Key Insights

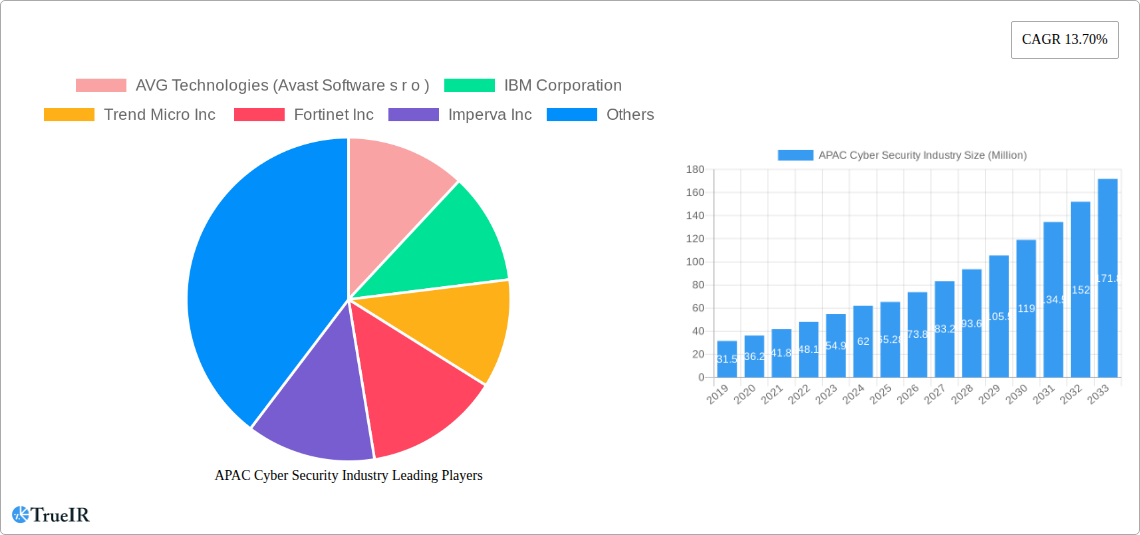

The APAC cybersecurity market is experiencing robust expansion, projected to reach a significant market size of USD 65.28 billion by 2025, with an impressive Compound Annual Growth Rate (CAGR) of 13.70% expected through 2033. This rapid growth is fueled by a confluence of factors, including escalating cyber threats, increased digitalization across industries, and a growing awareness of data protection. The surge in sophisticated cyberattacks targeting sensitive information and critical infrastructure is compelling organizations to invest heavily in advanced security solutions. Furthermore, the widespread adoption of cloud technologies and the Internet of Things (IoT) in the APAC region creates a larger attack surface, necessitating comprehensive cybersecurity strategies. Government initiatives promoting digital transformation and stricter data privacy regulations are also acting as significant catalysts for market growth.

The market is segmented across various product types, with solutions like Identity and Access Management (IAM), Threat Detection and Response, Security and Vulnerability Management, and Next-Generation Firewalls witnessing particularly strong demand. Services, including managed security services and consulting, are also crucial as organizations seek specialized expertise to navigate the complex threat landscape. Deployment models are shifting, with both cloud-based and on-premises solutions seeing adoption, though cloud-native security is gaining traction due to its scalability and flexibility. The end-user industry landscape is diverse, with significant investments coming from sectors like IT and Telecommunication, Banking, Financial Services, and Insurance (BFSI), and Healthcare, all grappling with unique cybersecurity challenges. Emerging economies within APAC, such as India and ASEAN nations, are expected to be key growth engines due to their rapidly expanding digital economies and increasing cybercrime incidents.

Here is a dynamic, SEO-optimized report description for the APAC Cyber Security Industry, designed for immediate use and maximum impact.

APAC Cyber Security Industry Market Structure & Competitive Landscape

The APAC Cyber Security industry is characterized by a highly dynamic and evolving market structure, driven by a constant influx of innovation and an increasingly sophisticated threat landscape. Market concentration varies across sub-segments, with a notable presence of both large, established global players and agile regional specialists. Innovation is a critical differentiator, with cybersecurity solutions and managed security services rapidly advancing to counter emerging threats. Regulatory impacts are significant, with governments across the APAC region implementing stricter data protection laws and cybersecurity mandates, thereby shaping market entry and operational strategies. Product substitutes exist, but the increasing complexity of threats often necessitates integrated solutions rather than standalone replacements.

End-user segmentation reveals a diverse adoption landscape, with the IT and Telecommunication sector and Banking, Financial Services, and Insurance (BFSI) sector leading in cybersecurity investments due to their critical infrastructure and sensitive data. However, sectors like Healthcare and Manufacturing are experiencing accelerated growth in cybersecurity spending driven by digital transformation initiatives and increasing cyber-attack volumes. Mergers and acquisitions (M&A) trends are a key indicator of market consolidation and strategic expansion, with companies seeking to acquire specialized technologies or expand their geographical reach. For instance, in the historical period of 2019-2024, over 50 significant M&A deals were observed, with an estimated aggregate value exceeding $10 Billion, reflecting a robust appetite for strategic consolidation. Concentration ratios in key solution segments, such as Identity and Access Management, indicate moderate to high concentration, with the top 5 players holding approximately 65% of the market share in 2024.

APAC Cyber Security Industry Market Trends & Opportunities

The APAC Cyber Security industry is poised for substantial growth, with the market size projected to expand significantly from an estimated $55 Billion in 2025 to over $120 Billion by 2033, exhibiting a Compound Annual Growth Rate (CAGR) of approximately 10.5% during the forecast period of 2025-2033. This expansion is fueled by a confluence of technological advancements, evolving consumer preferences for enhanced data protection, and intensifying competitive dynamics.

Technological shifts are at the forefront of this evolution. The increasing adoption of cloud computing and the burgeoning Internet of Things (IoT) ecosystem present new attack vectors, necessitating advanced cybersecurity solutions like cloud security posture management, IoT security platforms, and advanced threat detection and response (XDR) systems. Artificial Intelligence (AI) and Machine Learning (ML) are increasingly integrated into cybersecurity offerings, enabling predictive threat analytics, automated incident response, and sophisticated anomaly detection. This trend is significantly impacting the demand for Security Information and Event Management (SIEM) solutions, which are becoming more intelligent and automated.

Consumer preferences are rapidly shifting towards proactive security measures and managed services. Organizations are moving away from purely reactive defense strategies to embrace comprehensive security frameworks that offer continuous monitoring, threat intelligence sharing, and rapid incident remediation. This preference for managed security services (MSSPs) is creating significant opportunities for providers offering specialized expertise and 24/7 support, particularly in regions with nascent cybersecurity talent pools. The demand for integrated cybersecurity portfolios that address network, cloud, and endpoint threats simultaneously is also on the rise.

Competitive dynamics are intensifying, with a clear trend towards partnerships and collaborations to enhance capabilities. Companies are actively seeking to expand their product portfolios and geographical presence through strategic alliances and acquisitions. The emergence of new market entrants with innovative technologies and the relentless pace of innovation from established players are creating a highly competitive environment. The focus is increasingly on providing end-to-end security solutions that address the entire attack chain, from prevention and detection to response and recovery.

Market penetration rates for advanced cybersecurity solutions are steadily increasing across all end-user industries, driven by regulatory compliance, growing awareness of cyber risks, and the high cost of data breaches. For instance, the penetration of advanced threat detection solutions in the BFSI sector is expected to reach over 80% by 2027, up from approximately 60% in 2024. The projected market size for Identity and Access Management (IAM) alone is estimated to reach $15 Billion by 2033, highlighting its critical role in securing digital identities. The ongoing digital transformation initiatives across various APAC economies further underscore the vast untapped potential and emerging opportunities within this vital industry.

Dominant Markets & Segments in APAC Cyber Security Industry

The APAC Cyber Security Industry exhibits distinct patterns of dominance across its diverse markets and segments. Geographically, East Asia, encompassing countries like China, Japan, and South Korea, is currently the leading region, driven by robust economic growth, advanced technological infrastructure, and significant government investment in cybersecurity. However, Southeast Asia is emerging as a rapidly growing market, propelled by increasing digitalization, a rising middle class, and a growing awareness of cyber threats among businesses and consumers. India, in particular, is witnessing exponential growth, with its large IT workforce and increasing adoption of advanced technologies contributing to a surging demand for cybersecurity solutions and services.

Within the Product Type segmentation, Solutions represent the largest segment, projected to capture over 75% of the market revenue by 2033. Within solutions, Identity and Access Management (IAM) is a particularly dominant sub-segment, driven by the critical need to secure digital identities in an era of remote work and cloud adoption. The market for Security and Vulnerability Management is also experiencing significant expansion, as organizations strive to proactively identify and remediate weaknesses in their IT infrastructure. Next Generation Firewalls (NGFW) and Intrusion Detection and Prevention Systems (IDS/IPS) remain foundational, with continuous innovation to address sophisticated network threats. Security Information and Event Management (SIEM) solutions are also showing strong growth due to the increasing volume of data requiring centralized monitoring and analysis.

Services are the second-largest segment and are witnessing a faster growth rate than solutions, indicating a strong shift towards outsourcing security functions. Managed Security Services (MSSPs) are particularly in high demand, providing organizations with round-the-clock monitoring, threat detection, and incident response capabilities. This trend is amplified in regions with a shortage of skilled cybersecurity professionals.

In terms of Deployment, On-cloud solutions are rapidly gaining traction, outpacing On-premises deployments. The flexibility, scalability, and cost-effectiveness of cloud-based security platforms are key drivers. However, certain industries, such as government and highly regulated financial institutions, continue to maintain a preference for on-premises solutions due to stringent data sovereignty and compliance requirements.

The End-user Industry landscape reveals that IT and Telecommunication remains the largest sector for cybersecurity spending, accounting for an estimated 30% of the total market in 2025. This is followed closely by Banking, Financial Services, and Insurance (BFSI), which invests heavily in protecting sensitive financial data and critical infrastructure. The Healthcare sector is a significant growth area, driven by the increasing digitization of patient records and the high value of healthcare data for cybercriminals. Aerospace and Defense also represent a high-spending segment due to national security concerns and the sensitive nature of their operations. The Manufacturing sector is increasingly adopting cybersecurity solutions to protect its operational technology (OT) and industrial control systems from cyber threats.

Key Growth Drivers within these dominant markets and segments include:

- Increasing Volume and Sophistication of Cyber Threats: Advanced persistent threats (APTs), ransomware, and nation-state attacks are compelling organizations to invest in comprehensive security measures.

- Rapid Digital Transformation: The widespread adoption of cloud computing, IoT, AI, and big data analytics creates new attack surfaces that require robust cybersecurity.

- Stringent Regulatory Landscape: Growing mandates around data privacy, data localization, and cybersecurity compliance (e.g., GDPR, CCPA equivalents in APAC) are driving investment.

- Government Initiatives and Investments: Many APAC governments are prioritizing cybersecurity as a national security and economic imperative, leading to increased public spending and supportive policies.

- Shortage of Skilled Cybersecurity Professionals: This deficit is fueling the demand for managed security services and automated security solutions.

- Growing Awareness of Cyber Risks: High-profile data breaches and their financial and reputational consequences are making businesses more proactive in their security investments.

APAC Cyber Security Industry Product Analysis

The APAC Cyber Security Industry is characterized by a continuous stream of product innovations designed to counter the ever-evolving threat landscape. Key product advancements focus on enhancing threat detection, response, and prevention capabilities. Solutions like AI-powered threat intelligence platforms, behavioral analytics engines, and advanced endpoint detection and response (EDR) systems are gaining prominence. Cloud-native security solutions offering seamless integration with public and private cloud environments are also critical. The competitive advantage for many vendors lies in their ability to offer unified security platforms that consolidate multiple functionalities, such as Identity and Access Management, Security and Vulnerability Management, and Network Security, into a single, cohesive offering. Emphasis is placed on user-friendly interfaces and automated workflows to address the cybersecurity talent shortage.

Key Drivers, Barriers & Challenges in APAC Cyber Security Industry

Key Drivers propelling the APAC Cyber Security industry forward include the escalating volume and sophistication of cyber threats, such as ransomware and APTs, forcing businesses to prioritize robust defense mechanisms. The rapid pace of digital transformation across all sectors, including cloud adoption and IoT expansion, inherently creates new vulnerabilities that demand advanced security solutions. Furthermore, increasingly stringent regulatory environments, with a growing emphasis on data privacy and protection, compel organizations to invest in compliance-driven cybersecurity measures. Government initiatives and substantial investments in cybersecurity as a national security priority also act as significant catalysts. The persistent global shortage of skilled cybersecurity professionals further fuels the demand for managed security services and automated solutions, ensuring continuous market growth.

Key Challenges and Restraints impacting the APAC Cyber Security industry include the significant shortage of skilled cybersecurity professionals, which limits the effective deployment and management of complex security solutions. The evolving and fragmented regulatory landscape across different APAC countries can create compliance complexities for global and regional players, potentially increasing operational costs and hindering market expansion. Supply chain vulnerabilities, particularly in hardware and software components, can introduce security risks and impact product availability. Intense competitive pressures from both established global vendors and agile local players necessitate continuous innovation and competitive pricing strategies, which can strain profit margins. The economic downturns and geopolitical uncertainties in certain regions can also lead to budget constraints for cybersecurity investments, particularly among small and medium-sized enterprises (SMEs).

Growth Drivers in the APAC Cyber Security Industry Market

Several key drivers are fueling the growth of the APAC Cyber Security Industry. Technologically, the pervasive adoption of cloud computing, the proliferation of IoT devices, and the increasing use of Artificial Intelligence (AI) are expanding the attack surface, thereby necessitating more sophisticated cybersecurity measures. Economically, the digital transformation initiatives across businesses in sectors like BFSI, healthcare, and manufacturing are driving substantial investments in protecting critical data and infrastructure. Regionally, the growing awareness of cyber threats, coupled with significant government investments and supportive policies aimed at enhancing national cybersecurity capabilities, are creating a favorable market environment. The increasing frequency and severity of cyber-attacks, including ransomware and data breaches, are compelling organizations to adopt proactive and comprehensive security strategies.

Challenges Impacting APAC Cyber Security Industry Growth

The growth of the APAC Cyber Security Industry faces several significant challenges. Regulatory complexities stemming from diverse data privacy laws and cybersecurity mandates across different APAC nations create compliance hurdles and increase operational overhead. Supply chain issues, including vulnerabilities in software and hardware components, can introduce security risks and disrupt the availability of critical security products, impacting timely deployment. Competitive pressures are intense, with a crowded market requiring continuous innovation and aggressive pricing strategies, which can be challenging for smaller players. Furthermore, the persistent global shortage of skilled cybersecurity professionals limits the ability of organizations to effectively implement and manage advanced security solutions, thereby hindering optimal utilization and market expansion.

Key Players Shaping the APAC Cyber Security Industry Market

- AVG Technologies (Avast Software s r o )

- IBM Corporation

- Trend Micro Inc

- Fortinet Inc

- Imperva Inc

- Check Point Software Technologies Ltd

- Cisco Systems Inc

- Broadcom Inc

- Proofpoint Inc

- Rapid7 Inc

- Cyber Ark Software Ltd

- Intel Security (Intel Corporation)

- Dell Technologies Inc

- Fireeye Inc

- Palo Alto Networks Inc

Significant APAC Cyber Security Industry Industry Milestones

- December 2022: VI Business introduced VI Secure, a comprehensive cybersecurity offering for enterprises in India, providing a robust portfolio to protect against network, cloud, and endpoint threats. This launch also included plans for email, web, and virtualized firewall protection utilizing Cisco's FirstWave CyberCision platform.

- July 2022: A strategic partnership was formed between Cyware and CyberQ Group, aiming to bolster cybersecurity capabilities across the Asia-Pacific region. This collaboration focuses on delivering advanced managed security services that enable customers to consolidate, analyze, and autonomously share threat intelligence, while enhancing threat response collaboration through Cyware's Cyber Fusion and Collective Defense technologies for MSSPs.

Future Outlook for APAC Cyber Security Industry Market

The future outlook for the APAC Cyber Security Industry is exceptionally bright, driven by a sustained increase in cyber threats and accelerated digital adoption. Key growth catalysts include the continued evolution of AI and machine learning in cybersecurity, leading to more proactive and predictive defense mechanisms. The expansion of cloud security services and the demand for Zero Trust architectures will further shape the market. Strategic opportunities lie in addressing the cybersecurity needs of emerging economies within APAC, focusing on SMBs and critical infrastructure protection. Market potential will be unlocked through partnerships, mergers, and acquisitions aimed at expanding technological capabilities and geographical reach, ensuring comprehensive security solutions for a diverse and dynamic regional market.

APAC Cyber Security Industry Segmentation

-

1. Product Type

-

1.1. Solutions

- 1.1.1. Identity and Access Management

- 1.1.2. Threat D

- 1.1.3. Security and Vulnerability Management

- 1.1.4. DDoS Mitigation

- 1.1.5. Next Generation Firewall

- 1.1.6. IDS/IPS

- 1.1.7. Security Information and Event Management

- 1.1.8. Other Solutions

- 1.2. Services

-

1.1. Solutions

-

2. Deployment

- 2.1. On-cloud

- 2.2. On-premises

-

3. End-user Industry

- 3.1. Aerospace and Defense

- 3.2. Banking, Financial Services, and Insurance

- 3.3. Healthcare

- 3.4. Manufacturing

- 3.5. Retail

- 3.6. IT and Telecommunication

- 3.7. Other End-user Industries

APAC Cyber Security Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

APAC Cyber Security Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 13.70% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rapidly Increasing Cybersecurity Incidents and Regulations Requiring Their Reporting; Growing M2M/IoT Connections Demanding Strengthened Cybersecurity in Enterprises

- 3.3. Market Restrains

- 3.3.1. Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness

- 3.4. Market Trends

- 3.4.1. Cloud Deployment Drives Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Solutions

- 5.1.1.1. Identity and Access Management

- 5.1.1.2. Threat D

- 5.1.1.3. Security and Vulnerability Management

- 5.1.1.4. DDoS Mitigation

- 5.1.1.5. Next Generation Firewall

- 5.1.1.6. IDS/IPS

- 5.1.1.7. Security Information and Event Management

- 5.1.1.8. Other Solutions

- 5.1.2. Services

- 5.1.1. Solutions

- 5.2. Market Analysis, Insights and Forecast - by Deployment

- 5.2.1. On-cloud

- 5.2.2. On-premises

- 5.3. Market Analysis, Insights and Forecast - by End-user Industry

- 5.3.1. Aerospace and Defense

- 5.3.2. Banking, Financial Services, and Insurance

- 5.3.3. Healthcare

- 5.3.4. Manufacturing

- 5.3.5. Retail

- 5.3.6. IT and Telecommunication

- 5.3.7. Other End-user Industries

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. South America

- 5.4.3. Europe

- 5.4.4. Middle East & Africa

- 5.4.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. North America APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Solutions

- 6.1.1.1. Identity and Access Management

- 6.1.1.2. Threat D

- 6.1.1.3. Security and Vulnerability Management

- 6.1.1.4. DDoS Mitigation

- 6.1.1.5. Next Generation Firewall

- 6.1.1.6. IDS/IPS

- 6.1.1.7. Security Information and Event Management

- 6.1.1.8. Other Solutions

- 6.1.2. Services

- 6.1.1. Solutions

- 6.2. Market Analysis, Insights and Forecast - by Deployment

- 6.2.1. On-cloud

- 6.2.2. On-premises

- 6.3. Market Analysis, Insights and Forecast - by End-user Industry

- 6.3.1. Aerospace and Defense

- 6.3.2. Banking, Financial Services, and Insurance

- 6.3.3. Healthcare

- 6.3.4. Manufacturing

- 6.3.5. Retail

- 6.3.6. IT and Telecommunication

- 6.3.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. South America APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Solutions

- 7.1.1.1. Identity and Access Management

- 7.1.1.2. Threat D

- 7.1.1.3. Security and Vulnerability Management

- 7.1.1.4. DDoS Mitigation

- 7.1.1.5. Next Generation Firewall

- 7.1.1.6. IDS/IPS

- 7.1.1.7. Security Information and Event Management

- 7.1.1.8. Other Solutions

- 7.1.2. Services

- 7.1.1. Solutions

- 7.2. Market Analysis, Insights and Forecast - by Deployment

- 7.2.1. On-cloud

- 7.2.2. On-premises

- 7.3. Market Analysis, Insights and Forecast - by End-user Industry

- 7.3.1. Aerospace and Defense

- 7.3.2. Banking, Financial Services, and Insurance

- 7.3.3. Healthcare

- 7.3.4. Manufacturing

- 7.3.5. Retail

- 7.3.6. IT and Telecommunication

- 7.3.7. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Europe APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Solutions

- 8.1.1.1. Identity and Access Management

- 8.1.1.2. Threat D

- 8.1.1.3. Security and Vulnerability Management

- 8.1.1.4. DDoS Mitigation

- 8.1.1.5. Next Generation Firewall

- 8.1.1.6. IDS/IPS

- 8.1.1.7. Security Information and Event Management

- 8.1.1.8. Other Solutions

- 8.1.2. Services

- 8.1.1. Solutions

- 8.2. Market Analysis, Insights and Forecast - by Deployment

- 8.2.1. On-cloud

- 8.2.2. On-premises

- 8.3. Market Analysis, Insights and Forecast - by End-user Industry

- 8.3.1. Aerospace and Defense

- 8.3.2. Banking, Financial Services, and Insurance

- 8.3.3. Healthcare

- 8.3.4. Manufacturing

- 8.3.5. Retail

- 8.3.6. IT and Telecommunication

- 8.3.7. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Middle East & Africa APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Solutions

- 9.1.1.1. Identity and Access Management

- 9.1.1.2. Threat D

- 9.1.1.3. Security and Vulnerability Management

- 9.1.1.4. DDoS Mitigation

- 9.1.1.5. Next Generation Firewall

- 9.1.1.6. IDS/IPS

- 9.1.1.7. Security Information and Event Management

- 9.1.1.8. Other Solutions

- 9.1.2. Services

- 9.1.1. Solutions

- 9.2. Market Analysis, Insights and Forecast - by Deployment

- 9.2.1. On-cloud

- 9.2.2. On-premises

- 9.3. Market Analysis, Insights and Forecast - by End-user Industry

- 9.3.1. Aerospace and Defense

- 9.3.2. Banking, Financial Services, and Insurance

- 9.3.3. Healthcare

- 9.3.4. Manufacturing

- 9.3.5. Retail

- 9.3.6. IT and Telecommunication

- 9.3.7. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. Asia Pacific APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 10.1.1. Solutions

- 10.1.1.1. Identity and Access Management

- 10.1.1.2. Threat D

- 10.1.1.3. Security and Vulnerability Management

- 10.1.1.4. DDoS Mitigation

- 10.1.1.5. Next Generation Firewall

- 10.1.1.6. IDS/IPS

- 10.1.1.7. Security Information and Event Management

- 10.1.1.8. Other Solutions

- 10.1.2. Services

- 10.1.1. Solutions

- 10.2. Market Analysis, Insights and Forecast - by Deployment

- 10.2.1. On-cloud

- 10.2.2. On-premises

- 10.3. Market Analysis, Insights and Forecast - by End-user Industry

- 10.3.1. Aerospace and Defense

- 10.3.2. Banking, Financial Services, and Insurance

- 10.3.3. Healthcare

- 10.3.4. Manufacturing

- 10.3.5. Retail

- 10.3.6. IT and Telecommunication

- 10.3.7. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by Product Type

- 11. North America APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Europe APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Asia Pacific APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Latin America APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. Middle East and Africa APAC Cyber Security Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 AVG Technologies (Avast Software s r o )

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 IBM Corporation

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Trend Micro Inc

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Fortinet Inc

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Imperva Inc

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Check Point Software Technologies Ltd

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Cisco Systems Inc

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Broadcom Inc

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Proofpoint Inc

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Rapid7 Inc

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Cyber Ark Software Ltd

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 Intel Security (Intel Corporation)

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Dell Technologies Inc

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.14 Fireeye Inc

- 16.2.14.1. Overview

- 16.2.14.2. Products

- 16.2.14.3. SWOT Analysis

- 16.2.14.4. Recent Developments

- 16.2.14.5. Financials (Based on Availability)

- 16.2.15 Palo Alto Networks Inc

- 16.2.15.1. Overview

- 16.2.15.2. Products

- 16.2.15.3. SWOT Analysis

- 16.2.15.4. Recent Developments

- 16.2.15.5. Financials (Based on Availability)

- 16.2.1 AVG Technologies (Avast Software s r o )

List of Figures

- Figure 1: Global APAC Cyber Security Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: Global APAC Cyber Security Industry Volume Breakdown (K Unit, %) by Region 2024 & 2032

- Figure 3: North America APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 4: North America APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 5: North America APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: North America APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

- Figure 7: Europe APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 8: Europe APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 9: Europe APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Europe APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

- Figure 11: Asia Pacific APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 12: Asia Pacific APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 13: Asia Pacific APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 14: Asia Pacific APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

- Figure 15: Latin America APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 16: Latin America APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 17: Latin America APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Latin America APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

- Figure 19: Middle East and Africa APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 20: Middle East and Africa APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 21: Middle East and Africa APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 22: Middle East and Africa APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

- Figure 23: North America APAC Cyber Security Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 24: North America APAC Cyber Security Industry Volume (K Unit), by Product Type 2024 & 2032

- Figure 25: North America APAC Cyber Security Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 26: North America APAC Cyber Security Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 27: North America APAC Cyber Security Industry Revenue (Million), by Deployment 2024 & 2032

- Figure 28: North America APAC Cyber Security Industry Volume (K Unit), by Deployment 2024 & 2032

- Figure 29: North America APAC Cyber Security Industry Revenue Share (%), by Deployment 2024 & 2032

- Figure 30: North America APAC Cyber Security Industry Volume Share (%), by Deployment 2024 & 2032

- Figure 31: North America APAC Cyber Security Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 32: North America APAC Cyber Security Industry Volume (K Unit), by End-user Industry 2024 & 2032

- Figure 33: North America APAC Cyber Security Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 34: North America APAC Cyber Security Industry Volume Share (%), by End-user Industry 2024 & 2032

- Figure 35: North America APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 36: North America APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 37: North America APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 38: North America APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

- Figure 39: South America APAC Cyber Security Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 40: South America APAC Cyber Security Industry Volume (K Unit), by Product Type 2024 & 2032

- Figure 41: South America APAC Cyber Security Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 42: South America APAC Cyber Security Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 43: South America APAC Cyber Security Industry Revenue (Million), by Deployment 2024 & 2032

- Figure 44: South America APAC Cyber Security Industry Volume (K Unit), by Deployment 2024 & 2032

- Figure 45: South America APAC Cyber Security Industry Revenue Share (%), by Deployment 2024 & 2032

- Figure 46: South America APAC Cyber Security Industry Volume Share (%), by Deployment 2024 & 2032

- Figure 47: South America APAC Cyber Security Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 48: South America APAC Cyber Security Industry Volume (K Unit), by End-user Industry 2024 & 2032

- Figure 49: South America APAC Cyber Security Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 50: South America APAC Cyber Security Industry Volume Share (%), by End-user Industry 2024 & 2032

- Figure 51: South America APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 52: South America APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 53: South America APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 54: South America APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

- Figure 55: Europe APAC Cyber Security Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 56: Europe APAC Cyber Security Industry Volume (K Unit), by Product Type 2024 & 2032

- Figure 57: Europe APAC Cyber Security Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 58: Europe APAC Cyber Security Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 59: Europe APAC Cyber Security Industry Revenue (Million), by Deployment 2024 & 2032

- Figure 60: Europe APAC Cyber Security Industry Volume (K Unit), by Deployment 2024 & 2032

- Figure 61: Europe APAC Cyber Security Industry Revenue Share (%), by Deployment 2024 & 2032

- Figure 62: Europe APAC Cyber Security Industry Volume Share (%), by Deployment 2024 & 2032

- Figure 63: Europe APAC Cyber Security Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 64: Europe APAC Cyber Security Industry Volume (K Unit), by End-user Industry 2024 & 2032

- Figure 65: Europe APAC Cyber Security Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 66: Europe APAC Cyber Security Industry Volume Share (%), by End-user Industry 2024 & 2032

- Figure 67: Europe APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 68: Europe APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 69: Europe APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 70: Europe APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

- Figure 71: Middle East & Africa APAC Cyber Security Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 72: Middle East & Africa APAC Cyber Security Industry Volume (K Unit), by Product Type 2024 & 2032

- Figure 73: Middle East & Africa APAC Cyber Security Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 74: Middle East & Africa APAC Cyber Security Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 75: Middle East & Africa APAC Cyber Security Industry Revenue (Million), by Deployment 2024 & 2032

- Figure 76: Middle East & Africa APAC Cyber Security Industry Volume (K Unit), by Deployment 2024 & 2032

- Figure 77: Middle East & Africa APAC Cyber Security Industry Revenue Share (%), by Deployment 2024 & 2032

- Figure 78: Middle East & Africa APAC Cyber Security Industry Volume Share (%), by Deployment 2024 & 2032

- Figure 79: Middle East & Africa APAC Cyber Security Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 80: Middle East & Africa APAC Cyber Security Industry Volume (K Unit), by End-user Industry 2024 & 2032

- Figure 81: Middle East & Africa APAC Cyber Security Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 82: Middle East & Africa APAC Cyber Security Industry Volume Share (%), by End-user Industry 2024 & 2032

- Figure 83: Middle East & Africa APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 84: Middle East & Africa APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 85: Middle East & Africa APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 86: Middle East & Africa APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

- Figure 87: Asia Pacific APAC Cyber Security Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 88: Asia Pacific APAC Cyber Security Industry Volume (K Unit), by Product Type 2024 & 2032

- Figure 89: Asia Pacific APAC Cyber Security Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 90: Asia Pacific APAC Cyber Security Industry Volume Share (%), by Product Type 2024 & 2032

- Figure 91: Asia Pacific APAC Cyber Security Industry Revenue (Million), by Deployment 2024 & 2032

- Figure 92: Asia Pacific APAC Cyber Security Industry Volume (K Unit), by Deployment 2024 & 2032

- Figure 93: Asia Pacific APAC Cyber Security Industry Revenue Share (%), by Deployment 2024 & 2032

- Figure 94: Asia Pacific APAC Cyber Security Industry Volume Share (%), by Deployment 2024 & 2032

- Figure 95: Asia Pacific APAC Cyber Security Industry Revenue (Million), by End-user Industry 2024 & 2032

- Figure 96: Asia Pacific APAC Cyber Security Industry Volume (K Unit), by End-user Industry 2024 & 2032

- Figure 97: Asia Pacific APAC Cyber Security Industry Revenue Share (%), by End-user Industry 2024 & 2032

- Figure 98: Asia Pacific APAC Cyber Security Industry Volume Share (%), by End-user Industry 2024 & 2032

- Figure 99: Asia Pacific APAC Cyber Security Industry Revenue (Million), by Country 2024 & 2032

- Figure 100: Asia Pacific APAC Cyber Security Industry Volume (K Unit), by Country 2024 & 2032

- Figure 101: Asia Pacific APAC Cyber Security Industry Revenue Share (%), by Country 2024 & 2032

- Figure 102: Asia Pacific APAC Cyber Security Industry Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global APAC Cyber Security Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global APAC Cyber Security Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Global APAC Cyber Security Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 4: Global APAC Cyber Security Industry Volume K Unit Forecast, by Product Type 2019 & 2032

- Table 5: Global APAC Cyber Security Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 6: Global APAC Cyber Security Industry Volume K Unit Forecast, by Deployment 2019 & 2032

- Table 7: Global APAC Cyber Security Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 8: Global APAC Cyber Security Industry Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 9: Global APAC Cyber Security Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: Global APAC Cyber Security Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 11: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 13: APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 15: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 17: APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 19: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 21: APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 25: APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 27: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 29: APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 31: Global APAC Cyber Security Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 32: Global APAC Cyber Security Industry Volume K Unit Forecast, by Product Type 2019 & 2032

- Table 33: Global APAC Cyber Security Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 34: Global APAC Cyber Security Industry Volume K Unit Forecast, by Deployment 2019 & 2032

- Table 35: Global APAC Cyber Security Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 36: Global APAC Cyber Security Industry Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 37: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 38: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 39: United States APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: United States APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 41: Canada APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Canada APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 43: Mexico APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Mexico APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 45: Global APAC Cyber Security Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 46: Global APAC Cyber Security Industry Volume K Unit Forecast, by Product Type 2019 & 2032

- Table 47: Global APAC Cyber Security Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 48: Global APAC Cyber Security Industry Volume K Unit Forecast, by Deployment 2019 & 2032

- Table 49: Global APAC Cyber Security Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 50: Global APAC Cyber Security Industry Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 51: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 52: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 53: Brazil APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 54: Brazil APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 55: Argentina APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 56: Argentina APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 57: Rest of South America APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 58: Rest of South America APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 59: Global APAC Cyber Security Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 60: Global APAC Cyber Security Industry Volume K Unit Forecast, by Product Type 2019 & 2032

- Table 61: Global APAC Cyber Security Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 62: Global APAC Cyber Security Industry Volume K Unit Forecast, by Deployment 2019 & 2032

- Table 63: Global APAC Cyber Security Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 64: Global APAC Cyber Security Industry Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 65: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 66: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 67: United Kingdom APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 68: United Kingdom APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 69: Germany APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 70: Germany APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 71: France APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 72: France APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 73: Italy APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 74: Italy APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 75: Spain APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 76: Spain APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 77: Russia APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 78: Russia APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 79: Benelux APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 80: Benelux APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 81: Nordics APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 82: Nordics APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 83: Rest of Europe APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 84: Rest of Europe APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 85: Global APAC Cyber Security Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 86: Global APAC Cyber Security Industry Volume K Unit Forecast, by Product Type 2019 & 2032

- Table 87: Global APAC Cyber Security Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 88: Global APAC Cyber Security Industry Volume K Unit Forecast, by Deployment 2019 & 2032

- Table 89: Global APAC Cyber Security Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 90: Global APAC Cyber Security Industry Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 91: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 92: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 93: Turkey APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 94: Turkey APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 95: Israel APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 96: Israel APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 97: GCC APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 98: GCC APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 99: North Africa APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 100: North Africa APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 101: South Africa APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 102: South Africa APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 103: Rest of Middle East & Africa APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 104: Rest of Middle East & Africa APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 105: Global APAC Cyber Security Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 106: Global APAC Cyber Security Industry Volume K Unit Forecast, by Product Type 2019 & 2032

- Table 107: Global APAC Cyber Security Industry Revenue Million Forecast, by Deployment 2019 & 2032

- Table 108: Global APAC Cyber Security Industry Volume K Unit Forecast, by Deployment 2019 & 2032

- Table 109: Global APAC Cyber Security Industry Revenue Million Forecast, by End-user Industry 2019 & 2032

- Table 110: Global APAC Cyber Security Industry Volume K Unit Forecast, by End-user Industry 2019 & 2032

- Table 111: Global APAC Cyber Security Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 112: Global APAC Cyber Security Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 113: China APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 114: China APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 115: India APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 116: India APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 117: Japan APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 118: Japan APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 119: South Korea APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 120: South Korea APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 121: ASEAN APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 122: ASEAN APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 123: Oceania APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 124: Oceania APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 125: Rest of Asia Pacific APAC Cyber Security Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 126: Rest of Asia Pacific APAC Cyber Security Industry Volume (K Unit) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the APAC Cyber Security Industry?

The projected CAGR is approximately 13.70%.

2. Which companies are prominent players in the APAC Cyber Security Industry?

Key companies in the market include AVG Technologies (Avast Software s r o ), IBM Corporation, Trend Micro Inc , Fortinet Inc, Imperva Inc, Check Point Software Technologies Ltd, Cisco Systems Inc, Broadcom Inc, Proofpoint Inc, Rapid7 Inc, Cyber Ark Software Ltd, Intel Security (Intel Corporation), Dell Technologies Inc, Fireeye Inc, Palo Alto Networks Inc.

3. What are the main segments of the APAC Cyber Security Industry?

The market segments include Product Type, Deployment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 65.28 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapidly Increasing Cybersecurity Incidents and Regulations Requiring Their Reporting; Growing M2M/IoT Connections Demanding Strengthened Cybersecurity in Enterprises.

6. What are the notable trends driving market growth?

Cloud Deployment Drives Market Growth.

7. Are there any restraints impacting market growth?

Lack of Cybersecurity Professionals; High Reliance on Traditional Authentication Methods and Low Preparedness.

8. Can you provide examples of recent developments in the market?

December 2022: VI Business introduced VI Secure, a new cybersecurity offering for enterprises, which has been developed as a complete cybersecurity portfolio with various trustworthy solutions that protect against several threats originating from networks, clouds, and endpoints in India. Additionally, the company has planned to provide email, web, and virtualized firewall protection using Cisco's FirstWave CyberCision platform.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "APAC Cyber Security Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the APAC Cyber Security Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the APAC Cyber Security Industry?

To stay informed about further developments, trends, and reports in the APAC Cyber Security Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence