Key Insights

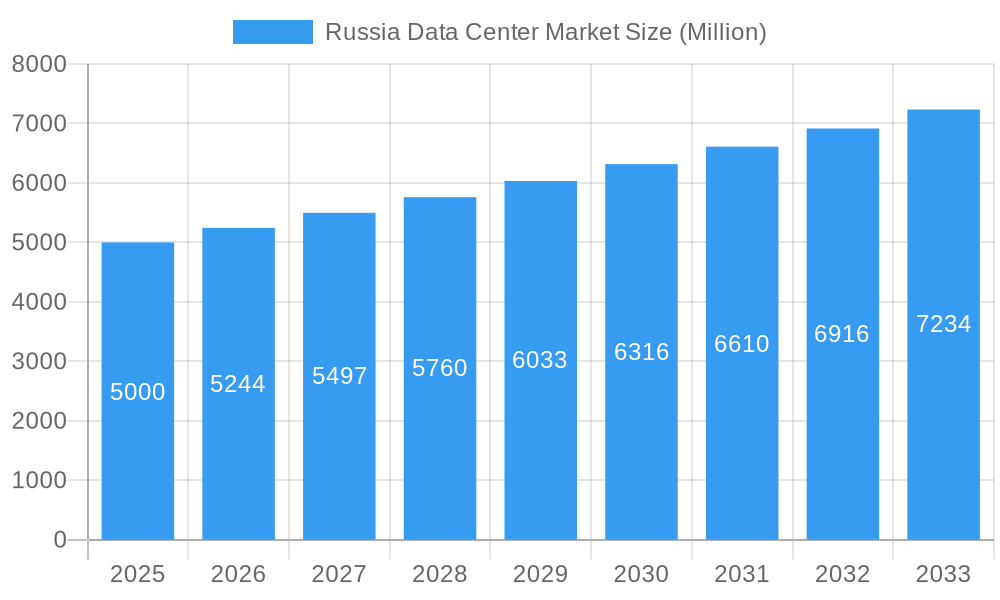

The Russian data center market is poised for significant growth, projected to reach a substantial XX million by 2033, driven by a compound annual growth rate (CAGR) of 4.87% from 2025. This expansion is fueled by robust demand from key sectors such as BFSI, cloud services, e-commerce, and government initiatives aimed at digital transformation and data localization. The increasing adoption of cloud computing, coupled with the burgeoning digital economy in Russia, necessitates greater colocation capacity. Hyperscale and wholesale colocation models are expected to lead this demand, catering to the evolving needs of large enterprises and cloud providers. Furthermore, the government's emphasis on data sovereignty and security is a critical driver, pushing organizations to invest in domestic data center infrastructure. The market's development is also supported by investments in modernization and expansion of existing facilities, particularly in major hubs like Moscow.

Russia Data Center Market Market Size (In Billion)

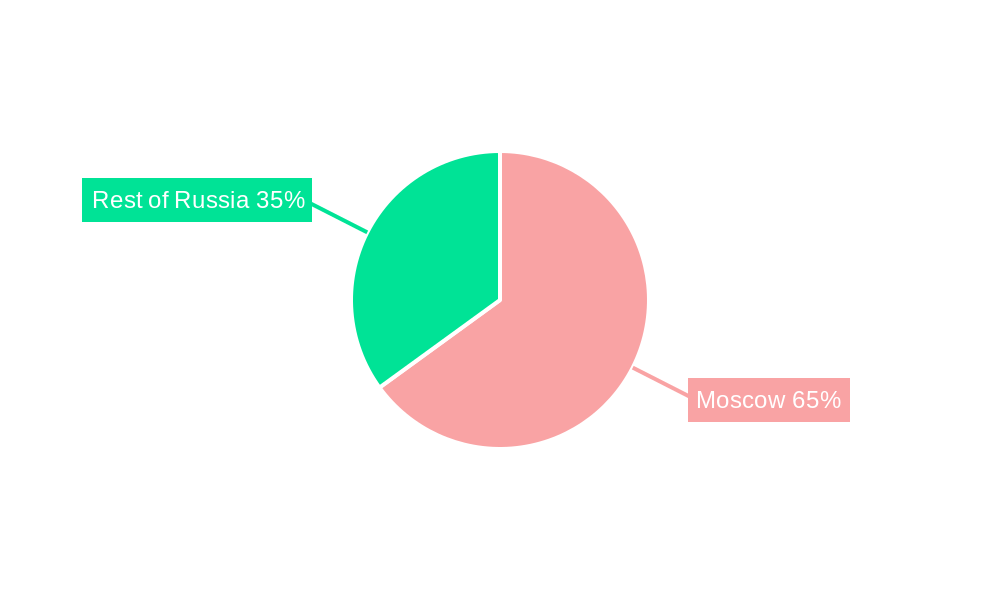

The Russian data center landscape is characterized by a diverse range of players, including established telecommunications companies like Rostelecom and MTS PJSC, alongside specialized colocation providers such as Selectel Ltd and Yandex Cloud LLC. The market segmentation reveals a strong focus on large and massive data center sizes, with Tier 3 and Tier 4 facilities becoming increasingly prevalent due to their reliability and advanced capabilities. While the "Rest of Russia" is expected to witness considerable growth as digital infrastructure expands beyond the capital, Moscow will continue to be the dominant market. Potential restraints could include geopolitical factors influencing foreign investment and technology access, as well as the ongoing need for skilled personnel to manage and operate sophisticated data center environments. However, the overarching trend of digitalization across all sectors strongly underpins the sustained positive outlook for the Russian data center market.

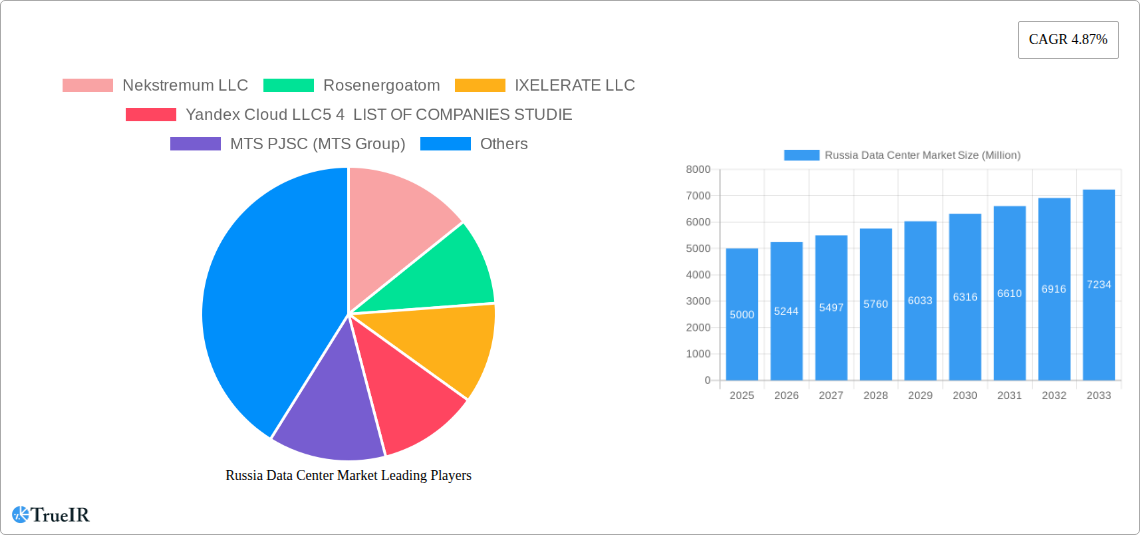

Russia Data Center Market Company Market Share

This in-depth report provides a dynamic and SEO-optimized analysis of the Russia Data Center Market, leveraging high-volume keywords for maximum search visibility and engagement. Covering the period from 2019 to 2033, with a base year of 2025, this report offers unparalleled insights into market structure, trends, dominant segments, key players, and future potential. Discover the critical factors driving the expansion of Russia's digital infrastructure, from burgeoning hyperscale deployments to the increasing demand for robust colocation services.

Russia Data Center Market Market Structure & Competitive Landscape

The Russia Data Center Market is characterized by a moderate level of concentration, with a growing influence of independent colocation providers alongside state-backed entities and major tech players. Innovation is primarily driven by the increasing demand for high-density computing, advanced cooling solutions, and the adoption of Tier IV infrastructure. Regulatory impacts are significant, with government initiatives aimed at ensuring data localization and digital sovereignty influencing investment and operational strategies. Product substitutes are limited, primarily revolving around on-premise solutions for highly sensitive data, but the cost-effectiveness and scalability of data center services continue to drive market preference. End-user segmentation reveals a strong presence of BFSI, Cloud, E-Commerce, and Telecom sectors, consistently driving demand. M&A trends are expected to accelerate as larger players seek to consolidate market share and expand their geographical and service offerings. Key metrics include a projected market concentration ratio of approximately 60% among the top five players by 2025, with an estimated M&A volume of over 500 Million in the forecast period.

Russia Data Center Market Market Trends & Opportunities

The Russia Data Center Market is poised for significant expansion, driven by a confluence of technological advancements and evolving market demands. The market is projected to witness a robust Compound Annual Growth Rate (CAGR) of approximately 12% from 2025 to 2033, fueled by the increasing adoption of cloud computing services across all industry verticals. This surge in cloud adoption is directly translating into a greater need for scalable, reliable, and secure data center infrastructure. Consumer preferences are shifting towards highly available and resilient data center solutions, with a growing emphasis on sustainability and energy efficiency. Competitive dynamics are intensifying, with both domestic and international players vying for market share. Opportunities abound for providers capable of offering specialized solutions, such as edge computing facilities and high-performance computing (HPC) environments, to cater to niche but rapidly growing demands. The penetration of data center services is expected to rise from around 15% in 2025 to an estimated 25% by 2033, indicating substantial room for growth. The market size is projected to grow from an estimated 1,500 Million in 2025 to over 3,500 Million by the end of the forecast period, driven by significant investments in new capacity and upgrades to existing facilities. The ongoing digital transformation initiatives across various sectors, coupled with the increasing reliance on data-intensive applications, are creating a fertile ground for sustained market growth and innovation. The development of smart cities and the Internet of Things (IoT) ecosystem are also expected to contribute significantly to this upward trajectory, creating new avenues for data processing and storage.

Dominant Markets & Segments in Russia Data Center Market

The Moscow region stands as the dominant market within Russia's data center landscape, driven by its concentration of businesses, government agencies, and a highly developed digital ecosystem. Its sophisticated infrastructure and proximity to major connectivity hubs make it the primary choice for hyperscale and enterprise deployments. Among data center sizes, Mega and Large facilities are experiencing the most significant growth, accommodating the escalating demands of cloud providers and large enterprises seeking substantial capacity. In terms of Tier Type, Tier 3 data centers represent the largest segment, offering a balance of reliability and cost-effectiveness for a broad range of applications. However, the demand for Tier 4 facilities is rapidly increasing, particularly from critical sectors like BFSI and government, seeking uninterrupted operations and the highest levels of resilience. By colocation type, Hyperscale deployments are leading the charge in terms of capacity expansion, driven by global cloud giants establishing a strong presence. Wholesale colocation also continues to be a significant segment, catering to large enterprises with specific infrastructure needs. The Cloud and BFSI end-user segments are the primary growth engines, necessitating advanced processing power, low latency, and stringent security measures. The Telecom sector is also a major contributor, requiring extensive network infrastructure and reliable data storage.

- Dominant Region: Moscow's extensive business network and advanced connectivity create unparalleled demand.

- Growth in Data Center Size: Mega and Large facilities are expanding to meet increasing colocation needs.

- Tier Type Demand: Tier 3 remains dominant, with a rapid surge in demand for Tier 4 for critical applications.

- Colocation Trends: Hyperscale and Wholesale colocation are leading capacity expansion.

- Key End-User Segments: Cloud and BFSI are driving significant growth, followed by Telecom.

Russia Data Center Market Product Analysis

The Russia Data Center Market is witnessing a surge in product innovation, focusing on enhancing efficiency, scalability, and resilience. This includes the development of modular data center solutions for rapid deployment and the adoption of advanced cooling technologies like liquid cooling to support high-density server configurations. Furthermore, there's a growing emphasis on software-defined infrastructure and integrated management platforms to optimize resource utilization and operational efficiency. Competitive advantages are being built around robust security features, compliance with data localization mandates, and superior uptime guarantees. The market fit for these innovations is evident in the increasing adoption by BFSI, Cloud, and E-Commerce sectors, which demand cutting-edge solutions to maintain a competitive edge.

Key Drivers, Barriers & Challenges in Russia Data Center Market

Key Drivers: The Russia Data Center Market is propelled by several key factors, including rapid digitalization across industries, substantial investments in cloud infrastructure by major tech companies, and government initiatives promoting data localization and domestic technology development. The growing adoption of AI and Big Data analytics further fuels demand for high-performance computing and storage.

Barriers & Challenges: Significant barriers include geopolitical uncertainties impacting international investment and supply chains, alongside the complex regulatory landscape. The availability of skilled IT professionals and the cost of energy can also pose challenges. Supply chain disruptions for specialized hardware and the need for substantial upfront capital investment for new facilities present further constraints.

Growth Drivers in the Russia Data Center Market Market

The growth of the Russia Data Center Market is primarily driven by the escalating demand for cloud computing services, fueled by the digital transformation initiatives of businesses across various sectors. Government policies supporting data localization and the development of domestic IT infrastructure are also significant catalysts. Technological advancements, such as the increasing adoption of AI, IoT, and Big Data analytics, necessitate more powerful and scalable data processing capabilities, thereby boosting the demand for data center capacity.

Challenges Impacting Russia Data Center Market Growth

Several challenges are impacting the growth of the Russia Data Center Market. Geopolitical tensions and associated sanctions can lead to disruptions in hardware supply chains and affect international investment flows. The complex and evolving regulatory environment, particularly concerning data privacy and localization, requires careful navigation by market players. Furthermore, attracting and retaining skilled IT talent remains a critical challenge, alongside the substantial capital investment required for building and upgrading data center facilities.

Key Players Shaping the Russia Data Center Market Market

- Nekstremum LLC

- Rosenergoatom

- IXELERATE LLC

- Yandex Cloud LLC

- MTS PJSC (MTS Group)

- Selectel Ltd

- Linxdatacenter

- Rostelecom

- Stack Net (Stack Group)

- 3Data

- DataPro

- RackStore

Significant Russia Data Center Market Industry Milestones

- October 2022: DataPro launched DataPro Moscow II, the first data center in Eastern Europe with a Tier-IV integrity level, capable of accommodating 1,600 racks. This expansion positions DataPro to become the second-largest player in the Russian commercial data-center market with a total of 3,600 racks.

- September 2022: Yandex announced plans to construct a new 63MW data center in Kaluga Oblast, western Russia. This facility, located in Grabtsevo Industrial Park, will span 130,000 square meters and accommodate over 3,800 server racks with a 15 kW load.

- May 2022: 3data, in partnership with Alias Group, planned the construction of a new data center in Krasnodar, with an expected opening around the end of 2023 under a franchise agreement.

Future Outlook for Russia Data Center Market Market

The future outlook for the Russia Data Center Market is exceptionally promising, characterized by sustained growth and strategic expansion. Key growth catalysts include the continued digital transformation across all sectors, the increasing adoption of hybrid and multi-cloud strategies, and the government's ongoing commitment to fostering a robust domestic digital infrastructure. Investments in high-density computing, edge data centers, and sustainable energy solutions are expected to shape the market landscape. Strategic opportunities lie in catering to the evolving needs of hyperscalers, the growing demand for colocation services from SMEs, and the specialized requirements of emerging technologies like AI and IoT. The market is poised to witness further consolidation and innovation, driven by a persistent need for secure, reliable, and scalable data processing and storage capabilities.

Russia Data Center Market Segmentation

-

1. Hotspot

- 1.1. Moscow

- 1.2. Rest of Russia

-

2. Data Center Size

- 2.1. Large

- 2.2. Massive

- 2.3. Medium

- 2.4. Mega

- 2.5. Small

-

3. Tier Type

- 3.1. Tier 1 and 2

- 3.2. Tier 3

- 3.3. Tier 4

-

4. Absorption

- 4.1. Non-Utilized

-

4.2. By Colocation Type

- 4.2.1. Hyperscale

- 4.2.2. Retail

- 4.2.3. Wholesale

-

4.3. By End User

- 4.3.1. BFSI

- 4.3.2. Cloud

- 4.3.3. E-Commerce

- 4.3.4. Government

- 4.3.5. Manufacturing

- 4.3.6. Media & Entertainment

- 4.3.7. Telecom

- 4.3.8. Other End User

Russia Data Center Market Segmentation By Geography

- 1. Russia

Russia Data Center Market Regional Market Share

Geographic Coverage of Russia Data Center Market

Russia Data Center Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.87% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Automation in the Security Screening Industry

- 3.2.2 Especially to Detect Advanced Threats

- 3.2.3 etc.; Upsurge in Terror Activities Across the Region; Increasing Government Initiatives on Security Inspection in Schools and Colleges; Increasing Government Initiatives for Smart Cities

- 3.3. Market Restrains

- 3.3.1 Supply Chain Issues Caused By Geopolitical Scenario and the COVID-19 Pandemic

- 3.3.2 etc.; High Installation and Maintenance Costs

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Russia Data Center Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 5.1.1. Moscow

- 5.1.2. Rest of Russia

- 5.2. Market Analysis, Insights and Forecast - by Data Center Size

- 5.2.1. Large

- 5.2.2. Massive

- 5.2.3. Medium

- 5.2.4. Mega

- 5.2.5. Small

- 5.3. Market Analysis, Insights and Forecast - by Tier Type

- 5.3.1. Tier 1 and 2

- 5.3.2. Tier 3

- 5.3.3. Tier 4

- 5.4. Market Analysis, Insights and Forecast - by Absorption

- 5.4.1. Non-Utilized

- 5.4.2. By Colocation Type

- 5.4.2.1. Hyperscale

- 5.4.2.2. Retail

- 5.4.2.3. Wholesale

- 5.4.3. By End User

- 5.4.3.1. BFSI

- 5.4.3.2. Cloud

- 5.4.3.3. E-Commerce

- 5.4.3.4. Government

- 5.4.3.5. Manufacturing

- 5.4.3.6. Media & Entertainment

- 5.4.3.7. Telecom

- 5.4.3.8. Other End User

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. Russia

- 5.1. Market Analysis, Insights and Forecast - by Hotspot

- 6. Western Russia Russia Data Center Market Analysis, Insights and Forecast, 2020-2032

- 7. Eastern Russia Russia Data Center Market Analysis, Insights and Forecast, 2020-2032

- 8. Southern Russia Russia Data Center Market Analysis, Insights and Forecast, 2020-2032

- 9. Northern Russia Russia Data Center Market Analysis, Insights and Forecast, 2020-2032

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 Nekstremum LLC

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Rosenergoatom

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 IXELERATE LLC

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Yandex Cloud LLC5 4 LIST OF COMPANIES STUDIE

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 MTS PJSC (MTS Group)

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Selectel Ltd

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Linxdatacenter

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Rostelecom

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Stack Net (Stack Group)

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 3Data

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 DataPro

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 RackStore

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.1 Nekstremum LLC

List of Figures

- Figure 1: Russia Data Center Market Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Russia Data Center Market Share (%) by Company 2025

List of Tables

- Table 1: Russia Data Center Market Revenue Million Forecast, by Region 2020 & 2033

- Table 2: Russia Data Center Market Revenue Million Forecast, by Hotspot 2020 & 2033

- Table 3: Russia Data Center Market Revenue Million Forecast, by Data Center Size 2020 & 2033

- Table 4: Russia Data Center Market Revenue Million Forecast, by Tier Type 2020 & 2033

- Table 5: Russia Data Center Market Revenue Million Forecast, by Absorption 2020 & 2033

- Table 6: Russia Data Center Market Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Russia Data Center Market Revenue Million Forecast, by Country 2020 & 2033

- Table 8: Western Russia Russia Data Center Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: Eastern Russia Russia Data Center Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Southern Russia Russia Data Center Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Northern Russia Russia Data Center Market Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Russia Data Center Market Revenue Million Forecast, by Hotspot 2020 & 2033

- Table 13: Russia Data Center Market Revenue Million Forecast, by Data Center Size 2020 & 2033

- Table 14: Russia Data Center Market Revenue Million Forecast, by Tier Type 2020 & 2033

- Table 15: Russia Data Center Market Revenue Million Forecast, by Absorption 2020 & 2033

- Table 16: Russia Data Center Market Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Russia Data Center Market?

The projected CAGR is approximately 4.87%.

2. Which companies are prominent players in the Russia Data Center Market?

Key companies in the market include Nekstremum LLC, Rosenergoatom, IXELERATE LLC, Yandex Cloud LLC5 4 LIST OF COMPANIES STUDIE, MTS PJSC (MTS Group), Selectel Ltd, Linxdatacenter, Rostelecom, Stack Net (Stack Group), 3Data, DataPro, RackStore.

3. What are the main segments of the Russia Data Center Market?

The market segments include Hotspot, Data Center Size, Tier Type, Absorption.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Automation in the Security Screening Industry. Especially to Detect Advanced Threats. etc.; Upsurge in Terror Activities Across the Region; Increasing Government Initiatives on Security Inspection in Schools and Colleges; Increasing Government Initiatives for Smart Cities.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Supply Chain Issues Caused By Geopolitical Scenario and the COVID-19 Pandemic. etc.; High Installation and Maintenance Costs.

8. Can you provide examples of recent developments in the market?

October 2022: DataPro Moscow II, the first data center in Eastern Europe with a Tier-IV integrity level, was opened by the DataPro corporation, an independent operator of data processing facilities in Russia. The new DataPro data center can accommodate 1,600 racks in total. The initial batch of 800 racks is currently in use. By the end of 2020, the second lot of 800 racks will be usable. It will enable DataPro to hold second place in the Russian commercial data-center market with 3,600 racks overall in its data centers.September 2022: Yandex plans to construct a brand-new 63MW data center in western Russia's Kaluga Oblast. The brand-new building will be situated in Kaluga's Grabtsevo Industrial Park, around 100 miles south of Moscow. With a 130,000 square meter footprint and 63 MW of power, the new data center can accommodate more than 3,800 server racks with a 15 kW load.May 2022: The Russian data center company 3data and the investment firm Alias Group will build a data center in Krasnodar. A new facility will open in the Krasnodar Territory, according to 3data. According to the business, the facility will open around the end of 2023 under a franchise agreement with the investment firm Alias Group.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Russia Data Center Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Russia Data Center Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Russia Data Center Market?

To stay informed about further developments, trends, and reports in the Russia Data Center Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence