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Omnichannel in Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Omnichannel in Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Omnichannel in Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Omnichannel in Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Omnichannel in Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Omnichannel in Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Omnichannel in Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Omnichannel in Healthcare Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Omnichannel in Healthcare Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Omnichannel in Healthcare Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Omnichannel in Healthcare Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Omnichannel in Healthcare?

The projected CAGR is approximately 12.1%.

2. Which companies are prominent players in the Omnichannel in Healthcare?

Key companies in the market include Microsoft, USAN, Qnomy, Nuance, Genesys, Compart, Wipro, TTEC Holdings, PDI, Arvato, Evolve IP, Adobe, MuleSoft.

3. What are the main segments of the Omnichannel in Healthcare?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Omnichannel in Healthcare," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Omnichannel in Healthcare report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Omnichannel in Healthcare?

To stay informed about further developments, trends, and reports in the Omnichannel in Healthcare, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence