Key Insights

The zero-emission airplane market is poised for significant growth, projected to reach a substantial size driven by escalating environmental concerns and government regulations aimed at reducing aviation's carbon footprint. The market's Compound Annual Growth Rate (CAGR) of 7.02% from 2019 to 2024 indicates a steady upward trajectory, expected to continue throughout the forecast period (2025-2033). This expansion is fueled by increasing investments in research and development of electric and hydrogen-powered aircraft, alongside advancements in battery technology and fuel cell efficiency. Key market segments, including commercial and general aviation and military aviation, are witnessing rising demand for sustainable flight solutions, creating opportunities for established aerospace giants and innovative startups alike. The integration of electric and hybrid-electric propulsion systems is a major driver, offering solutions with reduced noise pollution and operational costs compared to traditional aircraft. However, challenges remain, including the limited range of current electric aircraft, high initial investment costs associated with developing and deploying new technologies, and the need for widespread infrastructure development to support the charging and refueling of these aircraft.

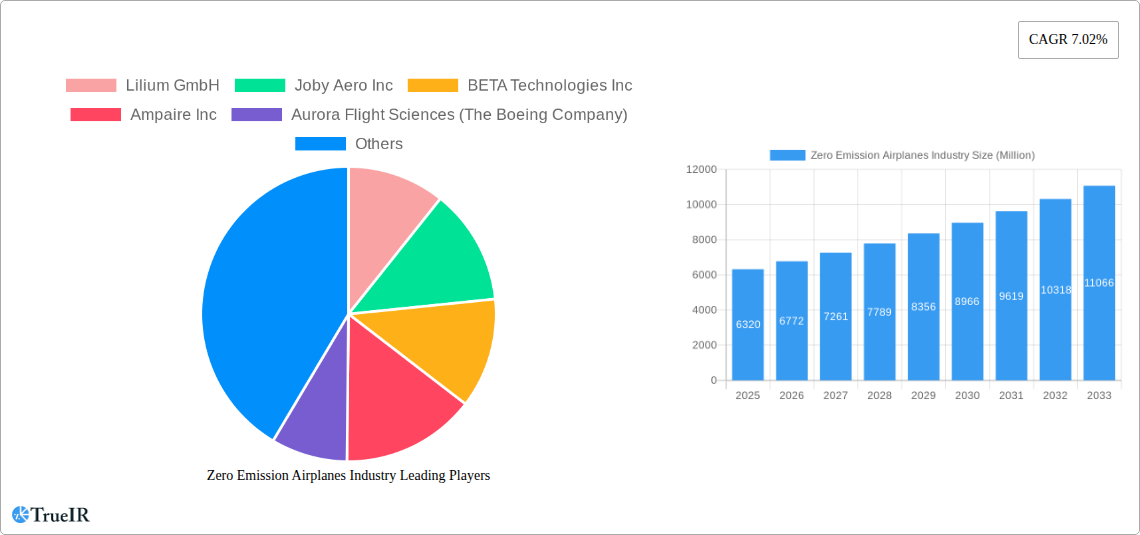

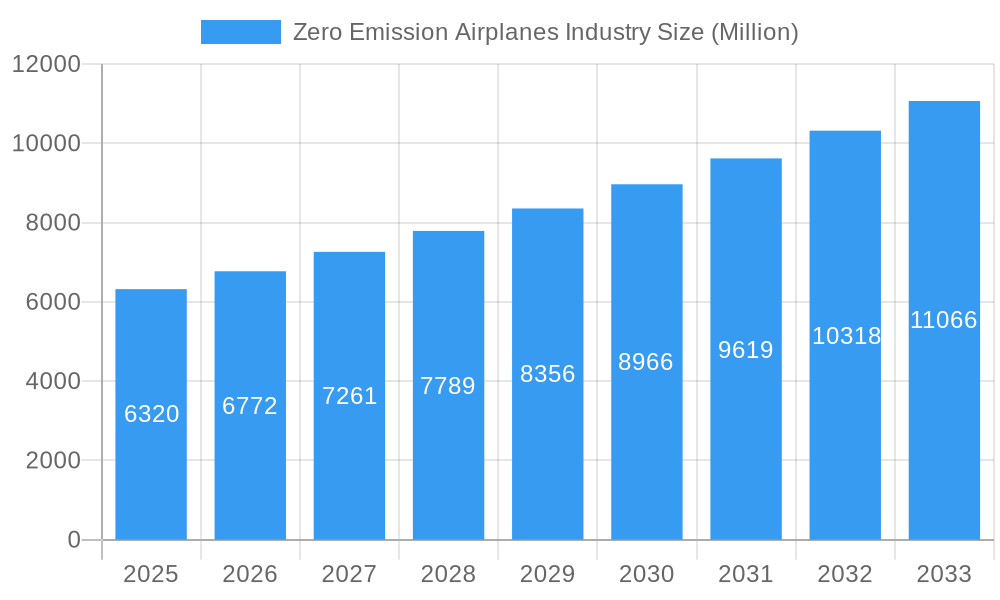

Zero Emission Airplanes Industry Market Size (In Billion)

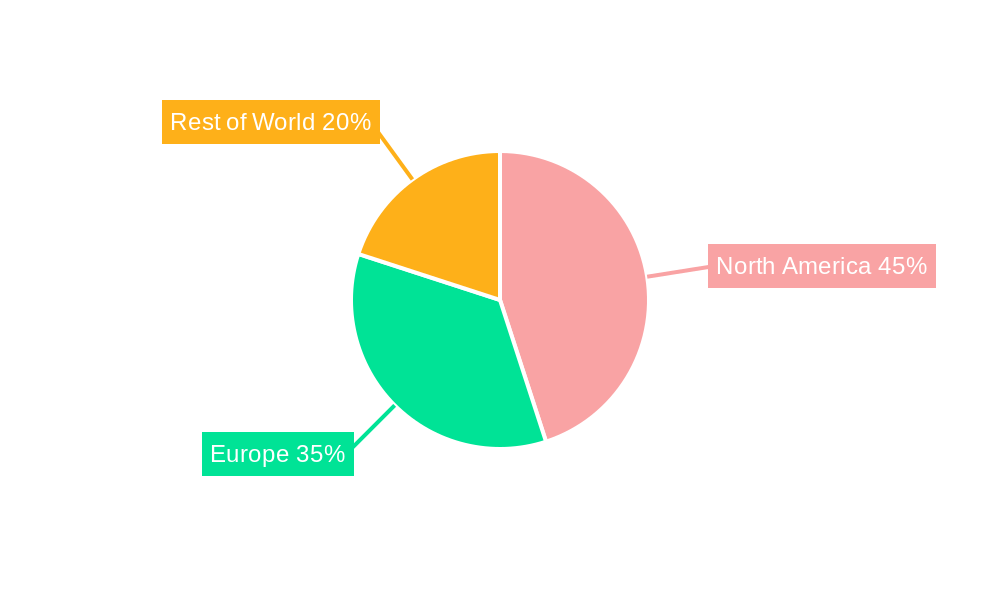

The geographical distribution of the market reveals substantial regional variations. While North America and Europe currently hold significant market share due to strong technological advancements and regulatory support, the Rest of the World segment is projected to witness substantial growth driven by increasing demand from emerging economies and government initiatives to promote sustainable aviation. Competition is fierce, with both established players like Airbus SE and Boeing (through Aurora Flight Sciences) alongside emerging innovators like Lilium and Joby Aero vying for market dominance. The successful commercialization of zero-emission aircraft will hinge on overcoming technological limitations, securing substantial investments, and establishing robust regulatory frameworks that support the wider adoption of sustainable aviation technologies. The strategic partnerships between aerospace companies and energy providers are essential in accelerating the market's transition toward a cleaner future for air travel. This transition will require overcoming hurdles in battery technology and energy storage to expand the range and capacity of zero-emission aircraft, making them a viable alternative to traditional options.

Zero Emission Airplanes Industry Company Market Share

Zero Emission Airplanes Industry: A Comprehensive Market Report (2019-2033)

This dynamic report provides an in-depth analysis of the burgeoning Zero Emission Airplanes industry, projecting a market valued at $XX Million by 2033. Leveraging extensive research and data from 2019-2024, with a base year of 2025, this report offers invaluable insights for investors, industry professionals, and policymakers. It covers key players like Lilium GmbH, Joby Aero Inc, and Airbus SE, analyzing market trends, competitive landscapes, and future growth potential. This report is crucial for understanding the trajectory of sustainable aviation and making informed business decisions.

Zero Emission Airplanes Industry Market Structure & Competitive Landscape

The zero-emission airplanes market is characterized by a complex interplay of emerging technologies, stringent regulations, and intense competition among established aerospace giants and innovative startups. Market concentration is currently low, with a fragmented landscape featuring numerous players vying for market share. However, consolidation through mergers and acquisitions (M&A) is expected to increase, particularly as larger companies seek to acquire smaller innovative firms with specialized technologies. The xx Million spent on M&A activities in the past five years indicate this trend. Innovation drivers include advancements in battery technology, electric motor design, and hydrogen fuel cell development. Stringent environmental regulations, particularly concerning carbon emissions, are significantly shaping the industry's trajectory, creating both challenges and opportunities. Product substitutes, such as high-speed rail and improved ground transportation, present competition, particularly for short-haul flights. End-user segmentation is primarily divided into commercial and general aviation, and military aviation, with each segment presenting unique requirements and market dynamics.

- High fragmentation: Numerous players with varying technological capabilities and market reach.

- Growing M&A activity: Larger companies actively acquiring innovative smaller businesses.

- Stringent regulations: Environmental regulations drive innovation and market growth.

- Product substitution: Competition from alternative transportation options.

- End-user segmentation: Commercial, general, and military aviation segments with distinct needs.

Zero Emission Airplanes Industry Market Trends & Opportunities

The zero-emission airplanes market is experiencing exponential growth, driven by a confluence of factors. The market size is projected to reach $XX Million by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). This remarkable expansion is fueled by increasing concerns about climate change, supportive government policies, and continuous technological advancements in electric propulsion systems and hydrogen fuel cells. Consumer preferences are shifting towards sustainable travel options, creating strong demand for environmentally friendly air travel. The market penetration rate is expected to significantly increase as the technology matures and becomes more cost-effective. The competitive landscape is dynamic, with established aerospace manufacturers and emerging startups innovating and collaborating to lead this technological shift. Opportunities abound for companies that can successfully navigate the regulatory landscape, secure funding, and develop reliable and cost-competitive zero-emission aircraft.

Dominant Markets & Segments in Zero Emission Airplanes Industry

The Commercial and General Aviation segment is currently the dominant market within the zero-emission airplane industry, accounting for approximately xx% of the total market value in 2025. This is attributed to:

- Growing demand for short-haul flights: Electric aircraft are well-suited for shorter routes, significantly reducing carbon emissions compared to traditional aircraft.

- Technological advancements: Continuous improvements in battery technology and electric propulsion systems are making electric aircraft more viable for commercial applications.

- Government incentives: Many countries are offering financial incentives and subsidies to stimulate the adoption of electric aircraft.

- Rising environmental awareness: Consumers are becoming more environmentally conscious, leading to a higher demand for sustainable travel solutions.

While the Military Aviation segment is currently smaller, it shows significant future potential, driven by the increasing demand for environmentally friendly and quiet aircraft for various military operations. Key growth drivers in this segment include:

- Technological advancements: Development of high-power electric propulsion systems capable of supporting heavy military aircraft.

- Operational benefits: Electric aircraft offer several advantages, including reduced noise pollution and operational costs.

- Environmental considerations: The military is increasingly focusing on minimizing its environmental footprint.

- Government investment: Increased government funding for the development of military electric aircraft.

Zero Emission Airplanes Industry Product Analysis

The zero-emission airplane industry showcases diverse product innovations, ranging from all-electric aircraft powered by advanced battery technology to hybrid-electric and hydrogen-fuel-cell-powered planes. These advancements offer varied applications, including short-haul commercial flights, urban air mobility (UAM), and military operations. Key competitive advantages are determined by factors such as flight range, payload capacity, operational costs, and technological maturity. The market is experiencing a rapid evolution, with new entrants continually pushing technological boundaries and introducing innovative aircraft designs to cater to diverse market segments.

Key Drivers, Barriers & Challenges in Zero Emission Airplanes Industry

Key Drivers: Technological breakthroughs in battery technology, electric motors, and hydrogen fuel cells are major drivers. Government incentives and supportive policies, along with rising environmental awareness among consumers, are also accelerating adoption. For example, the $XX Million in government funding allocated to electric aircraft research and development demonstrates strong commitment.

Challenges: The high cost of battery technology remains a significant barrier, impacting aircraft affordability. The limited flight range of current electric aircraft compared to conventional ones restricts their applicability to long-haul routes. Regulatory hurdles surrounding airworthiness certification and operational safety also present substantial obstacles. Supply chain disruptions and competition from established aerospace manufacturers also impede growth. These issues affect the growth rate negatively by approximately XX%.

Growth Drivers in the Zero Emission Airplanes Industry Market

Technological advancements, particularly in battery technology and electric propulsion systems, are key drivers of growth. Government support, including funding and regulatory frameworks that encourage electric aviation, is crucial. The rising consumer demand for sustainable air travel and reduced noise pollution further fuels market expansion.

Challenges Impacting Zero Emission Airplanes Industry Growth

High initial costs of electric and hybrid-electric aircraft, the limited range of electric aircraft compared to traditional planes, and the need for extensive charging infrastructure present considerable challenges. Complex certification processes and regulatory hurdles create significant barriers to market entry, further slowing adoption rates. Competition from established aerospace manufacturers possessing greater financial resources and experience also poses a significant challenge.

Key Players Shaping the Zero Emission Airplanes Industry Market

- Lilium GmbH

- Joby Aero Inc

- BETA Technologies Inc

- Ampaire Inc

- Aurora Flight Sciences (The Boeing Company)

- Avinor AS

- Wright Electric

- Airbus SE

- Evektor spol s r o

- PIPISTREL d o o

- Equator Aircraft AS

- Rolls-Royce plc

- Heart Aerospace

- ZeroAvia Inc

- Eviation

- NASA

- Bye Aerospace

Significant Zero Emission Airplanes Industry Industry Milestones

- July 2021: Airbus Helicopters conducted the full-scale demonstrator flight of its electric helicopter, CityAirbus. This milestone demonstrated the feasibility of electric propulsion for larger aircraft.

- July 2021: Beta Technologies completed the longest crewed test flight of its Alia aircraft (205 miles), showcasing significant progress in battery technology and electric flight range.

Future Outlook for Zero Emission Airplanes Industry Market

The future outlook for the zero-emission airplanes industry is exceptionally positive. Continued technological advancements, particularly in battery energy density and hydrogen fuel cell efficiency, will significantly enhance the range and payload capacity of electric and hydrogen aircraft. Supportive government policies, increasing environmental awareness, and a growing demand for sustainable transportation solutions are key catalysts for sustained market growth. This convergence of factors indicates substantial market expansion and significant opportunities for innovation and investment in the coming years.

Zero Emission Airplanes Industry Segmentation

-

1. Application

- 1.1. Commercial and General Aviation

- 1.2. Military Aviation

Zero Emission Airplanes Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Rest of World

Zero Emission Airplanes Industry Regional Market Share

Geographic Coverage of Zero Emission Airplanes Industry

Zero Emission Airplanes Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.02% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Commercial and General Aviation

- 5.1.2. Military Aviation

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. North America

- 5.2.2. Europe

- 5.2.3. Rest of World

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Zero Emission Airplanes Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Commercial and General Aviation

- 6.1.2. Military Aviation

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Zero Emission Airplanes Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Commercial and General Aviation

- 7.1.2. Military Aviation

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Zero Emission Airplanes Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Commercial and General Aviation

- 8.1.2. Military Aviation

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Rest of World Zero Emission Airplanes Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Commercial and General Aviation

- 9.1.2. Military Aviation

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Lilium GmbH

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 Joby Aero Inc

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 BETA Technologies Inc

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 Ampaire Inc

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Aurora Flight Sciences (The Boeing Company)

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 Avinor AS

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Wright Electric

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Airbus SE

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 Evektor spol s r o

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 PIPISTREL d o o

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 Equator Aircraft AS

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.12 Rolls-Royce plc

- 10.1.12.1. Company Overview

- 10.1.12.2. Products

- 10.1.12.3. Company Financials

- 10.1.12.4. SWOT Analysis

- 10.1.13 Heart Aerospace

- 10.1.13.1. Company Overview

- 10.1.13.2. Products

- 10.1.13.3. Company Financials

- 10.1.13.4. SWOT Analysis

- 10.1.14 ZeroAvia Inc

- 10.1.14.1. Company Overview

- 10.1.14.2. Products

- 10.1.14.3. Company Financials

- 10.1.14.4. SWOT Analysis

- 10.1.15 Eviation

- 10.1.15.1. Company Overview

- 10.1.15.2. Products

- 10.1.15.3. Company Financials

- 10.1.15.4. SWOT Analysis

- 10.1.16 NASA

- 10.1.16.1. Company Overview

- 10.1.16.2. Products

- 10.1.16.3. Company Financials

- 10.1.16.4. SWOT Analysis

- 10.1.17 Bye Aerospace

- 10.1.17.1. Company Overview

- 10.1.17.2. Products

- 10.1.17.3. Company Financials

- 10.1.17.4. SWOT Analysis

- 10.1.1 Lilium GmbH

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: Global Zero Emission Airplanes Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: North America Zero Emission Airplanes Industry Revenue (Million), by Application 2025 & 2033

- Figure 3: North America Zero Emission Airplanes Industry Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Zero Emission Airplanes Industry Revenue (Million), by Country 2025 & 2033

- Figure 5: North America Zero Emission Airplanes Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: Europe Zero Emission Airplanes Industry Revenue (Million), by Application 2025 & 2033

- Figure 7: Europe Zero Emission Airplanes Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: Europe Zero Emission Airplanes Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Europe Zero Emission Airplanes Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Rest of World Zero Emission Airplanes Industry Revenue (Million), by Application 2025 & 2033

- Figure 11: Rest of World Zero Emission Airplanes Industry Revenue Share (%), by Application 2025 & 2033

- Figure 12: Rest of World Zero Emission Airplanes Industry Revenue (Million), by Country 2025 & 2033

- Figure 13: Rest of World Zero Emission Airplanes Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Zero Emission Airplanes Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 2: Global Zero Emission Airplanes Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 3: Global Zero Emission Airplanes Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Zero Emission Airplanes Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 5: Global Zero Emission Airplanes Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 6: Global Zero Emission Airplanes Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: Global Zero Emission Airplanes Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global Zero Emission Airplanes Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Zero Emission Airplanes Industry?

The projected CAGR is approximately 7.02%.

2. Which companies are prominent players in the Zero Emission Airplanes Industry?

Key companies in the market include Lilium GmbH, Joby Aero Inc, BETA Technologies Inc, Ampaire Inc, Aurora Flight Sciences (The Boeing Company), Avinor AS, Wright Electric, Airbus SE, Evektor spol s r o, PIPISTREL d o o, Equator Aircraft AS, Rolls-Royce plc, Heart Aerospace, ZeroAvia Inc, Eviation, NASA, Bye Aerospace.

3. What are the main segments of the Zero Emission Airplanes Industry?

The market segments include Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 6.32 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Evolving Emissions Regulations Driving the Pace of Development.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

In July 2021, Airbus Helicopters conducted the full-scale demonstrator flight of its electric helicopter. CityAirbus has a multi-copter configuration that features four ducted high-lift propulsion units. Its eight propellers are driven by electric motors at around 950 rpm to ensure a low acoustic footprint.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Zero Emission Airplanes Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Zero Emission Airplanes Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Zero Emission Airplanes Industry?

To stay informed about further developments, trends, and reports in the Zero Emission Airplanes Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence