Key Insights

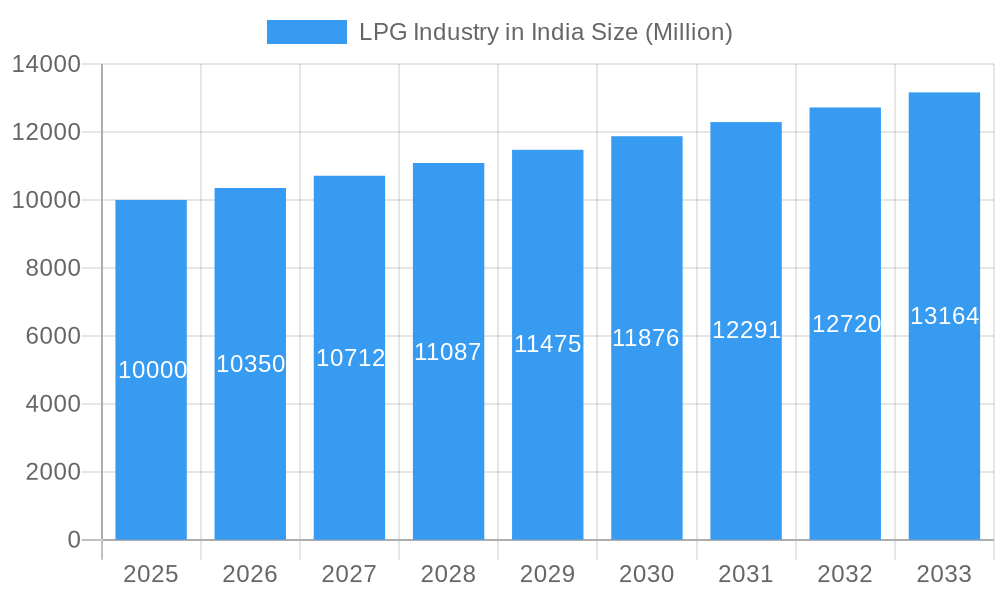

The Indian LPG market is projected to reach $136.548 billion by 2025, with a Compound Annual Growth Rate (CAGR) of 4.71%. This growth is driven by increasing urbanization, rising disposable incomes, and the expanding industrial sector's demand for cleaner energy solutions. Government initiatives promoting cleaner cooking fuels and reducing reliance on traditional biomass are significant catalysts. Key challenges include fluctuating crude oil prices and the need for robust rural distribution infrastructure. The market is segmented by source (crude oil, natural gas liquids) and application (residential & commercial, industrial, automotive fuels, others). Major players like Indian Oil Corporation, Bharat Petroleum, HPCL, and Reliance Industries compete on price, distribution efficiency, and brand recognition. Regional consumption varies across North, South, East, and West India. Strategic investments in infrastructure and technology, alongside continued government support, will be crucial for sustained growth through 2033.

LPG Industry in India Market Size (In Billion)

The competitive landscape features established and emerging players focused on supply diversification, logistics optimization, and innovative marketing. Development of new LPG infrastructure, including pipelines and storage, is vital to meet growing demand, particularly in underserved regions. The increasing emphasis on environmental sustainability is expected to drive the adoption of cleaner LPG technologies. Market evolution will be influenced by government regulations on fuel subsidies, renewable energy adoption, and growing environmental awareness. The forecast period (2025-2033) anticipates continued moderate growth, contingent on effectively addressing market challenges and capitalizing on opportunities.

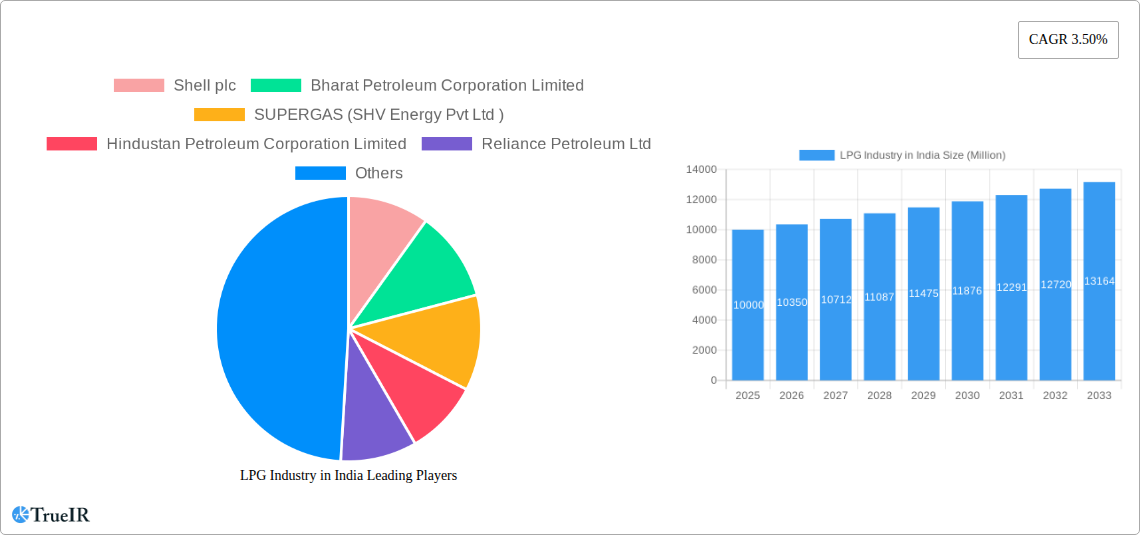

LPG Industry in India Company Market Share

LPG Industry in India: A Comprehensive Market Report (2019-2033)

This dynamic report provides a detailed analysis of the LPG industry in India, encompassing market structure, competitive landscape, trends, opportunities, and future outlook. Leveraging extensive data from 2019-2024 (Historical Period), with a base year of 2025 and a forecast period extending to 2033, this report is an indispensable resource for industry stakeholders, investors, and strategic planners. The report utilizes high-volume keywords to ensure maximum search engine visibility and engagement.

LPG Industry in India Market Structure & Competitive Landscape

The Indian LPG market is characterized by a moderately concentrated structure, with a few major players holding significant market share. While exact concentration ratios require proprietary data, it's estimated that the top five players control approximately xx% of the market in 2025. Innovation is driven primarily by efficiency improvements in production, distribution, and cylinder technology, as well as efforts to reduce carbon emissions. Regulatory changes, particularly those related to safety and pricing, significantly impact market dynamics. The primary product substitutes are PNG and electricity, particularly in the residential and commercial segments. The market is segmented by application into residential & commercial, industrial, autofuels, and other applications. M&A activity has been relatively limited in recent years, with only xx major transactions recorded between 2019 and 2024, primarily focused on smaller players consolidating their operations.

- Market Concentration: Estimated top 5 players control xx% of the market in 2025.

- Innovation Drivers: Efficiency improvements, emission reduction technologies, and cylinder technology advancements.

- Regulatory Impacts: Significant influence on pricing, safety standards, and market access.

- Product Substitutes: PNG and electricity, posing competitive pressure.

- End-User Segmentation: Residential & Commercial, Industrial, Autofuels, Other Applications.

- M&A Trends: Limited activity in recent years, with xx major transactions (2019-2024).

LPG Industry in India Market Trends & Opportunities

The Indian LPG market exhibits robust growth, driven by rising disposable incomes, expanding urbanization, and increasing demand across all segments. The market size is projected to reach approximately XX Million USD in 2025, with a CAGR of xx% during the forecast period (2025-2033). Technological shifts towards digitalization in distribution and supply chain management are enhancing efficiency and transparency. Consumer preferences are increasingly focused on safety, convenience, and environmentally friendly options. Competitive dynamics are shaped by price wars, product differentiation, and expansion strategies. Market penetration remains high in urban areas, but there's significant growth potential in rural regions. This expansion is fueled by government initiatives aimed at expanding LPG access in underserved areas.

Dominant Markets & Segments in LPG Industry in India

The residential & commercial segment dominates the Indian LPG market, accounting for approximately xx% of total consumption in 2025. Growth in this segment is primarily driven by the rising middle class and increasing preference for convenient and clean cooking fuel. The industrial segment also displays consistent growth, driven by the expansion of various manufacturing industries. The Autofuels segment has witnessed a decline owing to the rise of CNG vehicles, yet still retains a significant presence in certain areas.

- Key Growth Drivers (Residential & Commercial): Rising disposable incomes, urbanization, and government subsidies.

- Key Growth Drivers (Industrial): Growth in manufacturing and industrial activities.

- Key Growth Drivers (Autofuels): Presence in regions with limited access to CNG.

- Source of Production: Natural gas liquids have seen a relative increase in usage compared to crude oil due to improved efficiency and cost-effectiveness, although crude oil still makes up a larger component.

LPG Industry in India Product Analysis

Product innovation in the Indian LPG market focuses on enhancing safety features, improving cylinder design, and developing more efficient distribution systems. Competitive advantages are derived from efficient supply chains, cost-effective pricing, and superior customer service. Technological advancements involve the implementation of smart meters and digital platforms for improved tracking and management of LPG distribution. These advancements enhance transparency and security and are gaining traction within the market.

Key Drivers, Barriers & Challenges in LPG Industry in India

Key Drivers: Increasing demand from residential and commercial sectors, government initiatives promoting LPG usage, and investments in infrastructure development.

Challenges: Supply chain disruptions, volatile global crude oil prices (impact on prices xx%), stringent safety regulations, and intense competition from substitutes (e.g., PNG, electricity) resulting in a price sensitive market.

Growth Drivers in the LPG Industry in India Market

Continued urbanization, government initiatives aimed at expanding LPG access to rural areas, and rising disposable incomes are pivotal growth drivers. Technological advancements in LPG delivery and distribution systems also contribute significantly.

Challenges Impacting LPG Industry in India Growth

Fluctuations in international crude oil prices directly impact LPG prices and profitability. Stringent safety regulations necessitate significant investments in infrastructure and safety measures. Competition from alternative fuels such as PNG and electricity also presents challenges.

Key Players Shaping the LPG Industry in India Market

- Shell plc

- Bharat Petroleum Corporation Limited

- SUPERGAS (SHV Energy Pvt Ltd)

- Hindustan Petroleum Corporation Limited

- Reliance Petroleum Ltd

- TotalEnergies SE

- Indian Oil Corporation Ltd

- Eastern Gases Lt

- Jyothi Gas Pvt Ltd

Significant LPG Industry in India Industry Milestones

- February 2022: Indian Oil Corp (IOC) announced plans to construct three new plants in Northeast India, increasing LPG bottling capacity by 53% (to 8 crore cylinders annually by 2030). Investment: INR 325-350 crore.

Future Outlook for LPG Industry in India Market

The Indian LPG market is poised for continued growth, driven by robust demand, government support, and technological innovation. Strategic opportunities lie in expanding distribution networks in rural areas, enhancing digitalization, and exploring sustainable and environmentally friendly LPG solutions. The market potential is substantial, promising significant returns for investors and stakeholders in the coming decade.

LPG Industry in India Segmentation

-

1. Source of Production

- 1.1. Crude Oil

- 1.2. Natural Gas Liquids

-

2. Application

- 2.1. Residential & Commercial

- 2.2. Industrial

- 2.3. Autofuels

- 2.4. Other Applications

LPG Industry in India Segmentation By Geography

-

1. Asia Pacific

- 1.1. India

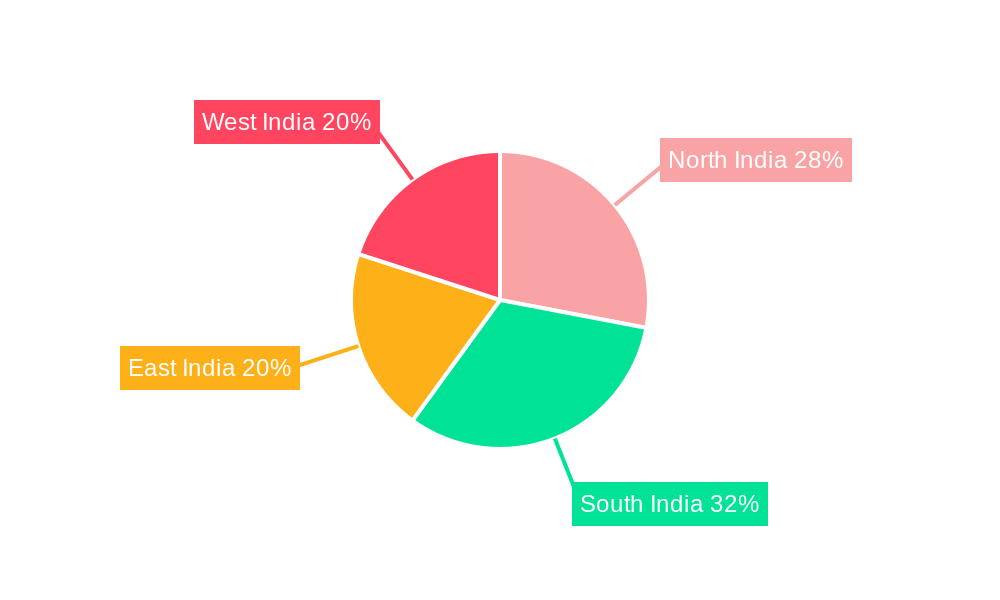

LPG Industry in India Regional Market Share

Geographic Coverage of LPG Industry in India

LPG Industry in India REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.71% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. TIR Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Source of Production

- 5.1.1. Crude Oil

- 5.1.2. Natural Gas Liquids

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Residential & Commercial

- 5.2.2. Industrial

- 5.2.3. Autofuels

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Source of Production

- 6. Global LPG Industry in India Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Source of Production

- 6.1.1. Crude Oil

- 6.1.2. Natural Gas Liquids

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Residential & Commercial

- 6.2.2. Industrial

- 6.2.3. Autofuels

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Source of Production

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Shell plc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Bharat Petroleum Corporation Limited

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 SUPERGAS (SHV Energy Pvt Ltd )

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Hindustan Petroleum Corporation Limited

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Reliance Petroleum Ltd

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 TotalEnergies SE

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Indian Oil Corporation Ltd

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Eastern Gases Lt

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Jyothi Gas Pvt Ltd

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Shell plc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Global LPG Industry in India Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific LPG Industry in India Revenue (billion), by Source of Production 2025 & 2033

- Figure 3: Asia Pacific LPG Industry in India Revenue Share (%), by Source of Production 2025 & 2033

- Figure 4: Asia Pacific LPG Industry in India Revenue (billion), by Application 2025 & 2033

- Figure 5: Asia Pacific LPG Industry in India Revenue Share (%), by Application 2025 & 2033

- Figure 6: Asia Pacific LPG Industry in India Revenue (billion), by Country 2025 & 2033

- Figure 7: Asia Pacific LPG Industry in India Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global LPG Industry in India Revenue billion Forecast, by Source of Production 2020 & 2033

- Table 2: Global LPG Industry in India Revenue billion Forecast, by Application 2020 & 2033

- Table 3: Global LPG Industry in India Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global LPG Industry in India Revenue billion Forecast, by Source of Production 2020 & 2033

- Table 5: Global LPG Industry in India Revenue billion Forecast, by Application 2020 & 2033

- Table 6: Global LPG Industry in India Revenue billion Forecast, by Country 2020 & 2033

- Table 7: India LPG Industry in India Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the LPG Industry in India?

The projected CAGR is approximately 4.71%.

2. Which companies are prominent players in the LPG Industry in India?

Key companies in the market include Shell plc, Bharat Petroleum Corporation Limited, SUPERGAS (SHV Energy Pvt Ltd ), Hindustan Petroleum Corporation Limited, Reliance Petroleum Ltd, TotalEnergies SE, Indian Oil Corporation Ltd, Eastern Gases Lt, Jyothi Gas Pvt Ltd.

3. What are the main segments of the LPG Industry in India?

The market segments include Source of Production, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 136.548 billion as of 2022.

5. What are some drivers contributing to market growth?

Declining Cost of Wind Energy. Increasing Investments in Wind Energy Power Generation Projects.

6. What are the notable trends driving market growth?

LPG Extracted From Natural Gas is Expected to Have Considerable Growth Rate.

7. Are there any restraints impacting market growth?

Increasing Adoption of Alternate Clean Power Sources.

8. Can you provide examples of recent developments in the market?

In February 2022, Indian Oil Corp (IOC) announced the plans to construct three new plants in Northeast India to increase its LPG bottling capacity by nearly 53% or to 8 crore cylinders annually by 2030, to meet the growing demand in the region. Furthermore, the total investment in the plant expansion is likely to range between INR 325-350 crore.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "LPG Industry in India," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the LPG Industry in India report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the LPG Industry in India?

To stay informed about further developments, trends, and reports in the LPG Industry in India, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence