Key Insights

The South America Thermoplastic Elastomer (TPE) market is projected for substantial growth, anticipating a market size of 30.83 billion by 2025, with a projected Compound Annual Growth Rate (CAGR) of 4.8%. This expansion is attributed to increasing demand in critical sectors including automotive, building and construction, and footwear. The automotive industry is a primary driver, with TPEs favored for lightweight, durable components that enhance fuel efficiency and passenger comfort. In building and construction, TPEs are increasingly adopted for sustainable sealing, gasketing, and insulation solutions due to their excellent weather resistance and flexibility. The footwear sector also significantly contributes, leveraging TPEs for superior comfort, durability, and design versatility.

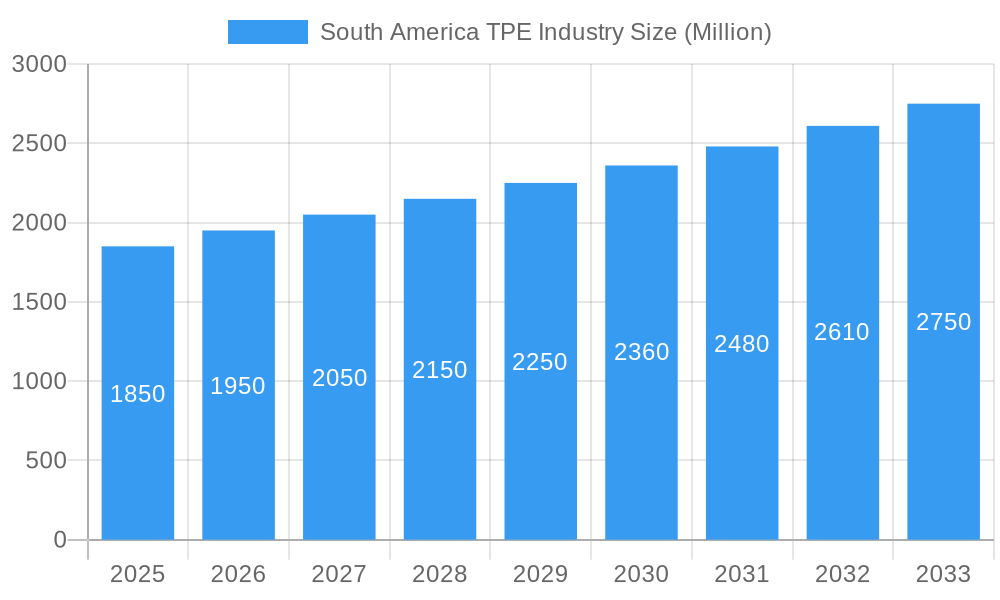

South America TPE Industry Market Size (In Billion)

Key product segments fueling this growth include Thermoplastic Olefin (TPE-O), Thermoplastic Polyurethane (TPU), and Elastomeric Alloys (TPE-V or TPV). TPE-O's versatility and cost-effectiveness make it suitable for consumer goods and automotive parts, while TPU's superior abrasion resistance and mechanical strength are critical for industrial and medical applications. Technological advancements in specialized TPE grades and a regional focus on sustainability and recyclability further propel market demand. Despite challenges such as raw material price volatility, the inherent advantages of TPEs and evolving industry needs in South America present significant market opportunities.

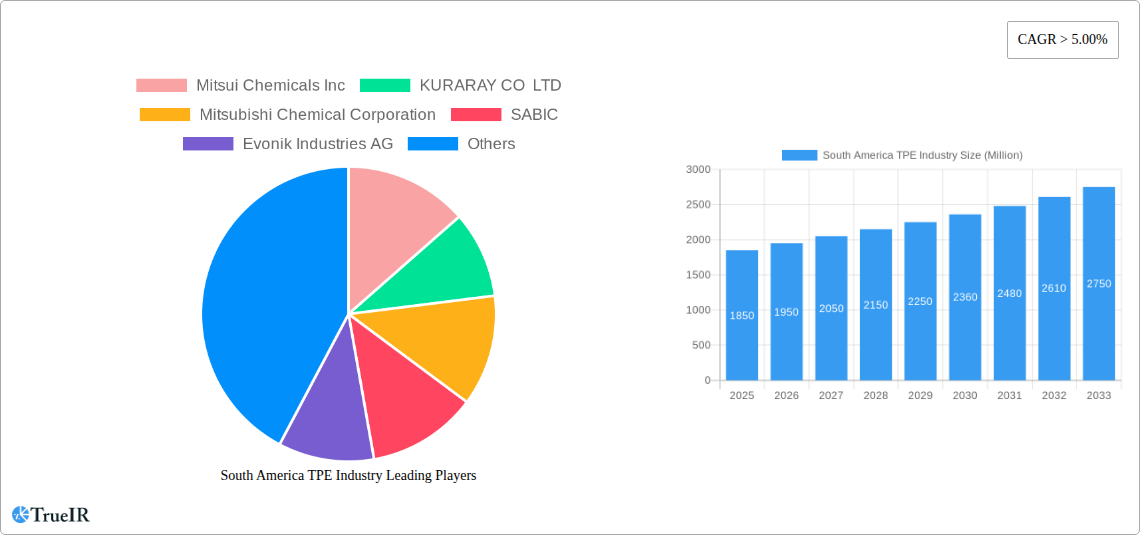

South America TPE Industry Company Market Share

South America TPE Industry Market Analysis: Forecast 2025–2033

This comprehensive report provides an in-depth analysis of the South America Thermoplastic Elastomers (TPE) industry, offering strategic insights and actionable intelligence for stakeholders. Spanning a study period from 2019 to 2033, with a base year of 2025, this report delves into market dynamics, competitive landscapes, emerging trends, and future growth opportunities. Leveraging high-volume keywords like "South America TPE market," "thermoplastic elastomers Brazil," "TPE applications," and "automotive TPE demand," this report is optimized for search engine visibility and engagement with industry professionals.

South America TPE Industry Market Structure & Competitive Landscape

The South America TPE market exhibits a moderately concentrated structure, with major global players and a growing number of regional manufacturers vying for market share. Innovation remains a key differentiator, driven by the constant demand for advanced material properties such as improved durability, flexibility, and eco-friendliness. Regulatory impacts are also significant, with evolving environmental standards and safety regulations influencing product development and adoption across various applications. Product substitutes, including traditional thermoset rubbers and other advanced polymers, present a competitive challenge, necessitating continuous product enhancement and cost optimization by TPE manufacturers. End-user segmentation highlights the automotive and construction sectors as primary consumers, demanding specialized TPE solutions for their evolving needs. Mergers and acquisitions (M&A) trends are observable, with companies strategically consolidating to expand their product portfolios, geographical reach, and technological capabilities. For instance, the past five years have seen an estimated xx Billion USD in M&A activities within the broader South American polymer industry, indicating a trend towards industry consolidation and vertical integration. Concentration ratios, while varying by specific TPE product segment, suggest that the top three players collectively hold approximately xx% of the market share for Styrenic Block Copolymers (TPE-S).

South America TPE Industry Market Trends & Opportunities

The South America TPE industry is poised for substantial growth, driven by a confluence of economic, technological, and societal factors. The estimated market size for TPEs in South America is projected to reach approximately $4.5 Billion USD by 2025, with an anticipated Compound Annual Growth Rate (CAGR) of xx% during the forecast period of 2025–2033. This robust expansion is fueled by escalating demand from key end-use industries, most notably automotive & transportation, which is undergoing a significant transformation towards lightweighting and electrification. The increasing adoption of electric vehicles (EVs) necessitates advanced sealing, cushioning, and interior components, areas where TPEs excel due to their inherent flexibility, durability, and processing ease. Furthermore, the building & construction sector is experiencing a surge in demand for TPEs in applications such as window seals, roofing membranes, and flooring, driven by a growing emphasis on energy efficiency and sustainable building practices.

Technological shifts are playing a pivotal role in shaping the market. Innovations in TPE formulation are leading to the development of materials with enhanced performance characteristics, including superior chemical resistance, higher temperature tolerance, and improved UV stability. The growing interest in bio-based and recycled TPEs is another significant trend, aligning with global sustainability initiatives and catering to the increasing consumer preference for eco-friendly products. This opens up new market opportunities for manufacturers who can invest in research and development of sustainable TPE solutions.

Consumer preferences are also evolving, with a greater demand for comfort, aesthetics, and safety in everyday products. This translates to increased TPE usage in footwear, consumer electronics, and household appliances, where soft-touch features, ergonomic designs, and durable components are highly valued. The medical industry continues to be a significant growth avenue, with TPEs finding applications in medical devices, tubing, and implants due to their biocompatibility and sterilization capabilities.

Competitive dynamics are intensifying, with both established global players and emerging regional manufacturers innovating to capture market share. Strategic partnerships, product differentiation, and cost competitiveness will be crucial for success. The expansion of local manufacturing capabilities and the growing maturity of the South American industrial base present significant opportunities for both domestic and international TPE suppliers. The market penetration rate of TPEs in certain applications, such as automotive interiors, is expected to rise from approximately xx% in 2024 to xx% by 2033, indicating a strong growth trajectory.

Dominant Markets & Segments in South America TPE Industry

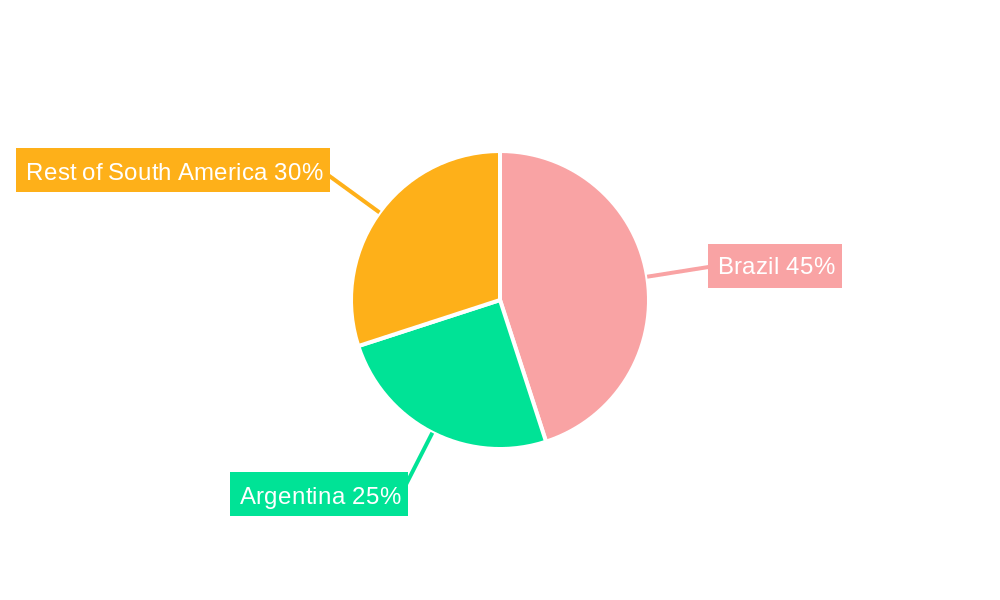

The South American TPE industry is characterized by significant dominance in specific geographies and product segments, driven by underlying industrial strengths and market demands. Brazil stands out as the largest and most dominant market within the region, accounting for an estimated xx% of the total South American TPE consumption in 2025. This dominance is attributed to its robust automotive manufacturing sector, extensive infrastructure development projects, and a large consumer base driving demand in sectors like footwear and household appliances. Argentina, while smaller, represents a significant secondary market, with its own established manufacturing base in automotive and a growing interest in construction materials. The "Rest of South America" segment, encompassing countries like Colombia, Chile, and Peru, shows promising growth potential, fueled by expanding industrial activities and increasing urbanization.

In terms of Product Type, Styrenic Block Copolymer (TPE-S) is currently the most dominant segment, projected to hold xx% of the market share in 2025. Its versatility, cost-effectiveness, and wide range of applications in adhesives, sealants, footwear, and consumer goods contribute to its leading position. However, Thermoplastic Polyurethane (TPU) is exhibiting the highest growth rate, driven by its exceptional abrasion resistance, flexibility, and strength, making it indispensable in the automotive, footwear, and medical industries. The Thermoplastic Olefin (TPE-O) segment is also experiencing steady growth, particularly in automotive components and construction due to its good weatherability and impact resistance.

The Automotive & Transportation application segment is the primary growth engine for TPEs in South America, expected to consume xx% of the total TPE volume in 2025. This is due to the increasing adoption of lightweight materials for fuel efficiency and performance, as well as the rising production of vehicles, including a growing number of electric vehicles that utilize advanced TPE solutions for seals, interior components, and wire insulation. The Building & Construction segment follows closely, propelled by infrastructure development initiatives and a growing demand for durable, weather-resistant sealing solutions, insulation, and flooring materials. The Footwear industry remains a significant consumer, driven by consumer demand for comfort, performance, and fashion.

- Key Growth Drivers in Dominant Markets:

- Brazil's Automotive Hub: Strong presence of global automotive manufacturers and increasing local production of vehicles, including EVs.

- Infrastructure Investment: Government initiatives and private sector investments in infrastructure projects across the region, boosting demand for construction materials.

- Consumer Spending: Growing middle class and increased disposable income driving demand for consumer goods, footwear, and appliances.

- Sustainability Initiatives: Growing awareness and adoption of eco-friendly materials in construction and consumer products, favoring TPEs with sustainable attributes.

South America TPE Industry Product Analysis

The South America TPE industry is witnessing significant product innovation centered on enhancing performance, sustainability, and cost-effectiveness. Key developments include the creation of TPEs with superior UV resistance and thermal stability for demanding outdoor applications in building and construction. In the automotive sector, advanced TPE formulations are enabling lightweighting initiatives through improved impact strength and flexibility for interior and exterior components. The medical segment is benefiting from the development of biocompatible and sterilizable TPEs for critical medical devices. Competitive advantages are being gained through material customization, enabling tailored solutions for specific end-user requirements and niche applications.

Key Drivers, Barriers & Challenges in South America TPE Industry

Key Drivers: Technological advancements in polymerization processes and material compounding are driving innovation, leading to TPEs with enhanced properties like higher temperature resistance and improved chemical inertness. Economic growth in key South American economies, coupled with increasing industrialization and infrastructure development, is creating substantial demand. Supportive government policies promoting domestic manufacturing and sustainable material adoption are also acting as significant growth catalysts. For example, initiatives like Brazil's "Rota 2030" program encourage the use of advanced materials in the automotive sector.

Challenges & Restraints: Volatility in raw material prices, particularly for petrochemical derivatives, poses a significant challenge to cost competitiveness. Supply chain disruptions, exacerbated by logistical complexities and geopolitical factors, can impact production and delivery timelines. Regulatory hurdles, especially concerning environmental compliance and product safety standards, require continuous adaptation and investment from manufacturers. Competitive pressures from established global players and the availability of alternative materials also present considerable restraints. The estimated impact of raw material price fluctuations can lead to +/- xx% variations in production costs annually.

Growth Drivers in the South America TPE Industry Market

The growth of the South America TPE industry is primarily propelled by technological advancements in material science, leading to the development of higher-performing and more sustainable TPE grades. Economic recovery and expansion across key South American nations, coupled with ongoing infrastructure projects, are creating robust demand across automotive, construction, and consumer goods sectors. Furthermore, a growing emphasis on lightweighting in the automotive industry to improve fuel efficiency and comply with emission standards is a significant driver. Government incentives and regulations promoting the use of advanced and environmentally friendly materials are also fostering market expansion. For instance, increased investment in renewable energy infrastructure is creating demand for durable TPE components in solar panel installations and wind turbines.

Challenges Impacting South America TPE Industry Growth

The South America TPE industry faces several challenges that can impede its growth trajectory. Significant regulatory complexities, particularly regarding environmental standards and import/export policies across different South American countries, create operational hurdles and increase compliance costs. Supply chain vulnerabilities, including dependence on imported raw materials and logistical inefficiencies, can lead to price volatility and delivery delays, impacting production schedules and customer satisfaction. Intense competitive pressures from both global TPE giants and local manufacturers, coupled with the threat of substitution from alternative materials, necessitate continuous innovation and cost optimization. The estimated impact of supply chain disruptions can lead to delays of up to xx% in product delivery during peak periods.

Key Players Shaping the South America TPE Industry Market

- Mitsui Chemicals Inc

- KURARAY CO LTD

- Mitsubishi Chemical Corporation

- SABIC

- Evonik Industries AG

- BASF SE

- Arkema Group

- Huntsman International LLC

- LG Chem

- DuPont

- KRATON CORPORATION

Significant South America TPE Industry Industry Milestones

- 2019 Q1: Launch of new bio-based TPE grades by major players, responding to increasing sustainability demands.

- 2020 Q2: Significant increase in TPE demand for medical applications due to the global pandemic, highlighting its biocompatibility.

- 2021 Q3: Expansion of TPE manufacturing facilities in Brazil by a leading global player to cater to the growing automotive sector.

- 2022 Q4: Introduction of advanced TPV formulations with enhanced chemical resistance for automotive under-the-hood applications.

- 2023 Q1: Growing trend of strategic partnerships between TPE producers and automotive OEMs to co-develop specialized materials.

- 2023 Q3: Increased focus on recycled TPEs and circular economy initiatives within the industry.

Future Outlook for South America TPE Industry Market

The future outlook for the South America TPE industry is highly optimistic, driven by sustained demand from burgeoning sectors like electric vehicles, renewable energy, and advanced healthcare. Strategic opportunities lie in the development of high-performance, sustainable TPE solutions that address evolving regulatory landscapes and consumer preferences for eco-friendly products. The continued growth of the automotive industry in Brazil and the increasing industrialization across the "Rest of South America" will fuel demand for specialized TPEs. Investment in local R&D and production capabilities will be crucial for companies to capitalize on the region's immense market potential and solidify their competitive positions.

South America TPE Industry Segmentation

-

1. Product Type

- 1.1. Styrenic Block Copolymer (TPE-S)

- 1.2. Thermoplastic Olefin (TPE-O)

- 1.3. Elastomeric Alloy (TPE-V or TPV)

- 1.4. Thermoplastic Polyurethane (TPU)

- 1.5. Thermoplastic Copolyester

- 1.6. Thermoplastic Polyamide

-

2. Application

- 2.1. Automotive & Transportation

- 2.2. Building & Construction

- 2.3. Footwear

- 2.4. Electricals & Electronics

- 2.5. Medical

- 2.6. Household Appliances

- 2.7. HVAC

- 2.8. Adhesive, Sealant & Coating

- 2.9. Other Applications

-

3. Geography

- 3.1. Brazil

- 3.2. Argentina

- 3.3. Rest of South America

South America TPE Industry Segmentation By Geography

- 1. Brazil

- 2. Argentina

- 3. Rest of South America

South America TPE Industry Regional Market Share

Geographic Coverage of South America TPE Industry

South America TPE Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Styrenic Block Copolymer (TPE-S)

- 5.1.2. Thermoplastic Olefin (TPE-O)

- 5.1.3. Elastomeric Alloy (TPE-V or TPV)

- 5.1.4. Thermoplastic Polyurethane (TPU)

- 5.1.5. Thermoplastic Copolyester

- 5.1.6. Thermoplastic Polyamide

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Automotive & Transportation

- 5.2.2. Building & Construction

- 5.2.3. Footwear

- 5.2.4. Electricals & Electronics

- 5.2.5. Medical

- 5.2.6. Household Appliances

- 5.2.7. HVAC

- 5.2.8. Adhesive, Sealant & Coating

- 5.2.9. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. Brazil

- 5.3.2. Argentina

- 5.3.3. Rest of South America

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Brazil

- 5.4.2. Argentina

- 5.4.3. Rest of South America

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. South America TPE Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Styrenic Block Copolymer (TPE-S)

- 6.1.2. Thermoplastic Olefin (TPE-O)

- 6.1.3. Elastomeric Alloy (TPE-V or TPV)

- 6.1.4. Thermoplastic Polyurethane (TPU)

- 6.1.5. Thermoplastic Copolyester

- 6.1.6. Thermoplastic Polyamide

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Automotive & Transportation

- 6.2.2. Building & Construction

- 6.2.3. Footwear

- 6.2.4. Electricals & Electronics

- 6.2.5. Medical

- 6.2.6. Household Appliances

- 6.2.7. HVAC

- 6.2.8. Adhesive, Sealant & Coating

- 6.2.9. Other Applications

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. Brazil

- 6.3.2. Argentina

- 6.3.3. Rest of South America

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Brazil South America TPE Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Styrenic Block Copolymer (TPE-S)

- 7.1.2. Thermoplastic Olefin (TPE-O)

- 7.1.3. Elastomeric Alloy (TPE-V or TPV)

- 7.1.4. Thermoplastic Polyurethane (TPU)

- 7.1.5. Thermoplastic Copolyester

- 7.1.6. Thermoplastic Polyamide

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Automotive & Transportation

- 7.2.2. Building & Construction

- 7.2.3. Footwear

- 7.2.4. Electricals & Electronics

- 7.2.5. Medical

- 7.2.6. Household Appliances

- 7.2.7. HVAC

- 7.2.8. Adhesive, Sealant & Coating

- 7.2.9. Other Applications

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. Brazil

- 7.3.2. Argentina

- 7.3.3. Rest of South America

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Argentina South America TPE Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Styrenic Block Copolymer (TPE-S)

- 8.1.2. Thermoplastic Olefin (TPE-O)

- 8.1.3. Elastomeric Alloy (TPE-V or TPV)

- 8.1.4. Thermoplastic Polyurethane (TPU)

- 8.1.5. Thermoplastic Copolyester

- 8.1.6. Thermoplastic Polyamide

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Automotive & Transportation

- 8.2.2. Building & Construction

- 8.2.3. Footwear

- 8.2.4. Electricals & Electronics

- 8.2.5. Medical

- 8.2.6. Household Appliances

- 8.2.7. HVAC

- 8.2.8. Adhesive, Sealant & Coating

- 8.2.9. Other Applications

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. Brazil

- 8.3.2. Argentina

- 8.3.3. Rest of South America

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Rest of South America South America TPE Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Styrenic Block Copolymer (TPE-S)

- 9.1.2. Thermoplastic Olefin (TPE-O)

- 9.1.3. Elastomeric Alloy (TPE-V or TPV)

- 9.1.4. Thermoplastic Polyurethane (TPU)

- 9.1.5. Thermoplastic Copolyester

- 9.1.6. Thermoplastic Polyamide

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Automotive & Transportation

- 9.2.2. Building & Construction

- 9.2.3. Footwear

- 9.2.4. Electricals & Electronics

- 9.2.5. Medical

- 9.2.6. Household Appliances

- 9.2.7. HVAC

- 9.2.8. Adhesive, Sealant & Coating

- 9.2.9. Other Applications

- 9.3. Market Analysis, Insights and Forecast - by Geography

- 9.3.1. Brazil

- 9.3.2. Argentina

- 9.3.3. Rest of South America

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Competitive Analysis

- 10.1. Company Profiles

- 10.1.1 Mitsui Chemicals Inc

- 10.1.1.1. Company Overview

- 10.1.1.2. Products

- 10.1.1.3. Company Financials

- 10.1.1.4. SWOT Analysis

- 10.1.2 KURARAY CO LTD

- 10.1.2.1. Company Overview

- 10.1.2.2. Products

- 10.1.2.3. Company Financials

- 10.1.2.4. SWOT Analysis

- 10.1.3 Mitsubishi Chemical Corporation

- 10.1.3.1. Company Overview

- 10.1.3.2. Products

- 10.1.3.3. Company Financials

- 10.1.3.4. SWOT Analysis

- 10.1.4 SABIC

- 10.1.4.1. Company Overview

- 10.1.4.2. Products

- 10.1.4.3. Company Financials

- 10.1.4.4. SWOT Analysis

- 10.1.5 Evonik Industries AG

- 10.1.5.1. Company Overview

- 10.1.5.2. Products

- 10.1.5.3. Company Financials

- 10.1.5.4. SWOT Analysis

- 10.1.6 BASF SE

- 10.1.6.1. Company Overview

- 10.1.6.2. Products

- 10.1.6.3. Company Financials

- 10.1.6.4. SWOT Analysis

- 10.1.7 Arkema Group

- 10.1.7.1. Company Overview

- 10.1.7.2. Products

- 10.1.7.3. Company Financials

- 10.1.7.4. SWOT Analysis

- 10.1.8 Huntsman International LLC

- 10.1.8.1. Company Overview

- 10.1.8.2. Products

- 10.1.8.3. Company Financials

- 10.1.8.4. SWOT Analysis

- 10.1.9 LG Chem

- 10.1.9.1. Company Overview

- 10.1.9.2. Products

- 10.1.9.3. Company Financials

- 10.1.9.4. SWOT Analysis

- 10.1.10 DuPont

- 10.1.10.1. Company Overview

- 10.1.10.2. Products

- 10.1.10.3. Company Financials

- 10.1.10.4. SWOT Analysis

- 10.1.11 KRATON CORPORATION

- 10.1.11.1. Company Overview

- 10.1.11.2. Products

- 10.1.11.3. Company Financials

- 10.1.11.4. SWOT Analysis

- 10.1.1 Mitsui Chemicals Inc

- 10.2. Market Entropy

- 10.2.1 Company's Key Areas Served

- 10.2.2 Recent Developments

- 10.3. Company Market Share Analysis 2025

- 10.3.1 Top 5 Companies Market Share Analysis

- 10.3.2 Top 3 Companies Market Share Analysis

- 10.4. List of Potential Customers

- 11. Research Methodology

List of Figures

- Figure 1: South America TPE Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: South America TPE Industry Share (%) by Company 2025

List of Tables

- Table 1: South America TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 2: South America TPE Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 3: South America TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: South America TPE Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 5: South America TPE Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 6: South America TPE Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 7: South America TPE Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 8: South America TPE Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 9: South America TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 10: South America TPE Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 11: South America TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 12: South America TPE Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 13: South America TPE Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 14: South America TPE Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 15: South America TPE Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 16: South America TPE Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 17: South America TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 18: South America TPE Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 19: South America TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 20: South America TPE Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 21: South America TPE Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 22: South America TPE Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 23: South America TPE Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: South America TPE Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 25: South America TPE Industry Revenue billion Forecast, by Product Type 2020 & 2033

- Table 26: South America TPE Industry Volume K Tons Forecast, by Product Type 2020 & 2033

- Table 27: South America TPE Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: South America TPE Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 29: South America TPE Industry Revenue billion Forecast, by Geography 2020 & 2033

- Table 30: South America TPE Industry Volume K Tons Forecast, by Geography 2020 & 2033

- Table 31: South America TPE Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 32: South America TPE Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the South America TPE Industry?

The projected CAGR is approximately 4.8%.

2. Which companies are prominent players in the South America TPE Industry?

Key companies in the market include Mitsui Chemicals Inc, KURARAY CO LTD, Mitsubishi Chemical Corporation, SABIC, Evonik Industries AG, BASF SE, Arkema Group, Huntsman International LLC, LG Chem, DuPont, KRATON CORPORATION.

3. What are the main segments of the South America TPE Industry?

The market segments include Product Type, Application, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 30.83 billion as of 2022.

5. What are some drivers contributing to market growth?

; Rising Demand from Building and Construction Industry; Growing Demand from Medical Sector.

6. What are the notable trends driving market growth?

Increasing Usage in the Automotive and Transportation Applications.

7. Are there any restraints impacting market growth?

; Government Regulations on the Commercial Use of TPE.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "South America TPE Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the South America TPE Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the South America TPE Industry?

To stay informed about further developments, trends, and reports in the South America TPE Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence