Key Insights

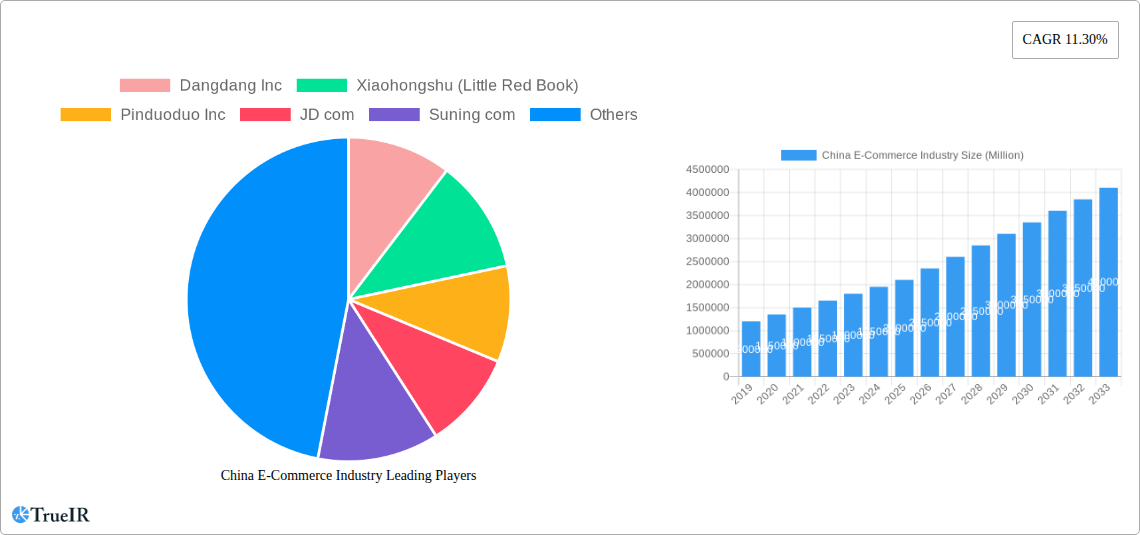

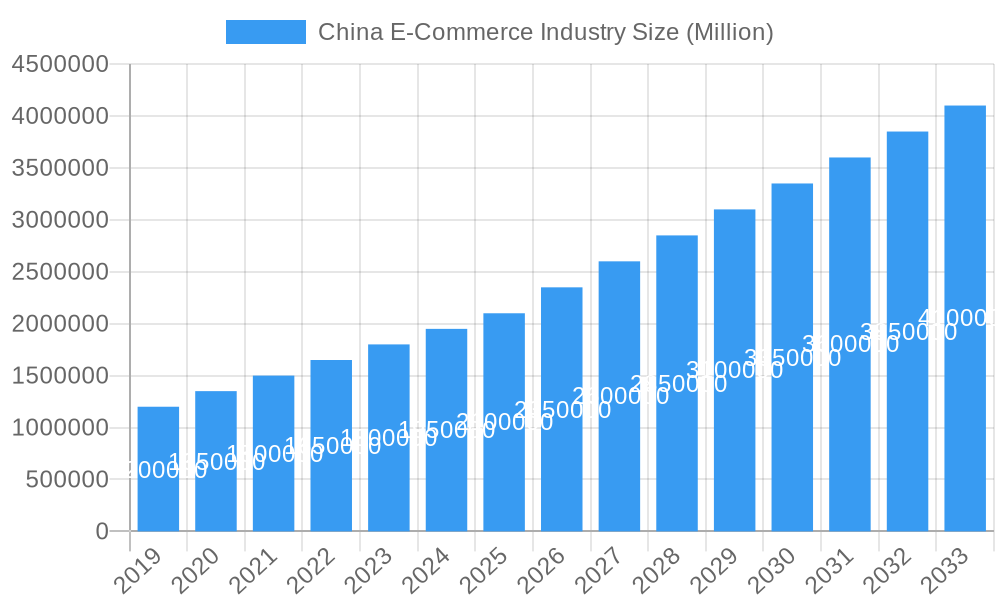

The China E-commerce Market is projected for significant expansion, driven by a digitally adept populace and increasing internet accessibility. Expected to reach a market size of 885.5 billion USD, the industry anticipates a Compound Annual Growth Rate (CAGR) of 21.5% from 2024 to 2033. Key growth catalysts include a burgeoning middle class with augmented purchasing power, the pervasive adoption of mobile commerce, and advanced logistics infrastructure facilitating efficient nationwide delivery. Continuous innovation in e-commerce platforms, prioritizing personalized user experiences and interactive features, further stimulates consumer expenditure and engagement.

China E-Commerce Industry Market Size (In Million)

The market is primarily segmented into B2C and B2B e-commerce, with B2C leading due to its direct consumer focus. Prominent B2C segments include Fashion & Apparel, Beauty & Personal Care, and Consumer Electronics, reflecting shifting consumer preferences for online procurement. Emerging trends such as social commerce, prominently featured on platforms like Xiaohongshu, alongside the sustained influence of major players like Alibaba and JD.com, are redefining the competitive environment. Challenges include intensifying competition, evolving regulatory frameworks, and the imperative for ongoing adaptation to technological advancements and changing consumer behaviors. The presence of innovative entities such as Pinduoduo, recognized for its group-buying strategy, and Vipshop, specializing in flash sales, highlights the market's dynamic and competitive nature.

China E-Commerce Industry Company Market Share

China E-Commerce Industry Market Structure & Competitive Landscape

The China e-commerce industry exhibits a dynamic market structure, characterized by high concentration within dominant players and intense competition. Innovation is a key differentiator, with companies constantly evolving their platforms and services to capture market share. Regulatory impacts, while sometimes presenting hurdles, also shape the landscape by fostering fairer competition and consumer protection. Product substitutes are abundant, forcing established players to continuously innovate and differentiate their offerings. End-user segmentation is critical, with companies tailoring their strategies to diverse consumer groups and their purchasing behaviors across various product categories. Mergers and acquisitions (M&A) trends are prevalent, indicating a maturing market where consolidation and strategic alliances are common. For instance, Alibaba Group continues to dominate with its vast ecosystem. Recent M&A activity, totaling approximately $5,000 Million in the historical period 2019-2024, reflects a strategic drive for market expansion and diversification. Concentration ratios, particularly in the B2C segment, remain high, with the top three players accounting for over 75% of the market share.

China E-Commerce Industry Market Trends & Opportunities

The China e-commerce industry is poised for sustained, robust growth, projected to reach a market size of over $5,000,000 Million by 2033. This expansion is fueled by a confluence of accelerating technological advancements, evolving consumer preferences, and a highly competitive market environment. The compound annual growth rate (CAGR) is estimated at a significant 15.5% from 2025 to 2033. A key trend is the escalating penetration of mobile commerce, with over 85% of e-commerce transactions now occurring via smartphones, driven by widespread internet access and user-friendly mobile applications. Social commerce continues its meteoric rise, with platforms like Xiaohongshu (Little Red Book) and Pinduoduo Inc. integrating social interaction and influencer marketing to drive sales. Live streaming e-commerce has become a powerful sales channel, generating billions in revenue and transforming how products are discovered and purchased.

The industry is also witnessing a shift towards greater personalization, with AI and big data analytics enabling e-commerce giants to offer tailored recommendations and shopping experiences. This hyper-personalization is crucial for retaining customers in a fiercely competitive landscape. The demand for cross-border e-commerce is also surging, as Chinese consumers seek access to international brands and products, while Chinese businesses increasingly look to expand their global reach. This trend is supported by government initiatives aimed at facilitating international trade and improving logistics.

Technological shifts, such as the adoption of augmented reality (AR) for virtual try-ons and the exploration of blockchain for supply chain transparency, are further enhancing the online shopping experience. Emerging technologies are not just enhancing convenience but also building trust and authenticity in the digital marketplace. The competitive dynamics are characterized by aggressive marketing campaigns, strategic partnerships, and a relentless focus on user experience. Companies are investing heavily in logistics and supply chain optimization to ensure faster delivery times and reduce operational costs, a critical factor for customer satisfaction. The increasing adoption of digital payment systems, coupled with a growing middle class and rising disposable incomes, provides a fertile ground for continued expansion across all e-commerce segments. The industry's resilience and adaptability, demonstrated through its rapid recovery and growth post-pandemic, underscore its immense potential for the foreseeable future.

Dominant Markets & Segments in China E-Commerce Industry

The China e-commerce industry is overwhelmingly dominated by the Business-to-Consumer (B2C) segment, which accounts for an estimated 80% of the total market value. Within B2C, the market segmentation by application reveals specific areas of exceptional growth and consumer engagement.

- Fashion and Apparel: This segment consistently leads, driven by evolving fashion trends, the influence of social media, and a young, trend-conscious demographic. The market size for fashion and apparel e-commerce is projected to exceed $1,500,000 Million by 2033, exhibiting a CAGR of 17% during the forecast period. Key growth drivers include the rise of independent designers, the increasing demand for sustainable fashion, and the seamless integration of online and offline retail experiences.

- Beauty and Personal Care: This segment is another powerhouse, benefiting from rising disposable incomes and a growing emphasis on self-care and premium products. With an estimated market size of over $1,200,000 Million, its CAGR is expected to be around 16%. The increasing influence of beauty influencers and the growing popularity of imported cosmetic brands fuel this segment's expansion.

- Consumer Electronics: While mature, this segment continues to grow at a steady pace, projected to reach over $1,000,000 Million. Technological innovation, the rapid release of new gadgets, and competitive pricing are key drivers. The adoption of 5G technology and the demand for smart home devices contribute significantly to this segment's sustained growth.

- Food and Beverages: This segment has experienced a dramatic surge, particularly in the historical period 2019-2024, due to convenience and the expansion of fast delivery services. It is estimated to reach $800,000 Million by 2033, with a CAGR of 18%. The increasing demand for fresh produce, ready-to-eat meals, and specialty food items fuels this growth.

- Furniture and Home: This segment is experiencing robust growth as consumers invest more in home improvement and decor. The market size is predicted to exceed $600,000 Million, with a CAGR of 15%. Online visualization tools and improved logistics for larger items are key enablers.

- Others (Toys, DIY, Media, etc.): This diverse category, while individually smaller, collectively contributes significantly. The gaming and entertainment sectors, in particular, are experiencing rapid digital transformation and online sales growth.

The Business-to-Business (B2B) e-commerce segment, though smaller in comparison to B2C, is rapidly evolving. Its market size is projected to grow substantially, with a CAGR of 14%, driven by the digital transformation of traditional industries, increased efficiency in procurement, and the integration of supply chain management solutions. Policies encouraging industrial digitization and the growing adoption of cloud-based B2B platforms are key drivers.

China E-Commerce Industry Product Analysis

China's e-commerce product landscape is characterized by rapid innovation and a strong market fit driven by consumer demand and technological advancements. Key product categories such as fashion and apparel, beauty and personal care, and consumer electronics are constantly refreshed with new designs, features, and user-centric functionalities. Companies like Alibaba and JD.com are at the forefront, leveraging AI for personalized recommendations and offering virtual try-on experiences with augmented reality for fashion and cosmetics. The integration of smart technologies into consumer electronics, from AI-powered home appliances to wearable devices, showcases a commitment to pushing the boundaries of product utility and convenience. This constant influx of novel products, coupled with efficient supply chains, ensures that the Chinese e-commerce market remains vibrant and responsive to evolving consumer needs, creating significant competitive advantages for agile players.

Key Drivers, Barriers & Challenges in China E-Commerce Industry

Key Drivers: The China e-commerce industry is propelled by several powerful forces. Technologically, the widespread adoption of 5G, AI-powered personalization, and augmented reality is enhancing the user experience and creating new avenues for engagement. Economically, a rapidly growing middle class with increasing disposable incomes and a burgeoning demand for diverse products fuels market expansion. Government support, including policies promoting digital infrastructure development and cross-border trade, further accelerates growth. For example, initiatives like "New Retail" encourage the integration of online and offline channels, creating seamless shopping journeys.

Barriers & Challenges: Despite its dynamism, the industry faces significant challenges. Regulatory complexities, including evolving data privacy laws and anti-monopoly regulations, require constant adaptation from companies. Supply chain vulnerabilities, though improving, can still be impacted by geopolitical factors and unforeseen disruptions, potentially affecting delivery times and costs. Competitive pressures are intense, with major players like Alibaba and JD.com constantly vying for market share, leading to high customer acquisition costs. Cybersecurity threats and the need for robust fraud prevention measures also present ongoing challenges. For instance, increased scrutiny on data usage by platforms has led to significant investment in compliance and security infrastructure.

Growth Drivers in the China E-Commerce Industry Market

Several key drivers are propelling the China E-Commerce Industry Market forward. Technological advancements, including the widespread adoption of 5G networks, artificial intelligence for personalized recommendations, and the integration of augmented reality for enhanced shopping experiences, are fundamental. The continued growth of China's middle class, coupled with rising disposable incomes, translates to increased consumer spending power and demand for a wider array of goods and services. Furthermore, government initiatives aimed at fostering digital economy growth, promoting cross-border e-commerce, and investing in logistics infrastructure create a favorable operating environment. The increasing penetration of smartphones and the widespread accessibility of the internet across urban and rural areas ensure a broad consumer base remains connected and engaged with online retail platforms.

Challenges Impacting China E-Commerce Industry Growth

The China E-Commerce Industry faces several significant challenges that impact its growth trajectory. Regulatory uncertainties, particularly concerning data privacy, anti-monopoly regulations, and platform oversight, necessitate continuous adaptation and compliance efforts from businesses, potentially increasing operational costs. Intense market competition, dominated by a few large players like Alibaba and JD.com, can lead to aggressive pricing strategies and high customer acquisition costs, squeezing profit margins for smaller enterprises. Supply chain disruptions, although improving, can still arise from geopolitical tensions, logistical bottlenecks, or unforeseen events, impacting delivery efficiency and customer satisfaction. Cybersecurity threats, including data breaches and online fraud, remain a persistent concern, requiring substantial investment in security measures to maintain consumer trust and platform integrity.

Key Players Shaping the China E-Commerce Industry Market

- Alibaba com

- JD com

- Pinduoduo Inc

- Vipshop Holdings Ltd

- Suning com

- JuMei com

- Xiaohongshu (Little Red Book)

- Mogujie

- Dangdang Inc

- Yihaodian

Significant China E-Commerce Industry Industry Milestones

- January 2022: Major Chinese E-commerce company JD.com formed a strategic partnership with Ottawa-based Shopify to help global brands tap China's enormous appetite for imported goods and help Chinese merchants sell overseas. JD.com promises to simplify access and compliance for Chinese brands and merchants looking to reach consumers in Western markets through the partnership.

- April 2022: SavMobi Technology, Inc., a Nevada corporation, signed a Memorandum of Understanding with Dalian Yuanmeng Media Co., Ltd, a company registered under the laws of the People's Republic of China. Under the MOU, Yuanmeng agreed to provide their client base to collaborate with SVMB to explore China's E-commerce market. The income sharing ratio will be fifty-fifty between both companies. The Company is currently operating in the provision of commercial mobile technical support services in China.

Future Outlook for China E-Commerce Industry Market

The future outlook for the China E-Commerce Industry remains exceptionally bright, with continued growth anticipated through the forecast period ending in 2033. Strategic opportunities abound, driven by the persistent rise of mobile commerce, the innovative integration of social commerce and live streaming, and the increasing demand for personalized online experiences. The expansion into lower-tier cities and rural areas, coupled with the growing appetite for cross-border e-commerce, presents substantial market potential. Investments in advanced logistics, AI-driven customer service, and sustainable e-commerce practices will be crucial for maintaining competitive advantage. The industry is expected to witness further consolidation and strategic alliances as players seek to optimize operations and expand their market reach, ensuring a dynamic and evolving landscape for years to come.

China E-Commerce Industry Segmentation

-

1. B2C E-commerce

-

1.1. Market Segmentation - by Application

- 1.1.1. Beauty and Personal Care

- 1.1.2. Consumer Electronics

- 1.1.3. Fashion and Apparel

- 1.1.4. Food and Beverages

- 1.1.5. Furniture and Home

- 1.1.6. Others (Toys, DIY, Media, etc.)

-

1.1. Market Segmentation - by Application

-

2. Application

- 2.1. Beauty and Personal Care

- 2.2. Consumer Electronics

- 2.3. Fashion and Apparel

- 2.4. Food and Beverages

- 2.5. Furniture and Home

- 2.6. Others (Toys, DIY, Media, etc.)

- 3. Beauty and Personal Care

- 4. Consumer Electronics

- 5. Fashion and Apparel

- 6. Food and Beverages

- 7. Furniture and Home

- 8. Others (Toys, DIY, Media, etc.)

- 9. B2B E-commerce

China E-Commerce Industry Segmentation By Geography

- 1. China

China E-Commerce Industry Regional Market Share

Geographic Coverage of China E-Commerce Industry

China E-Commerce Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by B2C E-commerce

- 5.1.1. Market Segmentation - by Application

- 5.1.1.1. Beauty and Personal Care

- 5.1.1.2. Consumer Electronics

- 5.1.1.3. Fashion and Apparel

- 5.1.1.4. Food and Beverages

- 5.1.1.5. Furniture and Home

- 5.1.1.6. Others (Toys, DIY, Media, etc.)

- 5.1.1. Market Segmentation - by Application

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Beauty and Personal Care

- 5.2.2. Consumer Electronics

- 5.2.3. Fashion and Apparel

- 5.2.4. Food and Beverages

- 5.2.5. Furniture and Home

- 5.2.6. Others (Toys, DIY, Media, etc.)

- 5.3. Market Analysis, Insights and Forecast - by Beauty and Personal Care

- 5.4. Market Analysis, Insights and Forecast - by Consumer Electronics

- 5.5. Market Analysis, Insights and Forecast - by Fashion and Apparel

- 5.6. Market Analysis, Insights and Forecast - by Food and Beverages

- 5.7. Market Analysis, Insights and Forecast - by Furniture and Home

- 5.8. Market Analysis, Insights and Forecast - by Others (Toys, DIY, Media, etc.)

- 5.9. Market Analysis, Insights and Forecast - by B2B E-commerce

- 5.10. Market Analysis, Insights and Forecast - by Region

- 5.10.1. China

- 5.1. Market Analysis, Insights and Forecast - by B2C E-commerce

- 6. China E-Commerce Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by B2C E-commerce

- 6.1.1. Market Segmentation - by Application

- 6.1.1.1. Beauty and Personal Care

- 6.1.1.2. Consumer Electronics

- 6.1.1.3. Fashion and Apparel

- 6.1.1.4. Food and Beverages

- 6.1.1.5. Furniture and Home

- 6.1.1.6. Others (Toys, DIY, Media, etc.)

- 6.1.1. Market Segmentation - by Application

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Beauty and Personal Care

- 6.2.2. Consumer Electronics

- 6.2.3. Fashion and Apparel

- 6.2.4. Food and Beverages

- 6.2.5. Furniture and Home

- 6.2.6. Others (Toys, DIY, Media, etc.)

- 6.3. Market Analysis, Insights and Forecast - by Beauty and Personal Care

- 6.4. Market Analysis, Insights and Forecast - by Consumer Electronics

- 6.5. Market Analysis, Insights and Forecast - by Fashion and Apparel

- 6.6. Market Analysis, Insights and Forecast - by Food and Beverages

- 6.7. Market Analysis, Insights and Forecast - by Furniture and Home

- 6.8. Market Analysis, Insights and Forecast - by Others (Toys, DIY, Media, etc.)

- 6.9. Market Analysis, Insights and Forecast - by B2B E-commerce

- 6.1. Market Analysis, Insights and Forecast - by B2C E-commerce

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Dangdang Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Xiaohongshu (Little Red Book)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Pinduoduo Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 JD com

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Suning com

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 JuMei com

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Mogujie*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Yihaodian

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Alibaba com

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Vipshop Holdings Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Dangdang Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China E-Commerce Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China E-Commerce Industry Share (%) by Company 2025

List of Tables

- Table 1: China E-Commerce Industry Revenue billion Forecast, by B2C E-commerce 2020 & 2033

- Table 2: China E-Commerce Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: China E-Commerce Industry Revenue billion Forecast, by Beauty and Personal Care 2020 & 2033

- Table 4: China E-Commerce Industry Revenue billion Forecast, by Consumer Electronics 2020 & 2033

- Table 5: China E-Commerce Industry Revenue billion Forecast, by Fashion and Apparel 2020 & 2033

- Table 6: China E-Commerce Industry Revenue billion Forecast, by Food and Beverages 2020 & 2033

- Table 7: China E-Commerce Industry Revenue billion Forecast, by Furniture and Home 2020 & 2033

- Table 8: China E-Commerce Industry Revenue billion Forecast, by Others (Toys, DIY, Media, etc.) 2020 & 2033

- Table 9: China E-Commerce Industry Revenue billion Forecast, by B2B E-commerce 2020 & 2033

- Table 10: China E-Commerce Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 11: China E-Commerce Industry Revenue billion Forecast, by B2C E-commerce 2020 & 2033

- Table 12: China E-Commerce Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 13: China E-Commerce Industry Revenue billion Forecast, by Beauty and Personal Care 2020 & 2033

- Table 14: China E-Commerce Industry Revenue billion Forecast, by Consumer Electronics 2020 & 2033

- Table 15: China E-Commerce Industry Revenue billion Forecast, by Fashion and Apparel 2020 & 2033

- Table 16: China E-Commerce Industry Revenue billion Forecast, by Food and Beverages 2020 & 2033

- Table 17: China E-Commerce Industry Revenue billion Forecast, by Furniture and Home 2020 & 2033

- Table 18: China E-Commerce Industry Revenue billion Forecast, by Others (Toys, DIY, Media, etc.) 2020 & 2033

- Table 19: China E-Commerce Industry Revenue billion Forecast, by B2B E-commerce 2020 & 2033

- Table 20: China E-Commerce Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China E-Commerce Industry?

The projected CAGR is approximately 21.5%.

2. Which companies are prominent players in the China E-Commerce Industry?

Key companies in the market include Dangdang Inc, Xiaohongshu (Little Red Book), Pinduoduo Inc, JD com, Suning com, JuMei com, Mogujie*List Not Exhaustive, Yihaodian, Alibaba com, Vipshop Holdings Ltd.

3. What are the main segments of the China E-Commerce Industry?

The market segments include B2C E-commerce, Application, Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverages, Furniture and Home, Others (Toys, DIY, Media, etc.), B2B E-commerce.

4. Can you provide details about the market size?

The market size is estimated to be USD 885.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Livestream E-commerce to drive the Market; Growing Penetration of Online Shoppers to Boost the E-commerce Market.

6. What are the notable trends driving market growth?

Livestream E-commerce to drive the Market.

7. Are there any restraints impacting market growth?

Budget Constraints and Technological Limitations; Regulatory and Legal Challenges.

8. Can you provide examples of recent developments in the market?

January 2022 - Major Chinese E-commerce company JD.com formed a strategic partnership with Ottawa-based Shopify to help global brands tap China's enormous appetite for imported goods and help Chinese merchants sell overseas. JD.com promises to simplify access and compliance for Chinese brands and merchants looking to reach consumers in Western markets through the partnership.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China E-Commerce Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China E-Commerce Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China E-Commerce Industry?

To stay informed about further developments, trends, and reports in the China E-Commerce Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence