Key Insights

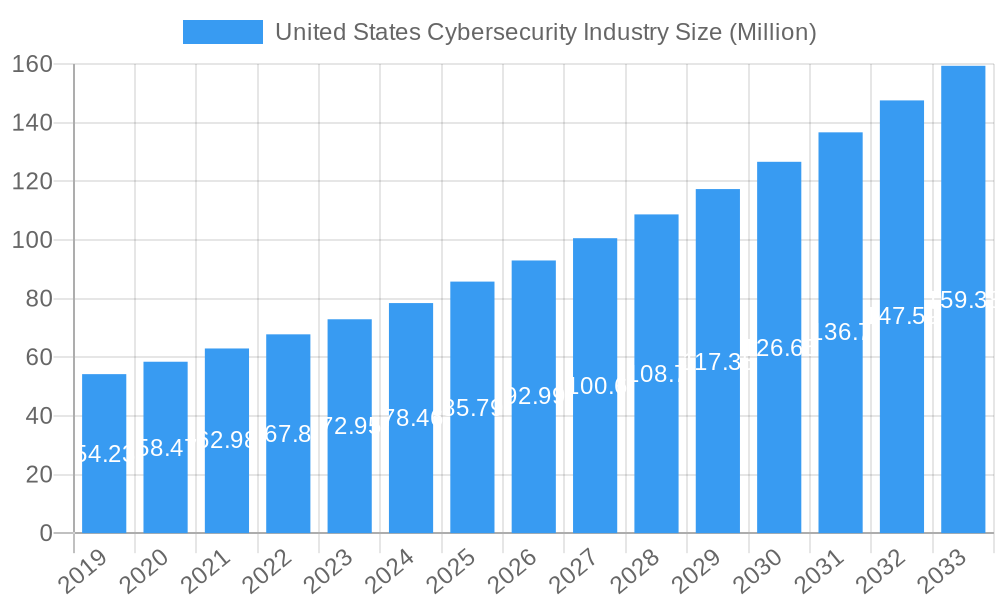

The United States cybersecurity market is poised for robust expansion, projected to reach approximately $85.79 billion by 2025, exhibiting a compound annual growth rate (CAGR) of 8.09% throughout the forecast period of 2025-2033. This significant market size underscores the nation's critical reliance on digital infrastructure and the escalating threat landscape. Key drivers fueling this growth include the increasing sophistication and frequency of cyberattacks, stringent regulatory mandates such as GDPR and CCPA, and the accelerating digital transformation across all sectors. The shift towards cloud-based solutions and the growing adoption of remote work have further amplified the demand for advanced cloud security, data security, and identity and access management (IAM) solutions. Leading market players like IBM Corporation, Fortinet Inc., and Cisco Systems Inc. are investing heavily in research and development, introducing innovative solutions to combat evolving threats, including advanced persistent threats (APTs) and ransomware.

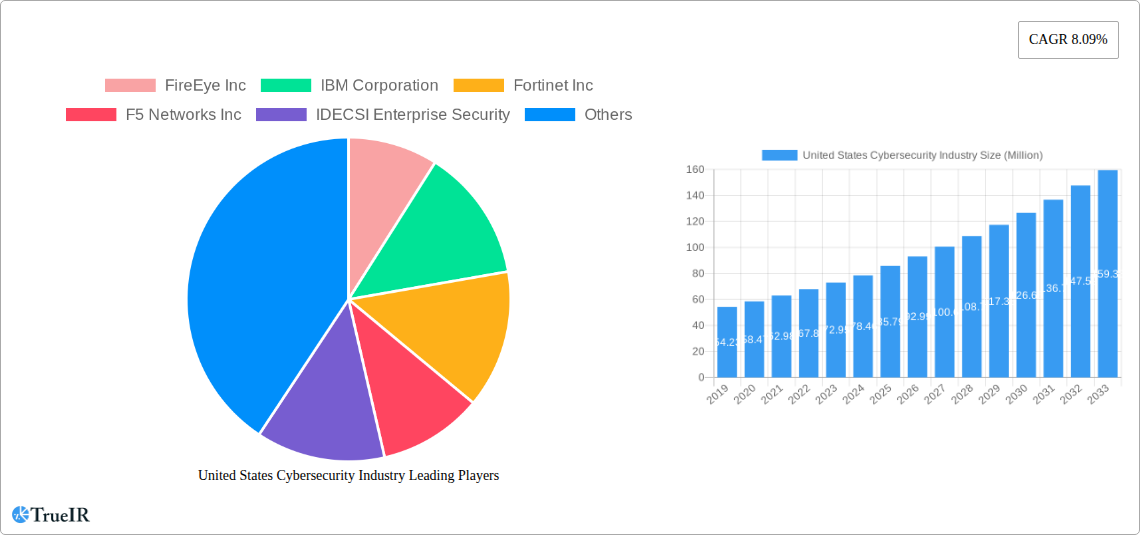

United States Cybersecurity Industry Market Size (In Million)

The United States cybersecurity market is characterized by a diverse range of offerings, encompassing cloud security, data security, identity access management, network security, consumer security, and infrastructure protection, alongside a comprehensive suite of services. Deployment models are increasingly tilting towards cloud solutions, though on-premise deployments remain significant, particularly within government and defense sectors. Key end-user industries such as BFSI, healthcare, manufacturing, and IT and telecommunication are primary adopters, driven by the need to protect sensitive data and maintain operational continuity. Emerging trends include the growing prominence of artificial intelligence (AI) and machine learning (ML) in threat detection and response, the rise of zero-trust architectures, and the increasing focus on cybersecurity for the Internet of Things (IoT) devices. However, challenges such as the cybersecurity skills gap, the high cost of advanced solutions, and the persistent threat of nation-state sponsored attacks, alongside the complexities of securing legacy systems, present significant restraints to the market.

United States Cybersecurity Industry Company Market Share

United States Cybersecurity Industry: Market Analysis, Trends, and Future Outlook (2019-2033)

This comprehensive report delves into the dynamic United States Cybersecurity Industry, providing an in-depth analysis of its market structure, competitive landscape, key trends, and future trajectory. Leveraging high-volume SEO keywords, this report is meticulously crafted to enhance search rankings and engage industry professionals, investors, and decision-makers. The study period spans from 2019 to 2033, with a base and estimated year of 2025 and a forecast period from 2025 to 2033. The historical period covers 2019 to 2024.

United States Cybersecurity Industry Market Structure & Competitive Landscape

The United States cybersecurity market exhibits a moderately consolidated structure, driven by a continuous influx of innovation and a robust ecosystem of established players and emerging startups. Key innovation drivers include the escalating sophistication of cyber threats, the rapid adoption of cloud technologies, and the increasing regulatory compliance demands across various sectors. Regulatory impacts, such as the California Consumer Privacy Act (CCPA) and the potential for federal data privacy legislation, significantly shape market strategies and product development. Product substitutes, while present in the form of in-house security teams or less advanced solutions, are increasingly being overshadowed by specialized and comprehensive cybersecurity offerings. End-user segmentation reveals a strong demand from the BFSI, Healthcare, and Government & Defense sectors due to the sensitive nature of the data they handle. Mergers and acquisitions (M&A) are a prominent feature, reflecting the industry's maturity and the strategic imperative for companies to expand their service portfolios and market reach. For instance, the market has witnessed M&A volumes in the billions of USD, as seen with Google's acquisition of Mandiant. Concentration ratios are influenced by the dominance of a few large players in specific segments, balanced by a vibrant mid-market and specialized niche providers.

United States Cybersecurity Industry Market Trends & Opportunities

The United States cybersecurity market is poised for substantial growth, projected to reach several hundred billion USD by 2025, with a Compound Annual Growth Rate (CAGR) of approximately 12-15% through 2033. This expansion is fueled by an increasing awareness of cyber risks, the proliferation of connected devices (IoT), and the digital transformation initiatives across all industries. Technological shifts are a primary catalyst, with a marked trend towards proactive security solutions, including AI-powered threat detection, extended detection and response (XDR), and zero-trust architectures. Consumer preferences are evolving from reactive to preventative security measures, demanding integrated and user-friendly solutions. The competitive dynamics are intensifying, with companies focusing on specialization, cloud-native offerings, and managed security services (MSSP) to capture market share. The increasing attack surface due to remote work and hybrid cloud environments presents significant opportunities for companies offering robust endpoint security, identity and access management (IAM), and data loss prevention (DLP) solutions. Market penetration rates are expected to rise across all end-user segments as organizations recognize the critical need for comprehensive cybersecurity strategies to safeguard their operations and sensitive data. The demand for cloud security solutions is particularly robust, driven by the accelerated migration of business applications and data to cloud platforms.

Dominant Markets & Segments in United States Cybersecurity Industry

Within the United States cybersecurity industry, Cloud Security stands out as a dominant segment, driven by the pervasive adoption of cloud computing across businesses of all sizes. The BFSI (Banking, Financial Services, and Insurance) sector consistently represents a leading end-user market, owing to the highly sensitive financial data it manages and the stringent regulatory compliance requirements it adheres to. The Government & Defense sector also exerts significant influence, driven by national security concerns and the need to protect critical infrastructure.

Key growth drivers in these dominant segments include:

- Infrastructure: The continuous expansion of cloud infrastructure and the increasing complexity of IT environments necessitate advanced cloud security measures to protect data and applications.

- Policies: Stringent data privacy regulations and government mandates for cybersecurity resilience in critical sectors are compelling organizations to invest heavily in cybersecurity solutions.

- Threat Landscape: The escalating frequency and sophistication of cyberattacks, particularly ransomware and advanced persistent threats (APTs), are forcing organizations to adopt more robust and proactive security postures.

Offering Dominance:

- Cloud Security: This segment is experiencing exponential growth due to the widespread migration to cloud environments, including public, private, and hybrid clouds. Companies are seeking solutions for cloud workload protection, cloud security posture management (CSPM), and cloud access security brokers (CASB).

- Data Security: Protecting sensitive data at rest, in transit, and in use is paramount. Solutions like data loss prevention (DLP), encryption, and data masking are in high demand across all industries.

- Identity Access Management (IAM): With the rise of remote work and the increasing complexity of user access, robust IAM solutions, including multi-factor authentication (MFA) and privileged access management (PAM), are essential.

Deployment Dominance:

- Cloud: Cloud-based deployment models are gaining significant traction due to their scalability, flexibility, and cost-effectiveness, aligning with the broader trend of cloud adoption.

End User Dominance:

- BFSI: This sector leads in cybersecurity spending due to the high value of financial data and the severe consequences of data breaches, including financial losses and reputational damage.

- Healthcare: The sensitive nature of patient health information (PHI) and the increasing digitization of healthcare records make this sector a prime target for cybercriminals, driving substantial investment in security solutions.

- Government & Defense: National security imperatives and the need to protect critical infrastructure from state-sponsored attacks and sophisticated cyber threats make this sector a significant cybersecurity consumer.

United States Cybersecurity Industry Product Analysis

Product innovations in the United States cybersecurity industry are largely focused on leveraging artificial intelligence (AI) and machine learning (ML) for predictive threat detection and automated response. Solutions are increasingly integrated, offering comprehensive protection across multiple security domains, such as XDR (Extended Detection and Response) platforms. Competitive advantages are derived from the ability to provide real-time threat intelligence, seamless integration with existing IT infrastructures, and user-friendly interfaces that simplify complex security management. The market also sees a rise in specialized offerings catering to niche industries and specific threat vectors, enhancing market fit and customer value.

Key Drivers, Barriers & Challenges in United States Cybersecurity Industry

Key Drivers:

- Escalating Cyber Threats: The increasing volume and sophistication of cyberattacks, including ransomware, phishing, and advanced persistent threats (APTs), are a primary catalyst for market growth. The constant need to defend against evolving threats compels organizations to invest in advanced cybersecurity solutions.

- Digital Transformation and Cloud Adoption: The widespread adoption of cloud computing, IoT devices, and digital transformation initiatives expands the attack surface, creating a greater demand for comprehensive and scalable cybersecurity solutions.

- Regulatory Compliance: Stringent data privacy regulations, such as CCPA, and industry-specific compliance mandates (e.g., HIPAA in healthcare, PCI DSS in finance) drive investment in security technologies and services to avoid penalties and maintain customer trust.

Barriers & Challenges:

- Talent Shortage: A significant and persistent shortage of skilled cybersecurity professionals creates a bottleneck for organizations seeking to implement and manage complex security solutions effectively. This talent gap can lead to understaffed security teams and increased operational risks.

- Complexity of Security Solutions: The ever-increasing complexity of IT environments and the proliferation of specialized security tools can make it challenging for organizations to integrate, manage, and maintain a cohesive security posture.

- Cost of Implementation and Maintenance: The substantial investment required for advanced cybersecurity technologies, ongoing maintenance, and expert personnel can be a barrier for small and medium-sized businesses (SMBs). Supply chain issues for hardware components can also impact deployment timelines and costs.

Growth Drivers in the United States Cybersecurity Industry Market

The United States cybersecurity market is propelled by a confluence of powerful growth drivers. Technologically, the relentless innovation in AI and machine learning for threat detection and response is creating more effective and proactive security solutions. Economically, the growing recognition of cybersecurity as a critical business imperative, rather than just an IT cost, is leading to increased budget allocations across all sectors. Regulatory drivers, such as evolving data privacy laws and government mandates for critical infrastructure protection, are creating a compelling business case for robust cybersecurity investments. The rise of remote work and the expanding attack surface presented by the Internet of Things (IoT) further amplify the demand for comprehensive security measures.

Challenges Impacting United States Cybersecurity Industry Growth

Several challenges impede the growth of the United States cybersecurity industry. The persistent and widening cybersecurity talent gap remains a critical restraint, limiting organizations' ability to deploy and effectively manage advanced security solutions. Regulatory complexities and the constant evolution of compliance requirements can create significant hurdles for businesses, particularly for smaller enterprises. Supply chain issues for essential hardware components can lead to deployment delays and increased costs, impacting the accessibility of certain security technologies. Moreover, intensifying competitive pressures from a crowded market necessitate continuous innovation and strategic pricing, adding to operational challenges for many companies.

Key Players Shaping the United States Cybersecurity Industry Market

- FireEye Inc

- IBM Corporation

- Fortinet Inc

- F5 Networks Inc

- IDECSI Enterprise Security

- Cisco Systems Inc

- AVG Technologies

- Intel Security (Intel Corporation)

- Dell Technologies Inc

- Cyberark Software Ltd

Significant United States Cybersecurity Industry Industry Milestones

- March 2022: Google Cloud announced its acquisition of cybersecurity firm Mandiant, a prominent player in proactive SaaS-based security. This USD 5.4 billion deal underscores the growing importance of security for all enterprises, irrespective of size, in light of increasing cybercrime impact. Mandiant is set to merge with Google Cloud upon regulatory and stockholder approvals.

- March 2022: HelpSystems announced a merger agreement to acquire AlertLogic, a key provider of managed detection and response (MDR) services. This acquisition aims to bolster HelpSystems' cybersecurity portfolio, addressing the growing pressure on organizations due to escalating cyberattacks and a shortage of skilled cybersecurity professionals.

Future Outlook for United States Cybersecurity Industry Market

The future outlook for the United States cybersecurity industry is exceptionally robust, driven by continued technological advancements and an ever-present threat landscape. Strategic opportunities lie in the increasing demand for AI-powered security solutions, zero-trust architectures, and comprehensive managed security services. The market potential is significant as businesses across all sectors prioritize resilience and data protection in an increasingly digital world. The ongoing evolution of cyber threats will necessitate continuous innovation, creating sustained demand for advanced cybersecurity products and services, further solidifying the industry's growth trajectory.

United States Cybersecurity Industry Segmentation

-

1. Offering

-

1.1. Security Type

- 1.1.1. Cloud Security

- 1.1.2. Data Security

- 1.1.3. Identity Access Management

- 1.1.4. Network Security

- 1.1.5. Consumer Security

- 1.1.6. Infrastructure Protection

- 1.1.7. Other Types

- 1.2. Services

-

1.1. Security Type

-

2. Deployment

- 2.1. Cloud

- 2.2. On-premise

-

3. End User

- 3.1. BFSI

- 3.2. Healthcare

- 3.3. Manufacturing

- 3.4. Government & Defense

- 3.5. IT and Telecommunication

- 3.6. Other End Users

United States Cybersecurity Industry Segmentation By Geography

- 1. United States

United States Cybersecurity Industry Regional Market Share

Geographic Coverage of United States Cybersecurity Industry

United States Cybersecurity Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.09% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Demand for Digitalization and Scalable IT Infrastructure; Need to tackle risks from various trends such as third-party vendor risks

- 3.2.2 the evolution of MSSPs

- 3.2.3 and adoption of cloud-first strategy

- 3.3. Market Restrains

- 3.3.1. Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness

- 3.4. Market Trends

- 3.4.1. Need For Identity Access Management is One of the Factor Driving the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. United States Cybersecurity Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 5.1.1. Security Type

- 5.1.1.1. Cloud Security

- 5.1.1.2. Data Security

- 5.1.1.3. Identity Access Management

- 5.1.1.4. Network Security

- 5.1.1.5. Consumer Security

- 5.1.1.6. Infrastructure Protection

- 5.1.1.7. Other Types

- 5.1.2. Services

- 5.1.1. Security Type

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. Cloud

- 5.2.2. On-premise

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. BFSI

- 5.3.2. Healthcare

- 5.3.3. Manufacturing

- 5.3.4. Government & Defense

- 5.3.5. IT and Telecommunication

- 5.3.6. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Offering

- 6. Belgium United States Cybersecurity Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 6.1.1.

- 7. Netherlands United States Cybersecurity Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 7.1.1.

- 8. Luxembourg United States Cybersecurity Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1.

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2025

- 9.2. Company Profiles

- 9.2.1 FireEye Inc

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 IBM Corporation

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 Fortinet Inc

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 F5 Networks Inc

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 IDECSI Enterprise Security

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 Cisco Systems Inc

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 AVG Technologies

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 Intel Security (Intel Corporation)

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 Dell Technologies Inc

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.10 Cyberark Software Ltd*List Not Exhaustive

- 9.2.10.1. Overview

- 9.2.10.2. Products

- 9.2.10.3. SWOT Analysis

- 9.2.10.4. Recent Developments

- 9.2.10.5. Financials (Based on Availability)

- 9.2.1 FireEye Inc

List of Figures

- Figure 1: United States Cybersecurity Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: United States Cybersecurity Industry Share (%) by Company 2025

List of Tables

- Table 1: United States Cybersecurity Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 2: United States Cybersecurity Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 3: United States Cybersecurity Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 4: United States Cybersecurity Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 5: United States Cybersecurity Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: United States Cybersecurity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United States Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: United States Cybersecurity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: United States Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: United States Cybersecurity Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 11: United States Cybersecurity Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: United States Cybersecurity Industry Revenue Million Forecast, by Offering 2020 & 2033

- Table 13: United States Cybersecurity Industry Revenue Million Forecast, by Deployment 2020 & 2033

- Table 14: United States Cybersecurity Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 15: United States Cybersecurity Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the United States Cybersecurity Industry?

The projected CAGR is approximately 8.09%.

2. Which companies are prominent players in the United States Cybersecurity Industry?

Key companies in the market include FireEye Inc, IBM Corporation, Fortinet Inc, F5 Networks Inc, IDECSI Enterprise Security, Cisco Systems Inc, AVG Technologies, Intel Security (Intel Corporation), Dell Technologies Inc, Cyberark Software Ltd*List Not Exhaustive.

3. What are the main segments of the United States Cybersecurity Industry?

The market segments include Offering, Deployment, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 85.79 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Digitalization and Scalable IT Infrastructure; Need to tackle risks from various trends such as third-party vendor risks. the evolution of MSSPs. and adoption of cloud-first strategy.

6. What are the notable trends driving market growth?

Need For Identity Access Management is One of the Factor Driving the Market.

7. Are there any restraints impacting market growth?

Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness.

8. Can you provide examples of recent developments in the market?

March 2022 - Google Cloud announced it is acquiring cybersecurity firm Mandiant, a player in proactive SaaS-based security. In light of the growing impact of cybercrime on all businesses across the country, the acquisition emphasizes the necessity of security for all enterprises, regardless of size. Mandiant will be acquired for an all-cash price of USD 23 per share in a deal worth USD 5.4 billion. Once the necessary stockholder and regulatory clearances are obtained, Mandiant will merge with Google Cloud.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "United States Cybersecurity Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the United States Cybersecurity Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the United States Cybersecurity Industry?

To stay informed about further developments, trends, and reports in the United States Cybersecurity Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence