Key Insights

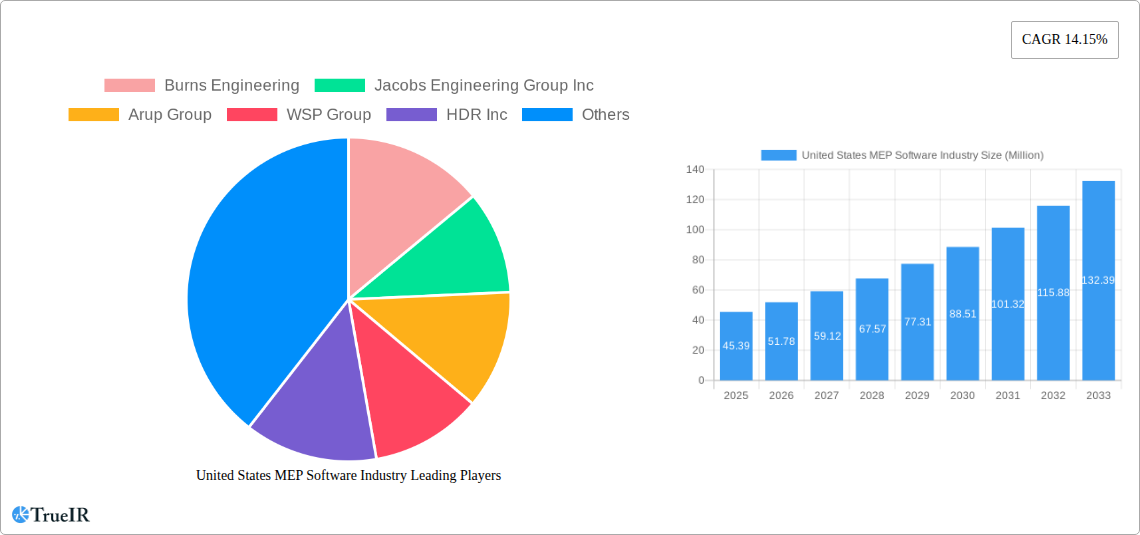

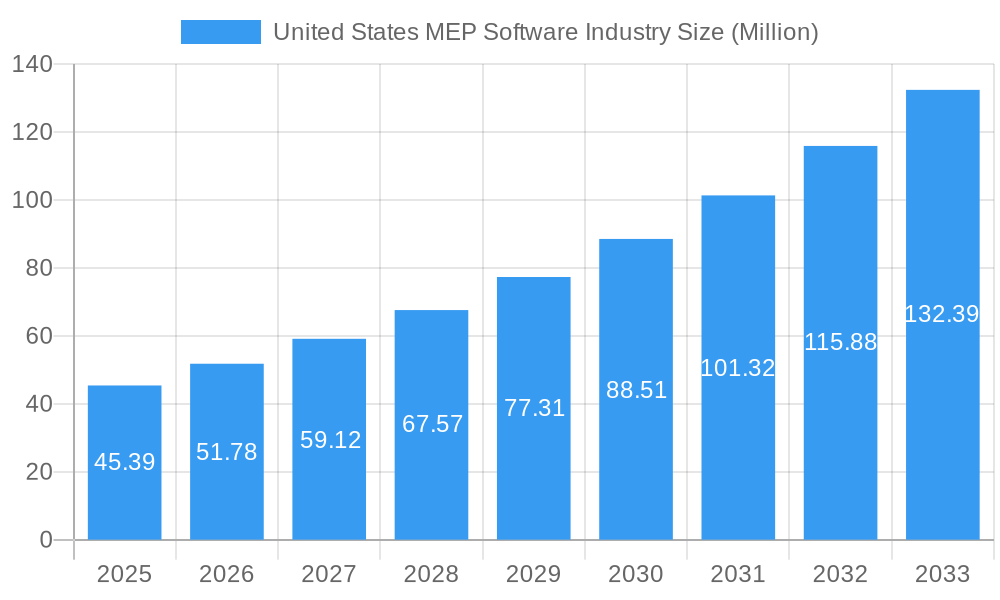

The United States MEP (Mechanical, Electrical, and Plumbing) software market is poised for significant expansion, with a current market size estimated at $45.39 million and projected to grow at a robust Compound Annual Growth Rate (CAGR) of 14.15% over the forecast period of 2025-2033. This strong growth is primarily fueled by increasing demand for energy-efficient buildings, stringent regulatory compliance for MEP systems, and the escalating adoption of Building Information Modeling (BIM) across the construction lifecycle. The "New Construction" segment is expected to lead the market, driven by ongoing infrastructure development and new commercial and residential projects. However, the "Retrofit & Renovation" segment is also witnessing substantial growth as existing buildings are upgraded to meet modern energy standards and incorporate smart building technologies. Furthermore, the increasing complexity of MEP designs and the need for enhanced collaboration among project stakeholders are compelling engineering and construction firms to invest in advanced MEP software solutions.

United States MEP Software Industry Market Size (In Million)

Key trends shaping the U.S. MEP software market include the integration of AI and machine learning for predictive maintenance and optimized system performance, the rise of cloud-based MEP software for enhanced accessibility and collaboration, and the growing importance of integrated design workflows that connect MEP design with structural and architectural elements. While the market is largely driven by positive trends, potential restraints include the initial cost of software implementation and the need for specialized training to leverage the full capabilities of these advanced tools. Major players like AECOM, Jacobs Engineering Group Inc., and WSP Group are actively innovating and expanding their offerings to cater to the evolving needs of the healthcare, commercial offices, and educational institutions sectors, which represent key end-user verticals. The U.S. market's advanced technological adoption and substantial construction activity underpin its leading position in the global MEP software landscape.

United States MEP Software Industry Company Market Share

This comprehensive report delves into the dynamic United States MEP (Mechanical, Electrical, and Plumbing) software industry, providing an in-depth analysis of market structure, trends, competitive landscape, and future outlook. Leveraging extensive market research and data analysis from the historical period of 2019–2024, with a base year of 2025 and a forecast period extending to 2033, this report equips stakeholders with actionable insights to navigate this rapidly evolving sector. The study targets industry professionals, software developers, engineering firms, construction companies, and investors seeking to capitalize on the growing demand for efficient and integrated MEP solutions.

United States MEP Software Industry Market Structure & Competitive Landscape

The United States MEP software industry exhibits a moderately concentrated market structure, characterized by the presence of large, established players alongside a growing number of innovative niche providers. Key innovation drivers include the increasing adoption of Building Information Modeling (BIM), the demand for enhanced collaboration across project stakeholders, and the growing emphasis on sustainability and energy efficiency in building design and operations. Regulatory impacts, such as evolving building codes and energy performance standards, also play a significant role in shaping software development and adoption. Product substitutes, while present in the form of manual processes or less integrated software solutions, are gradually being displaced by the comprehensive capabilities of modern MEP software. End-user segmentation reveals a diverse client base, with significant contributions from healthcare, commercial offices, and educational institutions. Mergers and acquisitions (M&A) trends indicate a strategic consolidation aimed at expanding service portfolios and market reach. For instance, the acquisition of KTA Group, Inc. by Bowman Consulting Group, Ltd. in February 2021, exemplifies this trend, bolstering expertise in MEP engineering and commissioning. The market concentration ratio is estimated to be approximately 60% for the top five players, indicating a competitive yet consolidating environment. M&A volumes have seen a steady increase, averaging 5-10 significant deals annually in recent years.

United States MEP Software Industry Market Trends & Opportunities

The United States MEP software industry is experiencing robust growth, driven by a confluence of technological advancements, evolving industry practices, and increasing demand for sophisticated building management solutions. The market size is projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from the base year of 2025 through 2033, reaching an estimated USD 4.5 billion by the end of the forecast period. Technological shifts are paramount, with the widespread integration of cloud-based platforms, artificial intelligence (AI) for predictive analysis and design optimization, and the Internet of Things (IoT) for real-time performance monitoring. Consumer preferences are increasingly leaning towards software solutions that offer seamless interoperability, enhanced visualization capabilities, and improved project lifecycle management. This includes a growing demand for tools that facilitate clash detection, energy modeling, and automated code compliance. Competitive dynamics are intensifying, with software providers focusing on developing feature-rich, user-friendly, and cost-effective solutions. Opportunities abound for companies offering specialized software for retrofits and renovations, as older buildings require modernization to meet current energy efficiency standards and occupant comfort demands. The increasing complexity of building systems and the growing emphasis on sustainable construction practices present significant opportunities for MEP software providers to offer integrated solutions that streamline design, installation, and maintenance processes. Furthermore, the rise of smart buildings and the need for data-driven decision-making in facility management will continue to fuel the demand for advanced MEP analytics and performance optimization tools. The market penetration rate for integrated MEP software solutions is expected to reach over 70% by 2033, up from approximately 50% in the historical period.

Dominant Markets & Segments in United States MEP Software Industry

Within the United States, the MEP software industry demonstrates significant dominance across specific regions and end-user verticals, driven by infrastructure development, supportive government policies, and evolving market demands. The Commercial Offices segment consistently emerges as a leading market, fueled by new construction projects and extensive renovation activities aimed at creating modern, energy-efficient, and technologically advanced workspaces. Factors such as corporate sustainability initiatives and the demand for flexible office layouts contribute to this dominance. The Healthcare sector also represents a substantial and growing market, driven by the need for highly reliable and precisely controlled MEP systems in hospitals and specialized medical facilities. Stringent regulations and the critical nature of these environments necessitate sophisticated software for design, commissioning, and ongoing maintenance.

- Leading Regions: The Northeast and the West Coast regions of the United States are identified as dominant markets due to their high concentration of commercial real estate development, significant investment in infrastructure, and proactive adoption of advanced technologies.

- Dominant Segments by Type:

- New Construction: Continues to be a primary driver, with large-scale projects requiring comprehensive MEP design and management.

- Retrofit & Renovation: This segment is experiencing accelerated growth as aging infrastructure is updated to meet modern energy codes and occupant comfort expectations.

- Dominant Segments by End-user Vertical:

- Commercial Offices: High volume of new builds and extensive renovations.

- Healthcare: Critical infrastructure demanding precision and reliability, driving adoption of advanced software.

- Educational Institutions: Ongoing investment in campus upgrades and new facilities.

The robust growth in New Construction is propelled by ongoing urbanization and the demand for modern infrastructure across all sectors. Simultaneously, the Retrofit & Renovation segment is experiencing a significant surge due to an increasing focus on energy efficiency upgrades and the modernization of aging building stock. Government incentives and stricter environmental regulations are further bolstering the adoption of MEP software in this segment. The Commissioning Activity segment is also gaining prominence as building owners and operators prioritize ensuring that MEP systems function as designed, leading to optimized performance and reduced operational costs.

United States MEP Software Industry Product Analysis

MEP software innovations are fundamentally transforming building design and operational efficiency. Key advancements include the seamless integration of Building Information Modeling (BIM) with sophisticated analytical tools, enabling detailed clash detection, energy performance simulations, and predictive maintenance. Cloud-based platforms are enhancing collaboration and accessibility for project teams, regardless of their geographic location. Competitive advantages are being realized through features like automated code compliance checks, AI-driven design optimization, and real-time performance monitoring enabled by IoT integration. The market fit for these products lies in their ability to reduce design errors, accelerate project timelines, optimize energy consumption, and ultimately lower the total cost of ownership for building owners.

Key Drivers, Barriers & Challenges in United States MEP Software Industry

The United States MEP software industry is propelled by several key drivers. Technologically, the widespread adoption of BIM and the increasing sophistication of data analytics and AI are transforming design and operational processes. Economically, the continuous investment in infrastructure development and the growing demand for sustainable and energy-efficient buildings create a strong market pull. Policy-driven factors, such as evolving building codes and government incentives for green building practices, further stimulate market growth. For example, the USD 3.5 billion Dallas Independent School District (DISD) 2020 Bond Program, managed by AECOM, highlights significant investment in educational facilities.

However, the industry faces significant challenges and restraints. High upfront costs of advanced software solutions can be a barrier for smaller firms. Regulatory complexities and the need for continuous software updates to comply with evolving standards present ongoing hurdles. Supply chain issues, particularly concerning the integration of hardware components with software, can also impact project timelines and costs. Competitive pressures from both established players and emerging disruptors necessitate constant innovation and value proposition refinement.

Growth Drivers in the United States MEP Software Industry Market

The growth of the United States MEP software industry is significantly influenced by several factors. Technological advancements, particularly the maturation of BIM technologies and the increasing integration of AI and machine learning for design optimization and predictive analytics, are key drivers. Economic factors, such as sustained investment in commercial and residential construction, coupled with government initiatives promoting energy efficiency and sustainability, are also critical. For instance, federal and state-level incentives for green building practices directly boost the demand for MEP software that facilitates compliance and performance monitoring. Furthermore, the growing complexity of building systems, especially in sectors like healthcare and data centers, necessitates sophisticated software solutions for accurate design, installation, and maintenance.

Challenges Impacting United States MEP Software Industry Growth

Several challenges can impede the growth trajectory of the United States MEP software industry. One significant barrier is the steep learning curve and initial investment required for advanced MEP software adoption, which can be prohibitive for small to medium-sized enterprises (SMEs). Interoperability issues between different software platforms and legacy systems continue to pose a challenge, leading to workflow inefficiencies. Data security and privacy concerns are also becoming increasingly critical as more project data is stored and shared in the cloud. Furthermore, a shortage of skilled professionals who can effectively utilize complex MEP software tools can create bottlenecks in project execution. The evolving regulatory landscape, while a driver, also presents a challenge as software providers must continuously adapt their solutions to comply with new codes and standards.

Key Players Shaping the United States MEP Software Industry Market

- Burns Engineering

- Jacobs Engineering Group Inc

- Arup Group

- WSP Group

- HDR Inc

- Stantec Inc

- MEP Engineering

- Wiley Wilson

- Affiliated Engineers Inc

- AHA Consulting

- AECOM

- Macro Services

Significant United States MEP Software Industry Industry Milestones

- February 2021: Bowman Consulting Group, Ltd. acquired KTA Group, Inc. This strategic acquisition significantly broadened Bowman's service offerings, particularly in MEP engineering, commissioning, third-party plan review, and lighting design, reinforcing its market position and capabilities.

- May 2021: AECOM was selected to provide program management services for Phase 1 of the USD 3.5 billion Dallas Independent School District (DISD) 2020 Bond Program. This contract, AECOM's fourth consecutive with DISD, underscores the company's expertise in overseeing large-scale educational facility construction and upgrades, highlighting the critical role of program management in complex MEP projects.

Future Outlook for United States MEP Software Industry Market

The future outlook for the United States MEP software industry is exceptionally promising, driven by continuous technological innovation and an increasing imperative for efficient, sustainable, and resilient building infrastructure. The growing adoption of AI and machine learning will lead to more intelligent design processes, predictive maintenance capabilities, and optimized energy management. The rise of smart cities and the demand for integrated building systems will further fuel the need for sophisticated MEP software solutions that facilitate connectivity and data exchange. Opportunities for market expansion lie in developing specialized software for emerging sectors like data centers and advanced manufacturing facilities. The ongoing emphasis on decarbonization and net-zero building goals will also propel the demand for software that can accurately model and verify energy performance, making it an indispensable tool for the future of construction and building management.

United States MEP Software Industry Segmentation

-

1. Type

- 1.1. New Construction

- 1.2. Retrofit & Renovation

- 1.3. Commissioning Activity

- 1.4. Other Types

-

2. End-user Vertical

- 2.1. Healthcare

- 2.2. Commercial Offices

- 2.3. Educational Institutions

- 2.4. Public Spaces and Institutions

- 2.5. Industrial establishments & Warehouses

- 2.6. Other Co

United States MEP Software Industry Segmentation By Geography

- 1. United States

United States MEP Software Industry Regional Market Share

Geographic Coverage of United States MEP Software Industry

United States MEP Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.15% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. New Construction

- 5.1.2. Retrofit & Renovation

- 5.1.3. Commissioning Activity

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 5.2.1. Healthcare

- 5.2.2. Commercial Offices

- 5.2.3. Educational Institutions

- 5.2.4. Public Spaces and Institutions

- 5.2.5. Industrial establishments & Warehouses

- 5.2.6. Other Co

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. United States MEP Software Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. New Construction

- 6.1.2. Retrofit & Renovation

- 6.1.3. Commissioning Activity

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by End-user Vertical

- 6.2.1. Healthcare

- 6.2.2. Commercial Offices

- 6.2.3. Educational Institutions

- 6.2.4. Public Spaces and Institutions

- 6.2.5. Industrial establishments & Warehouses

- 6.2.6. Other Co

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Burns Engineering

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Jacobs Engineering Group Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Arup Group

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 WSP Group

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 HDR Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 Stantec Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 MEP Engineering

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Wiley Wilson*List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Affiliated Engineers Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 AHA Consulting

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 AECOM

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 Macro Services

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.1 Burns Engineering

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: United States MEP Software Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: United States MEP Software Industry Share (%) by Company 2025

List of Tables

- Table 1: United States MEP Software Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: United States MEP Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 3: United States MEP Software Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: United States MEP Software Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 5: United States MEP Software Industry Revenue Million Forecast, by End-user Vertical 2020 & 2033

- Table 6: United States MEP Software Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States MEP Software Industry?

The projected CAGR is approximately 14.15%.

2. Which companies are prominent players in the United States MEP Software Industry?

Key companies in the market include Burns Engineering, Jacobs Engineering Group Inc, Arup Group, WSP Group, HDR Inc, Stantec Inc, MEP Engineering, Wiley Wilson*List Not Exhaustive, Affiliated Engineers Inc, AHA Consulting, AECOM, Macro Services.

3. What are the main segments of the United States MEP Software Industry?

The market segments include Type, End-user Vertical.

4. Can you provide details about the market size?

The market size is estimated to be USD 45.39 Million as of 2022.

5. What are some drivers contributing to market growth?

Growing Emphasis on Outsourcing of MEP Services to Focus on Core Offering; Steady Demand from Commercial and Healthcare Institutions; Evolving Business Models and Nature of Collaboration between Firms and Service Vendors.

6. What are the notable trends driving market growth?

New Construction to Drive the Market Growth.

7. Are there any restraints impacting market growth?

Operational Challenges in High Market Concentration and Growing Demand for End-to-end Offering Affect Smaller Firms.

8. Can you provide examples of recent developments in the market?

February 2021 - Bowman Consulting Group, Ltd., acquired KTA Group, Inc. KTA is a forty-person engineering firm with core expertise in mechanical, electrical, and plumbing engineering, commissioning third-party plan review, and lighting design. The move supports Bowman's continued growth and substantially broadens its scope of service offerings.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States MEP Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States MEP Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States MEP Software Industry?

To stay informed about further developments, trends, and reports in the United States MEP Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence