Key Insights

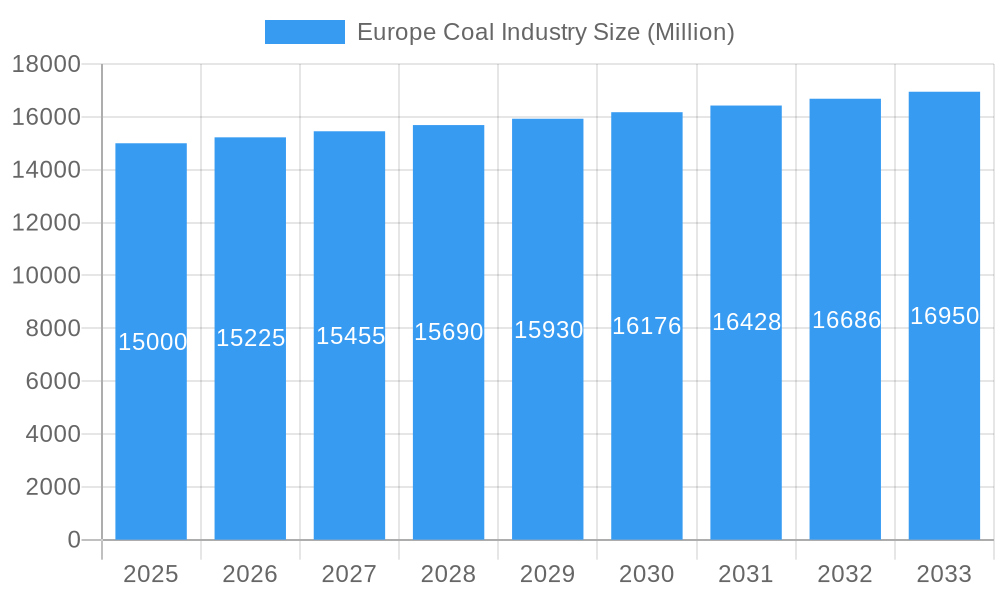

The European coal market is projected to grow at a Compound Annual Growth Rate (CAGR) of 1.9% from 2025 to 2033, reaching a market size of 42.6 billion. Despite significant decarbonization efforts and the rise of renewable energy, this growth reflects regional variations and evolving energy security needs. Bituminous coal is expected to lead market share due to its high energy density, followed by sub-bituminous and lignite. Electricity generation remains the primary application, with steel and cement industries also contributing significantly. Key players are likely to focus on efficiency, diversification, and carbon capture technologies to maintain competitiveness.

Europe Coal Industry Market Size (In Billion)

Market dynamics will be shaped by regional differences. While Germany is phasing out coal, other European nations may increase reliance on coal for energy security, particularly where renewable infrastructure is less developed. Key market restraints include strict environmental regulations, carbon taxes, and public pressure for cleaner energy. Competition from international imports and volatile energy prices further challenge the industry. Strategic investments in efficient technologies and carbon capture and storage (CCS) will be crucial for market players to navigate the evolving energy landscape.

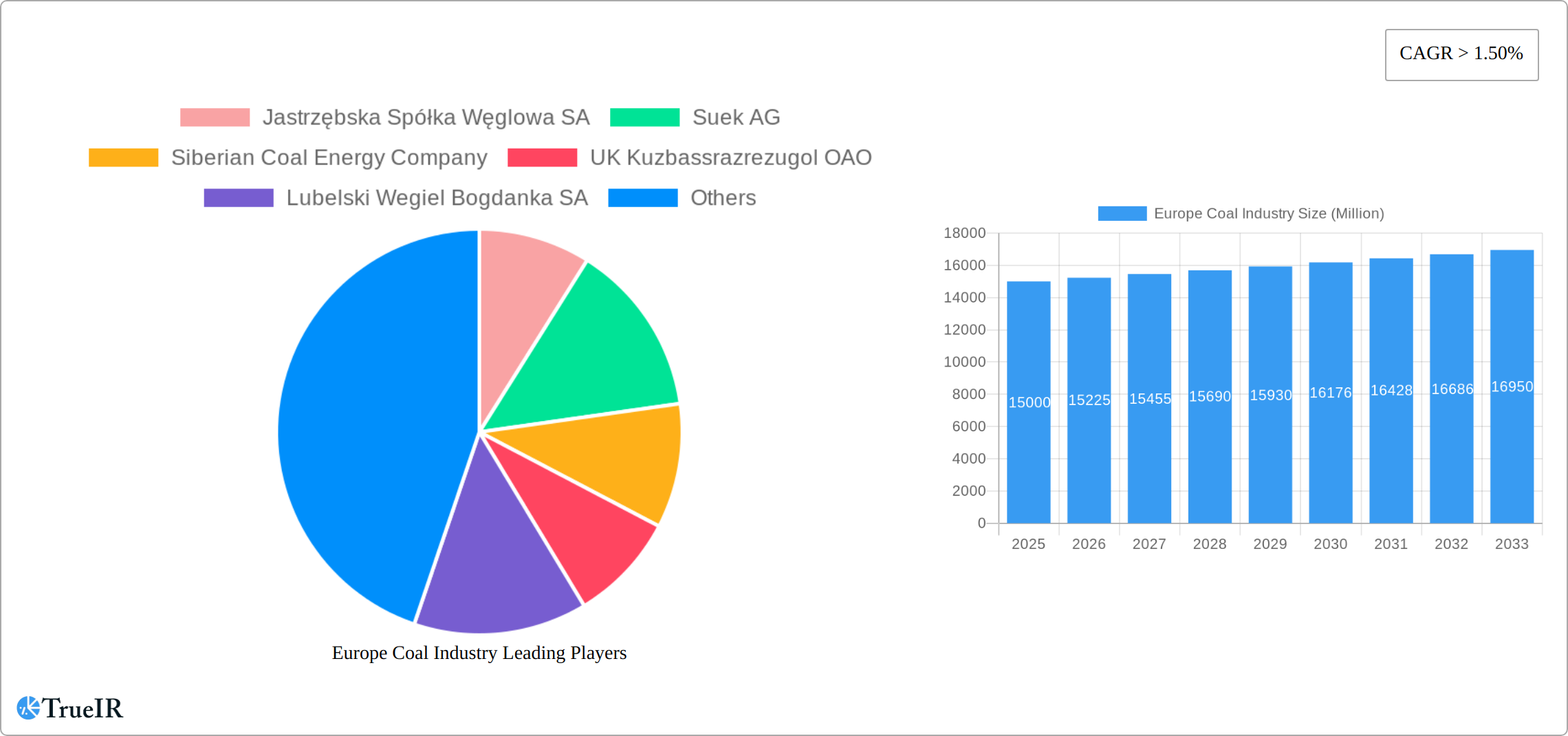

Europe Coal Industry Company Market Share

Europe Coal Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the European coal industry, covering market structure, competitive dynamics, trends, opportunities, and future outlook from 2019 to 2033. With a focus on key players like Jastrzębska Spółka Węglowa SA, Suek AG, and others, this report is an essential resource for industry professionals, investors, and policymakers. The study period spans 2019-2033, with 2025 as the base and estimated year. The forecast period is 2025-2033, and the historical period covers 2019-2024.

Europe Coal Industry Market Structure & Competitive Landscape

The European coal market presents a moderately concentrated structure, with several key players dominating production and distribution. While year-on-year fluctuations occur, a trend towards consolidation is evident, largely driven by mergers and acquisitions (M&A) activity. Between 2019 and 2024, approximately [Insert Precise Figure] million USD in M&A transactions were recorded, with projections of [Insert Precise Figure] million USD anticipated for the 2025-2033 forecast period. Innovation within the sector remains incremental, with companies prioritizing operational efficiency improvements over radical technological advancements. Stringent environmental regulations, particularly those targeting CO2 emissions, pose significant challenges, forcing companies to adopt cleaner production methods and potentially impacting profitability. The increasing competitiveness of substitute energy sources, such as natural gas and renewables, further complicates the market landscape. End-user segmentation primarily comprises electricity generation, steel production, and cement manufacturing, with a smaller "other applications" segment.

- Market Concentration: The Herfindahl-Hirschman Index (HHI) for the European coal market is estimated at [Insert Precise Figure] in 2025, indicating a moderately concentrated market. This suggests a level of market power held by a relatively small number of firms. Further analysis of the HHI over time can reveal shifts in market concentration.

- Innovation Drivers: Focus remains primarily on enhancing extraction efficiency and minimizing operational costs through process optimization and technological upgrades rather than major breakthroughs.

- Regulatory Impacts: Stringent environmental regulations, including carbon pricing mechanisms and emission limits, exert significant influence on production costs and investment decisions, creating a considerable barrier to entry and impacting overall profitability.

- Product Substitutes: Natural gas and renewables (wind, solar, hydro) represent major substitutes, steadily gaining market share due to falling costs and increasing policy support. This competitive pressure necessitates continuous adaptation from coal producers.

- End-User Segmentation: A projected breakdown for 2025 is as follows: Electricity generation (60%), Steel production (25%), Cement manufacturing (10%), Other applications (5%). These figures are estimates and may vary based on several factors. Detailed analysis of individual segments would provide a more granular understanding.

- M&A Trends: Ongoing consolidation is expected, driven by the pursuit of economies of scale and the imperative to navigate increasingly complex regulatory and competitive landscapes. This creates opportunities for larger firms but can also raise antitrust concerns.

Europe Coal Industry Market Trends & Opportunities

The European coal market is experiencing a complex interplay of declining demand and persistent supply-side challenges. While the overall market size shows a decreasing trend, the CAGR for the forecast period (2025-2033) is projected at -xx%, reflecting a gradual contraction. This is primarily driven by the increasing adoption of renewable energy sources and stricter environmental regulations across Europe. However, certain niche segments, particularly those catering to specific industrial applications where coal remains a competitive fuel source, may exhibit limited growth. The market penetration rate of coal in electricity generation is expected to decline further, while its role in steel and cement production remains more resilient, although facing growing pressure from alternative technologies. Technological shifts are limited, focusing on marginal efficiency improvements in mining and processing. Consumer preferences, influenced by growing environmental awareness, are shifting towards decarbonized energy solutions, putting downward pressure on coal consumption. Competitive dynamics are shaped by the ongoing transition to cleaner energy sources, increasing competition from renewable energy companies, and regulatory hurdles.

Dominant Markets & Segments in Europe Coal Industry

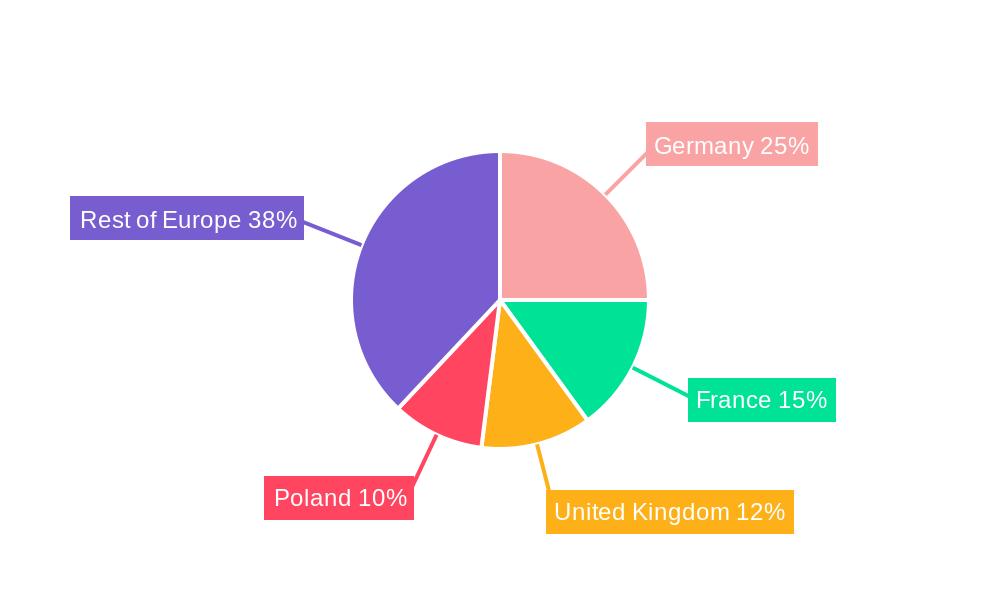

Germany retains its position as the dominant European coal market, followed by Poland and the Czech Republic. Lignite constitutes the largest market share among coal types, owing to its abundant reserves and historical reliance in electricity generation. Bituminous coal maintains its importance in the steel and cement industries. The regional distribution reflects historical patterns of energy production and infrastructure development.

- Leading Region: Germany, benefiting from substantial lignite reserves and existing infrastructure.

- Leading Coal Type: Lignite, driven by its cost-effectiveness and abundant reserves, particularly in Germany. However, this dominance is challenged by environmental regulations and renewable energy transition.

- Leading Application: Electricity generation, accounting for the most significant portion of coal consumption. This is gradually changing with the push for renewable energy sources.

Key Growth Drivers (with caveats):

- Existing infrastructure: Established power plants and industrial facilities reliant on coal represent a significant sunk cost, creating inertia and slowing the transition to alternative fuels.

- Policy support (limited and declining): While overall policy leans towards decarbonization, some sectors continue to rely on coal, especially during the transition period. This support is often subject to political and economic factors.

- Price competitiveness (in specific segments and contexts): Coal remains price-competitive in certain industrial applications and specific market conditions, particularly when considering the cost of energy transition and intermittent nature of renewables.

Detailed Analysis: Germany's lignite dominance is inextricably linked to its extensive reserves and pre-existing infrastructure. Despite the significant shift towards renewable energy, the phase-out is gradual, ensuring lignite’s continued role in the energy mix for the foreseeable future. A similar pattern, albeit with varying degrees of coal dependence, is observed in other European nations. The pace of transition varies significantly across regions and is influenced by factors including energy security concerns, political will, and the economic feasibility of alternative energy sources.

Europe Coal Industry Product Analysis

Current product innovations within the European coal industry concentrate on enhancing extraction and processing efficiency to reduce costs and lessen environmental impact. This involves the adoption of advanced mining technologies, streamlined logistics, and the implementation of cleaner coal technologies (though limited in scale and impact). Technological advancements are predominantly incremental, adapting existing technologies rather than introducing revolutionary innovations. Competitive advantage significantly hinges on cost efficiency and access to reliable, cost-effective reserves, with a growing emphasis on environmental performance metrics.

Key Drivers, Barriers & Challenges in Europe Coal Industry

Key Drivers:

- Continued demand from specific industrial applications (steel, cement), especially in developing countries.

- Reliability and affordability compared to intermittent renewable sources in certain contexts.

Key Barriers & Challenges:

- Stringent environmental regulations (EU ETS, national regulations) leading to increased production costs and potential plant closures.

- Growing competition from renewable energy sources and natural gas.

- Supply chain vulnerabilities due to geopolitical factors and infrastructure limitations. Recent geopolitical events have highlighted this fragility, potentially impacting the cost and availability of coal.

Growth Drivers in the Europe Coal Industry Market

The limited growth drivers are primarily tied to the continued need for energy in specific industries. Existing infrastructure dependent on coal and its relatively stable pricing in some niches compared to fluctuating renewables support its presence.

Challenges Impacting Europe Coal Industry Growth

Significant regulatory hurdles, encompassing carbon pricing mechanisms, stringent emission limits, and broader environmental regulations, present substantial headwinds for the coal industry. Supply chain disruptions, amplified by geopolitical instability, and intense competition from less expensive and cleaner energy sources pose major threats to the industry's long-term viability and sustainability. The industry faces a period of significant transformation.

Key Players Shaping the Europe Coal Industry Market

- Jastrzębska Spółka Węglowa SA

- Suek AG

- Siberian Coal Energy Company

- UK Kuzbassrazrezugol OAO

- Lubelski Wegiel Bogdanka SA

- Mechel PAO

- Raspadskaya PAO

- Mitteldeutsche Braunkohlengesellschaft mbH (MIBRAG)

- Severstal PAO

Significant Europe Coal Industry Industry Milestones

- October 2022: Agreement to expand Garzweiler lignite mine in Germany, impacting 280 Million metric tons of lignite extraction by 2030. This highlights the continued investment in lignite despite the overall trend towards renewable energy.

- August 2022: Reactivation of the Heyden coal power plant in Germany (875 MW capacity). This demonstrates a short-term reliance on coal due to energy security concerns.

Future Outlook for Europe Coal Industry Market

The future outlook for the European coal industry is characterized by a gradual decline. While certain industrial applications will continue to require coal for the near future, the long-term trend is clear. Stricter environmental regulations and the increasing competitiveness of renewable energies will drive a continuous reduction in coal's share of the energy mix. Opportunities for coal companies may lie in niche applications and carbon capture technologies, but substantial growth is unlikely. The focus for many coal companies will shift towards diversification into other energy sectors and adaptation to the changing energy landscape.

Europe Coal Industry Segmentation

-

1. Type

- 1.1. Anthracite

- 1.2. Bituminous

- 1.3. Sub-Bituminous

- 1.4. Lignite

-

2. Application

- 2.1. Electricity

- 2.2. Steel

- 2.3. Cement

- 2.4. Other Applications

Europe Coal Industry Segmentation By Geography

- 1. Russia

- 2. Germany

- 3. Poland

- 4. Rest of Europe

Europe Coal Industry Regional Market Share

Geographic Coverage of Europe Coal Industry

Europe Coal Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 1.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Anthracite

- 5.1.2. Bituminous

- 5.1.3. Sub-Bituminous

- 5.1.4. Lignite

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Electricity

- 5.2.2. Steel

- 5.2.3. Cement

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Russia

- 5.3.2. Germany

- 5.3.3. Poland

- 5.3.4. Rest of Europe

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Europe Coal Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Anthracite

- 6.1.2. Bituminous

- 6.1.3. Sub-Bituminous

- 6.1.4. Lignite

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Electricity

- 6.2.2. Steel

- 6.2.3. Cement

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Russia Europe Coal Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Anthracite

- 7.1.2. Bituminous

- 7.1.3. Sub-Bituminous

- 7.1.4. Lignite

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Electricity

- 7.2.2. Steel

- 7.2.3. Cement

- 7.2.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Germany Europe Coal Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Anthracite

- 8.1.2. Bituminous

- 8.1.3. Sub-Bituminous

- 8.1.4. Lignite

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Electricity

- 8.2.2. Steel

- 8.2.3. Cement

- 8.2.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Poland Europe Coal Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Anthracite

- 9.1.2. Bituminous

- 9.1.3. Sub-Bituminous

- 9.1.4. Lignite

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Electricity

- 9.2.2. Steel

- 9.2.3. Cement

- 9.2.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Rest of Europe Europe Coal Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Anthracite

- 10.1.2. Bituminous

- 10.1.3. Sub-Bituminous

- 10.1.4. Lignite

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Electricity

- 10.2.2. Steel

- 10.2.3. Cement

- 10.2.4. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Company Profiles

- 11.1.1 Jastrzębska Spółka Węglowa SA

- 11.1.1.1. Company Overview

- 11.1.1.2. Products

- 11.1.1.3. Company Financials

- 11.1.1.4. SWOT Analysis

- 11.1.2 Suek AG

- 11.1.2.1. Company Overview

- 11.1.2.2. Products

- 11.1.2.3. Company Financials

- 11.1.2.4. SWOT Analysis

- 11.1.3 Siberian Coal Energy Company

- 11.1.3.1. Company Overview

- 11.1.3.2. Products

- 11.1.3.3. Company Financials

- 11.1.3.4. SWOT Analysis

- 11.1.4 UK Kuzbassrazrezugol OAO

- 11.1.4.1. Company Overview

- 11.1.4.2. Products

- 11.1.4.3. Company Financials

- 11.1.4.4. SWOT Analysis

- 11.1.5 Lubelski Wegiel Bogdanka SA

- 11.1.5.1. Company Overview

- 11.1.5.2. Products

- 11.1.5.3. Company Financials

- 11.1.5.4. SWOT Analysis

- 11.1.6 Mechel PAO

- 11.1.6.1. Company Overview

- 11.1.6.2. Products

- 11.1.6.3. Company Financials

- 11.1.6.4. SWOT Analysis

- 11.1.7 Raspadskaya PAO*List Not Exhaustive

- 11.1.7.1. Company Overview

- 11.1.7.2. Products

- 11.1.7.3. Company Financials

- 11.1.7.4. SWOT Analysis

- 11.1.8 Mitteldeutsche Braunkohlengesellschaft mbH (MIBRAG)

- 11.1.8.1. Company Overview

- 11.1.8.2. Products

- 11.1.8.3. Company Financials

- 11.1.8.4. SWOT Analysis

- 11.1.9 Severstal PAO

- 11.1.9.1. Company Overview

- 11.1.9.2. Products

- 11.1.9.3. Company Financials

- 11.1.9.4. SWOT Analysis

- 11.1.1 Jastrzębska Spółka Węglowa SA

- 11.2. Market Entropy

- 11.2.1 Company's Key Areas Served

- 11.2.2 Recent Developments

- 11.3. Company Market Share Analysis 2025

- 11.3.1 Top 5 Companies Market Share Analysis

- 11.3.2 Top 3 Companies Market Share Analysis

- 11.4. List of Potential Customers

- 12. Research Methodology

List of Figures

- Figure 1: Europe Coal Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: Europe Coal Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 2: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 3: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 4: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 5: Europe Coal Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 6: Europe Coal Industry Volume K Tons Forecast, by Region 2020 & 2033

- Table 7: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 8: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 9: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 10: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 11: Europe Coal Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: Europe Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 13: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 14: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 15: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 16: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 17: Europe Coal Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 18: Europe Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 19: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 20: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 21: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 22: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 23: Europe Coal Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Europe Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

- Table 25: Europe Coal Industry Revenue billion Forecast, by Type 2020 & 2033

- Table 26: Europe Coal Industry Volume K Tons Forecast, by Type 2020 & 2033

- Table 27: Europe Coal Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 28: Europe Coal Industry Volume K Tons Forecast, by Application 2020 & 2033

- Table 29: Europe Coal Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 30: Europe Coal Industry Volume K Tons Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Coal Industry?

The projected CAGR is approximately 1.9%.

2. Which companies are prominent players in the Europe Coal Industry?

Key companies in the market include Jastrzębska Spółka Węglowa SA, Suek AG, Siberian Coal Energy Company, UK Kuzbassrazrezugol OAO, Lubelski Wegiel Bogdanka SA, Mechel PAO, Raspadskaya PAO*List Not Exhaustive, Mitteldeutsche Braunkohlengesellschaft mbH (MIBRAG), Severstal PAO.

3. What are the main segments of the Europe Coal Industry?

The market segments include Type, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 42.6 billion as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Renewable Energy Installations 4.; Energy Infrastructure Development.

6. What are the notable trends driving market growth?

Electricity Sector to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Political and Economic Instability.

8. Can you provide examples of recent developments in the market?

October 2022: The German government has an agreement with a German multinational energy company that plans to expand the Garzweiler coal mine over Lutzerath village. The company plans to extract 280 million metric tons of lignite by 2030.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion and volume, measured in K Tons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Coal Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Coal Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Coal Industry?

To stay informed about further developments, trends, and reports in the Europe Coal Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence