Key Insights

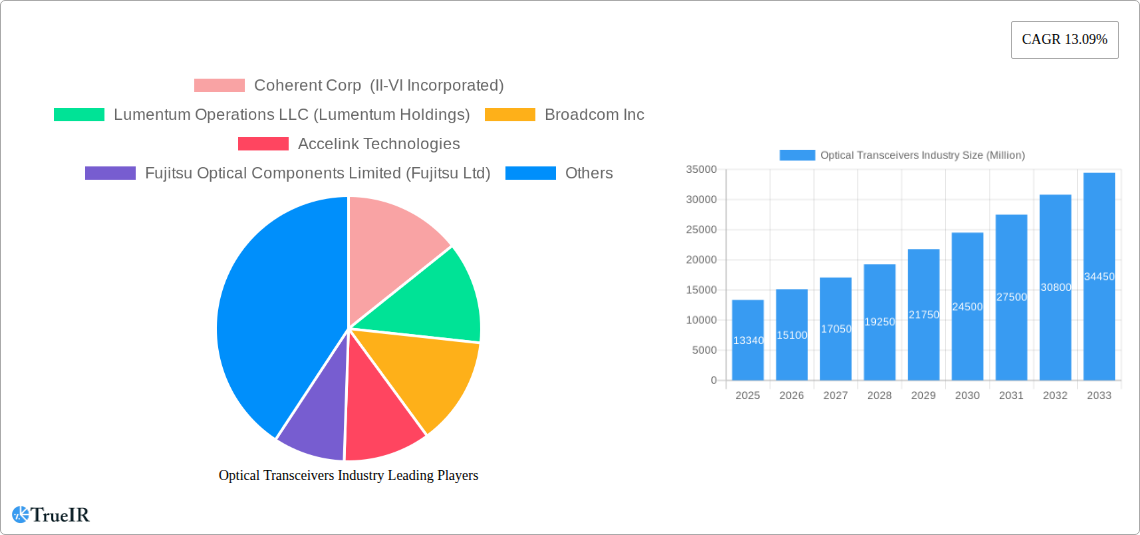

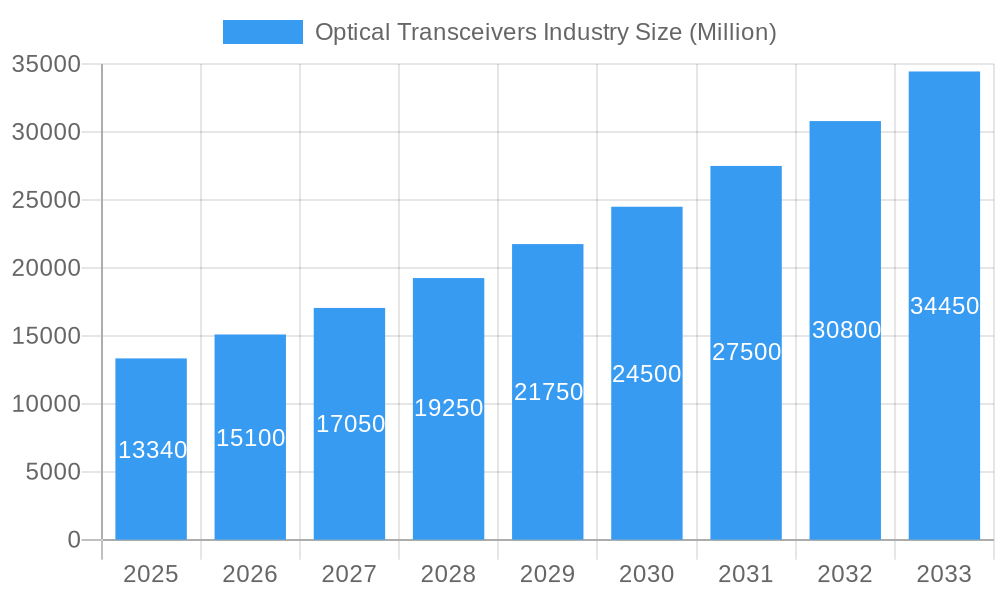

The global Optical Transceivers Industry is poised for remarkable expansion, projected to reach an estimated market size of $13.34 billion by 2025. This robust growth is fueled by a compelling Compound Annual Growth Rate (CAGR) of 13.09% throughout the forecast period of 2025-2033. The increasing demand for higher bandwidth and faster data transmission speeds across diverse applications, particularly in data centers and telecommunications, serves as a primary driver. Advancements in technologies like Ethernet, Fiber Channel, CWDM/DWDM, and FTTX are continuously pushing the boundaries of what optical transceivers can achieve, enabling seamless and efficient data flow. The proliferation of 5G networks, cloud computing adoption, and the burgeoning Internet of Things (IoT) ecosystem further amplify the need for advanced optical transceiver solutions.

Optical Transceivers Industry Market Size (In Billion)

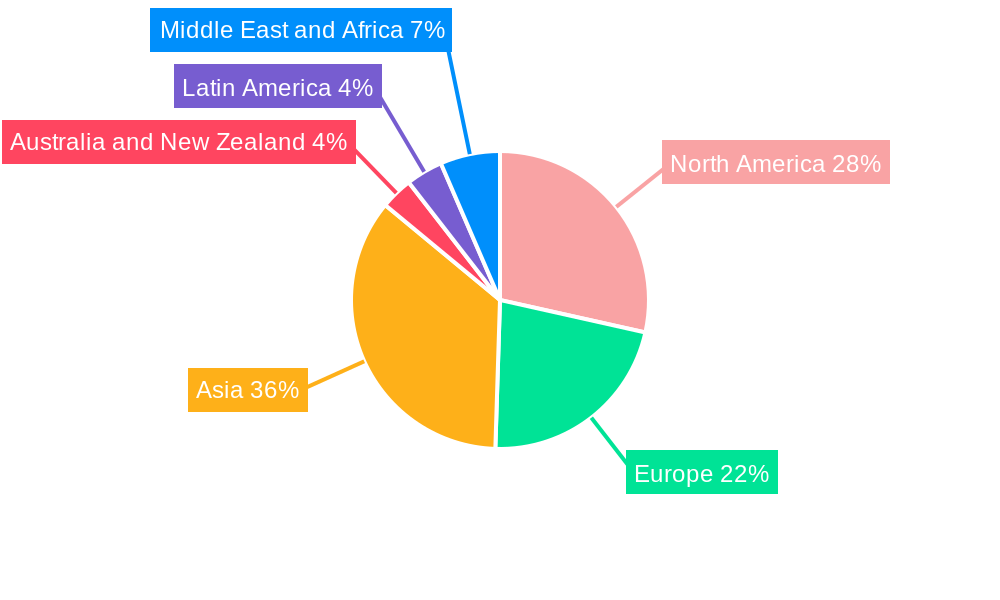

The industry's trajectory is also shaped by significant trends such as the ongoing transition to higher data rates, with a strong emphasis on 100 Gbps and greater than 100 Gbps segments, essential for handling the ever-growing volume of data. Emerging applications in areas like artificial intelligence, machine learning, and virtual/augmented reality also contribute to this upward trend. While the market enjoys substantial growth, certain restraints, such as the high cost of advanced optical components and the complexity of deployment in certain scenarios, need to be navigated. Key players like Coherent Corp (II-VI Incorporated), Lumentum Operations LLC, and Broadcom Inc. are at the forefront of innovation, driving technological advancements and catering to the evolving demands of the global optical transceiver market. Regional dynamics, with North America and Asia expected to lead in market share due to significant investments in digital infrastructure, will also play a crucial role in the industry's overall performance.

Optical Transceivers Industry Company Market Share

This comprehensive report delves into the dynamic global optical transceivers market, providing in-depth analysis from 2019 to 2033, with a base year of 2025 and a forecast period extending to 2033. Leveraging high-volume keywords and structured for optimal SEO, this report targets industry professionals seeking critical insights into market dynamics, technological advancements, and future growth opportunities within the optical transceiver ecosystem. We meticulously examine market segmentation by protocol, data rate, and application, alongside an in-depth exploration of key industry players and their strategic initiatives.

Optical Transceivers Industry Market Structure & Competitive Landscape

The optical transceivers industry is characterized by a moderately concentrated market structure, with a few dominant players holding significant market share, particularly in high-speed, high-density transceiver segments. Innovation is a primary driver, fueled by the relentless demand for increased bandwidth and lower latency in data centers, telecommunications networks, and emerging enterprise applications. Regulatory impacts, while not overtly restrictive, often focus on standardization and interoperability to foster a competitive environment. Product substitutes, primarily copper-based solutions for shorter reach applications, continue to be present but are increasingly challenged by the performance advantages of optical technologies. End-user segmentation reveals a substantial reliance on data centers and telecommunications providers, with growing adoption in industrial automation and automotive sectors. Mergers and acquisitions (M&A) are a recurring theme, with companies consolidating to enhance technological capabilities, expand product portfolios, and gain market access. For instance, the acquisition of Semtech Corporation's Fiberdge PAM4 PMDs by Broadcom signifies a strategic move to integrate advanced semiconductor technology with optical transceiver solutions. This consolidation aims to streamline product development and accelerate the deployment of next-generation solutions. The industry's growth is intrinsically linked to advancements in cloud computing, AI/ML, and the expansion of 5G networks, creating a perpetual cycle of innovation and investment.

Optical Transceivers Industry Market Trends & Opportunities

The global optical transceivers market is poised for substantial expansion, driven by the insatiable demand for higher bandwidth and lower latency across a multitude of applications. This market is projected to experience a Compound Annual Growth Rate (CAGR) of approximately 12-15% from 2025 to 2033. The foundational growth driver remains the exponential increase in data traffic generated by cloud computing, big data analytics, and the proliferation of connected devices. Technological shifts are central to this market’s evolution, with a pronounced movement towards higher data rates, exemplified by the widespread adoption of 100 Gbps, 200 Gbps, 400 Gbps, and the emerging 800 Gbps and 1.6 Tbps optical transceivers. The development and implementation of advanced modulation formats like PAM4 (Pulse Amplitude Modulation) are critical enablers for these higher speeds, allowing for more bits per symbol transmission. Consumer preferences, though indirectly influencing this B2B market, are shaped by the demand for faster internet speeds, immersive entertainment, and seamless connectivity, all of which necessitate robust optical infrastructure. Competitive dynamics are intensifying, with key players investing heavily in research and development to secure a leading position in next-generation optical technology. Opportunities abound in the development of cost-effective, high-performance optical transceivers for data center interconnects (DCIs), metro networks, and emerging areas like AI/ML clusters. The ongoing evolution of Ethernet standards, particularly towards higher speeds like 400GbE and 800GbE, presents a significant market penetration opportunity. Furthermore, the increasing deployment of Fiber-to-the-X (FTTX) networks globally fuels demand for FTTX-specific optical transceivers. The integration of advanced technologies such as silicon photonics and co-packaged optics offers further avenues for innovation and market differentiation, enabling smaller, more power-efficient, and higher-performance solutions. The strategic partnerships and demonstrations, such as the October 2023 collaboration between Broadcom and Semtech, underscore the industry's focus on pushing the boundaries of speed and efficiency to meet future network demands.

Dominant Markets & Segments in Optical Transceivers Industry

The global optical transceivers market exhibits clear dominance across specific segments, driven by the foundational infrastructure needs of the digital economy.

Dominant Protocol:

- Ethernet: This protocol stands as the undisputed leader, powering the vast majority of data center interconnects and enterprise networking. The relentless drive for higher speeds within Ethernet, from 100GbE to 400GbE and beyond, fuels sustained demand for advanced Ethernet optical transceivers.

- CWDM/DWDM (Coarse/Dense Wavelength Division Multiplexing): These technologies are crucial for maximizing fiber capacity, particularly in long-haul and metro telecommunication networks. Their importance is amplified by the increasing need for spectral efficiency in bandwidth-constrained environments.

- FTTX (Fiber-to-the-X): The global rollout of fiber optic broadband networks for residential and business connectivity directly translates to significant and growing demand for FTTX-specific optical transceivers.

Dominant Data Rate:

- 100 Gbps: Currently represents a substantial market share, serving as the workhorse for many high-performance data center and telecommunication applications.

- Greater than 100 Gbps (including 200 Gbps, 400 Gbps, 800 Gbps): This segment is experiencing the most rapid growth, driven by the insatiable demand for higher bandwidth in AI/ML workloads, hyperscale data centers, and next-generation telecom infrastructure. The demonstrations of 800G and 1.6T technologies by industry leaders highlight the aggressive trajectory of this segment.

- 10 Gbps to 40 Gbps: While still relevant, this segment is gradually being surpassed by higher data rates as network upgrade cycles progress.

Dominant Application:

- Data Center: This segment is the largest consumer of optical transceivers. The expansion of hyperscale data centers, edge computing, and the increasing demand for AI/ML processing power are paramount drivers. The need for high-density, high-speed interconnects within data centers is a constant source of innovation and market growth.

- Telecommunication: Driven by the deployment of 5G networks, the expansion of fiber optic backhaul, and the growth of metro networks, the telecommunication sector remains a critical and expanding market for optical transceivers. The push for higher capacity and lower latency in mobile backhaul and core networks directly fuels this demand.

The expansion of 5G infrastructure, coupled with the continuous upgrades within hyperscale data centers, are key growth drivers. Government initiatives promoting digital infrastructure development and broadband penetration also play a significant role. The increasing adoption of cloud services and the burgeoning field of artificial intelligence and machine learning are creating unprecedented demand for high-speed, high-density optical connectivity within data centers. Furthermore, the ongoing digital transformation across various industries, from manufacturing to healthcare, is necessitating more robust and high-performance network infrastructure, thereby boosting the demand for optical transceivers.

Optical Transceivers Industry Product Analysis

The optical transceivers industry is defined by relentless product innovation focused on enhancing speed, efficiency, and form factor miniaturization. Key product advancements include the widespread adoption of 400G and 800G transceivers, leveraging advanced modulation techniques like PAM4 to achieve higher data rates. Silicon photonics is a transformative technology enabling the integration of optical and electronic components on a single chip, leading to smaller, more power-efficient, and cost-effective transceivers. The development of pluggable modules in standardized form factors (e.g., QSFP-DD, OSFP) ensures interoperability and ease of deployment in diverse network environments. Competitive advantages are derived from superior optical performance, lower power consumption, advanced thermal management, and robust signal integrity. Products designed for specific applications, such as low-latency data center interconnects or ruggedized industrial transceivers, cater to niche but growing market demands.

Key Drivers, Barriers & Challenges in Optical Transceivers Industry

Key Drivers: The optical transceivers market is propelled by several key drivers. The escalating demand for bandwidth, fueled by cloud computing, AI/ML, and the expansion of 5G networks, is a primary catalyst. Technological advancements, particularly in higher data rates (400G, 800G, and beyond) and emerging technologies like silicon photonics, are crucial. Government initiatives promoting digital infrastructure and broadband expansion also provide significant impetus. The growing adoption of high-performance computing (HPC) and the increasing interconnectivity of data centers are further contributing to market growth.

Key Barriers & Challenges: Despite robust growth, the industry faces several challenges. High research and development costs associated with cutting-edge technology present a significant barrier to entry for smaller players. Supply chain disruptions, as seen in recent years, can impact production timelines and component availability. Intense competition and price erosion, particularly in mature segments, put pressure on profit margins. Furthermore, the complexity of global regulatory environments and the need for adherence to diverse industry standards can pose challenges. Evolving technological requirements and the need for constant innovation to stay competitive also represent ongoing hurdles.

Growth Drivers in the Optical Transceivers Industry Market

The optical transceivers industry is experiencing significant growth driven by fundamental shifts in global technology consumption. The exponential increase in data traffic, largely attributed to cloud computing, big data analytics, and the widespread adoption of AI and machine learning applications, creates an insatiable demand for higher bandwidth solutions. The ongoing global rollout and upgrades of 5G mobile networks necessitate substantial investments in optical interconnects for backhaul and fronthaul infrastructure. Furthermore, the rapid expansion of hyperscale data centers and the emergence of edge computing further amplify the need for high-density, high-performance optical transceivers. Government initiatives worldwide aimed at improving digital infrastructure and bridging the digital divide through fiber optic deployments are also key growth catalysts.

Challenges Impacting Optical Transceivers Industry Growth

While the trajectory is upward, several challenges temper the growth of the optical transceivers industry. The intricate and often volatile global supply chain for critical components can lead to production delays and increased costs, impacting the timely delivery of products. Intense competition among established players and emerging manufacturers can lead to price erosion, particularly in high-volume segments, squeezing profit margins. The continuous and rapid pace of technological innovation requires substantial and ongoing investment in research and development, posing a significant financial burden and a risk of obsolescence if R&D efforts are not aligned with market demands. Navigating the complex landscape of international trade regulations, tariffs, and geopolitical factors adds another layer of complexity and potential disruption.

Key Players Shaping the Optical Transceivers Industry Market

- Coherent Corp (II-VI Incorporated)

- Lumentum Operations LLC (Lumentum Holdings)

- Broadcom Inc

- Accelink Technologies

- Fujitsu Optical Components Limited (Fujitsu Ltd)

- Huawei Technologies Co Ltd

- Source Photonics (Redview Capital)

- HUBER+SUHNER Cube Optics

- Smiths Interconnect (Reflex Photonics Inc)

- Sumitomo Electric Industries Ltd

Significant Optical Transceivers Industry Industry Milestones

- October 2023: Broadcom and Semtech Corporation announced the demonstration of a 200 G/lane optical transceiver at the ECOC 2023, featuring Semtech’s latest Fiberdge 200 G PAM4 PMDs and Broadcom’s latest generation DSP PHY and single-mode optics. This collaboration signifies a leap in data transmission speeds for high-performance networking.

- October 2023: II-VI Incorporated (now Coherent Corp) announced its demonstration of next-generation transceivers and laser technology for 800 G and 1.6T datacom transmission at ECOC 2023 in Glasgow, Scotland. These advances are critical to sustaining the accelerating growth of the cloud driven by artificial intelligence and machine learning (AI/ML). These transceivers are used in 25 T and 50 T Ethernet switches with 100 G electrical lanes. This announcement highlights the industry's commitment to powering AI/ML infrastructure with unprecedented optical capabilities.

Future Outlook for Optical Transceivers Industry Market

The future outlook for the optical transceivers market is exceptionally robust, driven by an ongoing surge in data consumption and the pervasive integration of digital technologies across all facets of life. Emerging technologies such as silicon photonics will continue to enable smaller, more energy-efficient, and cost-effective transceivers, paving the way for wider adoption. The increasing demand from AI/ML applications and the continued expansion of 5G and beyond will necessitate even higher bandwidth solutions, pushing the industry towards terabit-per-second capabilities. Strategic opportunities lie in the development of advanced co-packaged optics solutions that integrate transceivers directly with processors, further reducing latency and power consumption. The growing adoption of optical interconnects in areas beyond traditional data centers and telecommunications, such as in advanced automotive systems and industrial IoT, presents significant untapped market potential. Overall, the market is poised for sustained growth as it remains fundamental to the progression of the digital economy.

Optical Transceivers Industry Segmentation

-

1. Protocol

- 1.1. Ethernet

- 1.2. Fiber Channel

- 1.3. CWDM/DWDM

- 1.4. FTTX

- 1.5. Other Protocols

-

2. Data Rate

- 2.1. Less than 10 Gbps

- 2.2. 10 Gbps to 40 Gbps

- 2.3. 100 Gbps

- 2.4. Greater than 100 Gbps

-

3. Application

- 3.1. Data Center

- 3.2. Telecommunication

Optical Transceivers Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Optical Transceivers Industry Regional Market Share

Geographic Coverage of Optical Transceivers Industry

Optical Transceivers Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 13.09% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Protocol

- 5.1.1. Ethernet

- 5.1.2. Fiber Channel

- 5.1.3. CWDM/DWDM

- 5.1.4. FTTX

- 5.1.5. Other Protocols

- 5.2. Market Analysis, Insights and Forecast - by Data Rate

- 5.2.1. Less than 10 Gbps

- 5.2.2. 10 Gbps to 40 Gbps

- 5.2.3. 100 Gbps

- 5.2.4. Greater than 100 Gbps

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Data Center

- 5.3.2. Telecommunication

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia

- 5.4.4. Australia and New Zealand

- 5.4.5. Latin America

- 5.4.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Protocol

- 6. Global Optical Transceivers Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Protocol

- 6.1.1. Ethernet

- 6.1.2. Fiber Channel

- 6.1.3. CWDM/DWDM

- 6.1.4. FTTX

- 6.1.5. Other Protocols

- 6.2. Market Analysis, Insights and Forecast - by Data Rate

- 6.2.1. Less than 10 Gbps

- 6.2.2. 10 Gbps to 40 Gbps

- 6.2.3. 100 Gbps

- 6.2.4. Greater than 100 Gbps

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Data Center

- 6.3.2. Telecommunication

- 6.1. Market Analysis, Insights and Forecast - by Protocol

- 7. North America Optical Transceivers Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Protocol

- 7.1.1. Ethernet

- 7.1.2. Fiber Channel

- 7.1.3. CWDM/DWDM

- 7.1.4. FTTX

- 7.1.5. Other Protocols

- 7.2. Market Analysis, Insights and Forecast - by Data Rate

- 7.2.1. Less than 10 Gbps

- 7.2.2. 10 Gbps to 40 Gbps

- 7.2.3. 100 Gbps

- 7.2.4. Greater than 100 Gbps

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Data Center

- 7.3.2. Telecommunication

- 7.1. Market Analysis, Insights and Forecast - by Protocol

- 8. Europe Optical Transceivers Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Protocol

- 8.1.1. Ethernet

- 8.1.2. Fiber Channel

- 8.1.3. CWDM/DWDM

- 8.1.4. FTTX

- 8.1.5. Other Protocols

- 8.2. Market Analysis, Insights and Forecast - by Data Rate

- 8.2.1. Less than 10 Gbps

- 8.2.2. 10 Gbps to 40 Gbps

- 8.2.3. 100 Gbps

- 8.2.4. Greater than 100 Gbps

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Data Center

- 8.3.2. Telecommunication

- 8.1. Market Analysis, Insights and Forecast - by Protocol

- 9. Asia Optical Transceivers Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Protocol

- 9.1.1. Ethernet

- 9.1.2. Fiber Channel

- 9.1.3. CWDM/DWDM

- 9.1.4. FTTX

- 9.1.5. Other Protocols

- 9.2. Market Analysis, Insights and Forecast - by Data Rate

- 9.2.1. Less than 10 Gbps

- 9.2.2. 10 Gbps to 40 Gbps

- 9.2.3. 100 Gbps

- 9.2.4. Greater than 100 Gbps

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Data Center

- 9.3.2. Telecommunication

- 9.1. Market Analysis, Insights and Forecast - by Protocol

- 10. Australia and New Zealand Optical Transceivers Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Protocol

- 10.1.1. Ethernet

- 10.1.2. Fiber Channel

- 10.1.3. CWDM/DWDM

- 10.1.4. FTTX

- 10.1.5. Other Protocols

- 10.2. Market Analysis, Insights and Forecast - by Data Rate

- 10.2.1. Less than 10 Gbps

- 10.2.2. 10 Gbps to 40 Gbps

- 10.2.3. 100 Gbps

- 10.2.4. Greater than 100 Gbps

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Data Center

- 10.3.2. Telecommunication

- 10.1. Market Analysis, Insights and Forecast - by Protocol

- 11. Latin America Optical Transceivers Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Protocol

- 11.1.1. Ethernet

- 11.1.2. Fiber Channel

- 11.1.3. CWDM/DWDM

- 11.1.4. FTTX

- 11.1.5. Other Protocols

- 11.2. Market Analysis, Insights and Forecast - by Data Rate

- 11.2.1. Less than 10 Gbps

- 11.2.2. 10 Gbps to 40 Gbps

- 11.2.3. 100 Gbps

- 11.2.4. Greater than 100 Gbps

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Data Center

- 11.3.2. Telecommunication

- 11.1. Market Analysis, Insights and Forecast - by Protocol

- 12. Middle East and Africa Optical Transceivers Industry Analysis, Insights and Forecast, 2020-2032

- 12.1. Market Analysis, Insights and Forecast - by Protocol

- 12.1.1. Ethernet

- 12.1.2. Fiber Channel

- 12.1.3. CWDM/DWDM

- 12.1.4. FTTX

- 12.1.5. Other Protocols

- 12.2. Market Analysis, Insights and Forecast - by Data Rate

- 12.2.1. Less than 10 Gbps

- 12.2.2. 10 Gbps to 40 Gbps

- 12.2.3. 100 Gbps

- 12.2.4. Greater than 100 Gbps

- 12.3. Market Analysis, Insights and Forecast - by Application

- 12.3.1. Data Center

- 12.3.2. Telecommunication

- 12.1. Market Analysis, Insights and Forecast - by Protocol

- 13. Competitive Analysis

- 13.1. Company Profiles

- 13.1.1 Coherent Corp (II-VI Incorporated)

- 13.1.1.1. Company Overview

- 13.1.1.2. Products

- 13.1.1.3. Company Financials

- 13.1.1.4. SWOT Analysis

- 13.1.2 Lumentum Operations LLC (Lumentum Holdings)

- 13.1.2.1. Company Overview

- 13.1.2.2. Products

- 13.1.2.3. Company Financials

- 13.1.2.4. SWOT Analysis

- 13.1.3 Broadcom Inc

- 13.1.3.1. Company Overview

- 13.1.3.2. Products

- 13.1.3.3. Company Financials

- 13.1.3.4. SWOT Analysis

- 13.1.4 Accelink Technologies

- 13.1.4.1. Company Overview

- 13.1.4.2. Products

- 13.1.4.3. Company Financials

- 13.1.4.4. SWOT Analysis

- 13.1.5 Fujitsu Optical Components Limited (Fujitsu Ltd)

- 13.1.5.1. Company Overview

- 13.1.5.2. Products

- 13.1.5.3. Company Financials

- 13.1.5.4. SWOT Analysis

- 13.1.6 Huawei Technologies Co Ltd

- 13.1.6.1. Company Overview

- 13.1.6.2. Products

- 13.1.6.3. Company Financials

- 13.1.6.4. SWOT Analysis

- 13.1.7 Source Photonics (Redview Capital)

- 13.1.7.1. Company Overview

- 13.1.7.2. Products

- 13.1.7.3. Company Financials

- 13.1.7.4. SWOT Analysis

- 13.1.8 HUBER+SUHNER Cube Optics

- 13.1.8.1. Company Overview

- 13.1.8.2. Products

- 13.1.8.3. Company Financials

- 13.1.8.4. SWOT Analysis

- 13.1.9 Smiths Interconnect (Reflex Photonics Inc )

- 13.1.9.1. Company Overview

- 13.1.9.2. Products

- 13.1.9.3. Company Financials

- 13.1.9.4. SWOT Analysis

- 13.1.10 Sumitomo Electric Industries Ltd

- 13.1.10.1. Company Overview

- 13.1.10.2. Products

- 13.1.10.3. Company Financials

- 13.1.10.4. SWOT Analysis

- 13.1.1 Coherent Corp (II-VI Incorporated)

- 13.2. Market Entropy

- 13.2.1 Company's Key Areas Served

- 13.2.2 Recent Developments

- 13.3. Company Market Share Analysis 2025

- 13.3.1 Top 5 Companies Market Share Analysis

- 13.3.2 Top 3 Companies Market Share Analysis

- 13.4. List of Potential Customers

- 14. Research Methodology

List of Figures

- Figure 1: Global Optical Transceivers Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Optical Transceivers Industry Revenue (Million), by Protocol 2025 & 2033

- Figure 3: North America Optical Transceivers Industry Revenue Share (%), by Protocol 2025 & 2033

- Figure 4: North America Optical Transceivers Industry Revenue (Million), by Data Rate 2025 & 2033

- Figure 5: North America Optical Transceivers Industry Revenue Share (%), by Data Rate 2025 & 2033

- Figure 6: North America Optical Transceivers Industry Revenue (Million), by Application 2025 & 2033

- Figure 7: North America Optical Transceivers Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: North America Optical Transceivers Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: North America Optical Transceivers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Optical Transceivers Industry Revenue (Million), by Protocol 2025 & 2033

- Figure 11: Europe Optical Transceivers Industry Revenue Share (%), by Protocol 2025 & 2033

- Figure 12: Europe Optical Transceivers Industry Revenue (Million), by Data Rate 2025 & 2033

- Figure 13: Europe Optical Transceivers Industry Revenue Share (%), by Data Rate 2025 & 2033

- Figure 14: Europe Optical Transceivers Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: Europe Optical Transceivers Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Optical Transceivers Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: Europe Optical Transceivers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Optical Transceivers Industry Revenue (Million), by Protocol 2025 & 2033

- Figure 19: Asia Optical Transceivers Industry Revenue Share (%), by Protocol 2025 & 2033

- Figure 20: Asia Optical Transceivers Industry Revenue (Million), by Data Rate 2025 & 2033

- Figure 21: Asia Optical Transceivers Industry Revenue Share (%), by Data Rate 2025 & 2033

- Figure 22: Asia Optical Transceivers Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: Asia Optical Transceivers Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Asia Optical Transceivers Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Asia Optical Transceivers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Australia and New Zealand Optical Transceivers Industry Revenue (Million), by Protocol 2025 & 2033

- Figure 27: Australia and New Zealand Optical Transceivers Industry Revenue Share (%), by Protocol 2025 & 2033

- Figure 28: Australia and New Zealand Optical Transceivers Industry Revenue (Million), by Data Rate 2025 & 2033

- Figure 29: Australia and New Zealand Optical Transceivers Industry Revenue Share (%), by Data Rate 2025 & 2033

- Figure 30: Australia and New Zealand Optical Transceivers Industry Revenue (Million), by Application 2025 & 2033

- Figure 31: Australia and New Zealand Optical Transceivers Industry Revenue Share (%), by Application 2025 & 2033

- Figure 32: Australia and New Zealand Optical Transceivers Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: Australia and New Zealand Optical Transceivers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Latin America Optical Transceivers Industry Revenue (Million), by Protocol 2025 & 2033

- Figure 35: Latin America Optical Transceivers Industry Revenue Share (%), by Protocol 2025 & 2033

- Figure 36: Latin America Optical Transceivers Industry Revenue (Million), by Data Rate 2025 & 2033

- Figure 37: Latin America Optical Transceivers Industry Revenue Share (%), by Data Rate 2025 & 2033

- Figure 38: Latin America Optical Transceivers Industry Revenue (Million), by Application 2025 & 2033

- Figure 39: Latin America Optical Transceivers Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Latin America Optical Transceivers Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Latin America Optical Transceivers Industry Revenue Share (%), by Country 2025 & 2033

- Figure 42: Middle East and Africa Optical Transceivers Industry Revenue (Million), by Protocol 2025 & 2033

- Figure 43: Middle East and Africa Optical Transceivers Industry Revenue Share (%), by Protocol 2025 & 2033

- Figure 44: Middle East and Africa Optical Transceivers Industry Revenue (Million), by Data Rate 2025 & 2033

- Figure 45: Middle East and Africa Optical Transceivers Industry Revenue Share (%), by Data Rate 2025 & 2033

- Figure 46: Middle East and Africa Optical Transceivers Industry Revenue (Million), by Application 2025 & 2033

- Figure 47: Middle East and Africa Optical Transceivers Industry Revenue Share (%), by Application 2025 & 2033

- Figure 48: Middle East and Africa Optical Transceivers Industry Revenue (Million), by Country 2025 & 2033

- Figure 49: Middle East and Africa Optical Transceivers Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Optical Transceivers Industry Revenue Million Forecast, by Protocol 2020 & 2033

- Table 2: Global Optical Transceivers Industry Revenue Million Forecast, by Data Rate 2020 & 2033

- Table 3: Global Optical Transceivers Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Optical Transceivers Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Optical Transceivers Industry Revenue Million Forecast, by Protocol 2020 & 2033

- Table 6: Global Optical Transceivers Industry Revenue Million Forecast, by Data Rate 2020 & 2033

- Table 7: Global Optical Transceivers Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global Optical Transceivers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: Global Optical Transceivers Industry Revenue Million Forecast, by Protocol 2020 & 2033

- Table 10: Global Optical Transceivers Industry Revenue Million Forecast, by Data Rate 2020 & 2033

- Table 11: Global Optical Transceivers Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 12: Global Optical Transceivers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Global Optical Transceivers Industry Revenue Million Forecast, by Protocol 2020 & 2033

- Table 14: Global Optical Transceivers Industry Revenue Million Forecast, by Data Rate 2020 & 2033

- Table 15: Global Optical Transceivers Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 16: Global Optical Transceivers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 17: Global Optical Transceivers Industry Revenue Million Forecast, by Protocol 2020 & 2033

- Table 18: Global Optical Transceivers Industry Revenue Million Forecast, by Data Rate 2020 & 2033

- Table 19: Global Optical Transceivers Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 20: Global Optical Transceivers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 21: Global Optical Transceivers Industry Revenue Million Forecast, by Protocol 2020 & 2033

- Table 22: Global Optical Transceivers Industry Revenue Million Forecast, by Data Rate 2020 & 2033

- Table 23: Global Optical Transceivers Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 24: Global Optical Transceivers Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Global Optical Transceivers Industry Revenue Million Forecast, by Protocol 2020 & 2033

- Table 26: Global Optical Transceivers Industry Revenue Million Forecast, by Data Rate 2020 & 2033

- Table 27: Global Optical Transceivers Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 28: Global Optical Transceivers Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Optical Transceivers Industry?

The projected CAGR is approximately 13.09%.

2. Which companies are prominent players in the Optical Transceivers Industry?

Key companies in the market include Coherent Corp (II-VI Incorporated), Lumentum Operations LLC (Lumentum Holdings), Broadcom Inc, Accelink Technologies, Fujitsu Optical Components Limited (Fujitsu Ltd), Huawei Technologies Co Ltd, Source Photonics (Redview Capital), HUBER+SUHNER Cube Optics, Smiths Interconnect (Reflex Photonics Inc ), Sumitomo Electric Industries Ltd.

3. What are the main segments of the Optical Transceivers Industry?

The market segments include Protocol, Data Rate, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 13.34 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Advanced Communication; Increasing Demand for Cloud-based Services.

6. What are the notable trends driving market growth?

Data Centers to the Fastest Growing Application for Optical Transceivers.

7. Are there any restraints impacting market growth?

Increase in Network Complexity.

8. Can you provide examples of recent developments in the market?

October 2023: Broadcom and Semtech Corporation announced the demonstration of a 200 G/lane optical transceiver at the ECOC 2023, featuring Semtech’s latest Fiberdge 200 G PAM4 PMDs and Broadcom’s latest generation DSP PHY and single-mode optics.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Optical Transceivers Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Optical Transceivers Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Optical Transceivers Industry?

To stay informed about further developments, trends, and reports in the Optical Transceivers Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence