Key Insights

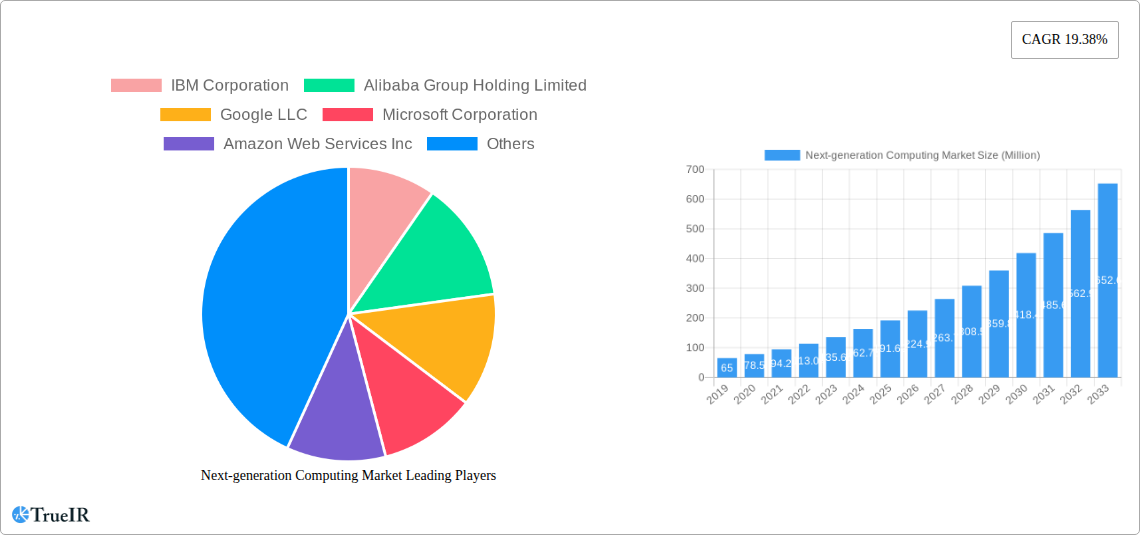

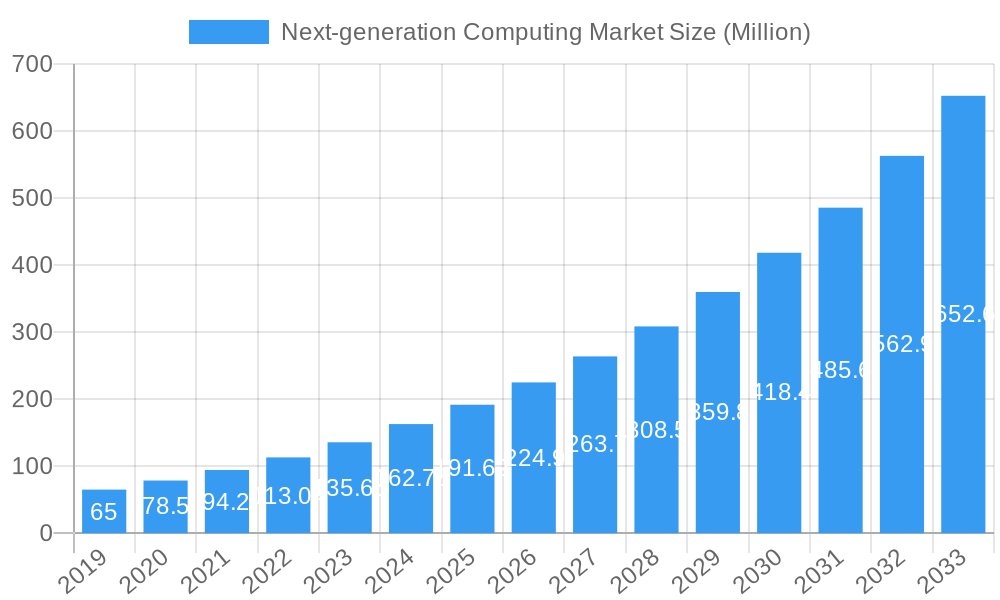

The Next-generation Computing Market is experiencing a period of unprecedented growth, projected to reach $191.62 million by 2025 and expand at a robust Compound Annual Growth Rate (CAGR) of 19.38%. This dynamic expansion is fueled by a confluence of powerful drivers, including the escalating demand for enhanced data processing capabilities across industries, the rapid evolution of artificial intelligence and machine learning, and the increasing need for sophisticated solutions to tackle complex computational challenges. Emerging technologies like Quantum Computing and Optical Computing, though nascent, are poised to revolutionize computation, offering capabilities far beyond current paradigms. The market is also being propelled by the widespread adoption of High-Performance Computing (HPC) and Edge Computing solutions, which are essential for real-time data analysis and distributed processing. This surge in innovation is creating significant opportunities for advancements in sectors such as Healthcare, Automotive & Transportation, and BFSI, where the ability to process vast datasets quickly and efficiently is paramount. The interplay between sophisticated hardware, advanced software, and comprehensive services is critical to unlocking the full potential of these next-generation computing solutions.

Next-generation Computing Market Market Size (In Million)

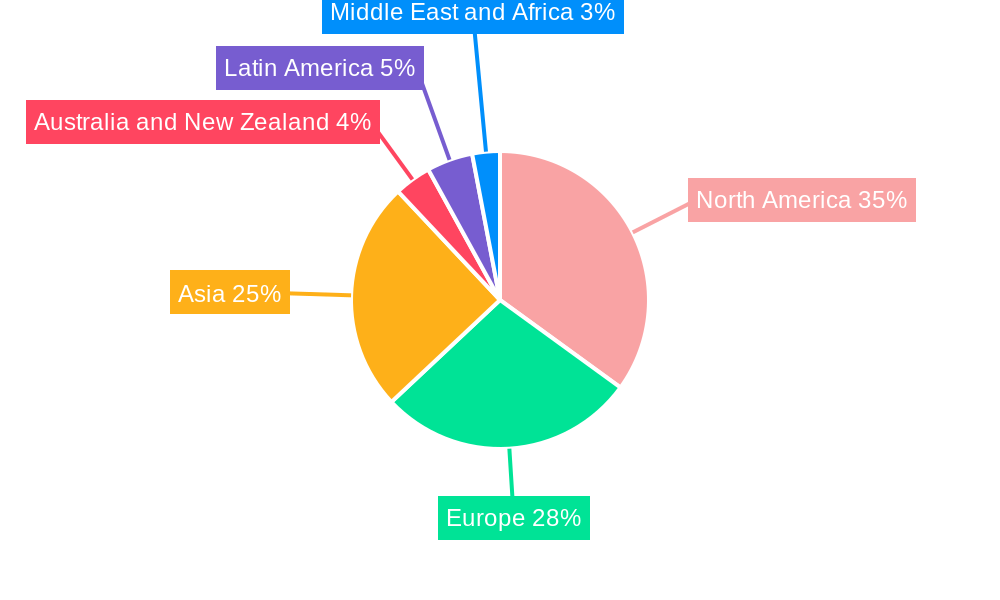

The market's trajectory is further shaped by key trends such as the increasing integration of AI and ML into core computing architectures, the growing emphasis on sustainable and energy-efficient computing, and the development of specialized hardware for AI workloads. While the potential for disruptive innovation is immense, certain restraints, such as the high cost of advanced hardware and the scarcity of skilled talent, need to be addressed for sustained growth. However, the pervasive adoption of cloud and on-premise deployment models caters to diverse organizational needs, further broadening market accessibility. Geographically, North America and Europe are expected to lead the market due to significant R&D investments and strong adoption of advanced technologies. Asia is rapidly emerging as a key growth region, driven by its burgeoning tech industry and increasing investments in digital transformation. The collaborative efforts of major technology players like IBM, Google, Microsoft, and NVIDIA are instrumental in pushing the boundaries of what is possible, ensuring a future where computing power is not a limitation but an enabler of transformative solutions across all sectors.

Next-generation Computing Market Company Market Share

Here is a dynamic, SEO-optimized report description for the Next-generation Computing Market, crafted for maximum engagement and search visibility without any placeholders.

Next-generation Computing Market: Unveiling the Future of Computation and Digital Transformation (2019–2033)

This comprehensive market research report delves into the rapidly evolving Next-generation Computing Market, a critical sector driving innovation across industries. Covering the study period of 2019–2033, with a base year of 2025, this analysis provides deep insights into the technological advancements, market dynamics, and strategic opportunities that will shape the future of computation. The report examines the forecast period of 2025–2033, leveraging historical data from 2019–2024 to provide accurate projections.

The Next-generation Computing Market is poised for exponential growth, fueled by the increasing demand for advanced processing capabilities, AI integration, and efficient data management. This report offers an in-depth exploration of key segments, including Hardware, Software, and Services components, and diverse computing types such as High-Performance Computing (HPC), Quantum Computing, Optical Computing, and Edge Computing. It scrutinizes deployment models like Cloud and On-Premise, and analyzes end-user industries ranging from Automotive & Transportation and Healthcare to BFSI and Manufacturing.

Gain a competitive edge with our detailed analysis of leading players including IBM Corporation, Alibaba Group Holding Limited, Google LLC, Microsoft Corporation, Amazon Web Services Inc, NVIDIA Corp, NEC Corporation, Oracle Corporation, Cisco Systems, and Intel Corporation. Understand the critical industry developments, key drivers, potential barriers, and the overarching future outlook of this transformative market.

Next-generation Computing Market Market Structure & Competitive Landscape

The Next-generation Computing Market exhibits a moderately concentrated structure, driven by significant capital investment requirements and the need for advanced research and development capabilities. Innovation remains the paramount driver, with companies continuously pushing the boundaries of processing power, efficiency, and application scope. Regulatory impacts, while nascent in some cutting-edge areas like quantum computing, are increasingly influencing data privacy, security, and ethical AI development, particularly in sectors like finance and healthcare. The threat of product substitutes is evolving; while traditional computing still holds sway, the rapid advancements in specialized hardware and AI-accelerated algorithms are increasingly offering alternatives for specific workloads.

End-user segmentation reveals a broad adoption landscape, with a pronounced demand from industries requiring intensive data processing and real-time analytics. Key players are strategically engaged in mergers and acquisitions (M&A) to consolidate market share, acquire specialized technologies, and expand their service portfolios. For instance, recent M&A activities in the cloud computing and AI infrastructure space highlight a trend towards vertical integration and ecosystem building. Concentration ratios in key sub-segments, such as HPC and specialized AI chip manufacturing, are estimated to be in the XX% range, indicating the dominance of a few key players. The M&A volume in the sector has seen an estimated XX% increase year-on-year, driven by the pursuit of synergistic capabilities and market expansion.

Next-generation Computing Market Market Trends & Opportunities

The Next-generation Computing Market is experiencing a seismic shift, driven by an unprecedented surge in data generation and the insatiable demand for advanced analytical capabilities across all sectors. The market size is projected to grow from an estimated $XXX Billion in 2025 to over $XXX Billion by 2033, exhibiting a robust Compound Annual Growth Rate (CAGR) of XX%. This expansion is underpinned by a series of transformative technological shifts, including the maturation of high-performance computing (HPC) for scientific research and complex simulations, the burgeoning potential of quantum computing for intractable problem-solving, the efficiency gains offered by optical computing, and the critical need for real-time processing at the edge with edge computing solutions.

Consumer preferences are evolving rapidly, with businesses increasingly seeking scalable, flexible, and secure computing solutions that can adapt to dynamic workloads. This is propelling the adoption of cloud-native architectures and hybrid cloud strategies. Competitive dynamics are intensifying, characterized by fierce innovation races, strategic partnerships, and significant investments in R&D by major technology giants. The market penetration rates for advanced computing solutions, particularly in emerging economies, are on an upward trajectory, signaling immense untapped potential. Opportunities abound for providers of specialized hardware, advanced AI/ML software, and managed cloud services tailored to the unique demands of next-generation applications. The increasing reliance on data-driven decision-making in sectors like BFSI, healthcare, and manufacturing is creating fertile ground for predictive analytics, AI-powered automation, and hyper-personalization, all of which are fundamentally reliant on next-generation computing power. The global push towards digital transformation further amplifies these trends, as organizations across industries strive to leverage the power of advanced computation to gain a competitive advantage, optimize operations, and unlock new revenue streams. The development of more energy-efficient computing architectures is also becoming a significant trend, addressing growing concerns about the environmental impact of large-scale data centers and high-performance computing clusters. This focus on sustainability opens up avenues for innovation in hardware design and algorithmic optimization, creating a dual opportunity for both technological advancement and corporate responsibility.

Dominant Markets & Segments in Next-generation Computing Market

The Next-generation Computing Market is characterized by distinct areas of dominance and rapid growth across its diverse segments. Regionally, North America and Asia-Pacific are emerging as leading markets due to substantial investments in technological infrastructure, robust research and development ecosystems, and government initiatives supporting digital transformation. Countries like the United States, China, and South Korea are at the forefront of innovation and adoption.

Within the Component segmentation, Hardware holds a significant share due to the foundational need for advanced processors, accelerators (GPUs, TPUs), and specialized memory solutions that power next-generation workloads. The demand for custom-designed chips for AI and HPC applications is a key growth driver.

Analyzing Computing Type, High-Performance Computing (HPC) currently dominates, driven by its established role in scientific research, weather forecasting, drug discovery, and financial modeling. However, Edge Computing is experiencing the most rapid growth, fueled by the proliferation of IoT devices and the need for real-time data processing and reduced latency in sectors like autonomous vehicles, industrial automation, and smart cities. Quantum Computing, while still in its nascent stages, represents a significant future growth opportunity, with substantial investments in research and early-stage commercialization efforts. Optical Computing offers a compelling long-term prospect for overcoming the limitations of electronic computing.

In terms of Deployment, the Cloud model continues to be a primary driver for next-generation computing, offering scalability, flexibility, and cost-effectiveness. Hybrid cloud strategies are also gaining traction, allowing organizations to leverage the benefits of both public and private cloud environments.

The End-user landscape reveals strong adoption across several key industries. BFSI is a major consumer, utilizing advanced analytics for fraud detection, risk management, and algorithmic trading. The Automotive & Transportation sector is increasingly adopting next-generation computing for autonomous driving systems, vehicle-to-everything (V2X) communication, and advanced driver-assistance systems (ADAS). Healthcare is leveraging these technologies for personalized medicine, genomic sequencing, drug discovery, and advanced medical imaging. IT & Telecom sectors are also significant adopters, driving the infrastructure and services that enable next-generation computing. Manufacturing is benefiting from AI-powered optimization, predictive maintenance, and smart factory initiatives. Aerospace & Defense relies on HPC for complex simulations and data analysis.

Key growth drivers across these segments include:

- Infrastructure Development: Government and private sector investments in high-speed networks, advanced data centers, and research facilities.

- Technological Advancements: Continuous innovation in AI algorithms, chip design, and quantum computing paradigms.

- Data Proliferation: The exponential growth of data necessitates more powerful and efficient processing capabilities.

- Industry-Specific Demands: Tailored solutions for complex challenges in fields like climate modeling, materials science, and cybersecurity.

- Policy Support: Government funding for R&D, tax incentives, and national strategies focused on emerging technologies.

Next-generation Computing Market Product Analysis

Next-generation computing products are defined by their ability to handle complex computations, large datasets, and advanced AI workloads with unprecedented speed and efficiency. Innovations are centered around specialized hardware accelerators like GPUs and TPUs, designed to optimize parallel processing for machine learning and deep learning. Software advancements include sophisticated AI/ML frameworks, quantum programming languages, and highly optimized operating systems for distributed computing environments. The competitive advantage lies in achieving higher processing power per watt, lower latency, enhanced security features, and seamless integration within existing IT infrastructures. Applications span from accelerating drug discovery and financial modeling to powering autonomous systems and enabling real-time environmental monitoring, showcasing a broad market fit for these cutting-edge solutions.

Key Drivers, Barriers & Challenges in Next-generation Computing Market

Key Drivers:

The Next-generation Computing Market is propelled by several fundamental forces. Technological advancements in AI, machine learning, quantum physics, and semiconductor design are creating entirely new computational paradigms and capabilities. The exponential growth of data across all industries, often termed the "data deluge," necessitates more powerful processing solutions. Economic incentives are also significant, as organizations seek to gain competitive advantages through enhanced efficiency, predictive analytics, and innovative product development. Government initiatives and funding for policy-driven research and development in areas like quantum computing and AI are crucial. For instance, national quantum initiatives aim to foster ecosystem growth and accelerate discovery. The increasing demand for real-time insights and personalized experiences across consumer and enterprise applications also acts as a powerful catalyst.

Barriers & Challenges:

Despite the immense potential, the market faces considerable barriers and challenges. High development and implementation costs associated with advanced hardware and specialized software are significant deterrents for many organizations, particularly SMEs. The shortage of skilled talent in areas like quantum computing, AI engineering, and specialized hardware design creates a bottleneck. Regulatory hurdles and ethical considerations, especially concerning data privacy, AI bias, and the potential misuse of powerful computing technologies, require careful navigation. Supply chain complexities for advanced components, particularly for high-end semiconductors and rare materials used in quantum systems, can lead to delays and increased costs. Furthermore, interoperability issues between different next-generation computing platforms and existing IT infrastructure can hinder seamless integration. The inherent complexity of some advanced computing technologies, like quantum computing, also poses a challenge for widespread understanding and adoption.

Growth Drivers in the Next-generation Computing Market Market

The Next-generation Computing Market is experiencing robust growth driven by a confluence of factors. Technological innovation is paramount, with continuous breakthroughs in AI algorithms, specialized chip architectures (like GPUs and TPUs), and quantum computing paradigms fundamentally expanding computational capabilities. The ever-increasing volume and velocity of data generation across all sectors necessitate more powerful and efficient processing solutions. Economic imperatives to enhance productivity, optimize operations, and unlock new revenue streams are pushing organizations to adopt advanced computing. Furthermore, supportive government policies and investments in research and development, such as national quantum initiatives and AI strategies, are fostering ecosystem growth and accelerating market penetration. The increasing demand for real-time analytics, hyper-personalization, and predictive capabilities in industries like finance, healthcare, and automotive further fuels this expansion.

Challenges Impacting Next-generation Computing Market Growth

The Next-generation Computing Market faces several significant challenges that could impede its growth trajectory. High capital expenditure for advanced hardware, specialized software, and the development of new computational paradigms presents a substantial barrier, especially for small and medium-sized enterprises. The scarcity of skilled professionals with expertise in areas like quantum physics, AI development, and specialized hardware engineering creates a critical talent gap. Regulatory complexities and ethical concerns surrounding data privacy, AI bias, and the responsible deployment of powerful computing technologies require careful consideration and proactive management. Supply chain vulnerabilities for critical components, including advanced semiconductors and rare earth materials, can lead to production delays and cost escalations. Finally, interoperability challenges between nascent next-generation computing platforms and existing IT infrastructures can hinder seamless integration and adoption.

Key Players Shaping the Next-generation Computing Market Market

- IBM Corporation

- Alibaba Group Holding Limited

- Google LLC

- Microsoft Corporation

- Amazon Web Services Inc

- NVIDIA Corp

- NEC Corporation

- Oracle Corporation

- Cisco Systems

- Intel Corporation

Significant Next-generation Computing Market Industry Milestones

- July 2023: Moody's and Microsoft announced a strategic partnership to co-create next-generation data, analytics, research, collaboration, and risk solutions for financial services. This initiative leverages Microsoft's Azure OpenAI Service, Fabric, and Teams, combined with Moody's proprietary data and analytics, aiming to enhance corporate intelligence and risk assessment.

- September 2022: General Atomics Aeronautical Systems partnered with the Indian startup 3rdiTech to develop next-generation integrated circuits, other semiconductor technologies, and computer chips, poised to fuel market growth in the forecast period.

Future Outlook for Next-generation Computing Market Market

The future outlook for the Next-generation Computing Market is exceptionally bright, characterized by sustained high growth and transformative potential. Key catalysts include the continued maturation and increasing accessibility of quantum computing, the widespread adoption of advanced AI and machine learning across all industries, and the deployment of edge computing solutions for real-time decision-making. Strategic opportunities lie in developing specialized solutions for nascent fields like personalized medicine and climate modeling, as well as enhancing the security and ethical frameworks surrounding these powerful technologies. The market's ability to address complex global challenges, from disease eradication to sustainable energy, will continue to drive innovation and investment, ensuring its pivotal role in shaping the digital future. The projected market value is estimated to exceed $XXX Billion by 2033.

Next-generation Computing Market Segmentation

-

1. Component

- 1.1. Hardware

- 1.2. Software

- 1.3. Services

-

2. Computing Type

- 2.1. High-Performance Computing

- 2.2. Quantum Computing

- 2.3. Optical Computing

- 2.4. Edge Computing

- 2.5. Other Computing Types

-

3. Deployement

- 3.1. Cloud

- 3.2. On-Premise

-

4. End-user

- 4.1. Automotive & Transportation

- 4.2. Energy & Utilities

- 4.3. Healthcare

- 4.4. BFSI

- 4.5. Aerospace & Defense

- 4.6. Media & Entertainment

- 4.7. IT & Telecom

- 4.8. Retail

- 4.9. Manufacturing

- 4.10. Other End Users

Next-generation Computing Market Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Next-generation Computing Market Regional Market Share

Geographic Coverage of Next-generation Computing Market

Next-generation Computing Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 19.38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growth in demand for high performance computing; Adoption of Advanced Analytics in SMEs

- 3.3. Market Restrains

- 3.3.1. Risk of Data Breach in Storing and Processing Large Data in Next-gen Computing; High operational challenges in Implementing the Solution

- 3.4. Market Trends

- 3.4.1. The Cloud Deployment of The Solutions Significantly Contributes to The Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.2. Software

- 5.1.3. Services

- 5.2. Market Analysis, Insights and Forecast - by Computing Type

- 5.2.1. High-Performance Computing

- 5.2.2. Quantum Computing

- 5.2.3. Optical Computing

- 5.2.4. Edge Computing

- 5.2.5. Other Computing Types

- 5.3. Market Analysis, Insights and Forecast - by Deployement

- 5.3.1. Cloud

- 5.3.2. On-Premise

- 5.4. Market Analysis, Insights and Forecast - by End-user

- 5.4.1. Automotive & Transportation

- 5.4.2. Energy & Utilities

- 5.4.3. Healthcare

- 5.4.4. BFSI

- 5.4.5. Aerospace & Defense

- 5.4.6. Media & Entertainment

- 5.4.7. IT & Telecom

- 5.4.8. Retail

- 5.4.9. Manufacturing

- 5.4.10. Other End Users

- 5.5. Market Analysis, Insights and Forecast - by Region

- 5.5.1. North America

- 5.5.2. Europe

- 5.5.3. Asia

- 5.5.4. Australia and New Zealand

- 5.5.5. Latin America

- 5.5.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. North America Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.2. Software

- 6.1.3. Services

- 6.2. Market Analysis, Insights and Forecast - by Computing Type

- 6.2.1. High-Performance Computing

- 6.2.2. Quantum Computing

- 6.2.3. Optical Computing

- 6.2.4. Edge Computing

- 6.2.5. Other Computing Types

- 6.3. Market Analysis, Insights and Forecast - by Deployement

- 6.3.1. Cloud

- 6.3.2. On-Premise

- 6.4. Market Analysis, Insights and Forecast - by End-user

- 6.4.1. Automotive & Transportation

- 6.4.2. Energy & Utilities

- 6.4.3. Healthcare

- 6.4.4. BFSI

- 6.4.5. Aerospace & Defense

- 6.4.6. Media & Entertainment

- 6.4.7. IT & Telecom

- 6.4.8. Retail

- 6.4.9. Manufacturing

- 6.4.10. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Europe Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Component

- 7.1.1. Hardware

- 7.1.2. Software

- 7.1.3. Services

- 7.2. Market Analysis, Insights and Forecast - by Computing Type

- 7.2.1. High-Performance Computing

- 7.2.2. Quantum Computing

- 7.2.3. Optical Computing

- 7.2.4. Edge Computing

- 7.2.5. Other Computing Types

- 7.3. Market Analysis, Insights and Forecast - by Deployement

- 7.3.1. Cloud

- 7.3.2. On-Premise

- 7.4. Market Analysis, Insights and Forecast - by End-user

- 7.4.1. Automotive & Transportation

- 7.4.2. Energy & Utilities

- 7.4.3. Healthcare

- 7.4.4. BFSI

- 7.4.5. Aerospace & Defense

- 7.4.6. Media & Entertainment

- 7.4.7. IT & Telecom

- 7.4.8. Retail

- 7.4.9. Manufacturing

- 7.4.10. Other End Users

- 7.1. Market Analysis, Insights and Forecast - by Component

- 8. Asia Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Component

- 8.1.1. Hardware

- 8.1.2. Software

- 8.1.3. Services

- 8.2. Market Analysis, Insights and Forecast - by Computing Type

- 8.2.1. High-Performance Computing

- 8.2.2. Quantum Computing

- 8.2.3. Optical Computing

- 8.2.4. Edge Computing

- 8.2.5. Other Computing Types

- 8.3. Market Analysis, Insights and Forecast - by Deployement

- 8.3.1. Cloud

- 8.3.2. On-Premise

- 8.4. Market Analysis, Insights and Forecast - by End-user

- 8.4.1. Automotive & Transportation

- 8.4.2. Energy & Utilities

- 8.4.3. Healthcare

- 8.4.4. BFSI

- 8.4.5. Aerospace & Defense

- 8.4.6. Media & Entertainment

- 8.4.7. IT & Telecom

- 8.4.8. Retail

- 8.4.9. Manufacturing

- 8.4.10. Other End Users

- 8.1. Market Analysis, Insights and Forecast - by Component

- 9. Australia and New Zealand Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Component

- 9.1.1. Hardware

- 9.1.2. Software

- 9.1.3. Services

- 9.2. Market Analysis, Insights and Forecast - by Computing Type

- 9.2.1. High-Performance Computing

- 9.2.2. Quantum Computing

- 9.2.3. Optical Computing

- 9.2.4. Edge Computing

- 9.2.5. Other Computing Types

- 9.3. Market Analysis, Insights and Forecast - by Deployement

- 9.3.1. Cloud

- 9.3.2. On-Premise

- 9.4. Market Analysis, Insights and Forecast - by End-user

- 9.4.1. Automotive & Transportation

- 9.4.2. Energy & Utilities

- 9.4.3. Healthcare

- 9.4.4. BFSI

- 9.4.5. Aerospace & Defense

- 9.4.6. Media & Entertainment

- 9.4.7. IT & Telecom

- 9.4.8. Retail

- 9.4.9. Manufacturing

- 9.4.10. Other End Users

- 9.1. Market Analysis, Insights and Forecast - by Component

- 10. Latin America Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Component

- 10.1.1. Hardware

- 10.1.2. Software

- 10.1.3. Services

- 10.2. Market Analysis, Insights and Forecast - by Computing Type

- 10.2.1. High-Performance Computing

- 10.2.2. Quantum Computing

- 10.2.3. Optical Computing

- 10.2.4. Edge Computing

- 10.2.5. Other Computing Types

- 10.3. Market Analysis, Insights and Forecast - by Deployement

- 10.3.1. Cloud

- 10.3.2. On-Premise

- 10.4. Market Analysis, Insights and Forecast - by End-user

- 10.4.1. Automotive & Transportation

- 10.4.2. Energy & Utilities

- 10.4.3. Healthcare

- 10.4.4. BFSI

- 10.4.5. Aerospace & Defense

- 10.4.6. Media & Entertainment

- 10.4.7. IT & Telecom

- 10.4.8. Retail

- 10.4.9. Manufacturing

- 10.4.10. Other End Users

- 10.1. Market Analysis, Insights and Forecast - by Component

- 11. Middle East and Africa Next-generation Computing Market Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Component

- 11.1.1. Hardware

- 11.1.2. Software

- 11.1.3. Services

- 11.2. Market Analysis, Insights and Forecast - by Computing Type

- 11.2.1. High-Performance Computing

- 11.2.2. Quantum Computing

- 11.2.3. Optical Computing

- 11.2.4. Edge Computing

- 11.2.5. Other Computing Types

- 11.3. Market Analysis, Insights and Forecast - by Deployement

- 11.3.1. Cloud

- 11.3.2. On-Premise

- 11.4. Market Analysis, Insights and Forecast - by End-user

- 11.4.1. Automotive & Transportation

- 11.4.2. Energy & Utilities

- 11.4.3. Healthcare

- 11.4.4. BFSI

- 11.4.5. Aerospace & Defense

- 11.4.6. Media & Entertainment

- 11.4.7. IT & Telecom

- 11.4.8. Retail

- 11.4.9. Manufacturing

- 11.4.10. Other End Users

- 11.1. Market Analysis, Insights and Forecast - by Component

- 12. Competitive Analysis

- 12.1. Global Market Share Analysis 2025

- 12.2. Company Profiles

- 12.2.1 IBM Corporation

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Alibaba Group Holding Limited

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 Google LLC

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Microsoft Corporation

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Amazon Web Services Inc

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 NVIDIA Corp

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 NEC Corporation

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Oracle Corporation

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Cisco Systems

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 Intel Corporation

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.1 IBM Corporation

List of Figures

- Figure 1: Global Next-generation Computing Market Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Next-generation Computing Market Volume Breakdown (K Unit, %) by Region 2025 & 2033

- Figure 3: North America Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 4: North America Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 5: North America Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 6: North America Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 7: North America Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 8: North America Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 9: North America Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 10: North America Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 11: North America Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 12: North America Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 13: North America Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 14: North America Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 15: North America Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 16: North America Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 17: North America Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 18: North America Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 19: North America Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 20: North America Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 21: North America Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 22: North America Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 23: Europe Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 24: Europe Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 25: Europe Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 26: Europe Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 27: Europe Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 28: Europe Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 29: Europe Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 30: Europe Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 31: Europe Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 32: Europe Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 33: Europe Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 34: Europe Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 35: Europe Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 36: Europe Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 37: Europe Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 38: Europe Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 39: Europe Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 40: Europe Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 41: Europe Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 42: Europe Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 43: Asia Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 44: Asia Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 45: Asia Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 46: Asia Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 47: Asia Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 48: Asia Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 49: Asia Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 50: Asia Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 51: Asia Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 52: Asia Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 53: Asia Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 54: Asia Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 55: Asia Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 56: Asia Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 57: Asia Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 58: Asia Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 59: Asia Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 60: Asia Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 61: Asia Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 62: Asia Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 63: Australia and New Zealand Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 64: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 65: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 66: Australia and New Zealand Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 67: Australia and New Zealand Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 68: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 69: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 70: Australia and New Zealand Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 71: Australia and New Zealand Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 72: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 73: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 74: Australia and New Zealand Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 75: Australia and New Zealand Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 76: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 77: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 78: Australia and New Zealand Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 79: Australia and New Zealand Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 80: Australia and New Zealand Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 81: Australia and New Zealand Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 82: Australia and New Zealand Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 83: Latin America Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 84: Latin America Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 85: Latin America Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 86: Latin America Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 87: Latin America Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 88: Latin America Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 89: Latin America Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 90: Latin America Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 91: Latin America Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 92: Latin America Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 93: Latin America Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 94: Latin America Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 95: Latin America Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 96: Latin America Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 97: Latin America Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 98: Latin America Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 99: Latin America Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 100: Latin America Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 101: Latin America Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 102: Latin America Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

- Figure 103: Middle East and Africa Next-generation Computing Market Revenue (Million), by Component 2025 & 2033

- Figure 104: Middle East and Africa Next-generation Computing Market Volume (K Unit), by Component 2025 & 2033

- Figure 105: Middle East and Africa Next-generation Computing Market Revenue Share (%), by Component 2025 & 2033

- Figure 106: Middle East and Africa Next-generation Computing Market Volume Share (%), by Component 2025 & 2033

- Figure 107: Middle East and Africa Next-generation Computing Market Revenue (Million), by Computing Type 2025 & 2033

- Figure 108: Middle East and Africa Next-generation Computing Market Volume (K Unit), by Computing Type 2025 & 2033

- Figure 109: Middle East and Africa Next-generation Computing Market Revenue Share (%), by Computing Type 2025 & 2033

- Figure 110: Middle East and Africa Next-generation Computing Market Volume Share (%), by Computing Type 2025 & 2033

- Figure 111: Middle East and Africa Next-generation Computing Market Revenue (Million), by Deployement 2025 & 2033

- Figure 112: Middle East and Africa Next-generation Computing Market Volume (K Unit), by Deployement 2025 & 2033

- Figure 113: Middle East and Africa Next-generation Computing Market Revenue Share (%), by Deployement 2025 & 2033

- Figure 114: Middle East and Africa Next-generation Computing Market Volume Share (%), by Deployement 2025 & 2033

- Figure 115: Middle East and Africa Next-generation Computing Market Revenue (Million), by End-user 2025 & 2033

- Figure 116: Middle East and Africa Next-generation Computing Market Volume (K Unit), by End-user 2025 & 2033

- Figure 117: Middle East and Africa Next-generation Computing Market Revenue Share (%), by End-user 2025 & 2033

- Figure 118: Middle East and Africa Next-generation Computing Market Volume Share (%), by End-user 2025 & 2033

- Figure 119: Middle East and Africa Next-generation Computing Market Revenue (Million), by Country 2025 & 2033

- Figure 120: Middle East and Africa Next-generation Computing Market Volume (K Unit), by Country 2025 & 2033

- Figure 121: Middle East and Africa Next-generation Computing Market Revenue Share (%), by Country 2025 & 2033

- Figure 122: Middle East and Africa Next-generation Computing Market Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 3: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 4: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 5: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 6: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 7: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 8: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 9: Global Next-generation Computing Market Revenue Million Forecast, by Region 2020 & 2033

- Table 10: Global Next-generation Computing Market Volume K Unit Forecast, by Region 2020 & 2033

- Table 11: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 12: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 13: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 14: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 15: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 16: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 17: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 18: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 19: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 20: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 21: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 22: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 23: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 24: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 25: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 26: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 27: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 28: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 29: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 30: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 31: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 32: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 33: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 34: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 35: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 36: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 37: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 38: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 39: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 41: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 42: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 43: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 44: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 45: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 46: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 47: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 48: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 49: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 50: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 51: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 52: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 53: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 54: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 55: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 56: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 57: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 58: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 59: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 60: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

- Table 61: Global Next-generation Computing Market Revenue Million Forecast, by Component 2020 & 2033

- Table 62: Global Next-generation Computing Market Volume K Unit Forecast, by Component 2020 & 2033

- Table 63: Global Next-generation Computing Market Revenue Million Forecast, by Computing Type 2020 & 2033

- Table 64: Global Next-generation Computing Market Volume K Unit Forecast, by Computing Type 2020 & 2033

- Table 65: Global Next-generation Computing Market Revenue Million Forecast, by Deployement 2020 & 2033

- Table 66: Global Next-generation Computing Market Volume K Unit Forecast, by Deployement 2020 & 2033

- Table 67: Global Next-generation Computing Market Revenue Million Forecast, by End-user 2020 & 2033

- Table 68: Global Next-generation Computing Market Volume K Unit Forecast, by End-user 2020 & 2033

- Table 69: Global Next-generation Computing Market Revenue Million Forecast, by Country 2020 & 2033

- Table 70: Global Next-generation Computing Market Volume K Unit Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Next-generation Computing Market?

The projected CAGR is approximately 19.38%.

2. Which companies are prominent players in the Next-generation Computing Market?

Key companies in the market include IBM Corporation, Alibaba Group Holding Limited, Google LLC, Microsoft Corporation, Amazon Web Services Inc, NVIDIA Corp, NEC Corporation, Oracle Corporation, Cisco Systems, Intel Corporation.

3. What are the main segments of the Next-generation Computing Market?

The market segments include Component, Computing Type, Deployement, End-user.

4. Can you provide details about the market size?

The market size is estimated to be USD 191.62 Million as of 2022.

5. What are some drivers contributing to market growth?

Growth in demand for high performance computing; Adoption of Advanced Analytics in SMEs.

6. What are the notable trends driving market growth?

The Cloud Deployment of The Solutions Significantly Contributes to The Market Growth.

7. Are there any restraints impacting market growth?

Risk of Data Breach in Storing and Processing Large Data in Next-gen Computing; High operational challenges in Implementing the Solution.

8. Can you provide examples of recent developments in the market?

July 2023: Moody's and Microsoft have partnered strategically to co-create next-generation data, analytics, research, collaboration, and risk solutions for financial services, which would be built by combining Microsoft's Azure OpenAI Service, Fabric, and Teams with Moody's proprietary data, analytics, and research and has been designed to enhance insights into corporate intelligence and risk assessment.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Next-generation Computing Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Next-generation Computing Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Next-generation Computing Market?

To stay informed about further developments, trends, and reports in the Next-generation Computing Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence