Key Insights

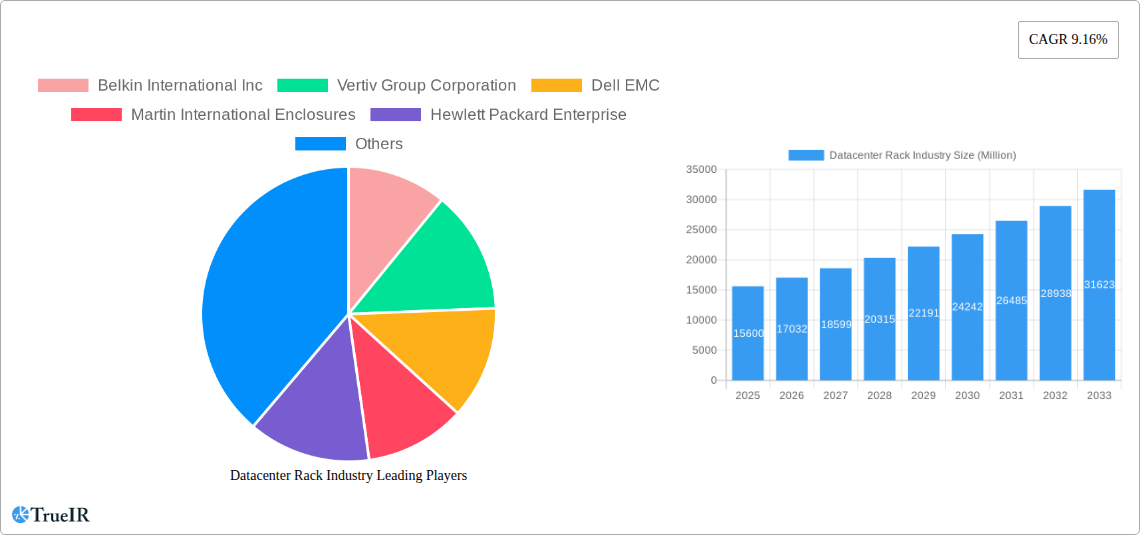

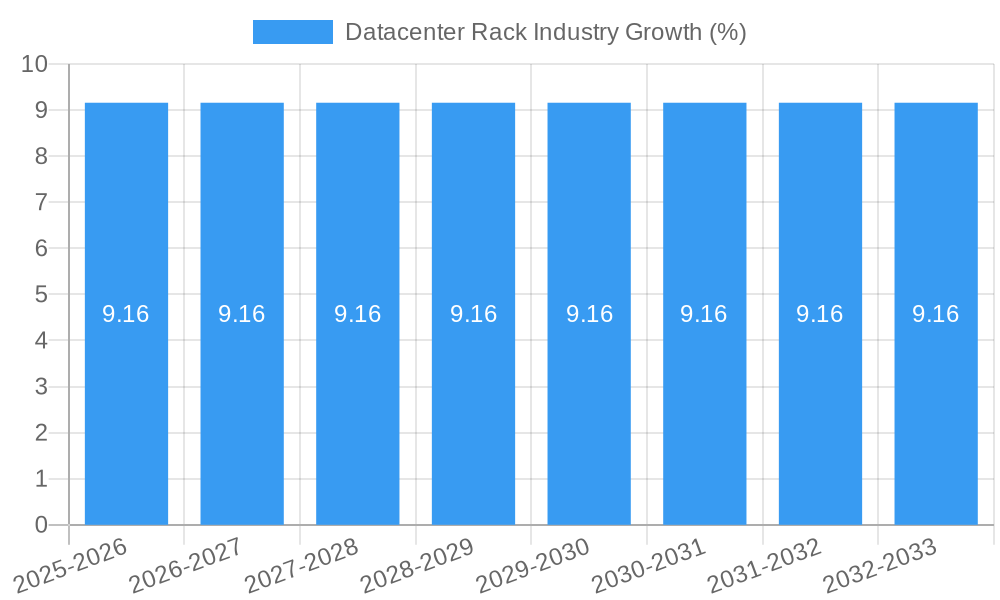

The global datacenter rack market is poised for significant expansion, projected to reach a market size of approximately USD 15,600 million by 2025, growing at a robust Compound Annual Growth Rate (CAGR) of 9.16% through 2033. This upward trajectory is propelled by a confluence of powerful drivers, primarily the insatiable demand for enhanced data storage, processing, and management capabilities. The escalating adoption of cloud computing, the exponential growth of big data analytics, and the proliferation of the Internet of Things (IoT) devices are fundamental forces fueling the need for more sophisticated and scalable datacenter infrastructure, with racks serving as the foundational element for housing critical IT equipment. Furthermore, the continuous innovation in server technology, leading to denser configurations and higher power requirements, necessitates the deployment of advanced rack solutions that offer superior thermal management, power distribution, and physical security. The increasing investment in building new datacenters and expanding existing facilities, driven by both hyperscale cloud providers and enterprise IT departments, underscores the sustained demand for datacenter racks.

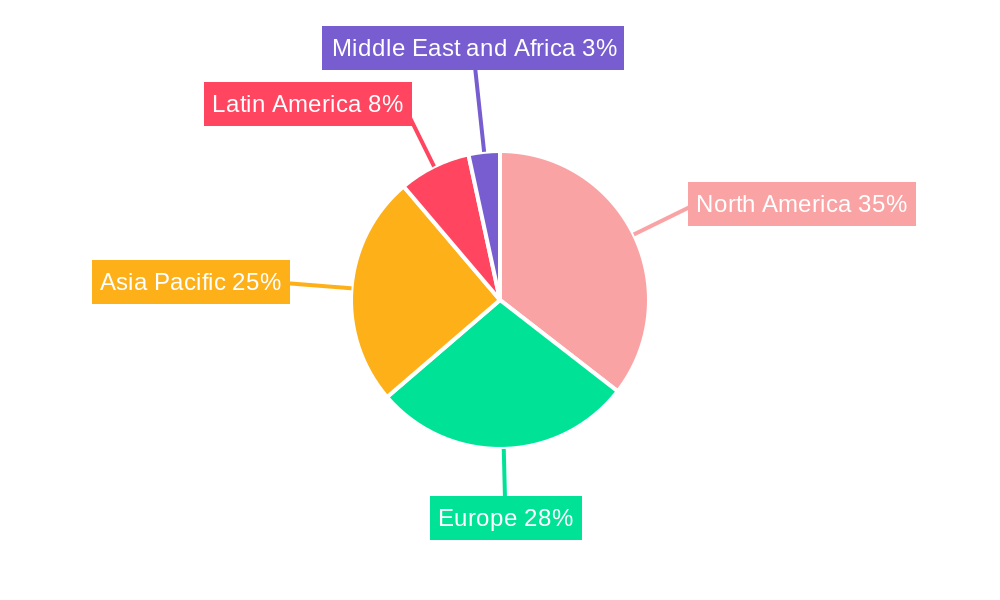

The market segmentation reveals a dynamic landscape, with "Medium" sized racks expected to dominate in terms of volume due to their versatility and suitability for a wide range of datacenter deployments, from enterprise facilities to colocation centers. However, the demand for "Large" racks is anticipated to surge as hyperscale datacenters continue to expand their footprint, requiring higher capacity solutions. On the end-user industry front, the IT and Telecom sector, alongside BFSI (Banking, Financial Services, and Insurance), are expected to remain the largest consumers of datacenter racks, reflecting their critical reliance on robust and secure IT infrastructure. The Manufacturing sector is also emerging as a significant growth area, driven by Industry 4.0 initiatives and the increasing deployment of edge computing solutions. Geographically, North America is anticipated to maintain its leading position, owing to the substantial presence of major cloud providers and a well-established IT infrastructure. Asia Pacific, however, is projected to witness the fastest growth, fueled by rapid digital transformation, increasing internet penetration, and substantial investments in building new datacenters to cater to the burgeoning digital economy. Key players such as Vertiv Group Corporation, Dell EMC, Schneider Electric SE, and Rittal GmbH & Co KG are actively innovating to meet these evolving demands, focusing on modular designs, enhanced cooling solutions, and smart rack technologies.

This in-depth datacenter rack market report provides a definitive analysis of the global industry from 2019 to 2033, with a comprehensive base year of 2025 and an extensive forecast period of 2025–2033. Delve into critical market dynamics, emerging trends, and strategic opportunities within the rapidly evolving IT infrastructure landscape. Explore the impact of colocation data centers, edge computing solutions, and high-density rack deployments on market growth. This report is essential for stakeholders seeking to understand the global datacenter rack market size, key industry players, technological advancements, and future growth trajectories.

Datacenter Rack Industry Market Structure & Competitive Landscape

The datacenter rack industry exhibits a moderately concentrated market structure, driven by a mix of established global manufacturers and specialized regional players. Innovation remains a paramount driver, with companies continuously investing in high-density racks, intelligent rack solutions, and advanced cooling technologies to meet the escalating demands of modern data centers. Regulatory impacts are primarily focused on energy efficiency standards and physical security mandates, influencing product design and deployment strategies. Product substitutes, while limited for core rack functionality, include integrated modular data center solutions and specialized enclosure systems.

Key aspects of market structure include:

- Market Concentration: Dominated by a few major players, but with a significant number of niche providers contributing to market diversity. Concentration ratios are estimated to be around xx% for the top 5 players.

- Innovation Drivers: The exponential growth of data, the proliferation of edge computing, and the need for increased power and cooling efficiency are spurring innovation in server rack design, cable management systems, and integrated power distribution units (PDUs).

- Regulatory Impacts: Stringent energy efficiency regulations and data security compliance are influencing the development of environmentally friendly rack solutions and secure enclosure designs.

- Product Substitutes: While traditional racks are core, pre-fabricated data center modules and custom-built IT infrastructure enclosures offer alternative solutions for specific deployment scenarios.

- End-User Segmentation: The market is broadly segmented by rack units (Small, Medium, Large) and end-user industries such as BFSI, IT and Telecom, Manufacturing, Retail, and others, each with distinct requirements and adoption rates.

- M&A Trends: The industry has witnessed strategic mergers and acquisitions aimed at expanding product portfolios, enhancing geographical reach, and consolidating market share. An estimated xx number of M&A deals were recorded in the historical period (2019-2024).

Datacenter Rack Industry Market Trends & Opportunities

The datacenter rack market is experiencing robust growth, fueled by the insatiable demand for digital infrastructure and the ongoing digital transformation across all sectors. The global market size is projected to reach over $XX Billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of XX% during the 2025-2033 forecast period. This expansion is a direct consequence of the ever-increasing volume of data generated, the rise of AI and machine learning applications, and the distributed nature of modern IT architectures. The increasing adoption of cloud computing services and the strategic deployment of edge data centers to minimize latency are significant market trends that present substantial opportunities for datacenter rack manufacturers.

Consumer preferences are shifting towards more intelligent, modular, and energy-efficient rack solutions. This includes a growing demand for smart racks equipped with integrated monitoring capabilities, hot-swappable components, and advanced thermal management systems to optimize power consumption and cooling efficiency. The trend towards higher rack densities necessitates racks capable of supporting heavier loads and accommodating specialized server hardware, networking equipment, and storage solutions.

Competitive dynamics are intensifying, with key players focusing on product differentiation through innovation, strategic partnerships, and a strong emphasis on customer support. The market penetration of advanced rack enclosure systems is steadily increasing as businesses recognize the value of robust and scalable data center infrastructure. Opportunities abound for companies offering solutions that address specific industry challenges, such as the need for rapid deployment of edge computing infrastructure, enhanced security features for sensitive data, and sustainable data center design. The increasing investment in 5G technology and the subsequent growth in connected devices further amplify the demand for distributed and high-performance datacenter rack solutions.

Dominant Markets & Segments in Datacenter Rack Industry

The datacenter rack industry is characterized by dominant markets and segments that reflect global IT infrastructure trends and regional economic development. North America and Europe currently represent the largest geographical markets, driven by the presence of major cloud providers, extensive enterprise IT investments, and a mature digital economy. Asia-Pacific, however, is emerging as the fastest-growing region, propelled by rapid digitalization, increasing data center construction, and government initiatives supporting the digital infrastructure ecosystem.

Within the rack unit segmentation, Large Rack Units are experiencing the most significant growth, catering to the demands of hyperscale data centers, enterprise colocation facilities, and high-performance computing (HPC) environments. The need for accommodating a high density of servers, storage, and networking equipment within a single footprint drives this demand.

The IT and Telecom end-user industry remains the largest segment, consistently investing in network expansion, cloud infrastructure upgrades, and the deployment of new technologies. This sector's continuous need for robust and scalable rack solutions underpins its market dominance. The BFSI sector is another significant driver, with its increasing reliance on data analytics, digital banking platforms, and stringent data security requirements demanding high-quality datacenter racks.

Key growth drivers for dominant markets and segments include:

- Infrastructure Development: Massive investments in building new data centers, expanding existing facilities, and establishing edge data center locations worldwide.

- Digital Transformation: The widespread adoption of digital technologies across all industries, leading to an exponential increase in data generation and processing needs.

- Technological Advancements: The proliferation of technologies like 5G, AI, IoT, and blockchain requiring powerful and distributed data processing capabilities.

- Cloud Computing Adoption: The continued migration of workloads to the cloud, driving demand for colocation data center racks and specialized cloud infrastructure solutions.

- Edge Computing Expansion: The growing need for low-latency processing closer to data sources, leading to the deployment of smaller, distributed edge data centers requiring compact and efficient rack solutions.

- Government Policies and Initiatives: Supportive government policies promoting digital infrastructure development, data localization, and smart city projects are accelerating market growth in key regions.

Datacenter Rack Industry Product Analysis

The datacenter rack industry is witnessing a surge in product innovation, focusing on enhanced functionality, improved efficiency, and greater adaptability. Key product innovations include the development of high-density racks capable of supporting massive server deployments and advanced cooling solutions integrated directly into the rack design. Intelligent racks equipped with real-time monitoring, environmental sensors, and remote management capabilities are becoming increasingly prevalent, offering greater control and visibility over data center operations. Furthermore, the trend towards modular and prefabricated data center solutions is driving the demand for standardized and easily deployable rack systems that can be quickly integrated into larger infrastructure projects. Competitive advantages are being gained by manufacturers who can offer customized solutions, superior cable management, robust build quality, and seamless integration with other data center infrastructure components like power distribution units (PDUs) and uninterruptible power supplies (UPS).

Key Drivers, Barriers & Challenges in Datacenter Rack Industry

The datacenter rack industry is propelled by several key drivers, including the relentless growth of data, the widespread adoption of cloud computing, and the burgeoning demand for edge computing solutions. Technological advancements in areas like AI, IoT, and 5G necessitate more robust and scalable data center infrastructure. Government initiatives promoting digitalization and the construction of new data centers also act as significant growth catalysts.

However, the industry faces substantial challenges. Supply chain disruptions, as experienced globally in recent years, can impact the availability of raw materials and components, leading to production delays and increased costs. Regulatory hurdles related to environmental sustainability and energy efficiency can add complexity to product development and compliance. Intense competitive pressures from both established players and emerging manufacturers can squeeze profit margins. Economic downturns and geopolitical instability can also dampen investment in new data center projects, indirectly affecting rack demand.

Growth Drivers in the Datacenter Rack Industry Market

The datacenter rack industry market is experiencing significant growth driven by a confluence of technological, economic, and regulatory factors. The exponential increase in data generation from IoT devices, social media, and big data analytics necessitates continuous expansion of data center capacity. The ongoing shift towards cloud computing and the widespread adoption of Software-Defined Data Centers (SDDC) are creating sustained demand for flexible and scalable rack solutions. Furthermore, the strategic imperative to reduce latency and enhance real-time data processing is fueling the rapid growth of edge computing, driving the deployment of smaller, distributed data centers requiring specialized rack configurations. Government initiatives aimed at fostering digital economies and supporting infrastructure development are also key growth catalysts.

Challenges Impacting Datacenter Rack Industry Growth

Several challenges can impact the growth trajectory of the datacenter rack industry. Navigating complex and evolving environmental regulations concerning energy consumption and waste management requires significant investment in sustainable product design and manufacturing processes. Persistent supply chain vulnerabilities, including material shortages and transportation bottlenecks, can lead to production delays and increased costs, affecting order fulfillment and pricing. The intense competitive landscape, marked by price wars and the need for continuous innovation, can pressure profit margins for manufacturers. Furthermore, global economic uncertainties and geopolitical risks can lead to reduced enterprise spending on IT infrastructure, thereby tempering demand for datacenter racks. The increasing sophistication of cybersecurity threats also demands racks with enhanced physical security features, adding to development costs and complexity.

Key Players Shaping the Datacenter Rack Industry Market

- Belkin International Inc

- Vertiv Group Corporation

- Dell EMC

- Martin International Enclosures

- Hewlett Packard Enterprise

- Schneider Electric SE

- Rittal GmbH & Co KG

- Legrand SA

- Black Box Corporation

- Kendall Howard LLC

- Oracle Corporation

- Fujitsu Corporation

Significant Datacenter Rack Industry Industry Milestones

- October 2022: NetRack launched iRack Block, a solution designed to cater to large requirements, moving towards intelligent infra capsules or modular data centers with self-cooking, self-powered, and self-contained capabilities, in contrast to their smaller iRack solution.

- June 2022: Schneider Electric partnered with Stratus Technologies and Avnet Integrated to enable streamlined, zero-touch edge computing and drive industrial innovation through their respective edge platforms and integration services.

Future Outlook for Datacenter Rack Industry Market

The future outlook for the datacenter rack industry is exceptionally bright, driven by persistent demand for digital infrastructure and ongoing technological advancements. The continued expansion of cloud services, the rapid growth of edge computing deployments, and the increasing adoption of data-intensive technologies like AI and 5G will fuel sustained market growth. Strategic opportunities lie in developing innovative solutions for high-density computing, sustainable data center designs, and integrated smart rack technologies. The market is poised for significant expansion as businesses across all sectors continue to invest heavily in their digital transformation journeys, requiring robust, efficient, and scalable datacenter rack solutions to support their evolving IT needs.

Datacenter Rack Industry Segmentation

-

1. Rack Units

- 1.1. Small

- 1.2. Medium

- 1.3. Large

-

2. End-user Industry

- 2.1. BFSI

- 2.2. IT and Telecom

- 2.3. Manufacturing

- 2.4. Retail

- 2.5. Other End-user Industries

Datacenter Rack Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Datacenter Rack Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 9.16% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Deployment of Data Center Facilities; Growing Cloud Computing Adoption Leading to Investment in Hyperscale Data Centers; BFSI Sector Expected to Hold a Significant Share

- 3.3. Market Restrains

- 3.3.1. Increasing Utilization of Blade Servers

- 3.4. Market Trends

- 3.4.1. BFSI Sector Expected to Hold a Significant Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Rack Units

- 5.1.1. Small

- 5.1.2. Medium

- 5.1.3. Large

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. BFSI

- 5.2.2. IT and Telecom

- 5.2.3. Manufacturing

- 5.2.4. Retail

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Latin America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Rack Units

- 6. North America Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Rack Units

- 6.1.1. Small

- 6.1.2. Medium

- 6.1.3. Large

- 6.2. Market Analysis, Insights and Forecast - by End-user Industry

- 6.2.1. BFSI

- 6.2.2. IT and Telecom

- 6.2.3. Manufacturing

- 6.2.4. Retail

- 6.2.5. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Rack Units

- 7. Europe Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Rack Units

- 7.1.1. Small

- 7.1.2. Medium

- 7.1.3. Large

- 7.2. Market Analysis, Insights and Forecast - by End-user Industry

- 7.2.1. BFSI

- 7.2.2. IT and Telecom

- 7.2.3. Manufacturing

- 7.2.4. Retail

- 7.2.5. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Rack Units

- 8. Asia Pacific Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Rack Units

- 8.1.1. Small

- 8.1.2. Medium

- 8.1.3. Large

- 8.2. Market Analysis, Insights and Forecast - by End-user Industry

- 8.2.1. BFSI

- 8.2.2. IT and Telecom

- 8.2.3. Manufacturing

- 8.2.4. Retail

- 8.2.5. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Rack Units

- 9. Latin America Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Rack Units

- 9.1.1. Small

- 9.1.2. Medium

- 9.1.3. Large

- 9.2. Market Analysis, Insights and Forecast - by End-user Industry

- 9.2.1. BFSI

- 9.2.2. IT and Telecom

- 9.2.3. Manufacturing

- 9.2.4. Retail

- 9.2.5. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Rack Units

- 10. Middle East and Africa Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Rack Units

- 10.1.1. Small

- 10.1.2. Medium

- 10.1.3. Large

- 10.2. Market Analysis, Insights and Forecast - by End-user Industry

- 10.2.1. BFSI

- 10.2.2. IT and Telecom

- 10.2.3. Manufacturing

- 10.2.4. Retail

- 10.2.5. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Rack Units

- 11. North America Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Europe Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Asia Pacific Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Latin America Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Middle East and Africa Datacenter Rack Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Belkin International Inc

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Vertiv Group Corporation

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Dell EMC

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Martin International Enclosures

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Hewlett Packard Enterprise

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Schneider Electric SE

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Rittal GmbH & Co KG

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Legrand SA*List Not Exhaustive

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Black Box Corporation

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Kendall Howard LLC

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Oracle Corporation

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 Fujitsu Corporation

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.1 Belkin International Inc

List of Figures

- Figure 1: Global Datacenter Rack Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Latin America Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Latin America Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Middle East and Africa Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Middle East and Africa Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America Datacenter Rack Industry Revenue (Million), by Rack Units 2024 & 2032

- Figure 13: North America Datacenter Rack Industry Revenue Share (%), by Rack Units 2024 & 2032

- Figure 14: North America Datacenter Rack Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 15: North America Datacenter Rack Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 16: North America Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Datacenter Rack Industry Revenue (Million), by Rack Units 2024 & 2032

- Figure 19: Europe Datacenter Rack Industry Revenue Share (%), by Rack Units 2024 & 2032

- Figure 20: Europe Datacenter Rack Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 21: Europe Datacenter Rack Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 22: Europe Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific Datacenter Rack Industry Revenue (Million), by Rack Units 2024 & 2032

- Figure 25: Asia Pacific Datacenter Rack Industry Revenue Share (%), by Rack Units 2024 & 2032

- Figure 26: Asia Pacific Datacenter Rack Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 27: Asia Pacific Datacenter Rack Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 28: Asia Pacific Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Latin America Datacenter Rack Industry Revenue (Million), by Rack Units 2024 & 2032

- Figure 31: Latin America Datacenter Rack Industry Revenue Share (%), by Rack Units 2024 & 2032

- Figure 32: Latin America Datacenter Rack Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 33: Latin America Datacenter Rack Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 34: Latin America Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Latin America Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Middle East and Africa Datacenter Rack Industry Revenue (Million), by Rack Units 2024 & 2032

- Figure 37: Middle East and Africa Datacenter Rack Industry Revenue Share (%), by Rack Units 2024 & 2032

- Figure 38: Middle East and Africa Datacenter Rack Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 39: Middle East and Africa Datacenter Rack Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 40: Middle East and Africa Datacenter Rack Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: Middle East and Africa Datacenter Rack Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Datacenter Rack Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Datacenter Rack Industry Revenue Million Forecast, by Rack Units 2019 & 2032

- Table 3: Global Datacenter Rack Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 4: Global Datacenter Rack Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Datacenter Rack Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Datacenter Rack Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Datacenter Rack Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Datacenter Rack Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: Datacenter Rack Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global Datacenter Rack Industry Revenue Million Forecast, by Rack Units 2019 & 2032

- Table 16: Global Datacenter Rack Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 17: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Datacenter Rack Industry Revenue Million Forecast, by Rack Units 2019 & 2032

- Table 19: Global Datacenter Rack Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 20: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 21: Global Datacenter Rack Industry Revenue Million Forecast, by Rack Units 2019 & 2032

- Table 22: Global Datacenter Rack Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 23: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Global Datacenter Rack Industry Revenue Million Forecast, by Rack Units 2019 & 2032

- Table 25: Global Datacenter Rack Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 26: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Global Datacenter Rack Industry Revenue Million Forecast, by Rack Units 2019 & 2032

- Table 28: Global Datacenter Rack Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 29: Global Datacenter Rack Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Datacenter Rack Industry?

The projected CAGR is approximately 9.16%.

2. Which companies are prominent players in the Datacenter Rack Industry?

Key companies in the market include Belkin International Inc, Vertiv Group Corporation, Dell EMC, Martin International Enclosures, Hewlett Packard Enterprise, Schneider Electric SE, Rittal GmbH & Co KG, Legrand SA*List Not Exhaustive, Black Box Corporation, Kendall Howard LLC, Oracle Corporation, Fujitsu Corporation.

3. What are the main segments of the Datacenter Rack Industry?

The market segments include Rack Units, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Deployment of Data Center Facilities; Growing Cloud Computing Adoption Leading to Investment in Hyperscale Data Centers; BFSI Sector Expected to Hold a Significant Share.

6. What are the notable trends driving market growth?

BFSI Sector Expected to Hold a Significant Share.

7. Are there any restraints impacting market growth?

Increasing Utilization of Blade Servers.

8. Can you provide examples of recent developments in the market?

October 2022 - In contrast to the smaller installations provided by the iRack solution, NetRack created iRack Block to cater to large requirements primarily. The rack is a step toward intelligent infra capsules or modular data centers because it includes self-cooking, self-powered, and self-contained capabilities.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Datacenter Rack Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Datacenter Rack Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Datacenter Rack Industry?

To stay informed about further developments, trends, and reports in the Datacenter Rack Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence